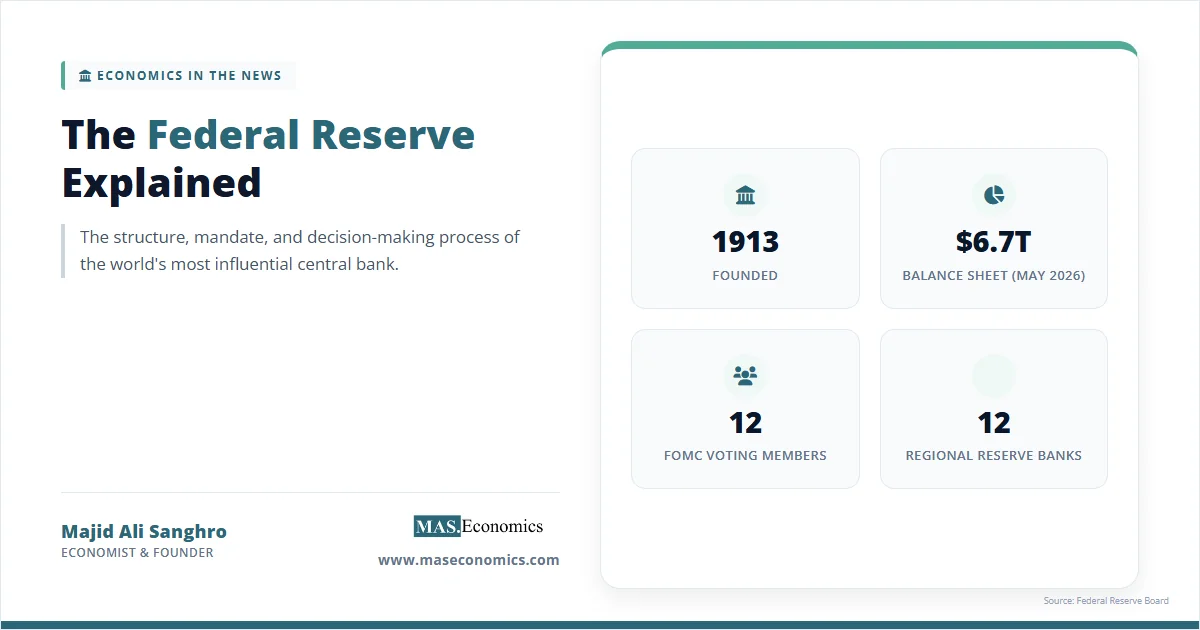

The Federal Reserve explained in plain terms is the central bank of the United States, established by Congress in 1913 and tasked with conducting monetary policy, supervising banks, and maintaining the stability of the financial system. As of May 2026, the Fed holds roughly $6.7 trillion in assets, sets the policy interest rate that anchors borrowing costs across the global economy, and operates through a hybrid structure of public oversight and regional Reserve Banks, unique among major central banks.

The institution sits at the centre of every economic story that matters in 2026. Its decisions on the federal funds rate move mortgage rates in Dallas and bond yields in Tokyo within minutes. Its balance sheet operations determine how much liquidity flows through the global dollar system. And its leadership transition from Jerome Powell to Kevin Warsh in mid-May 2026 has placed the question of central bank independence at the centre of American political debate.

This profile covers the Fed’s mandate, governance, tools, and track record. It is the foundational reference that supports every news article on US monetary policy decisions, inflation prints, and labour market data.

The Mission of the Federal Reserve

The Federal Reserve operates under a dual mandate written into the Federal Reserve Act and reaffirmed by the 1977 Humphrey-Hawkins amendments: maximum employment and stable prices. Congress added a third operational goal of moderate long-term interest rates, though the Fed treats this as a consequence of meeting the first two rather than a separate target.

Maximum employment has no fixed numerical target. The Fed estimates the longer-run unemployment rate consistent with stable inflation and uses that estimate as a benchmark, but it explicitly recognises that this level can shift with demographics, technology, and labour market structure. Price stability, in contrast, has been operationalised since 2012 as a 2% annual increase in the personal consumption expenditures price index, the inflation gauge the Fed prefers over the more widely cited consumer price index.

