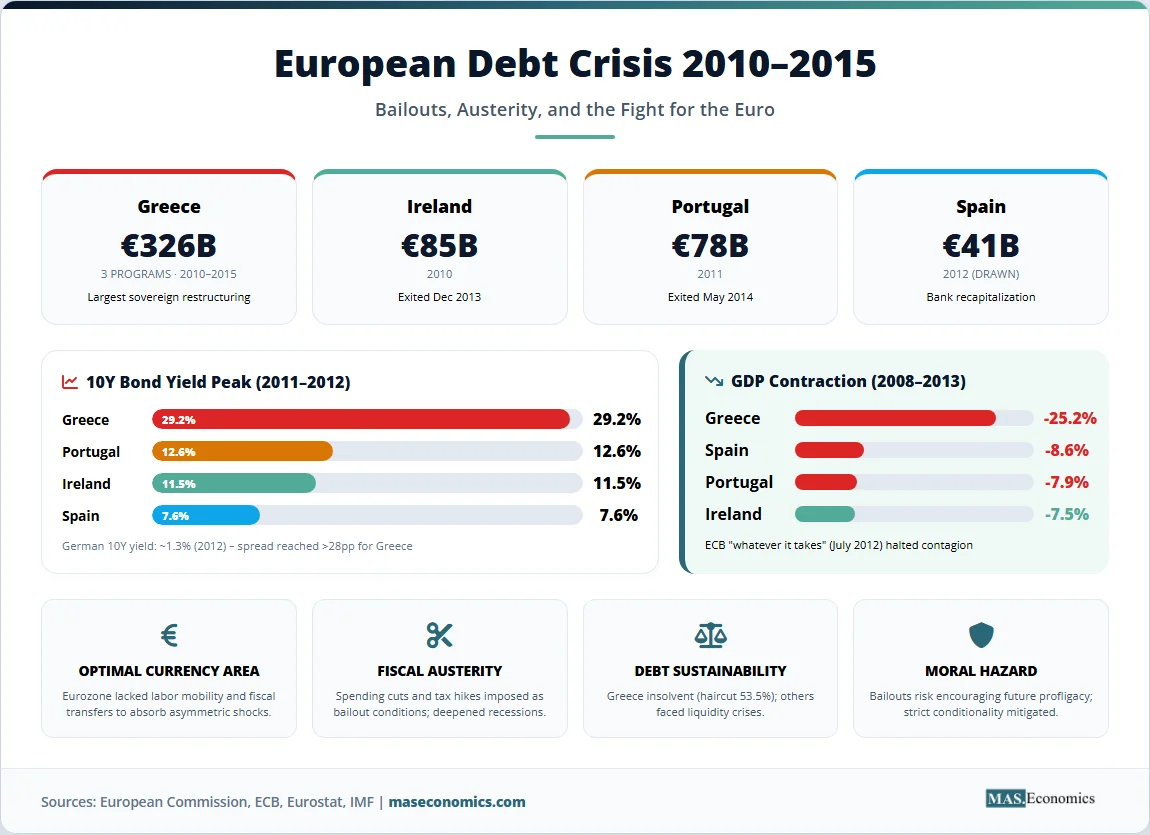

In 2010, Greece was told to cut pensions, slash public sector wages, and raise taxes in exchange for a €110 billion bailout from the European Union and the International Monetary Fund. By 2013, Spain’s unemployment rate had climbed to 27% according to Eurostat data, the highest in the eurozone, with over six million people out of work. Italy’s public debt exceeded 130% of GDP, second only to Greece, raising fears that the eurozone’s third-largest economy might be too big to bail out. The European debt crisis explained how a currency union designed to promote stability and prosperity could instead amplify financial contagion and test the limits of political solidarity.

The crisis forced the eurozone to create permanent rescue mechanisms, fundamentally alter the role of the European Central Bank, and impose harsh austerity programs that reshaped the social contract across southern Europe. Total rescue commitments reached €396 billion across Greece, Ireland, Portugal, Spain, and Cyprus, according to European Commission data on EU financial assistance programmes. The crisis exposed deep flaws in the architecture of the euro: a monetary union without a fiscal union, where member states shared a currency but not a common budget, debt instrument, or banking supervision framework. The question of whether the eurozone could survive such a fundamental asymmetry became the central economic and political challenge of the decade.

