A mortgage is a long-term loan secured by real property, in which the lender holds a lien on the home until the borrower repays the debt. If the borrower defaults, the lender can foreclose, take possession of the property, and sell it to recover the outstanding balance. That single piece of legal architecture, debt collateralised by the home itself, is what makes the Economics of Mortgages the most consequential corner of consumer finance, and arguably of the entire credit system.

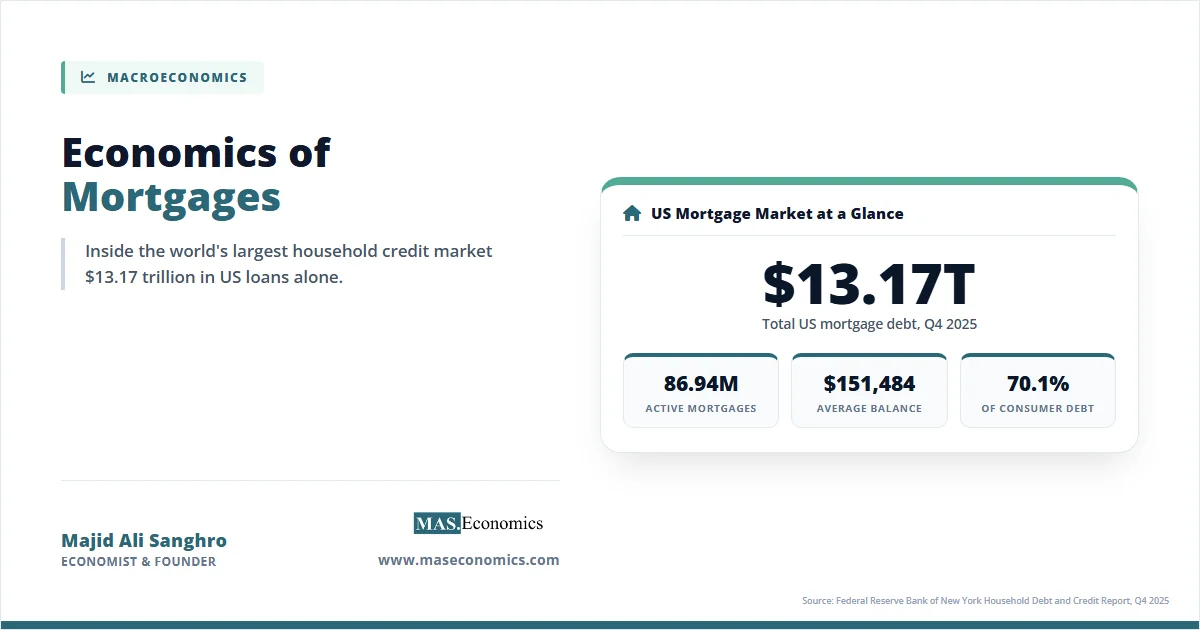

The scale is hard to grasp without numbers. According to the New York Fed’s Quarterly Report on Household Debt and Credit for Q4 2025, US mortgage debt outstanding stood at $13.17 trillion across 86.94 million accounts, with an average balance of $151,484. Mortgages alone accounted for 70.1% of total US household debt, larger than student loans, credit cards, and auto loans combined.

This article unpacks the mortgage market through four lenses: the contract structure that defines what the borrower owes, the funding chain that moves capital from savers to homebuyers, the market institutions (especially the US government-sponsored enterprises) that shape the system, and the macroeconomic role that makes housing the single most cyclically powerful asset class in the economy.

Table 1. The US Mortgage Market in Numbers (Q4 2025)

| Metric | Value | Source |

|---|---|---|

| Total mortgage debt outstanding | $13.17 trillion | NY Fed Household Debt Report Q4 2025 |

| Number of mortgage accounts | 86.94 million | NY Fed Household Debt Report Q4 2025 |

| Average balance per account | $151,484 | NY Fed Household Debt Report Q4 2025 |

| Mortgage share of US consumer debt | 70.1% | NY Fed Household Debt Report Q4 2025 |

| Q3 2025 originations | $512 billion | NY Fed Household Debt Report |

| New foreclosures in 2025 | 227,360 | NY Fed Consumer Credit Panel / Equifax |

| Seriously delinquent share (Q4 2025) | 0.92% | NY Fed Household Debt Report Q4 2025 |

| 30-year fixed rate (April 30, 2026) | 6.30% | Freddie Mac PMMS |

How It Works

Contract types

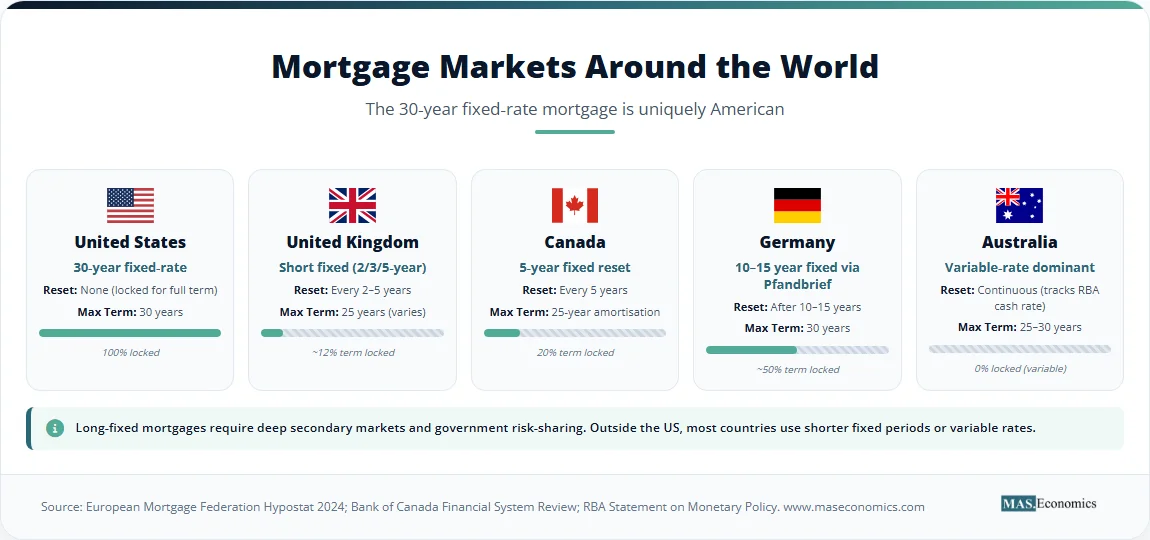

The mortgage you sign is one of several distinct contract structures. The four most common globally are:

- Fixed-rate mortgages. The rate is locked for the entire term. The 30-year fixed dominates the US market.

- Adjustable-rate mortgages (ARMs). The rate is fixed for an initial period (often 5, 7, or 10 years) and then resets periodically against a benchmark index.

- Interest-only mortgages. The borrower pays only interest for an initial period, then begins amortising principal.

- Balloon mortgages. Partial amortisation over the term with a large final lump-sum payment.

The 30-year fixed-rate mortgage is a US peculiarity. The UK uses 2 to 5-year fixed periods that reset to a variable rate. Canada uses 5-year fixed terms with mandatory refinancing. Germany finances long fixed terms (often 10 to 15 years) through Pfandbrief covered bonds, where the bank, rather than an external investor, bears the credit risk. No other major economy offers a 30-year locked rate as the default consumer product. Why the US does is a question we return to in Section 3.

Amortisation mathematics

Every fixed-rate mortgage payment is calculated using the same formula:

Where \(M\) is the monthly payment, \(P\) is the principal (loan amount), \(r\) is the monthly interest rate (annual rate divided by 12), and \(n\) is the total number of payments (years × 12).

To make this concrete: a $300,000 loan at 6.5% over 30 years gives \(r = 0.0054167\) and \(n = 360\), producing a monthly payment of $1,896. But that level payment hides a lopsided split. In the very first month, $1,625 of the $1,896 goes to interest and only $271 to principal. By the final year, those proportions are reversed.

This is the front-loading of amortisation, and it has real consequences. A homeowner who sells after five years has paid roughly $114,000 in mortgage payments but reduced the principal balance by less than $20,000. The rest went to the lender as interest. Over the full 30-year term, total interest paid on a $300,000 loan at 6.5% comes to roughly $382,000, more than the original principal.

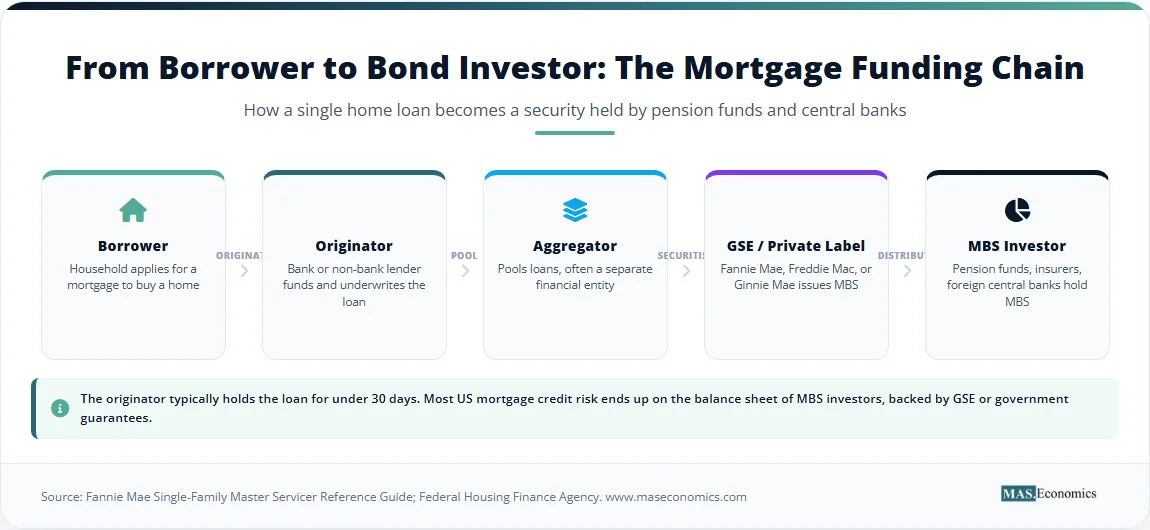

The funding chain

Most mortgage borrowers assume the bank that issued their loan still owns it. In the United States, that is rarely true. The modern US mortgage moves through a five-stage funding chain:

Borrower → Originator → Aggregator → GSE or Private-Label MBS Issuer → MBS Investor.

The originator (a bank, credit union, or non-bank lender like Rocket or UWM) underwrites the loan and funds it briefly on its own balance sheet. Within weeks, the loan is sold, often to an aggregator who bundles it with thousands of similar loans, then to one of the government-sponsored enterprises (Fannie Mae or Freddie Mac) or to a private-label issuer. The GSE wraps the pool with a credit guarantee and issues a mortgage-backed security that trades in the bond market. The ultimate holders are pension funds, insurance companies, banks, foreign central banks, and the Federal Reserve itself.

This separation of origination from credit risk is the defining structural feature of the post-1970 US mortgage market. It allows MBS investors who price duration risk against the deep Treasury bonds yield curve to fund 30-year fixed-rate loans that no individual bank would willingly hold. It also creates the asymmetric information problem that detonated in 2008: the originator underwriting the loan is not the entity bearing the credit risk.

Government guarantees

The US government’s footprint in the mortgage market is larger than most borrowers realise:

- FHA loans. Insured by the Federal Housing Administration, allow down payments as low as 3.5% for borrowers with weaker credit.

- VA loans. Guaranteed by the Department of Veterans Affairs, available to military veterans and active service members, often with zero down payment.

- Ginnie Mae. Issues MBS backed by FHA and VA loans, carrying the full faith and credit of the US government.

- Conforming loan limits. Set annually by the Federal Housing Finance Agency. Loans larger than the limit (called “jumbo” loans) cannot be sold to Fannie Mae or Freddie Mac and must be funded privately, typically at slightly higher rates.

The Mortgage Market in Practice

The 30-year fixed is a global outlier

Most countries simply do not offer a deep 30-year fixed-rate mortgage market. The reason is technical. A 30-year fixed-rate loan exposes the lender to two risks: that interest rates rise (and the lender is stuck earning a below-market rate) and that they fall (and the borrower refinances, ending the loan early). These risks are so severe that no commercial bank would willingly hold them at scale.

The US solves the problem by transferring both risks to capital markets. Fannie Mae and Freddie Mac buy conforming loans from originators, pool them, and issue pass-through MBS that distribute the cash flows, and the prepayment risk to a vast pool of bond investors. The depth of the US Treasury market gives MBS investors a clean reference curve to hedge against, and the GSEs’ guarantee removes credit risk from the equation. No other country has built that combination.

The UK, Canada, and Australia rely on shorter fixed-rate periods or floating-rate mortgages, transmitting policy rate changes to households quickly. Germany’s Pfandbrief covered-bond system permits long fixed terms but keeps the credit risk on the bank’s balance sheet, which is why German banks underwrite far more conservatively than US originators ever did.

The 2008 crisis was a credit-standards collapse

By 2006, the US originator-to-distributor model had reached its logical extreme. NINJA loans (no income, no job, no assets), low-doc and stated-income origination, teaser-rate ARMs that reset sharply higher after two years, and 100% loan-to-value financing had pushed underwriting standards to historic lows. Originators bore little risk because the loans were sold within weeks; rating agencies stamped pools investment-grade based on faulty assumptions about regional house-price correlations; investors bought MBS and CDOs they could not independently evaluate.

When house prices stopped rising in 2006 and began falling in 2007, the credit losses cascaded through the securitisation chain into bank balance sheets, money-market funds, and ultimately the global banking system. The full anatomy is covered in the 2008 financial crisis piece, but the regulatory response is essential context here. The Dodd-Frank Act introduced the ability-to-repay rule, requiring originators to verify a borrower’s capacity to make payments. The qualified mortgage definition created a safe-harbour standard that channelled most origination toward fully-documented, fully-amortising loans. Fannie Mae and Freddie Mac were placed in federal conservatorship in September 2008 and remain there in 2026.

The 2020–2024 rate cycle and the lock-in effect

The mortgage market of the 2020s has been shaped by one of the sharpest interest-rate cycles in postwar history. The 30-year fixed rate hit a record low of 2.65% in January 2021, driven by the Federal Reserve’s pandemic-era zero-rate policy. Two and a half years later, in October 2023, it peaked at 7.79% as the Fed raised rates aggressively to combat inflation. As of April 30, 2026, the rate stood at 6.30% per the Freddie Mac PMMS.

That swing produced a uniquely American friction: the lock-in effect. By industry estimates, roughly 60% of US mortgaged homeowners hold rates below 4%. For these households, selling the existing home and buying a new one at current rates would dramatically increase monthly payments, even on an identically priced property. A homeowner with a 3% rate trading up to a similar home at 6.30% can see monthly principal-and-interest payments rise by 50% or more.

The result is that millions of homeowners simply do not list their properties. Existing-home inventory has stayed historically tight through 2024 and 2025, propping up prices even as Federal Reserve rate decisions would normally cool demand. This is a canonical example of a macroeconomic friction generated by a contract structure, one that exists almost nowhere outside the United States.

Charts & Visuals

US 30-year fixed mortgage rates from Freddie Mac’s Primary Mortgage Market Survey. The rate hit a record low of 2.65% in January 2021 and peaked at 7.79% in October 2023 a swing of more than 5 percentage points in under three years. Source: Freddie Mac PMMS via FRED.

Limitations & Systemic Risks

The mortgage system has four structural weaknesses that policy has not fully resolved.

Concentrated systemic risk. Housing comprises roughly a quarter of US household wealth, and mortgage debt at $13.17 trillion is the single largest household liability category, 70.1% of all consumer debt as of Q4 2025. A nationwide house-price correction transmits through the financial system more powerfully than any other asset shock, because mortgage debt is collateralised by the very asset whose price is falling. That feedback loop has no equivalent in equity markets, where leverage is smaller, and collateral is less concentrated.

Securitisation’s information problem. Pooling and tranching mortgages can mask credit risk by transferring it to investors who cannot easily assess the quality of the underlying loans. The 2008 crisis was the case study; the qualified mortgage rule and ability-to-repay requirements are the partial response. But the basic asymmetry, the originator knows the borrower better than the investor does, is structural, not soluble.

The government guarantees moral hazard. Implicit and explicit guarantees on Fannie Mae, Freddie Mac, FHA, and VA loans subsidise mortgage credit but also create incentives for excessive risk-taking. Both GSEs have remained in conservatorship since 2008. Eighteen years on, no political consensus has emerged on how to release them without either losing the 30-year fixed rate or saddling taxpayers with explicit liability for trillions of dollars of MBS guarantees.

Affordability erosion. Median US house-price-to-income ratios are at multi-decade highs in 2026. Combined with elevated mortgage rates, the median first-time buyer cannot purchase a median home in many major metros. The lock-in effect has compounded the problem by suppressing existing-home supply. The deeper drivers of housing affordability are covered in our dedicated explainer, but they intersect directly with the mortgage market through the channel of monthly payment capacity.

MASEconomics Explains

Mortgage-Backed Security (MBS)

A fixed-income security whose cash flows come from a pool of mortgages. Investors receive the principal and interest payments made by the underlying borrowers, less servicing fees. Most US residential MBS are agency-issued by Fannie Mae, Freddie Mac, or Ginnie Mae and carry credit guarantees against borrower default. Private-label MBS, issued by banks without GSE backing, exist but are a much smaller market post-2008.

Loan-to-Value Ratio (LTV)

The ratio of the mortgage amount to the home’s appraised value. Conventional US mortgages typically require LTV at or below 80% to avoid private mortgage insurance; FHA loans permit LTV as high as 96.5%. LTV is the most-watched single risk indicator at origination because it determines how much of a price decline the lender can absorb before the borrower has negative equity and a financial incentive to default.

Amortisation

The schedule by which a loan’s principal is repaid over its term. In a fixed-rate 30-year mortgage, early payments are mostly interest, and late payments are mostly principal, a direct consequence of the constant-payment formula. Total interest paid over the life of the loan typically equals or exceeds the original principal, which is why early extra payments (which apply directly to principal) reduce total interest cost so dramatically.

Prepayment Risk

The risk that borrowers repay their mortgages early, typically by refinancing when rates fall or by selling the home. From the MBS investor’s perspective, prepayment shortens the security’s effective life and forces reinvestment of returned principal at lower rates. Pricing prepayment risk, modelling how borrowers behave under different rate scenarios, is the single most important technical problem in MBS valuation, and it is the reason MBS yields trade at a spread above Treasuries even when both are credit-risk-free.

Conclusion

The Economics of Mortgages sits at an unusual intersection: it is simultaneously the most personal financial decision most households ever make and the largest single channel by which household demand for shelter is connected to global capital markets. A retiree’s pension fund in Tokyo holds the agency MBS that funds a teacher’s home in Phoenix. A change in Federal Reserve policy ripples through the Treasury yield curve, into MBS spreads, and onto the rate sheet a borrower sees the next morning. A regional house-price correction in one country can, through securitisation chains, surface as losses on a balance sheet on the other side of the world.

The contract structure of the US 30-year fixed-rate mortgage is the product of seventy years of institutional engineering: the GSEs, the agency MBS market, the Treasury yield curve, and the federal guarantee architecture. It produces benefits no other country has replicated: payment certainty for the borrower, deep liquidity for the investor, transmission of monetary policy that is slow but consequential. It also produces frictions no other country experiences: the lock-in effect, the GSEs’ indefinite conservatorship, and the systemic risk concentrated in a single asset class. Understanding how those features fit together is what it means to understand the connective tissue between household housing demand and the global capital markets that finance it.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.