Beyond monetary policy, the Fed performs four other functions that often go unnoticed. It supervises and regulates banks, including the largest globally systemic institutions. It serves as the lender of last resort to the banking system, a role it leaned on heavily during the 2008 crisis and again in March 2023 when regional banks failed. It operates the payments infrastructure that clears trillions of dollars daily through Fedwire and the newer FedNow real-time settlement system. And it acts as a fiscal agent for the US Treasury, handling government securities and Treasury cash balances. Each of these functions is explored in our companion piece on the functions of central banks.

From Founding to Modern Mandate

The Fed was the third attempt at a US central bank. Both predecessors, the First and Second Banks of the United States, were dissolved in the nineteenth century after political opposition to centralised financial power. The 1907 banking panic, which only ended after J.P. Morgan personally orchestrated a private rescue, made it clear the country needed a permanent institutional backstop. Six years of negotiation produced the Federal Reserve Act, signed by President Woodrow Wilson on December 23, 1913.

The original design reflected a political compromise. Eastern bankers wanted a single central bank in New York. Western and southern populists wanted no central bank at all. The result was twelve regional Reserve Banks scattered across the country, supervised by a Washington-based Board appointed by the President. The structure was deliberately decentralised so that no single financial centre could dominate national monetary policy.

The Banking Act of 1933 created the Federal Open Market Committee after the Great Depression exposed the cost of fragmented decision-making, when different regional Reserve Banks had pulled monetary policy in opposite directions. The 1935 Banking Act consolidated power further by giving the Washington-based Board control over discount rates and reserve requirements. The Treasury-Fed Accord of 1951 marked the moment the Fed gained independence from political pressure to peg interest rates at low levels, an episode that economic historians treat as the founding of modern Fed independence.

The mandate evolved through major economic shocks. The Great Inflation of the 1970s, which we examine in detail in our piece on comparing the Great Inflation across countries, prompted Paul Volcker’s drastic tightening that pushed the federal funds rate above 19% in 1981 and recommitted the institution to price stability. The 2008 financial crisis added crisis-fighting tools that fundamentally changed the size and composition of the balance sheet. The 2020 pandemic response pushed those tools further, and the post-pandemic inflation surge tested whether the framework could deliver disinflation without recession.

Inside the Federal Reserve

The Federal Reserve is governed by three interlocking bodies: the Board of Governors, the twelve regional Reserve Banks, and the Federal Open Market Committee. Each has distinct legal authority, and understanding the division clarifies what the Fed can and cannot do.

The Board of Governors sits in Washington, D.C. and consists of seven members appointed by the President and confirmed by the Senate to fourteen-year non-renewable terms. The staggered terms are designed to insulate the Board from any single president’s influence; in theory, no two-term president can replace a majority of the Board through normal turnover. The Chair and Vice Chair are nominated separately to four-year terms in those leadership roles. As of May 2026, Jerome Powell’s term as Chair ended on May 15, with Kevin Warsh confirmed as his successor following a Senate Banking Committee vote that split 13-11 along party lines. Powell announced he would remain on the Board as a Governor rather than resign, a departure from the post-chairmanship convention of stepping down. The implications of this transition are analysed in our piece on Kevin Warsh and the Federal Reserve.

The twelve Reserve Banks are headquartered in Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. Each operates as a quasi-private institution, technically owned by the member commercial banks in its district but supervised by the Board. The President of each Reserve Bank is selected by that bank’s board of directors but must be approved by the Board of Governors, a procedure that gives Washington effective veto power. The New York Fed sits at the apex of the regional system because it operates the open market trading desk that executes monetary policy.

The Federal Open Market Committee is where monetary policy is actually made. It has twelve voting members at any given time: the seven Governors, the President of the New York Fed (a permanent vote), and four of the remaining eleven Reserve Bank Presidents who rotate annually. All twelve Reserve Bank Presidents attend every meeting and contribute to the discussion, but only the four rotating votes count alongside the Governors and the New York Fed. Decisions are taken by simple majority, though dissents are recorded in the minutes and treated as an important signal of internal disagreement.

The FOMC meets eight times a year, typically over two days, with quarterly meetings followed by the release of the Summary of Economic Projections, the so-called dot plot that aggregates each participant’s expected path for the federal funds rate. The Chair holds a press conference after every meeting, a practice introduced under Ben Bernanke in 2011 and expanded under Powell to maximise transparency. For more on how monetary policy decisions translate into the broader economy, see our explainer on the monetary transmission mechanism.

How the Fed Acts

The Fed’s policy toolkit has expanded significantly since 2008. Before the financial crisis, the central bank conducted monetary policy almost exclusively through small open market operations that nudged the federal funds rate toward its target. After the crisis, the toolkit grew to include large-scale asset purchases, forward guidance, the interest rate paid on reserve balances, the overnight reverse repurchase facility, and a range of emergency lending programs. The full set of monetary policy tools is covered in our dedicated explainer.

The federal funds rate target is the headline tool. The FOMC sets a target range, currently a band 25 basis points wide, and the New York Fed’s open market desk uses two administered rates to keep the actual federal funds rate inside that range. The interest rate on reserve balances, currently the upper bound, ensures that banks holding reserves at the Fed earn at least that rate and therefore will not lend to one another below it. The overnight reverse repurchase rate, the lower bound, provides money market funds and other non-bank counterparties with a guaranteed return, preventing rates from falling below the target.

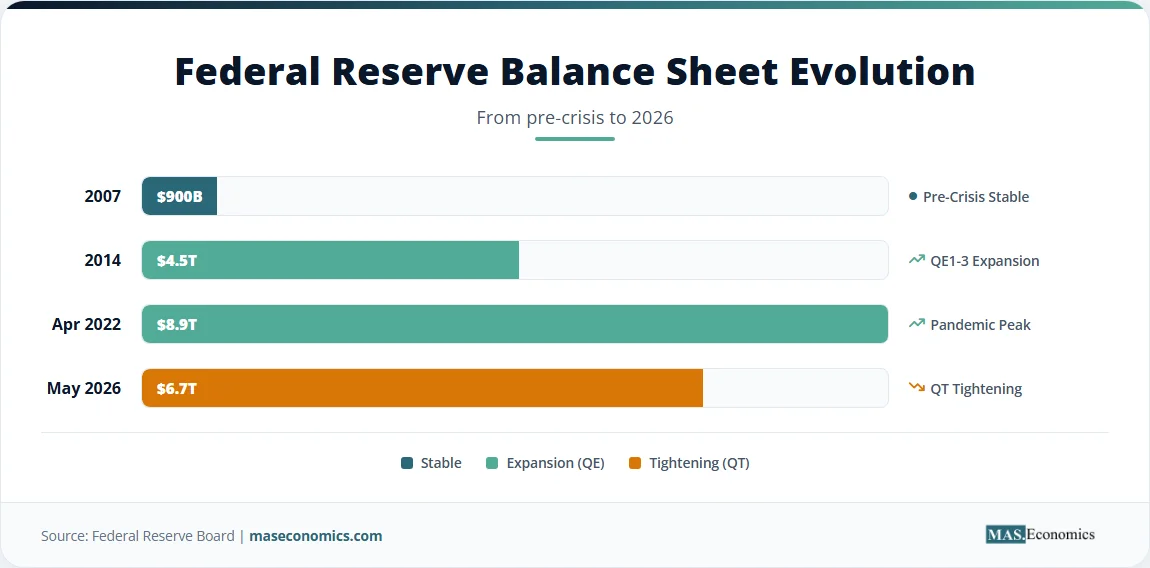

Quantitative easing and quantitative tightening operate on the longer end of the yield curve. By buying or shrinking holdings of Treasury securities and mortgage-backed securities, the Fed influences term premiums and credit conditions when the policy rate alone is insufficient. The balance sheet expanded from below $1 trillion in 2007 to roughly $9 trillion at the 2022 peak, before the current quantitative tightening cycle reduced it to about $6.7 trillion as of late April 2026. The mechanics and consequences of this experiment are detailed in our piece on quantitative tightening and the foundational explainer on quantitative easing.

Forward guidance is a verbal tool. The FOMC communicates the likely future path of rates through statements, press conferences, and the dot plot, which shapes market expectations and therefore long-term interest rates. The discount window, the original lender-of-last-resort facility, lends directly to banks against collateral. Emergency lending facilities under Section 13(3) of the Federal Reserve Act allow the Fed to lend to non-bank entities in unusual and exigent circumstances, the authority that powered the 2008 and 2020 crisis responses.

The table below summarises the main tools and how each is deployed.

| Tool | What It Does | Typical Use |

|---|---|---|

| Federal funds rate target | Sets the policy interest rate range that anchors short-term borrowing costs | Standard monthly policy adjustment at FOMC meetings |

| Interest on reserve balances | Administered rate that forms the upper bound of the federal funds range | Used continuously to keep market rates inside target range |

| Overnight reverse repos (ON RRP) | Administered rate forming the lower bound for non-bank counterparties | Floor for money market rates, particularly during liquidity surplus |

| Open market operations | Buying or selling Treasury and agency securities | Adjusts reserves and balance sheet size |

| Quantitative easing / tightening | Large-scale asset purchases or run-off to influence long-term rates | Crisis response (QE) and post-crisis normalisation (QT) |

| Forward guidance | Communication about future rate path via statements and dot plot | Shapes market expectations, especially when policy rate is constrained |

| Discount window | Direct lending to banks against collateral | Liquidity backstop, counter-cyclical bank funding support |

| Section 13(3) emergency facilities | Lending to non-bank entities in unusual and exigent circumstances | Crisis response (used in 2008, 2020, and March 2023 bank failures) |

|

||

Source: Federal Reserve Board, Policy Tools documentation.

The Federal Reserve Through Crises

The Fed has been defined as much by its crisis decisions as by its routine policy work. Three episodes capture the institution’s evolution.

The Volcker disinflation of 1979 to 1982 reset the Fed’s credibility on inflation. Paul Volcker, appointed Chair by Jimmy Carter in August 1979, pushed the federal funds rate above 19% in mid-1981 to break the wage-price spiral that had defined the 1970s. The decision triggered a deep recession with unemployment peaking at 10.8% in late 1982, but inflation fell from above 13% in 1980 to below 4% by 1983. Volcker’s willingness to absorb the political cost established the credibility that anchored inflation expectations for the next four decades and gave economists their modern understanding of the Phillips Curve.

The 2008 financial crisis tested the Fed’s role as lender of last resort on a scale not seen since the 1930s. After Lehman Brothers failed in September 2008, the Fed cut rates to near zero, launched three rounds of quantitative easing, and created an alphabet soup of emergency facilities to keep credit flowing. The balance sheet rose from $900 billion in mid-2008 to $4.5 trillion by 2014. Whether the Fed should have moved faster, supported Lehman, or designed exit terms differently remains debated; what is undisputed is that the experience permanently expanded the Fed’s tool set. Our deeper analysis is available in the 2008 financial crisis explained.

The 2020 pandemic response was even larger and faster. Within weeks of the COVID shock, the FOMC cut rates to zero, restarted asset purchases at unprecedented scale, and reactivated almost every Section 13(3) facility from 2008, plus several new ones. The balance sheet doubled from $4.2 trillion in February 2020 to $8.9 trillion by April 2022. The post-pandemic inflation surge that followed forced the most aggressive tightening cycle since Volcker, with the federal funds rate rising from near zero to a 5.25-5.5% range between March 2022 and July 2023. The Fed has since cut rates back toward 4% by early 2026, though pace and timing have been the subject of intense political and market debate.

The chart below shows the federal funds rate across these episodes alongside key policy turning points.

Source: FRED, Federal Reserve Bank of St. Louis; Federal Open Market Committee meeting minutes.

Beyond rate cycles, the March 2023 regional bank failures reminded markets that the Fed’s supervisory and liquidity functions operate continuously. Silicon Valley Bank, Signature Bank, and First Republic failed within weeks, and the Fed responded by creating the Bank Term Funding Program to lend against held-to-maturity Treasury securities at par. The episode reignited debate about supervisory adequacy and the design of the discount window, themes covered in our piece on central banks as lenders of last resort.

The Future of the Federal Reserve

The institution faces three structural challenges that will shape its next decade.

The first is independence. The Fed’s operational autonomy has always rested on a political consensus that monetary policy should be insulated from short-term electoral pressure. That consensus has frayed since 2018, with both Trump administrations openly criticising Fed decisions and exploring the legal limits of presidential authority over the Board. The May 2026 transition has crystallised the question. Powell’s announcement that he would remain on the Board through the end of his Governor term in 2028 was framed by Powell himself as a defence of institutional integrity against a series of legal attacks on the Fed. Whether Kevin Warsh’s Fed maintains the operational independence that markets have priced in for decades is the most significant single question facing the institution. Our analysis of threats to central bank independence covers the legal and economic stakes.

The second challenge is the framework review. The Fed adopted average inflation targeting in 2020, committing to allow inflation to run modestly above 2% after periods below to maintain a 2% average over time. The post-pandemic inflation surge tested that framework severely, and the 2025 framework review revisited several core assumptions. The current Federal Reserve framework still aims at 2% inflation, but the operational meaning of the dual mandate is being rewritten in real time. How the Warsh-led FOMC interprets maximum employment and price stability over the next two years will set the doctrine for the next cycle.

The third challenge is the changing nature of monetary transmission. The federal funds rate still anchors short-term funding, but the channels through which it influences the real economy have shifted. Bank lending matters less than capital markets. Mortgage rates respond to Treasury yields and mortgage-backed security spreads more than to the policy rate directly. Crypto markets, stablecoins, and the rise of non-bank financial intermediaries create new pathways for credit and liquidity that sit partly outside the Fed’s regulatory perimeter. The institution that emerged in 1913 was designed to discipline a banking system. The institution of 2026 must influence a financial system in which banks are only one node.

MASEconomics Explains

Four economic concepts behind the Federal Reserve

Conclusion

The Federal Reserve explained at the institutional level is a system that combines a politically appointed Board, twelve regional Reserve Banks, and the FOMC into a hybrid central bank with a dual mandate of price stability and maximum employment. As of May 2026, it manages a $6.7 trillion balance sheet, operates the dollar-clearing infrastructure that underpins global finance, and supervises the largest banks in the world’s largest economy. The leadership transition from Powell to Warsh, the continuing debate over independence, and the unfinished framework review will shape how the institution responds to the next decade of inflation, employment, and financial stability questions.

Frequently Asked Questions

What is the Federal Reserve in simple terms?

The Federal Reserve is the central bank of the United States. It manages monetary policy, supervises parts of the banking system, supports financial stability, provides payment services, and acts as a lender of last resort during crises. Its most visible job is setting interest-rate policy through the Federal Open Market Committee.

What is the Federal Reserve’s dual mandate?

The Federal Reserve’s dual mandate is to promote maximum employment and stable prices. Maximum employment means the strongest labour market that can be sustained without creating excessive inflation. Stable prices mean keeping inflation low and predictable so households, firms, and financial markets can make long-term decisions with less uncertainty.

How does the Federal Reserve affect interest rates?

The Federal Reserve affects interest rates mainly by setting a target range for the federal funds rate and using monetary tools to keep market rates near that range. Changes in the federal funds rate influence borrowing costs across the economy, including mortgages, business loans, credit cards, bond yields, and asset prices. These channels affect demand, employment, inflation, and financial conditions.

What is the difference between the Fed Board and Reserve Banks?

The Federal Reserve Board is the central governing body in Washington, DC. The regional Federal Reserve Banks operate across different districts and bring local economic information into the system. Together, the Board and Reserve Banks form a hybrid structure that combines national oversight with regional economic representation.

Why is Federal Reserve independence important?

Federal Reserve independence is important because monetary policy often requires decisions that are unpopular in the short run but necessary for price stability. If interest-rate decisions were controlled directly by day-to-day politics, inflation expectations could become less stable. Independence does not mean the Fed is above accountability; it means the Fed has operational space to pursue the mandate given by Congress.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics