In the third quarter of 2024, the United States Treasury spent more on interest payments than on national defense for the first time in modern peacetime, with net interest outlays running at an annualized $950 billion against $874 billion for defense. The shift was the arithmetic consequence of two facts: the federal debt held by the public had risen above 97 percent of GDP, and the average interest rate the Treasury paid on that stock had climbed past 3.3 percent after a decade below 2 percent. A similar pattern was visible in Italy, the United Kingdom, France, and Japan. The same numbers that frame this as a budget question also frame it as a monetary one, because they sit at the heart of an old debate about whether central banks remain free to set interest rates for inflation control when the debt has grown large enough to make tighter rates unbearable. That debate has a name in macroeconomic theory: fiscal dominance.

The term entered modern literature with Thomas Sargent and Neil Wallace’s 1981 paper “Some Unpleasant Monetarist Arithmetic,” which showed that a government running persistent primary deficits forces its central bank to eventually monetize debt or default. Subsequent work, especially the fiscal theory of the price level associated with Christopher Sims, Eric Leeper, and John Cochrane, extended the idea: when fiscal policy does not adjust to stabilize debt, the price level itself becomes the equilibrating variable. Both threads share a structural insight. Monetary policy is independent only when fiscal policy makes it so. When the fiscal authority cannot or will not absorb the cost of disinflation, the monetary authority’s nominal target ceases to be a free choice.

Government Budget Identity

The starting point is the consolidated government budget constraint. Treat the government and the central bank together. In each period, the change in nominal public debt equals the primary deficit plus interest on existing debt minus revenue from money creation. In real per-GDP terms, the evolution of the debt-to-GDP ratio follows:

Debt-to-GDP Dynamics

The expression carries the entire intuition for fiscal dominance. Debt-to-GDP grows when the real interest-rate-growth differential \((r – g)\) is positive, when the government runs a primary deficit (\(s < 0\)), and when seigniorage revenue \(\sigma\) is small. It declines when growth outpaces real rates, when the government runs a primary surplus, or when seigniorage is large enough to retire nominal debt. A government with high debt, weak growth, and persistent deficits faces a stark menu of stabilizing moves: raise the primary surplus, lower the real interest rate, accelerate growth, or extract more seigniorage.

The monetary regime determines which lever is available. Under what Leeper (1991) calls an “active monetary, passive fiscal” regime, the fiscal authority adjusts primary surpluses to stabilize debt, leaving the central bank free to pursue an inflation target through \(r_t\). This is the textbook configuration assumed by inflation-targeting central banks. Under a “passive monetary, active fiscal” regime, the fiscal authority sets primary surpluses based on political constraints rather than debt stabilization. The central bank then has no choice but to deliver whatever inflation is needed to keep the present-value debt equation balanced. The first regime is monetary dominance. The second is fiscal dominance.

Sargent and Wallace’s Arithmetic

The 1981 Sargent and Wallace paper made the trade-off precise by considering a government that issues bonds to finance permanent primary deficits. Suppose the central bank insists on a low money-growth rate today to keep inflation low. With deficits unchanged, the stock of bonds grows over time. If the real interest rate on the debt exceeds the real growth rate of the economy, debt-to-GDP rises without limit. At some future date, the bond market refuses to absorb additional debt at the current interest rate, and the central bank has to choose between letting the government default and printing money to retire the debt.

The unpleasant arithmetic is that tighter money today implies looser money tomorrow. By keeping the policy rate high and money growth low while deficits continue, the central bank lets debt accumulate at a faster pace than it would have under accommodation. The eventual monetization required to stabilize debt then produces higher inflation in the future than would have been needed if the central bank had monetized continuously from the start. Sargent and Wallace’s claim was conditional rather than absolute. It assumed a primary deficit that the fiscal authority refused to close, and it assumed the real interest rate stayed above the real growth rate. In any given economy, either assumption could fail, and the timing of when the constraint binds depends on the maturity structure of the debt and the credibility of future fiscal adjustment.

Fiscal Theory of the Price Level

A second strand of theory pushes the logic further. The fiscal theory of the price level, developed by Sims (1994), Woodford (1995), Leeper (1991), and elaborated in Cochrane (2023), treats the government’s intertemporal budget constraint as an equilibrium condition that determines the price level directly. The identity at the core of the theory is:

Government Intertemporal Budget Identity

Read this as an asset-pricing equation. The real value of government debt is the present value of the future primary surpluses that will service it. Conventional theory treats the right-hand side as adjusting through fiscal policy. The fiscal theory of the price level inverts the causation. If the future primary surpluses on the right-hand side are fixed by political constraints, then the price level \(P_t\) on the left-hand side must adjust to balance the equation. A surprise loosening of expected future surpluses, with the nominal debt stock unchanged, requires the price level to rise.

The fiscal theory of the price level is contested. Critics, including Bennett McCallum and Willem Buiter, have argued that the identity is a constraint that holds in any equilibrium rather than an equation that determines the price level, and that fiscal theory papers smuggle in additional assumptions about which variable adjusts. The empirical case is also debated. But even sceptics of the strong version accept the weaker proposition: when fiscal policy fails to stabilize debt, monetary policy alone cannot anchor the price level indefinitely.

Channels of Fiscal Dominance

The constraint operates through three channels. The first is the interest expense channel. A 100-basis-point increase in the policy rate raises the government’s annual interest bill by roughly 1 percent of GDP for every 100 percent of GDP in debt. With US debt at around 100 percent of GDP, the Federal Reserve’s 525-basis-point hiking cycle from 2022 to 2023 added approximately 5 percentage points of GDP to the annual interest cost once the debt fully repriced. For Italy, at around 135 percent of GDP, the same hike by the European Central Bank carried a still higher fiscal cost. When this cost dominates political conversation about the central bank, the political constraint on further tightening is non-trivial.

The second channel is the financial-stability channel. High debt is held somewhere, typically by domestic banks, pension funds, and insurance companies. Sharply rising rates push down the market price of long-duration bonds, generating mark-to-market losses for the holders. The March 2023 failure of Silicon Valley Bank, triggered in part by unrealized losses on long-duration Treasury and agency holdings, was a small-scale demonstration of the channel. In a fiscal dominance scenario, the central bank’s capacity to keep raising rates is limited by the threat of a banking crisis triggered by losses on government debt held in the banking system.

The third channel is the expectations channel. If markets believe the central bank will eventually monetize debt rather than allow a fiscal crisis, long-term inflation expectations rise even before any monetary action. Higher inflation expectations push up nominal yields, raising debt service costs, which brings forward the moment when the central bank does, in fact, accommodate. The expectations channel is what makes fiscal dominance a self-fulfilling problem rather than a slow-moving one.