From Greek Revelation to Systemic Crisis

The European debt crisis began with a statistical revelation. In October 2009, Greece’s newly elected government announced that the country’s budget deficit for the year would reach 12.7% of GDP, more than double the previously reported 6%, a figure later revised upward to 15%. The admission shattered market confidence. Credit rating agencies downgraded Greek debt, and the interest rate the Greek government had to pay on its 10-year bonds soared from below 5% in late 2009 to above 8.5% by April 2010, making it unsustainable for Greece to borrow on commercial markets.

Greece’s problems were not unique. The 2008 global financial crisis had exposed similar vulnerabilities across the eurozone periphery: Ireland’s property bubble had burst, forcing the government to guarantee bank liabilities that overwhelmed public finances; Portugal’s weak growth and high private debt made it vulnerable to shifts in investor sentiment; Spain’s housing collapse left its banks with enormous losses on real estate loans. Italy, with a debt-to-GDP ratio exceeding 120%, faced refinancing needs that could overwhelm the eurozone’s rescue capacity. Financial markets began to treat these countries not as individual cases but as a single asset class: “peripheral” eurozone debt, all vulnerable to the same forces.

Contagion spread through multiple channels. When Greece’s borrowing costs rose, investors reassessed the risk of all eurozone sovereign debt, driving up yields for Portugal, Ireland, and eventually Spain and Italy. By mid-2011, the risk premium over German yields for distressed sovereigns exceeded 10 percentage points, and the spreads paid by Spain and Italy threatened to spiral out of control until the ECB’s decisive intervention in September 2012. The Mundell-Fleming model helps explain why countries that had surrendered monetary policy autonomy were particularly vulnerable: with exchange rates fixed within the eurozone and no independent monetary policy, the only adjustment mechanisms were fiscal austerity and internal devaluation, falling wages and prices relative to trading partners.

Timeline: Key Events of the European Debt Crisis

| Date | Event | Economic Significance |

|---|---|---|

| October 2009 | Greece reveals deficit is 12.7% of GDP, later revised to 15% | Triggers loss of market confidence; bond yields surge. |

| May 2010 | First Greek bailout (€110 billion) approved | First eurozone bailout; conditional on severe austerity. |

| November 2010 | Ireland receives €85 billion bailout | Banking crisis overwhelms public finances. |

| May 2011 | Portugal receives €78 billion bailout | Third eurozone country locked out of bond markets. |

| February 2012 | Second Greek bailout (€130 billion) and debt restructuring | Largest sovereign debt restructuring in history; private creditors take 53.5% haircut. |

| July 2012 | Spain receives €100 billion for bank recapitalization | Crisis spreads to major eurozone economy; ECB announces “whatever it takes.” |

| September 2012 | ECB announces Outright Monetary Transactions (OMT) program | Market panic subsides; peripheral bond yields fall sharply. |

| October 2012 | European Stability Mechanism (ESM) launched | Permanent eurozone bailout fund with €500 billion lending capacity. |

| 2013–2014 | Ireland, Portugal, and Spain exit bailout programs | Return to market financing; austerity eases. |

| July 2015 | Third Greek bailout (€86 billion) agreed after referendum | Final crisis resolution; Greece remains in eurozone. |

|

||

The human toll was severe. Greece’s economy contracted by 25% between 2008 and 2015 according to Eurostat national accounts data, and unemployment reached 27%. Spain’s unemployment peaked at 27.2% in early 2013, with youth unemployment exceeding 56%. Portugal and Ireland also experienced deep recessions, though Ireland’s recovery was faster due to its more flexible economy and strong export sector. The crisis reshaped the political landscape: anti-austerity parties gained power in Greece (Syriza in 2015) and Spain (Podemos), while nationalist and eurosceptic movements strengthened across the continent.

Optimal Currency Area, Austerity, Debt Sustainability, and Moral Hazard

The European debt crisis can be understood through four interconnected economic concepts that illuminate why the eurozone was vulnerable and why resolving the crisis proved so difficult.

Optimal Currency Area: The Euro’s Design Flaw

The theory of optimal currency areas (OCA), developed by economist Robert Mundell, specifies the conditions under which a group of countries benefits from sharing a single currency. Key criteria include labor mobility, capital mobility, synchronized business cycles, and a system of fiscal transfers to cushion asymmetric shocks. The eurozone, as many economists warned before its creation, fell short on several counts. Labor mobility within Europe remained limited by language barriers and differing national labor market regulations. Business cycles across member states were not synchronized: Germany’s export-driven economy often diverged from the consumption-driven growth of southern Europe. Most critically, the eurozone lacked a centralized fiscal authority capable of transferring resources from booming regions to those in recession.

Research comparing the euro area to the United States finds that the U.S. remains closer to an optimum currency area than the eurozone. The eurozone’s vulnerability was exposed when asymmetric shocks, the sudden stop of capital flows to the periphery after 2008, could not be cushioned by exchange rate adjustment or fiscal transfers. Countries like Greece and Spain, which had experienced high inflation and loss of competitiveness during the euro’s first decade, could not devalue to regain export competitiveness. Instead, they were forced into painful internal devaluation: cutting wages and prices relative to their trading partners through prolonged recession. The limits of economic integration without corresponding political integration became starkly apparent.

Fiscal Austerity: The Policy Response and Its Critics

Austerity, sharp reductions in government spending and increases in taxes, was the core condition attached to all eurozone bailouts. The economic logic was straightforward: countries with unsustainable debt burdens had to reduce their deficits to restore market confidence and regain access to private capital markets. Greece’s first bailout required pension cuts, public sector wage reductions of 15%, and VAT increases. Spain implemented labor market reforms and public sector freezes. Ireland cut public sector pay and social welfare. Portugal raised taxes and reduced public investment.

The economic impact of austerity remains intensely debated. Proponents argue that fiscal consolidation was necessary to restore credibility and reduce borrowing costs. By 2014, Greece achieved a primary surplus (excluding interest payments) of 0.4% of GDP, and Ireland and Portugal successfully exited their bailout programs and returned to bond markets. Critics, including Nobel laureate Paul Krugman, contend that austerity during a recession was self-defeating: spending cuts reduced aggregate demand, deepening the recession and making debt-to-GDP ratios worse, not better. The fiscal policy contraction across the eurozone was estimated to have reduced GDP by 4-5% cumulatively in the periphery. The fiscal multiplier effect, the amount by which GDP falls for each euro of spending cuts, was likely higher than the IMF initially assumed, leading to deeper-than-forecast recessions.

Debt Sustainability: When Borrowing Becomes Unsustainable

Debt sustainability refers to a government’s ability to service its debt without an unrealistic adjustment to the primary budget balance. The crisis exposed the difference between liquidity problems (temporary inability to borrow) and solvency problems (fundamental inability to repay). Ireland and Spain entered the crisis with relatively low public debt; Ireland’s was 25% of GDP in 2007, but faced liquidity crises when markets panicked. Greece, by contrast, faced a solvency crisis: with debt exceeding 170% of GDP and an economy in freefall, full repayment was impossible.

The recognition of Greece’s insolvency led to the largest sovereign debt restructuring in history in 2012, when private creditors accepted a 53.5% write-down on the face value of their Greek bond holdings. Even this was insufficient, and Greece required a third bailout in 2015. The crisis demonstrated that debt sustainability depends not only on debt levels but on growth rates, interest rates, and the primary budget balance. The eurozone’s institutional response, the creation of the European Stability Mechanism with €500 billion in lending capacity, provided a permanent backstop for liquidity crises but could not resolve underlying solvency problems.

Moral Hazard: Bailouts and Future Behavior

Moral hazard arises when one party takes excessive risks because another party bears the cost of those risks. In the eurozone context, the availability of bailouts created a moral hazard problem: if countries believed they would be rescued, they might borrow excessively, and if investors believed they would be protected from losses, they might lend recklessly. The pre-crisis convergence of peripheral bond yields to German levels reflected this belief: markets priced Greek debt as nearly as safe as German debt, despite fundamental differences in fiscal positions.

The eurozone’s response tried to balance two competing objectives: preventing financial contagion that could destroy the currency union, while avoiding a permanent bailout guarantee that would encourage future profligacy. The “no bailout” clause in the EU treaties was effectively overridden by the reality that a Greek default could trigger a systemic crisis. The compromise was “strict conditionality”: bailouts were provided, but with harsh austerity and structural reform requirements intended to deter other countries from seeking assistance. The ECB’s OMT program, which promised unlimited bond purchases for countries that agreed to reform programs, represented a similar balance: a powerful backstop, but only for countries that submitted to external monitoring. The coordination of fiscal and monetary policy became the central challenge of crisis management.

Bond Yields and Economic Contraction

The chart below tracks 10-year government bond yields for Greece, Italy, Spain, and Germany from 2008 through 2015. The divergence between core (Germany) and periphery yields illustrates the crisis timeline: initial Greek stress in 2010, contagion to Italy and Spain in 2011-2012, and the decisive impact of Draghi’s “whatever it takes” commitment in July 2012, after which peripheral yields fell sharply.

Eurozone Government Bond Yields (10-Year, 2008–2015)

Sources: European Central Bank euro area yield curves; World Government Bonds historical data on Greek 10-year yields.

The second chart shows the cumulative GDP contraction during the crisis years (2008–2013) for the most affected countries. Greece’s 25% cumulative decline stands out as the deepest peacetime recession of any advanced economy in modern history. Spain, Portugal, and Ireland also experienced severe contractions, while Italy’s more moderate decline reflects its lower pre-crisis growth and smaller boom-bust cycle.

Cumulative GDP Contraction: Peak to Trough (2008–2013)

Sources: World Bank World Development Indicators on GDP growth; Eurostat national accounts data for cumulative GDP changes.

The following table summarizes the bailout packages provided to eurozone countries and their outcomes. The total committed funds exceeded €500 billion, though actual disbursements were lower as some programs were not fully drawn.

Eurozone Bailout Packages: Commitments and Outcomes

| Country | Bailout Amount | Year(s) | Outcome |

|---|---|---|---|

| Greece (first) | €110 billion | 2010 | Insufficient; second bailout required. |

| Ireland | €85 billion | 2010 | Exited program December 2013; strong recovery. |

| Portugal | €78 billion | 2011 | Exited program May 2014; moderate recovery. |

| Greece (second + PSI) | €130 billion + debt restructuring | 2012 | Largest sovereign debt restructuring in history. |

| Spain (bank recapitalization) | €100 billion (€41 billion drawn) | 2012 | Exited program January 2014; recovery underway. |

| Cyprus | €10 billion | 2013 | Exited program March 2016; first use of bail-in. |

| Greece (third) | €86 billion | 2015 | Exited program August 2018; last crisis resolution. |

|

|

|||

Sources: European Commission financial assistance programmes; European Stability Mechanism lending toolkit; IMF Greece country page.

Lessons and Takeaways

The European debt crisis offers four enduring lessons for currency unions and macroeconomic policy.

First, a monetary union without a fiscal union is fundamentally incomplete and vulnerable to asymmetric shocks. The eurozone’s inability to transfer resources from surplus to deficit regions forced adjustment entirely onto deficit countries through austerity and internal devaluation. The creation of the European Stability Mechanism and the ECB’s OMT program partially addressed this gap but did not create a genuine fiscal capacity at the eurozone level. The debate over a common eurozone budget, unemployment insurance scheme, or safe asset (eurobonds) continues.

Second, austerity during a deep recession may be self-defeating if fiscal multipliers are high. The IMF later acknowledged that it underestimated the size of fiscal multipliers in the eurozone periphery, leading to overly optimistic growth forecasts and deeper-than-expected recessions. The appropriate pace of fiscal consolidation remains contested, but the crisis demonstrated that attempting to reduce debt too quickly when monetary policy is constrained can backfire.

Third, central bank credibility can be a powerful stabilizing force. The ECB’s commitment to do “whatever it takes” to preserve the euro, backed by the OMT program, calmed financial markets without spending a single euro. This episode demonstrates that a central bank acting as lender of last resort for sovereign debt can break self-fulfilling panic spirals, provided its commitment is credible and its policy framework is clear.

Fourth, debt restructuring for insolvent sovereigns is inevitable but must be managed carefully to avoid systemic contagion. The delay in recognizing Greek insolvency prolonged the crisis and increased the eventual cost to taxpayers. The eurozone’s initial resistance to private sector involvement reflected fears of triggering a European “Lehman moment”, but when restructuring finally occurred in 2012, contagion was contained because the ECB had established a credible backstop. The role of central banking in crisis management was transformed by this experience.

MASEconomics Explains

Four economic concepts behind the European debt crisis

Conclusion

The European debt crisis explained the vulnerabilities inherent in a currency union built without fiscal and political integration. Greece’s budget deficit revelation triggered a systemic crisis that spread through financial contagion to Ireland, Portugal, Spain, and Italy. The eurozone’s response to bailouts, conditioned on austerity, the creation of permanent rescue mechanisms, and the ECB’s unprecedented commitment to act as lender of last resort, prevented the currency’s collapse but imposed severe economic and social costs. Spain’s unemployment hit 27%, Greece’s economy contracted by a quarter, and a generation of young Europeans faced lost opportunities. The crisis reshaped the eurozone’s institutional architecture. The lessons of 2010–2015 will shape European economic policy for decades to come.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.