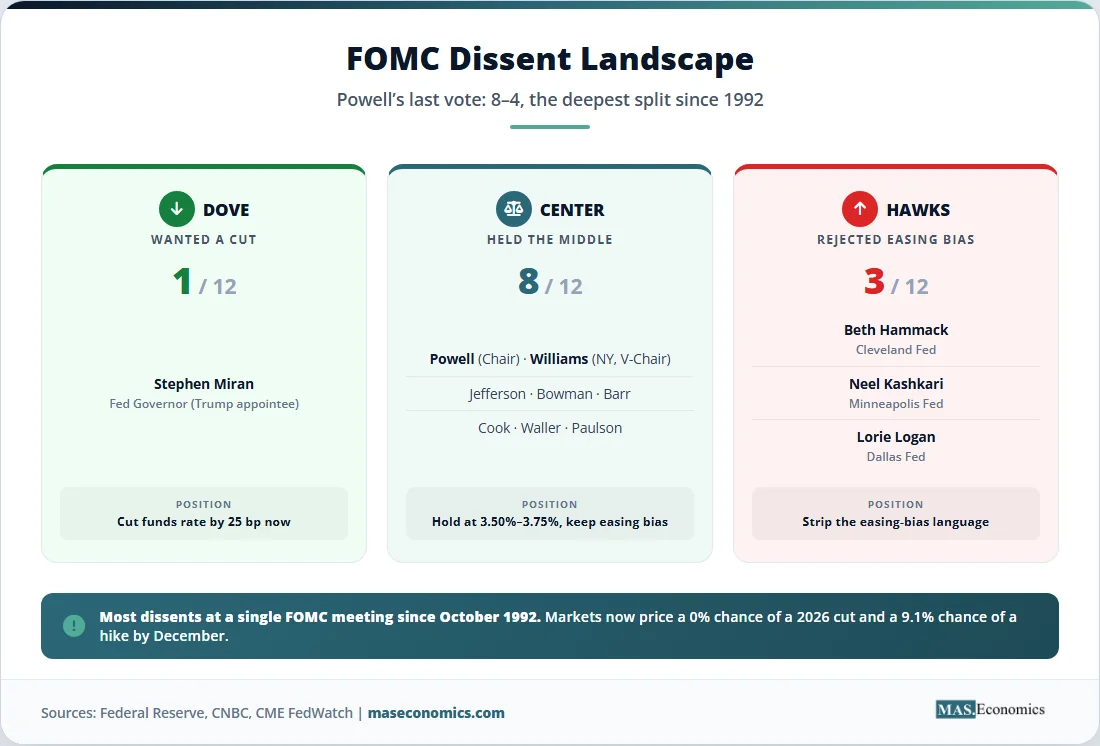

The Federal Reserve held interest rates at 3.50%–3.75% on Wednesday, delivering the most divided FOMC vote in more than three decades and closing the book on Jerome Powell’s tumultuous eight-year tenure as chair. The Jerome Powell final rate decision split the committee 8–4: one Trump-appointed governor wanted a quarter-point cut, three regional bank presidents wanted to slam the door on cuts entirely, and eight members held the uneasy middle. It was the most dissents at a single FOMC meeting since October 1992, and it landed at the worst possible moment for an outgoing chair trying to hand his successor a steady ship.

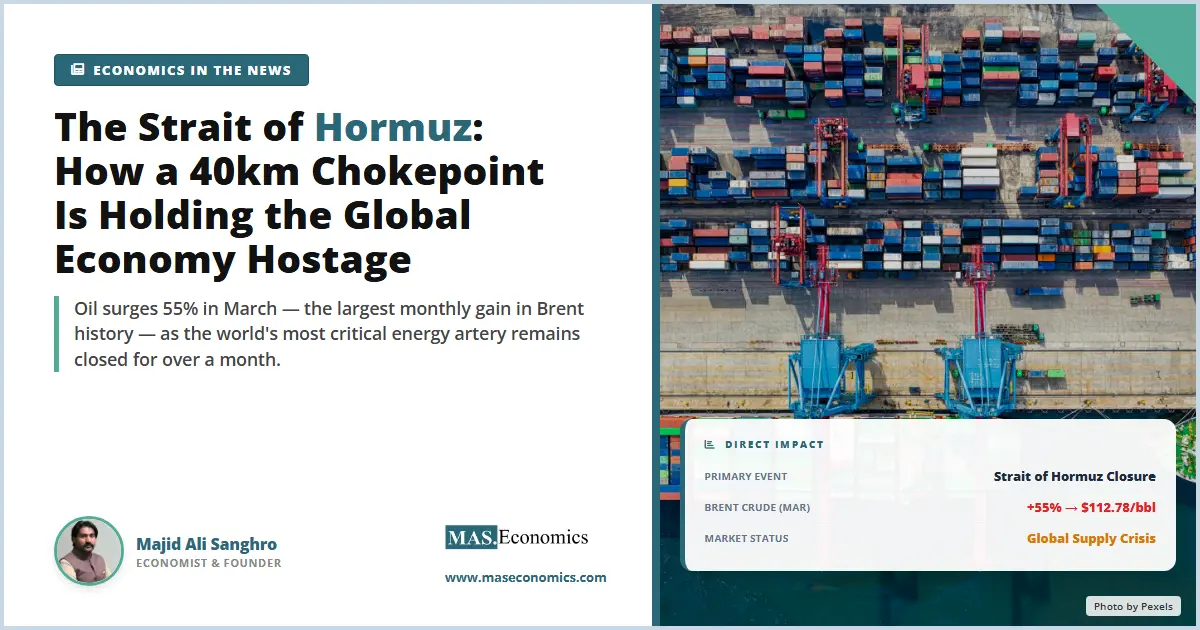

The economic backdrop made consensus impossible. Brent crude closed above $118 a barrel after President Donald Trump pledged to keep a US naval blockade on Iran. March headline CPI clocked in at 3.3% year-on-year, the hottest reading since May 2024, with the energy component jumping 10.9% month-on-month. The Strait of Hormuz remains effectively closed, choking off roughly 20% of seaborne global oil trade in what the International Energy Agency has called the largest supply disruption in the history of the global oil market. Hours before the meeting, the Senate Banking Committee advanced Trump’s nominee Kevin Warsh on a party-line vote, the first fully partisan committee vote on a Fed chair in the panel’s history.

Then Powell did something no recent Fed chair has done. He announced he will remain on the Board of Governors after his chair term expires on May 15, citing what he called the legal assaults battering the institution. The decision denies Trump a vacancy, complicates Warsh’s path to a friendly board, and writes the final chapter of a tenure that will be remembered for pandemic firefighting, an inflation misdiagnosis that almost cost Powell his soft landing, and a year-long fight to keep monetary policy out of the Oval Office.

The 8–4 Vote That Divided the Fed

Markets had priced a 100% probability of no change going into the meeting. The vote count was the surprise. Stephen Miran, the Trump-appointed governor who joined the board in September 2025, dissented in favor of a 25-basis-point cut for the sixth consecutive meeting. That was expected. The other three dissents were not. Beth Hammack of the Cleveland Fed, Neel Kashkari of Minneapolis, and Lorie Logan of Dallas all voted to hold rates but rejected the statement’s so-called “easing bias”, the sentence that read: “In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.”

The three hawks wanted that line stripped. They believed signaling future cuts when energy prices are surging, and core services inflation remains sticky was a strategic error. As Powell put it at the press conference, more members of the committee wanted the language to communicate a neutral stance, “so that a hike is as likely as a cut.” That phrase, embedded almost casually in a routine press conference, did something the Fed has not done in this cycle: it put a 2026 rate hike officially on the table. According to CME Group’s FedWatch tool, traders now assign a 0% probability of a cut by December and a 9.1% probability of a hike, up from zero a day earlier. On Polymarket, the zero-cuts-in-2026 outcome jumped to 55.6%.

The economic data behind the split tells the story. Headline payrolls grew by a stronger-than-expected 178,000 in March, and the unemployment rate slipped to 4.3%, suggesting a labor market that, while cooler than 2023, is not collapsing. Inflation, by contrast, is moving in the wrong direction. The combination of tariffs from the Trump administration’s 2025 trade overhaul and the energy spike from the Iran war has pushed core PCE, the Fed’s preferred gauge, back toward 3%, well above the 2% target. Powell described the situation in terms that few central bankers would choose lightly. The committee, he said, is no longer in textbook look-through mode on energy. The full FOMC statement is on the Federal Reserve website.

The geopolitical context for the decision sits in two earlier MASEconomics pieces: the Strait of Hormuz chokepoint analysis and oil price shocks and why energy crises keep coming back. Both explain the supply-side dynamics that just ate the 2026 rate-cut narrative.

Powell’s Tenure in Numbers

Stripping away rhetoric and looking only at outcomes, Powell ran the Fed during a period that contained almost every kind of macroeconomic event that can happen to a central banker: a global pandemic, a 40-year inflation surge, the most aggressive hiking cycle since the Volcker era, two major wars, a tariff regime, and a presidential pressure campaign. The scoreboard is mixed but defensible. According to data compiled by Investopedia and the Federal Reserve, Powell had the lowest average unemployment rate of any Fed chair since 1978 and the third-highest average inflation since the dual mandate was codified in 1977. PCE inflation averaged 3% across his tenure, above the 2% target and above what Yellen, Bernanke, and even most of Greenspan’s tenure delivered.

The table below compares Powell with the four chairs who preceded him on the four metrics that matter most: average unemployment, average inflation, the S&P 500’s annualized return, and balance sheet behaviour.

Table 1. Fed Chairs Compared: Powell Against Volcker, Greenspan, Bernanke, and Yellen

| Fed Chair | Tenure | Avg Unemployment | Avg Inflation (PCE) | S&P 500 Annual Return | Balance Sheet Path |

|---|---|---|---|---|---|

| Paul Volcker | 1979–1987 | 7.6% | 5.4% | 10.0% | Stable, small |

| Alan Greenspan | 1987–2006 | 5.6% | 2.6% | 11.4% | Modest expansion |

| Ben Bernanke | 2006–2014 | 7.5% | 1.9% | 5.6% | $0.9T → $4.5T |

| Janet Yellen | 2014–2018 | 4.9% | 1.4% | 11.0% | $4.5T → $4.4T |

| Jerome Powell | 2018–2026 | 4.4% | 3.0% | 14.7% | $4.4T → $9.0T peak |

| |||||

Sources: Federal Reserve Economic Data (FRED), Bureau of Labor Statistics, Bureau of Economic Analysis, Yahoo Finance. Inflation series uses headline PCE; Volcker pre-1985 figures use CPI for consistency with that era. S&P 500 returns are total annualized.

Two numbers stand out. The first is unemployment: 4.4% on average, despite a pandemic that briefly pushed the rate to 14.7%. That is a stronger labor-market record than any chair in nearly half a century. The second is inflation: 3% on average, fifty percent above target. Tariffs and a wartime energy shock are propping the figure up in the final months, but even before those events, inflation had been stubbornly above 2% since mid-2021. The S&P 500’s 14.7% annualized return looks spectacular but partly reflects the same liquidity that kept inflation hot. The balance sheet doubled. Both can be true at once.

Pandemic Response: The Finest Hour

In March 2020, the global economy froze. Within ten days, Powell led the FOMC through the most aggressive monetary easing in Fed history. The federal funds rate was cut to 0–0.25%, the discount window was opened wide, and a series of emergency lending facilities (the Primary Market Corporate Credit Facility, the Secondary Market Corporate Credit Facility, the Municipal Liquidity Facility, and the Main Street Lending Program) were stood up in coordination with the Treasury. The Fed bought Treasuries and mortgage-backed securities at a pace that made the 2008 quantitative easing programs look modest. Within six weeks, the balance sheet expanded by roughly $2 trillion.

The mechanism behind that expansion is the focus of our explainer on quantitative easing, and the playbook itself was a refined version of what Bernanke pioneered during the 2008 financial crisis. What Powell added was speed and scale. Critics later argued the Fed crossed lines it should not have crossed. Defenders argued those lines existed precisely so they could be crossed in a once-in-a-century emergency.

The recovery vindicated the bet. US GDP regained its pre-pandemic level by mid-2021, faster than any G7 economy. Unemployment, which peaked at 14.7% in April 2020, fell to 3.4% by early 2023, a 50-year low. The dual mandate, examined in our piece on central banking and monetary policy, looked like a triumph. Then came the inflation.

The Transitory Mistake

In August 2021, with CPI already running near 5%, Powell stood at the Jackson Hole symposium and said the inflation effects of pandemic dislocations were likely to be transitory. By summer 2022, headline CPI hit 9.1%, the highest reading since 1981. The diagnosis had been wrong.

The intellectual error was specific. Fed economists believed pandemic supply-chain bottlenecks (the chip shortage, port congestion, the Suez Canal blockage) would unwind on their own and that demand would normalise without aggressive tightening. They underweighted the demand-side impact of the 2020 and 2021 fiscal stimulus packages and the cumulative effect of years of accommodative monetary policy. By the time Powell publicly retired the word in November 2021, real interest rates were still falling because inflation was rising faster than the nominal funds rate. The Fed did not begin hiking until March 2022, four months after acknowledging the problem. A detailed analysis in the American Institute for Economic Research laid out the timing in painful detail.

What followed was the most aggressive hiking cycle since Volcker: 525 basis points in 16 months, taking the funds rate from near zero to a peak range of 5.25%–5.50%. The full mechanics of how those reports are read in real time are in our guide to CPI, PCE, and PPI. The shift in framework that enabled the original miscalculation, Flexible Average Inflation Targeting (adopted in August 2020), promised to let inflation run modestly above 2% to make up for years of undershooting. In practice, that promise gave the Fed political and analytical cover to delay tightening when the data was already turning. The 2025 framework review is expected to walk much of FAIT back.

The Soft Landing That Nearly Happened

From mid-2022 to early 2026, Powell pulled off something most economists thought was impossible. He raised rates from 0% to 5.5%, held them there for over a year, then began cautiously cutting in September 2024, and unemployment did not rise. The peak unemployment rate during the disinflation was 4.3%, barely above the long-run estimate of the natural rate. Headline PCE fell from 7.0% in mid-2022 to 2.4% by late 2024. Real wages grew. The S&P 500 set new highs.

This is the textbook definition of a soft landing, and it is genuinely rare. Of the eleven significant Fed tightening cycles since 1955, only one (the 1994–1995 cycle under Greenspan) is commonly classified as a clean soft landing. The Powell cycle was on track to be the second. The job market data is unpacked in our jobs report explainer, and the recession-prediction frameworks that did not flag a downturn during this cycle are reviewed in Recession Watch 2026.

Then the Iran war hit. Brent went from $71 in late February to $126 at the March peak, then settled in the $108–$118 range by late April. CPI re-accelerated. Tariffs added another layer. By April 29, 2026, Powell faced a textbook supply shock: prices rising, labor market softening, recession risk ticking up. The soft landing is no longer something the Fed can claim. Whether it can still be salvaged depends on developments far outside the FOMC’s control. Chiefly, whether the Strait of Hormuz reopens before the energy shock embeds in services inflation. Powell admitted as much in the press conference, listing the four supply shocks his Fed has now absorbed: the pandemic, the Ukraine invasion, the tariffs, and Iran.

The Fight for Fed Independence

For many analysts, Powell’s defining legacy is not the pandemic response or the inflation fight. It is the year-long defence of central bank independence against the most sustained presidential pressure campaign in modern Fed history. The arc is worth tracing in full because it explains why he is staying on the board.

Trump appointed Powell in 2018 and turned on him within months when the Fed kept hiking rates into a cooling economy. The public attacks escalated through Trump’s first term. By the second term, beginning in January 2025, they became routine. Trump called Powell a “moron” and a “numbskull,” nicknamed him “Too Late,” and at various points threatened to fire him. Each threat injected uncertainty into Treasury markets and the dollar. The legal question of whether a president can dismiss a Fed chair “for cause” has never been definitively settled.

The escalation came in November 2025, when federal prosecutors in Washington, DC, opened a criminal investigation into Powell over cost overruns on the Marriner S. Eccles Building renovation. The project, originally budgeted at $1.9 billion, had grown to roughly $2.5 billion because of asbestos remediation, an unexpectedly high water table, blast-resistant security upgrades required by the Department of Homeland Security, and historic-preservation requirements. US Attorney Jeanine Pirro issued subpoenas in January 2026. In March, Judge James Boasberg quashed them, writing that the government had offered no evidence Powell committed any crime “other than displeasing the president.” Pirro vowed to appeal. On April 24, five days before the FOMC meeting, she dropped the criminal probe and referred the matter to the Fed’s Inspector General, with the explicit option to restart the investigation if the IG made a criminal referral.

That is the legal threat Powell cited at the press conference. He had received what he called “assurances” over the weekend that the DOJ would not reopen the investigation unless the IG made a criminal referral, but he made clear those assurances were not enough. He told reporters his concern was about “the series of legal attacks on the Fed which threaten our ability to conduct monetary policy without considering political factors.” By staying on the Board of Governors until at least the IG report concludes, Powell does three things: he denies Trump a vacancy, he keeps a senior monetary-policy voice in the room as Warsh takes over, and he sets a precedent that will outlast his own tenure. The constitutional and institutional stakes are explored in our analysis of central bank independence threats and in the foundational explainer on central bank independence.

The four dissents on Wednesday are part of the same story. They were not a rebellion against Powell. They were a signal to Warsh. As Renaissance Macro’s Neil Dutta put it, the chair’s power is the power of persuasion, and Warsh inherits a committee where four of twelve voting members already disagree with the consensus in opposite directions. Convincing Lorie Logan to back early cuts when energy prices are spiking will not be easy. Senator Elizabeth Warren noted that the 13–11 Senate Banking Committee vote advancing Warsh was the first fully partisan committee vote on a Fed chair in the panel’s history. The institution is not as protected as it was eight years ago. Powell’s choice to stay is, in part, an attempt to slow that erosion.

Eight Years in One Chart

The chart below tracks three series across Powell’s full tenure, from his February 2018 swearing-in through Wednesday’s decision: the federal funds rate target (upper bound), headline CPI year-on-year, and the S&P 500 indexed to 100 at the start. The story is visible at a glance: the COVID crash and zero-rate response, the inflation surge while rates stayed low, the catch-up hiking cycle, the disinflation, and the late re-acceleration as the Iran war broke through.

Sources: Federal Reserve, Bureau of Labor Statistics, Yahoo Finance. S&P 500 indexed to 100 at February 2018. Annual data points; 2026 figure as of April 29.

Powell’s Policy Innovations and Controversies

Beyond the headline events, Powell’s tenure reshaped the Fed’s operating framework in several ways that will outlast him. The first was the August 2020 adoption of Flexible Average Inflation Targeting, which committed the Fed to letting inflation run modestly above 2% to make up for years of undershooting. The intent was sensible: pre-pandemic, the Fed had spent most of a decade with inflation below target and feared a Japanese-style deflationary trap. The execution was poor. FAIT gave officials a rationale to delay tightening in 2021 even as the data turned. The 2025 framework review is widely expected to recommend abandoning the average-targeting feature in favor of a more symmetric approach.

The second innovation was the consolidation of the so-called ample reserves operating framework, in which the Fed steers short-term rates by setting the interest rate on reserve balances rather than by managing the supply of reserves directly. That regime, inherited from Yellen but cemented under Powell, fundamentally changed how monetary policy is implemented. The third was the September 2024 decision to start the cutting cycle with a 50-basis-point move rather than the customary 25. The choice was criticized at the time as too aggressive, given still-sticky services inflation, and one that some economists, including Carnegie Mellon’s Chester Spatt, now argue contributed to the 2025 reflation.

The fourth was quantitative tightening, the slow runoff of the balance sheet from its $9 trillion peak. The mechanics and lessons of the experiment are covered in our piece on what QT taught us. The reduction was orderly. The peak balance sheet, however, may turn out to be permanent in real terms. The Fed has signaled the new normal for reserves is much higher than the pre-2008 baseline. That is a structural change Bernanke started, Yellen managed, and Powell institutionalized.

The Warsh Transition and What Comes Next

Kevin Warsh is set to be confirmed by the full Senate within weeks. He served as a Fed governor from 2006 to 2011, was widely considered for the chair in 2017 before Trump picked Powell, and has spent the years since at the Hoover Institution writing pointed critiques of expansive Fed action. He has called for a “strategic reset” of monetary policy, advocated a smaller balance sheet, and historically argued for tighter rates than Powell delivered. SoFi CEO Anthony Noto told Yahoo Finance he expects Warsh to deliver more cuts in 2026, but most economists are sceptical. As Claudia Sahm, the former Fed economist who created the Sahm Rule, put it bluntly: with inflation elevated and an active war pushing energy prices higher, an early cut would require seven votes that Warsh does not have. The data simply isn’t there.

The “two popes” scenario complicates everything. Powell’s continued presence on the board as a governor (even with the “low profile” he promised) gives the institutional faction a senior anchor. Warsh would have inherited three Trump appointees on the seven-member board (Christopher Waller, Michelle Bowman, and now himself, replacing Miran). With Powell staying, that head count drops to three of seven rather than three of seven plus an opening. Investment strategist Josh Jamner of ClearBridge told CNBC that this means Warsh’s addition to the FOMC will not swing the dove-hawk balance, since he replaces Miran rather than adding a net Trump-aligned vote. The mathematical reality is that Warsh needs to persuade hawks and centrists, not stack the board.

The international context matters too. Most other G7 central banks have continued cutting through 2025 and 2026. The Bank of England, the European Central Bank, and the Bank of Canada have all moved well below their peaks. The Bank of Japan, going the other way, is normalizing from negative rates. The dynamics are explored in our piece on central bank divergence in 2026, with a broader interest-rate decision context in how the Fed, ECB, and BoE shape your economy. The Fed is now the hawkish outlier, and a Warsh-led Fed that maintains restraint will keep the dollar strong and complicate trade dynamics that are already tense.

Two questions hang over the transition. The first is whether the FAIT framework gets formally retired in the 2025 review, due to be published before Warsh fully takes over. The second is whether Powell’s decision to stay sets a precedent that future former chairs will follow. If it does, the relationship between the chair and the rest of the board changes permanently, and so does the politics of presidential pressure on the Fed.

MASEconomics Explains

Four economic concepts behind the Powell final rate decision

Conclusion

The Jerome Powell final rate decision closes one of the most consequential chairmanships in modern Federal Reserve history. The 8–4 vote on April 29, 2026, reflected a genuine policy dispute. Three hawks worried about an inflation re-acceleration, one dove demanding cuts, eight members trying to hold a credible middle, while energy prices spike and a war drags on. The numbers across Powell’s eight-year tenure show the lowest average unemployment of any chair since 1978, the third-highest average inflation, a 14.7% annualized stock-market return, and a balance sheet that doubled. The pandemic response saved the recovery. The “transitory” misdiagnosis cost the Fed credibility. The soft landing was within reach until the Iran war intervened. The fight to defend institutional independence against unprecedented presidential pressure is now Powell’s most-cited legacy, and his decision to remain on the Board of Governors after his chair term ends is the final chapter of that fight.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.s