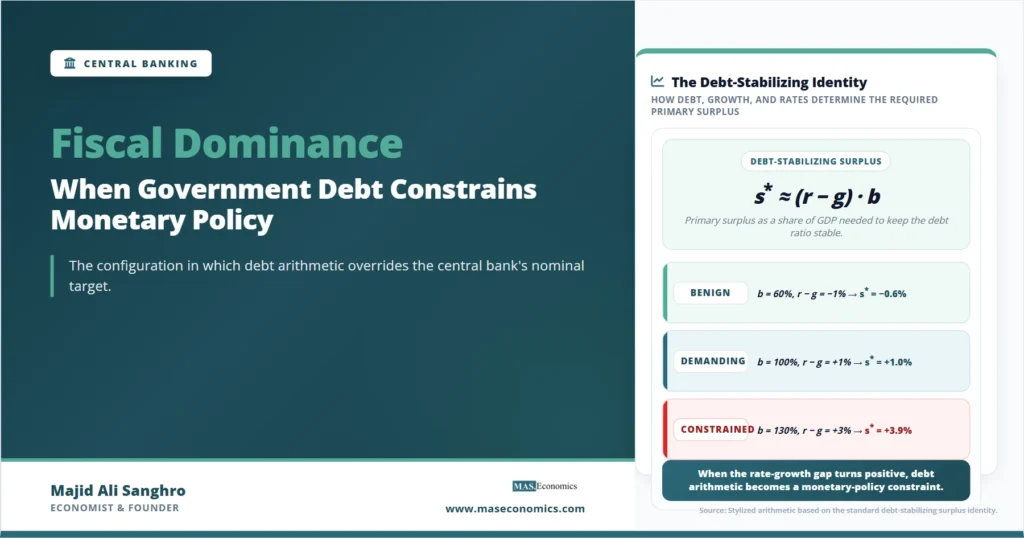

| Initial debt / GDP | Real rate–growth gap \((r – g)\) | Primary surplus needed to stabilize debt | Implied fiscal effort |

|---|---|---|---|

| 60% | −1.0% | −0.6% | Mild deficit tolerated |

| 60% | +1.0% | +0.6% | Modest surplus required |

| 100% | +1.0% | +1.0% | Persistent surplus |

| 100% | +2.0% | +2.0% | Significant tightening |

| 130% | +2.0% | +2.6% | Politically demanding |

| 130% | +3.0% | +3.9% | Rarely achieved historically |

| Identity | \(s^{\ast} \approx (r – g)\,b\) | Stylized debt-stabilizing surplus | |

|

Stylized example based on the standard debt-dynamics identity. The required surplus rises with both the debt stock and the real rate–growth gap.

|

|||

The arithmetic explains why the question of fiscal dominance has become more pressing since the mid-2010s. The post-2008 environment featured \(r – g\) below zero in most advanced economies, making any positive primary surplus enough to stabilize even very high debt ratios. The post-pandemic environment has flipped the sign: real rates are positive again in most advanced economies, growth is constrained by demographics and productivity slowdowns, and the required primary surpluses now look closer to historical highs than to typical post-war averages.

Historical Episodes of Fiscal Dominance

The strongest empirical episodes are sovereign debt crises in emerging markets, where the constraint binds visibly. The Argentine experience documented in Argentina’s recurrent defaults shows the cycle: persistent primary deficits financed by a mix of borrowing and money creation, ending in inflation spikes that erode the real value of nominal debt. Brazil in the 1980s, Turkey in the late 1990s, and Russia in 1998 followed similar paths. In each case, the central bank’s nominal authority remained intact, but the fiscal arithmetic dictated when monetization would have to happen.

The post-World War II American experience is a different and milder demonstration. Federal debt held by the public had risen to roughly 106 percent of GDP by 1946. The Treasury–Federal Reserve Accord of 1951 ended a wartime arrangement under which the Federal Reserve had pegged short-term Treasury yields below market rates, holding interest expense down at the cost of accommodating inflation. The pre-Accord period is widely read as fiscal dominance, since the Fed had agreed not to use the policy rate for inflation control while debt was being inflated down. The post-Accord period saw the debt-to-GDP ratio fall from above 80 percent to below 30 percent over three decades, achieved through a combination of real growth, controlled but positive inflation, and modest primary surpluses.

The European sovereign debt crisis of 2010 to 2012 offered a contemporary advanced-economy stress test. Italy, Spain, and Portugal faced rising debt-service costs as bond yields spiked, with no obvious fiscal adjustment capacity. The European Central Bank’s resolution, especially Mario Draghi’s “whatever it takes” announcement in July 2012 and the subsequent Outright Monetary Transactions framework, can be read as a refusal to accept fiscal dominance: the central bank committed to backstop sovereign debt markets to restore the conditions under which monetary policy could still be used for inflation control. The fact that the OMT framework was contested by the German Constitutional Court reflects exactly the worry that the line between monetary support and fiscal support had been crossed.

Japan’s Counterexample

Japan’s gross government debt has exceeded 200 percent of GDP since the late 2000s, and yet Japan has not experienced fiscal dominance in the standard sense. Inflation remained near zero or negative for most of the 2000s and 2010s, and the Bank of Japan was able to maintain ultra-low policy rates without obvious accommodation costs. The case is often cited as evidence that high debt ratios are compatible with monetary independence.

The Japanese experience is consistent with the theory rather than against it. Two conditions held that prevented the constraint from binding. First, the real interest rate–growth differential was deeply negative for much of the period, often by 2 to 3 percentage points. With \(r – g\) below zero, debt can grow modestly without rising as a share of GDP, even with primary deficits. Second, the bulk of Japanese government debt was held domestically and at historically low yields anchored by deflationary expectations. The Bank of Japan’s quantitative easing programs absorbed a large share of new issuance, but at prices that markets willingly accepted. The arithmetic worked because the conditions made it work, not because the constraint disappeared.

The 2022 to 2024 normalization of Japanese inflation and the Bank of Japan’s gradual exit from yield curve control are now testing whether the favorable arithmetic can persist. If Japanese nominal yields rise faster than nominal growth, the same primary deficits that were sustainable for two decades become a source of accelerating debt accumulation. The case study has not yet concluded.

Caveat. High debt ratios alone do not establish fiscal dominance. The binding constraint is the joint condition of a high debt stock, a positive real rate–growth differential, persistent primary deficits, and political resistance to fiscal adjustment. Removing any one of these breaks the chain.

Warning Signs for Central Banks

Fiscal dominance is rarely declared. It emerges from a sequence of small accommodations that, in retrospect, constrained monetary independence. The literature identifies several indicators that signal pressure.

The first is yield curve steepening in response to monetary tightening. In a normal monetary-dominance regime, a credible rate hike flattens or inverts the yield curve as long rates rise less than short rates, reflecting expectations that inflation will fall. In a fiscal-dominance regime, long rates can rise more than short rates because investors expect future monetization. The 2022 to 2023 episode in the United Kingdom around the Truss-Kwarteng mini-budget showed a compressed version of this dynamic: long gilt yields jumped sharply on the announcement of unfunded tax cuts, with the move signaling a perceived deterioration in the fiscal-monetary configuration.

The second is the sovereign-bank loop, where domestic banks hold large shares of national government debt. Rising rates impose losses on banks, which require recapitalization, which raises fiscal cost, which raises future debt, which raises long-term rates further. The European Central Bank’s 2014 banking-union framework was partly designed to break this loop, with mixed success.

The third is the politicization of central bank decisions about asset purchases. When asset-purchase programs are framed as financial-stability operations during a crisis, they are consistent with monetary dominance. When the same programs continue to absorb sovereign issuance during periods of normal markets, the framing shifts. The post-pandemic debate about the quantitative tightening pace has hinged on this distinction.

| Indicator | Monetary-Dominance Signal | Fiscal-Dominance Signal |

|---|---|---|

| Yield curve response to rate hikes | Flattens or inverts | Steepens as long rates rise |

| Term premium | Stable or compressed | Rising and volatile |

| Long-term inflation expectations | Anchored near target | De-anchoring upward |

| Central bank balance sheet | Contracts after crises end | Persistently large and growing |

| Public debate around the central bank | Focused on inflation forecast | Focused on debt service cost |

| Sovereign-bank exposure | Diversified, limited concentration | Banks heavily exposed to domestic sovereign |

|

Source: MASEconomics editorial synthesis based on Sargent and Wallace (1981), Leeper (1991), and Bank for International Settlements policy work on fiscal-monetary interaction.

|

||

2026 Configuration in Major Economies

Several major economies now show some, but not all, of the indicators. In the United States, federal debt held by the public has reached roughly 100 percent of GDP, the average interest cost on that debt has tripled from its 2021 low, and net interest outlays have moved above defense spending. The Congressional Budget Office’s 2025 long-term projection has debt-to-GDP rising past 130 percent by 2035 under current law. Long-term inflation expectations as measured by the five-year forward breakeven rate remain reasonably well anchored near 2.3 to 2.5 percent, but the term premium has been positive since mid-2023 after a decade near zero. The configuration is consistent with monetary dominance under stress rather than active fiscal dominance, but the safety margin is smaller than it has been at any point since the early 1990s.

In the United Kingdom, the gilt market’s reaction to the September 2022 mini-budget showed how quickly the configuration can shift even at debt levels (around 100 percent of GDP) similar to the United States. Italy’s debt ratio remains above 135 percent of GDP, supported by ECB asset holdings and OMT credibility but with limited fiscal adjustment capacity. France faces an intermediate position with debt around 110 percent of GDP and persistent deficits. Japan’s adjustment is the most novel case, since the country is exiting a multi-decade regime of negative \(r – g\) and the new arithmetic is still being established.

None of these economies has reached the point where the central bank is openly subordinated to fiscal needs. Several have reached the point where the question is regularly asked. As central bank independence rests on the unspoken understanding that fiscal policy will adjust to make monetary independence feasible, the gap between current fiscal trajectories and that requirement is a meaningful constraint.

Distinguishing Fiscal Dominance from Related Concepts

The literature is dense with terms that overlap with but are not identical to fiscal dominance. Worth keeping distinct:

Monetization refers to the act of the central bank financing government deficits by creating reserves. Monetization can occur under monetary dominance (during wartime, or as a crisis response) without permanently subordinating monetary policy. It becomes fiscal dominance only when the central bank cannot stop monetizing without producing a fiscal crisis.

Financial repression refers to administrative measures that keep nominal yields below their market-clearing level, often through interest-rate ceilings on bank deposits, capital controls, or regulatory caps on what financial institutions can pay savers. Financial repression is the policy toolkit that makes fiscal dominance bearable politically. The post-1945 reduction of US debt-to-GDP relied on a mix of growth, modest inflation, and financial repression that kept savers earning negative real returns.

Modern Monetary Theory argues that a sovereign government issuing debt in its own currency is constrained by inflation rather than by financing capacity. MMT and fiscal dominance share the observation that monetization is always feasible. They diverge on whether continuous monetization is desirable. MMT treats the inflation constraint as something to be managed actively through fiscal policy. Fiscal dominance theory treats the inflation constraint as something that binds painfully when fiscal policy fails to manage it.

Seigniorage, covered in greater depth in our article on seigniorage as an inflation tool, is the revenue a government collects by creating new base money. In a monetary-dominance regime, seigniorage is a small fraction of government revenue. In a fiscal-dominance regime, it rises until the inflation tax becomes politically costly.

Conditions That Could Bind

The empirical literature, including work by Reinhart and Rogoff (2010), Reinhart and Sbrancia (2015) on financial repression, and Mauro et al. (2013) at the IMF, has identified conditions that historically produced fiscal-dominance episodes. Three stand out.

The first is a sudden upward shift in the real rate–growth differential. The Volcker disinflation in the United States moved \(r – g\) from negative to substantially positive within a few years, raising debt service costs faster than primary surpluses could be adjusted. Federal debt-to-GDP rose from 25 percent in 1980 to 47 percent by 1992 despite reasonably strong nominal growth. The episode did not produce fiscal dominance because the initial debt stock was low. The same shock applied to current debt levels would produce a much larger debt impulse.

The second is a maturity-structure mismatch. Short-duration debt reprices quickly when rates rise, while long-duration debt provides a buffer. The United Kingdom held the longest average debt maturity in the G7 for most of the post-1990 period, which helped insulate the UK from short-term rate shocks. The United States average maturity, at roughly six years, is closer to the OECD median and reprices faster. A country that has shifted its debt structure more recently has implicitly raised its vulnerability to fiscal dominance.

The third is the politicization of monetary policy. Pressure on the central bank to keep rates low for fiscal reasons need not be explicit; it can take the form of appointment patterns, public criticism of rate decisions, or institutional changes that reduce operational independence. The historical evidence in Cukierman, Webb, and Neyapti (1992) and updated by subsequent work shows that measured central bank independence correlates with lower inflation, but the causal mechanism runs both ways: independent central banks deliver lower inflation, and economies with stable fiscal policy can afford independent central banks.

Explains

Four concepts that frame the fiscal-monetary balance

Continue exploring how debt, deficits, and inflation interact with monetary policy.

Explore the MASEconomics BlogConclusion

Fiscal dominance is not a single event but a configuration of fiscal and monetary variables. It binds when the debt stock is high, the real interest rate exceeds the real growth rate persistently, primary surpluses fail to adjust, and political constraints prevent the central bank from imposing the disinflation that the textbook regime would require. None of the major advanced economies sits clearly inside the constraint today. Several sit close enough to it that conversations about central bank policy now include explicit references to the fiscal cost of higher rates, and that shift in framing is itself a partial loss of the institutional separation that monetary dominance requires.

The theoretical work from Sargent and Wallace through the fiscal theory of the price level has clarified what a return to fiscal dominance would look like: long-term inflation expectations would de-anchor first, the term premium would rise, sovereign-bank loops would tighten, and central bank balance sheets would absorb sovereign issuance for reasons that no longer fit a standard financial-stability framing. The arithmetic that produces those outcomes is not new. What is new in 2026 is that the arithmetic now bears on the largest economies in the world, where the assumption of fiscal accommodation has been treated as automatic for two decades. Whether that assumption holds depends on choices that are political rather than monetary. The central bank’s job, in the meantime, is to set policy under the assumption that the choices will be made, while preparing for the conditions under which they will not.

Frequently Asked Questions

What is the simplest definition of fiscal dominance?

Fiscal dominance describes a situation in which government debt and deficits have grown large enough that the central bank cannot raise interest rates to control inflation without triggering a fiscal crisis. In that configuration, monetary policy is effectively subordinated to fiscal needs, and inflation becomes the variable that adjusts to keep public debt sustainable.

Is the United States in fiscal dominance now?

No, by the standard definition. Long-term inflation expectations remain anchored near the Federal Reserve’s target, the Fed retained the ability to raise rates by 525 basis points between 2022 and 2023, and the Treasury continues to issue debt at market-determined yields. However, with federal debt held by the public near 100 percent of GDP, rising net interest outlays, and projected debt trajectories that continue upward, the conditions that historically produce fiscal dominance episodes are closer to being met than at any point in recent decades.

How is fiscal dominance different from Modern Monetary Theory?

Both ideas observe that a government issuing debt in its own currency can always monetize. They differ on the implications. Modern Monetary Theory treats monetization as a normal policy instrument constrained by inflation. Fiscal dominance theory treats forced monetization as a failure state in which monetary policy loses its ability to anchor inflation. Fiscal dominance is descriptive of what happens when the fiscal-monetary balance breaks down; MMT is a prescriptive framework for managing the relationship.

Why has Japan not experienced fiscal dominance despite very high debt?

The Japanese case worked because the real interest rate stayed well below the real growth rate for most of the period since the late 1990s, which allowed even modest primary surpluses or small deficits to stabilize the debt ratio. With real rates rising and inflation now near 2 percent, the arithmetic that protected Japan from fiscal dominance is changing, and the durability of the configuration is now being tested.

Can a central bank prevent fiscal dominance?

Not on its own. Central bank independence is a necessary but not sufficient condition for monetary dominance. The fiscal authority must adjust primary surpluses over time to stabilize debt at any prevailing interest rate. If it does not, the central bank can delay accommodation but cannot indefinitely avoid it. Sustained monetary dominance requires fiscal cooperation, not just monetary determination.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics