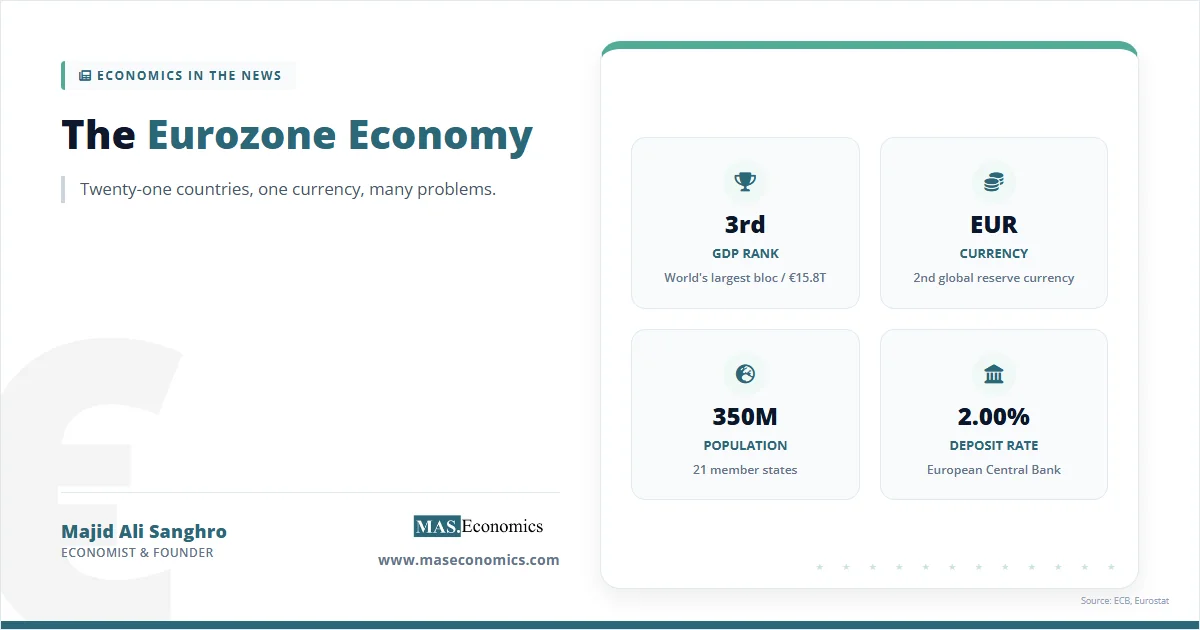

The Eurozone economy covers twenty-one countries, 350 million people, and roughly €15.8 trillion in annual output, making it the third-largest economic bloc in the world after the United States and China. Bulgaria became the twenty-first member on 1 January 2026, the first new entrant since Croatia joined in 2023. In nominal dollar terms, the bloc produces close to $17 trillion of goods and services each year and accounts for about one-seventh of global GDP.

The currency union has spent the last two decades stress-testing whether twenty-one different national economies can share a single monetary policy without sharing a single fiscal policy. The answer, recorded across the 2010-2012 sovereign debt crisis, the 2022-2023 energy shock, and the 2025-2026 trade and Middle East shocks, is “barely, and only with extensive central bank intervention.” Real GDP grew 1.4% in 2025 and is projected to slow to 0.9% in 2026 according to the March 2026 ECB staff projections, with annual headline inflation expected to rise to 2.6% as the war in the Middle East pushed energy prices higher.

Structure of the Eurozone Economy

The eurozone is the subset of the European Union that has adopted the euro as legal tender. Six EU members remain outside: Sweden, Czechia, Poland, Hungary, Romania, and Denmark, with the last operating a tight peg to the euro through ERM II. The non-Euro EU group accounts for the rest of the EU’s €17 trillion economy.

Inside the bloc, four countries do most of the work. Germany alone contributes roughly 29% of eurozone GDP, France 20%, Italy 14%, and Spain 11%. Together, these four economies make up about three-quarters of the bloc’s output. The remaining seventeen members range from the Netherlands and Belgium, both deeply industrialised, to Estonia and Malta, each smaller than many U.S. metropolitan areas.

Population density and demographics shape policy as much as output does. The bloc’s median age is now above 45, and the working-age population peaked around 2010. Germany’s working-age population has been shrinking since 2018, Italy’s since 2014. The labour market remains tight by historical standards, with unemployment at 6.2% in February 2026 according to the ECB, but the headline figure conceals a structural shortage of skilled workers in manufacturing, construction, and care services.

The euro itself is the second most-held reserve currency in the world after the U.S. dollar, accounting for roughly 20% of allocated global foreign exchange reserves. That share has been broadly stable since 2015, neither rising as the dollar’s share has slowly fallen, nor falling as the renminbi’s share has slowly risen. The euro’s reserve role gives the European Central Bank a unique seat among the world’s monetary authorities, and gives eurozone borrowers continued access to deep capital markets even when fiscal positions deteriorate.

Origins of the Euro

The euro was the answer to a problem that had defined European economics for forty years: small open economies tied together by trade kept devaluing their currencies against the Deutsche Mark, importing inflation from each other, and breaking apart every fixed exchange rate arrangement Europe attempted to build.

The 1957 Treaty of Rome created the European Economic Community and a customs union. The Werner Report of 1970 first proposed a monetary union but was killed by the collapse of Bretton Woods in 1971. The European Monetary System launched in 1979 with the Exchange Rate Mechanism, which fixed currencies in narrow bands around a central rate. The mechanism survived for fourteen years, then nearly collapsed in 1992 when George Soros and other speculators forced sterling and the lira out of the system in what came to be called Black Wednesday.

The lesson policymakers drew was that half-measures would not survive open capital markets. The 1992 Maastricht Treaty laid out a path to full monetary union, with five convergence criteria covering inflation, long-term interest rates, exchange rate stability, government deficits below 3% of GDP, and government debt below 60% of GDP. The euro launched as an accounting currency on 1 January 1999, with eleven founding members. Notes and coins entered circulation on 1 January 2002.

The first decade looked like a triumph. Peripheral countries borrowed at near-German interest rates. Construction boomed in Spain and Ireland. Greek government bond yields converged with Bunds. The architecture of the bloc, however, was incomplete. There was a single monetary policy but no banking union, no common deposit insurance, no fiscal transfer mechanism, and no lender of last resort for sovereign borrowers. When the 2008 financial crisis exposed Greek fiscal misreporting, the bloc had no playbook. The result was the European debt crisis, which pushed Greece, Ireland, Portugal, and Cyprus into bailout programmes between 2010 and 2013.

The crisis forced the missing institutions into being. The European Stability Mechanism was created in 2012 with €500 billion of firepower. ECB President Mario Draghi’s “whatever it takes” speech in July 2012 ended the acute phase by signalling that the central bank would buy peripheral sovereign bonds without limit if needed. Spreads on Italian, Spanish, and Portuguese debt collapsed within weeks of the speech. The Single Supervisory Mechanism in 2014 brought the largest 130 banks under direct ECB oversight, removing the cosy relationship between national supervisors and national banks that had let problems fester before 2010. The Single Resolution Mechanism was established in 2016, creating a framework to wind down failing banks without taxpayer bailouts.

Quantitative easing began in 2015 with the Public Sector Purchase Programme and continued, with breaks, until 2022. At its peak, the ECB balance sheet held close to €5 trillion of euro area government bonds, plus corporate, covered, and asset-backed securities. The pandemic emergency response in 2020 produced two new instruments. The Pandemic Emergency Purchase Programme committed €1.85 trillion of additional asset purchases. NextGenerationEU, agreed by EU leaders in July 2020 after a marathon negotiation, established an €800 billion recovery fund financed by joint EU borrowing, distributed largely as grants rather than loans, and managed at the European level. NextGenerationEU is the closest the bloc has come to true fiscal federalism, though it remains a one-off rather than a permanent stabiliser.

The 2022-2023 inflation surge tested the bloc again. Headline inflation hit 10.6% in October 2022, the highest since the euro was created. Energy prices, supply-chain disruption, and post-pandemic demand combined with the war in Ukraine to overwhelm the ECB’s inflation-targeting framework. The policy response was the fastest tightening in ECB history. Inflation fell back to the 2% target by mid-2024 without triggering a recession, an outcome that few forecasters predicted in late 2022. The 2025-2026 trade war and Middle East conflict have produced a fourth shock cycle, though so far less acute than the previous three.

Sectoral Composition of Output

Services account for roughly 73% of eurozone gross value added, industry for 20%, construction for 5%, and agriculture for under 2%. The high services share masks how much of the bloc’s identity, and its export earnings, still come from manufacturing.

Germany is the manufacturing core. Its automotive sector, machine tools, chemicals, and pharmaceuticals account for the bulk of the bloc’s industrial exports. Volkswagen, BMW, Mercedes-Benz, BASF, Siemens, and Bayer are the names that dominate global trade flows in their categories. Italy’s strength sits in mid-sized engineering firms, fashion, and food processing. France runs the bloc’s largest aerospace cluster through Airbus, plus a deep nuclear power industry and a luxury-goods sector that exports far above its GDP weight. The Netherlands hosts ASML, the only company in the world that produces extreme ultraviolet lithography machines for advanced semiconductor manufacturing, a fact that has placed Dutch trade policy at the centre of the U.S.-China chip dispute, as covered in the economics of the semiconductor industry.

The bloc imports nearly all the energy it consumes. Before 2022, Russia supplied roughly 40% of EU natural gas. After the invasion of Ukraine and the Nord Stream pipeline rupture, the share collapsed to under 15%. Liquefied natural gas from the United States and Qatar filled the gap, but at structurally higher prices. Energy import dependence is the single most important macroeconomic vulnerability of the bloc, and it has shaped every recession the eurozone has suffered since 1973. The 2022 spike in gas prices to over €300 per megawatt-hour pushed eurozone inflation to a peak of 10.6% in October 2022. The 2025-2026 Middle East war pushed prices back above €45 per megawatt-hour and added 0.5 to 0.7 percentage points to inflation projections.

Tourism is the other large hidden export. Spain alone receives more than 90 million international visitors a year, with tourism contributing close to 13% of Spanish GDP. France, Italy, Greece, and Portugal each rely on the sector for between 8% and 20% of national output. Tourism receipts substantially offset persistent goods trade deficits in southern member states.

The bloc’s industrial structure shows striking specialisation across countries. Spain has built a world-leading wind energy sector, with companies such as Iberdrola operating renewable assets across four continents. Ireland hosts the European headquarters of most major U.S. technology and pharmaceutical companies, an arrangement that has lifted Irish per capita GDP to among the world’s highest while distorting national output statistics through the activity of multinational corporations. Belgium and Luxembourg punch far above their population weight in financial services and EU institutional employment. Finland holds a quiet leadership in paper and pulp, plus surviving fragments of its mobile-handset cluster. The smaller central and eastern members, including Slovakia, Slovenia, and the Baltic states, have integrated deeply into German automotive and machine-tool supply chains, with Slovakia producing more cars per capita than any other country in the world.

Monetary and Fiscal Governance

The European Central Bank sets a single interest rate for the entire bloc. Its primary mandate is price stability, defined since 2021 as a symmetric 2% target over the medium term. This is the same mandate the Bundesbank operated under before 1999, transplanted onto a far larger and far more heterogeneous economy. The ECB has three main policy rates: the deposit facility rate, the main refinancing operations rate, and the marginal lending facility rate. The deposit rate is the operational instrument that markets watch.

The Governing Council meets every six weeks and votes on rate decisions. It has 26 members: six executive board members and the governors of all twenty-one national central banks. National central bank governors rotate voting rights under a system that gives Germany, France, Italy, Spain, and the Netherlands more frequent votes than smaller members, though all governors participate in every discussion. President Christine Lagarde, in her second four-year term until 2027, chairs the council and gives the post-meeting press conference that markets parse for signals.

From its launch through 2022, the ECB ran an extraordinary monetary policy regime. The deposit rate fell to -0.5% by 2014 and stayed negative for eight years, the longest sustained negative-rate experiment in monetary history. Quantitative easing accumulated a balance sheet of close to €9 trillion at its peak. The 2022-2024 inflation surge ended that regime. The deposit rate rose from -0.5% in July 2022 to 4.0% by September 2023, the fastest tightening cycle in ECB history. Cuts began in June 2024 and brought the rate to 2.0% by early 2026, where it has stayed through the Middle East shock. For a broader context on how the institution makes these decisions and how it compares to other major central banks, see the article on central bank divergence in 2026.

Fiscal policy remains national. The Stability and Growth Pact set the original 3% deficit and 60% debt rules from 1997, suspended during the pandemic, and replaced from 2024 by a reformed framework that focuses on country-specific medium-term plans. The new rules tolerate higher debt as long as governments commit to credible declining paths. Compliance is uneven. Eurostat data for end-2025 show that twelve of the twenty euro members had debt ratios above 60% of GDP, with Greece at 146.1%, Italy at 137.1%, and France at 115.6%. Eleven member states ran deficits at or above 3% of GDP, with France at -5.1% and Belgium at -5.2% the most exposed among major economies.

The bloc has no common Treasury. There is no eurobond and no permanent fiscal stabiliser. The closest substitutes are the European Stability Mechanism, which can lend to governments in distress, and NextGenerationEU, which is a one-off recovery instrument due to wind down by 2026. Successive Franco-German pushes for a permanent eurozone budget have been blocked by the Netherlands, Austria, Finland, and other northern creditor states.

The ECB has built a parallel set of crisis tools to substitute, imperfectly, for the missing fiscal architecture. The Outright Monetary Transactions programme, announced in 2012 but never used, gave the ECB the power to buy unlimited quantities of a specific country’s bonds if that country accepted an ESM programme. The Transmission Protection Instrument, announced in July 2022, allows the ECB to buy bonds of countries facing market dysfunction unrelated to their fundamentals, with no formal conditionality attached. The longer-term refinancing operations, which provide cheap multi-year funding to commercial banks, have been used repeatedly to ease credit conditions in stressed countries. None of these tools resolves the underlying problem that the eurozone has no fiscal authority capable of issuing a true safe asset comparable to U.S. Treasuries or German bunds at scale.

The Eurozone in the Global Economy

The bloc runs persistent current account surpluses. The 2024 surplus was close to 3.5% of GDP and the 2025 surplus around 3.2%, driven by Germany and the Netherlands, which both produce far more than they consume. France and Italy run roughly balanced external accounts. Greece, Portugal, and Cyprus run deficits that are now far smaller than in the pre-2010 period.

The United States is the single largest external trading partner, accounting for around 19% of extra-eurozone goods exports and 13% of imports. China is second on both sides, followed by the United Kingdom, which, despite Brexit, remains the bloc’s third-largest export market. Trade with Russia collapsed by more than 80% between 2021 and 2024 following sanctions. The pattern of trade is shifting. U.S. tariff increases announced in 2025 affected an estimated $400 billion of EU exports and forced a 2026 Trade and Technology Council renegotiation that remains unresolved at the time of writing.

Foreign exchange reserves held by Eurosystem central banks total close to €600 billion, with another €500 billion held as gold. These holdings are small relative to the size of the bloc’s external transactions but reflect the fact that the euro itself is a reserve currency: the Eurosystem holds reserves in dollars, yen, and renminbi, not in its own currency. The euro’s effective exchange rate has traded in a range of roughly 95 to 110 since 2015, with the recent move toward the upper end of that range partly reflecting the dollar’s weakness against the basket of major currencies. Internal trade dominates the picture. About 60% of all eurozone goods exports go to other eurozone countries, an unusually high share that reflects both proximity and the elimination of currency risk inside the bloc.

Source: Eurostat, ECB, and IMF Direction of Trade Statistics, 2025.

Structural Pressures in the Eurozone

The bloc’s structural challenges fall into five categories: demographic decline, productivity stagnation, energy and industrial transition, divergent fiscal positions, and the unfinished architecture of the union itself.

Demographics are the most fundamental. The eurozone’s total fertility rate sits around 1.5 children per woman, well below replacement, and the European Commission projects the working-age population will fall by close to 30 million by 2050, absent migration changes. Germany alone needs a net immigration of roughly 400,000 people a year just to keep its labour force stable. Italy’s working-age population is projected to fall by close to 9 million by 2050. The fiscal arithmetic is unforgiving: pension and healthcare spending will rise from roughly 25% of GDP today to close to 28-30% in major member states by mid-century, even on optimistic productivity assumptions. The full mechanics are explored in the silver economy profile.

Productivity is the second concern. Eurozone labour productivity growth averaged less than 0.5% per year in the 2010s and barely 0.7% in the post-pandemic recovery, compared to 1.5% in the United States. The gap is concentrated in services and digital adoption. The bloc has world-class manufacturing firms but produces almost no global tech platforms. Of the world’s twenty largest companies by market capitalisation in early 2026, only one, ASML, is headquartered in the eurozone. The Draghi report on European competitiveness, published in September 2024, estimated the bloc would need an annual investment of €750-800 billion above current levels to close the productivity and innovation gap with the United States.

The energy and industrial transition is the third pressure. German manufacturing employment has fallen by close to 1% since mid-2024, with industries that combine high energy intensity and high export exposure, such as basic chemicals, glass, and aluminium, leading the decline. The bloc’s commitment to a 55% reduction in emissions by 2030 and net zero by 2050 implies an industrial restructuring on a scale comparable to the 1970s deindustrialisation of the British Midlands or the 1990s collapse of East German manufacturing. Whether the political consensus around the European Green Deal can survive a multi-year recession in heavy industry is one of the open questions of the next decade.

Fiscal divergence is the fourth tension. The gap between high-debt and low-debt member states has widened, not narrowed, over the last decade. Estonia, Luxembourg, Bulgaria, and Ireland all run debt ratios below 35% of GDP. Greece, Italy, France, Belgium, and Spain all run debt ratios above 100%. France is now the most acutely watched case: a 5.1% deficit in 2025, debt at 115.6% of GDP, and a Fitch downgrade in September 2025 have pushed French ten-year yields close to Italian levels for the first time in decades. The structural tension is straightforward. The ECB cannot run a tight monetary policy that high-debt members can comfortably afford and a loose monetary policy that low-debt members are willing to tolerate.

The fifth challenge is institutional. The bloc still lacks common deposit insurance, a permanent fiscal stabiliser, and a single capital market. The Capital Markets Union, first proposed in 2015, has advanced incrementally but remains far from completion. Cross-border banking inside the eurozone is still constrained by national supervisors, despite the formal banking union. Repeated proposals for a “safe asset” backed by joint EU borrowing have run into political resistance from creditor states.

| Indicator | Eurozone (2025) | Comparator |

|---|---|---|

| Real GDP growth | 1.4% | United States: 2.0% |

| Government debt-to-GDP | 87.8% | United States: roughly 121% |

| Fiscal deficit | -2.9% of GDP | EU average: -3.1% of GDP |

| Total fertility rate | 1.50 | Replacement level: 2.10 |

| Labour productivity growth (2015-2025 avg) | 0.6% per year | United States: 1.5% per year |

| R&D spending | 2.3% of GDP | United States: 3.5%; South Korea: 4.9% |

| Working-age population (2025-2050 projected change) | -30 million | United States: +20 million |

| Energy import dependency | 58% of consumption | United States: net energy exporter |

| Headline inflation (March 2026) | 2.5% | ECB target: 2.0% |

| Unemployment rate (Feb 2026) | 6.2% | United States: roughly 4.2% |

|

||

Sources: ECB staff macroeconomic projections, March 2026; Eurostat government finance statistics, April 2026; IMF World Economic Outlook, April 2026; OECD Economic Outlook.

The bloc faces these challenges from a position of considerable strength. Household savings rates are high, current account surpluses persist, sovereign borrowing costs remain manageable for most members, and the banking system is in better shape than at any point since 2008. The question is whether the political consensus to act exists. The Draghi report’s call for €750-800 billion in additional annual investment has not been followed by a financing plan. The reformed Stability and Growth Pact tolerates rather than reduces high debt. The capital markets union remains aspirational. The next decade will test whether the bloc can do more than survive each successive shock.

MASEconomics Explains

Four economic concepts behind the eurozone economy

Conclusion

The Eurozone economy is the world’s third-largest currency bloc, producing close to €15.8 trillion of output, accounting for one-seventh of global GDP, and serving as the home of the world’s second reserve currency. It groups twenty-one countries under one monetary authority while leaving fiscal policy to national governments, an arrangement that has survived three major crises and continues to expand, with Bulgaria joining as the twenty-first member in January 2026.

The bloc enters 2026 with growth of 0.9% projected, headline inflation rising to 2.6%, the deposit rate held at 2.0%, and an aggregate debt-to-GDP ratio of 87.8%. Its structural challenges are well documented: an ageing population, productivity that has trailed the United States for two decades, deep dependence on imported energy, persistent fiscal divergence between northern and southern members, and an institutional architecture that remains incomplete. Its strengths are equally clear: a manufacturing base that still leads the world in several categories, persistent current account surpluses, deep capital markets, and a central bank that has demonstrated, repeatedly, the willingness to act as a lender of last resort.

Frequently Asked Questions

What is the Eurozone economy?

The Eurozone economy is the combined economy of the European Union countries that use the euro as their shared currency. These countries share one monetary policy through the European Central Bank, but they keep separate national budgets, tax systems, labour-market rules, and public-debt positions. This makes the Eurozone a currency union without a fully unified fiscal union.

How is the Eurozone different from the European Union?

The European Union is the broader political and economic union. The Eurozone is the smaller group of EU members that have adopted the euro as their currency. Some EU countries remain outside the euro area, which means they participate in the single market but keep their own national currencies and monetary policies.

Why is one currency difficult for many economies?

One currency is difficult because countries can face different economic conditions while sharing the same interest rate and exchange rate. A policy stance that fits Germany or the Netherlands may not fit Greece, Italy, Spain, or Portugal at the same moment. Without national exchange rates, adjustment often has to come through wages, prices, migration, fiscal policy, and structural reform.

What are the main strengths of the Eurozone economy?

The Eurozone’s main strengths are a large single currency area, deep trade integration, strong industrial capacity, high household savings in several countries, advanced infrastructure, and the global role of the euro. The shared currency reduces exchange-rate risk inside the bloc and supports cross-border trade. The European Central Bank also gives the region a common monetary anchor.

What are the main weaknesses of the Eurozone economy?

The Eurozone’s main weaknesses are uneven productivity, fragmented fiscal policy, banking and capital-market fragmentation, demographic ageing, and different debt levels across member states. The region has one monetary policy but many national fiscal policies. This creates coordination challenges during recessions, debt crises, energy shocks, and periods of high inflation.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics