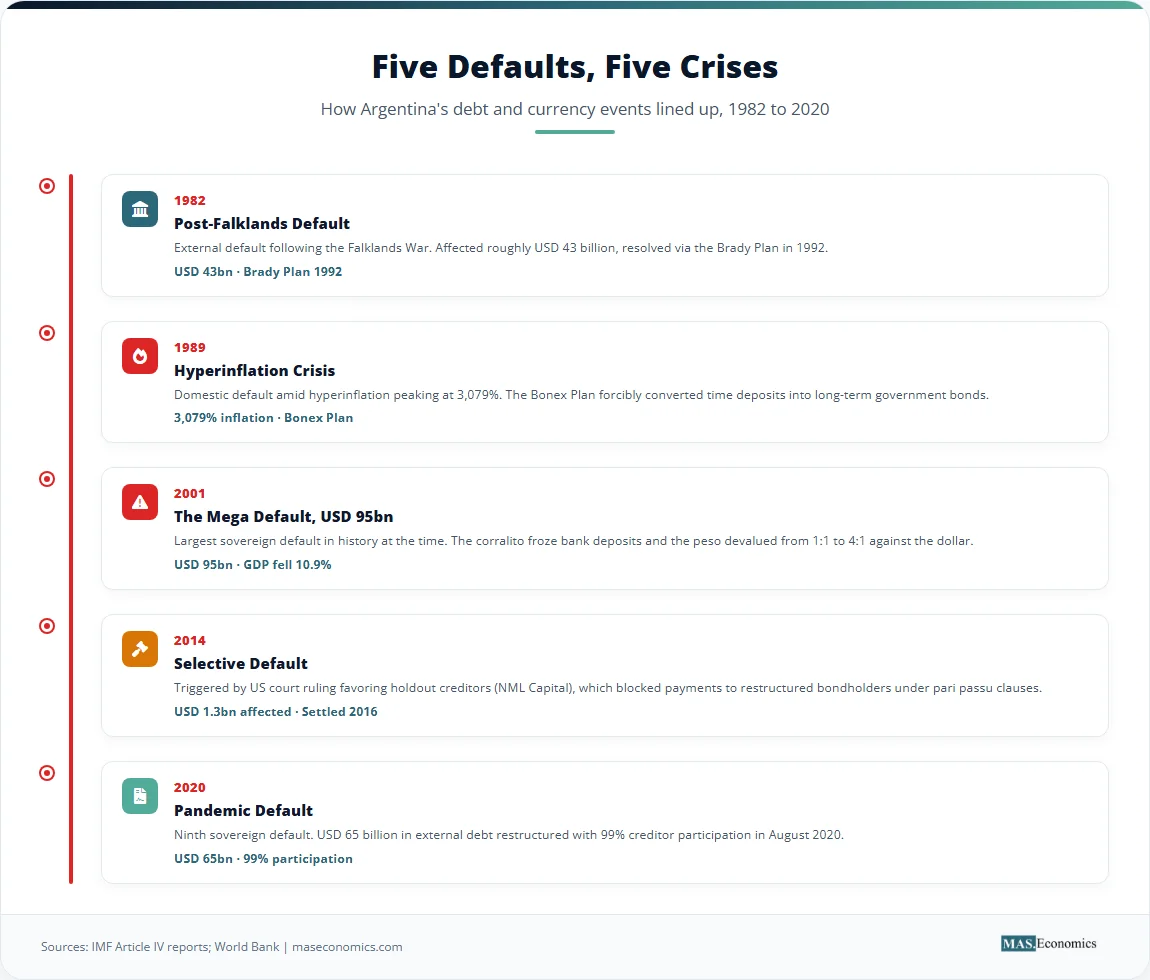

Argentina’s annual inflation rate fell to 31.5% for calendar 2025, the lowest reading since 2017, after peaking at 211.4% in 2023 and 117.8% in 2024. The country has defaulted on external sovereign debt nine times since independence: in 1827, 1890, 1951, 1956, 1982, 1989, 2001, 2014, and 2020. Three of those defaults occurred since the year 2001. The economic record is a sequence of boom-bust cycles anchored in fiscal imbalances and monetary financing.

Argentina’s Recurrent Defaults sit at the centre of modern sovereign-debt economics. The country ran the convertibility experiment in the 1990s, recorded the largest sovereign default in history in 2001, two further defaults in 2014 and 2020, and a shock-therapy stabilisation programme launched in December 2023 that has now received a 23rd IMF arrangement and a US Treasury currency swap. The case provides the empirical ground truth for theories of fiscal dominance, original sin, and hyperinflation dynamics.

Argentina’s experience divides into five policy phases from the 1991 Convertibility Plan to the Milei programme as of early 2026, guided by the Sargent-Wallace fiscal-dominance, Cagan hyperinflation, and original-sin frameworks. The sequence has absorbed and reshaped sovereign-debt theory across three decades, with the 2024–2026 stabilisation adding a new and still-unresolved chapter.

How Argentina’s Crisis Unfolded

The modern Argentine crisis has its roots in the hyperinflation of 1989. Annual inflation reached 3,079% that year, wiping out savings and collapsing output. The political system demanded a radical solution. Economy Minister Domingo Cavallo delivered one. The 1991 Convertibility Law fixed the peso to the US dollar at a one-to-one rate. The central bank was required to hold dollar reserves equal to the monetary base, functioning as an approximation of a currency board. Inflation fell from 84% in 1991 to single digits by 1993. Capital flowed in. Growth returned. The initial success made Argentina a model for fixed-exchange-rate regimes.

The peg hid structural rot. Argentina could not devalue to regain competitiveness, and it could not print pesos to finance deficits because the Convertibility Law prohibited seigniorage financing. Provincial governments issued their own quasi-currencies, called patacones, to pay workers, violating the spirit of the law. Public debt rose from 29% of GDP in 1993 to 53% in 2001. When emerging market contagion spread from the Russian default in 1998 and the Brazilian devaluation in 1999, Argentine exports lost competitiveness. Investors demanded higher risk premiums. The debt trajectory became unsustainable. Argentina had given up the Mundell trilemma tool of monetary autonomy, and fiscal policy was undisciplined.

The collapse was violent. In December 2001, Argentina defaulted on USD 95 billion of external sovereign debt, the largest default in history at the time. The government froze bank deposits to stop capital flight, a measure known as the corralito. The peso was devalued from 1:1 to 4:1 within months. The banking system suffered asymmetric pesification, where dollar loans were converted to pesos at 1:1, but dollar deposits were converted at 1.4:1, destroying bank balance sheets. GDP fell 10.9% in 2002. Poverty rates doubled. The crisis showed the destructive power of exchange rate overshooting when a hard peg shatters.

The restructuring that followed was protracted and legally unprecedented. Argentina offered bondholders a 65% haircut in 2005, with 76% participation. A second exchange in 2010 brought another 17% of holdouts into the deal. The remaining holdouts, including the hedge fund NML Capital, pursued litigation in New York courts. NML argued that Argentine bond contracts contained a pari passu clause, meaning the country could not pay the restructured bondholders while refusing to pay the holdouts. The legal doctrine of sovereign debt sustainability was permanently altered by this dispute.

The litigation came to a head in 2014. US District Judge Thomas Griesa ruled that Argentina could not pay its restructured bondholders unless it also paid the holdouts in full. When Argentina refused, the transfer agent was blocked from processing payments to restructured bondholders, pushing the country into a selective default. The standoff lasted until 2016, when President Mauricio Macri’s administration settled with the holdouts for USD 9.3 billion, ending a decade of financial isolation. Capital markets reopened briefly. Then fiscal deficits returned. The Macri government borrowed heavily in dollar-denominated bonds. When investor confidence faltered in 2018, a sudden stop forced Argentina to seek an IMF bailout of USD 57 billion, the largest in IMF history at that time. The programme failed to stabilise the economy.

The ninth sovereign default occurred in May 2020 under President Alberto Fernández. Argentina restructured USD 65 billion of foreign-law bonds with 99% participation by August 2020. The successful participation rate masked deeper problems. The central bank continued to monetize fiscal deficits through adelantos transitorios, short-term transfers to the Treasury. Inflation accelerated from 36% in 2020 to 211.4% in 2023, the highest reading in the country since 1990 and the highest in the G20.

In December 2023, President Javier Milei took office and launched a shock-therapy programme. He devalued the official peso by 54% on day one, slashed energy and transport subsidies, and froze public works. The fiscal balance moved into surplus in 2024, the first annual primary surplus in over a decade. The economy contracted by about 1.7% in 2024, then rebounded by 4.4% in 2025, according to the World Bank. Quarterly inflation fell from 52% in the first quarter of 2024 to 8.7% in the first quarter of 2025. In April 2025, the IMF approved a 48-month, USD 20 billion Extended Fund Facility, the country’s 23rd IMF programme since 1958, with an upfront disbursement of USD 12 billion. Buenos Aires used the IMF support to lift most capital controls on individuals and let the peso trade within a band of 1,000 to 1,400 pesos per dollar. By October 2025, the US Treasury added a USD 20 billion currency swap line and intervened directly in the peso market ahead of the midterm legislative elections. La Libertad Avanza won 40.8% of the vote in those elections, extending the political runway for the programme. Annual inflation closed 2025 at 31.5% and stood at 32.6% in March 2026 according to INDEC, with poverty falling from a peak of 57% in early 2024 to 14.7% in 2025 on the World Bank’s USD 8.30/day measure.

Economic Mechanisms Driving Default and Inflation

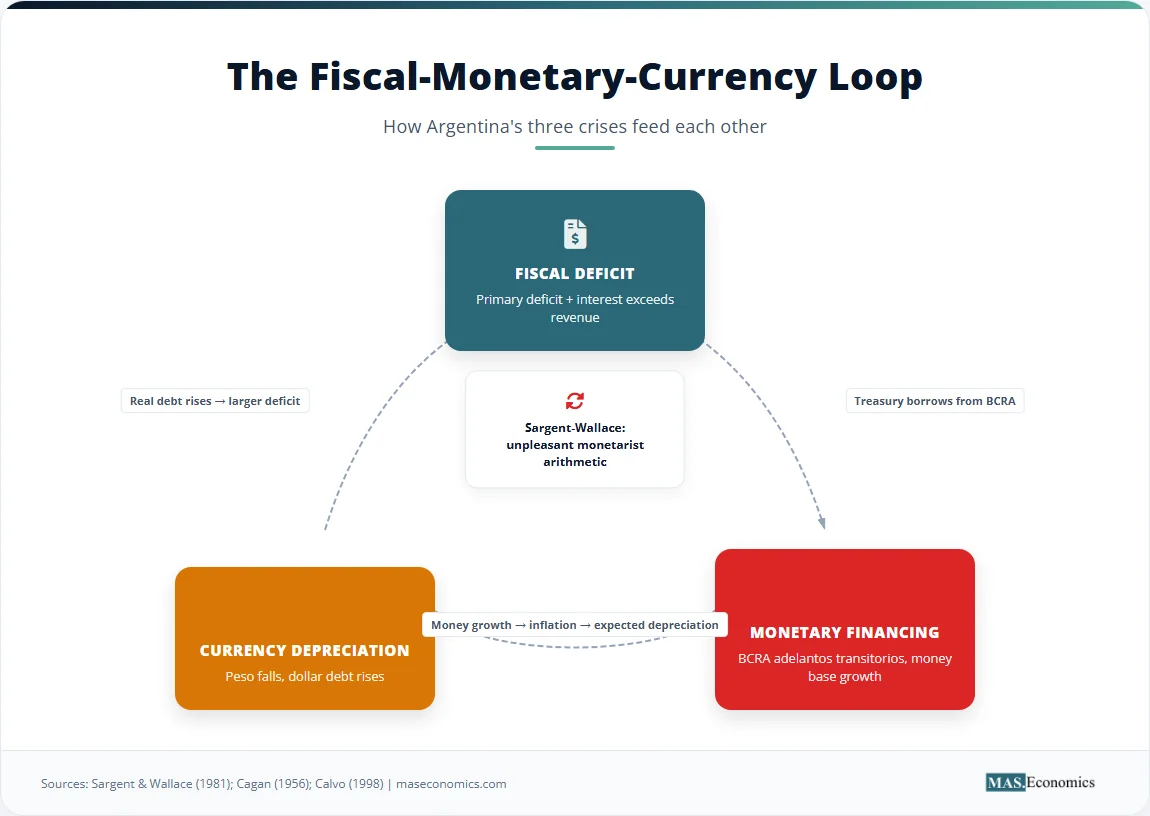

The Argentine case validates several theoretical frameworks that explain why sovereign default and hyperinflation occur together. The core mechanism is the fiscal-monetary nexus. When a government cannot finance its deficits through taxation or sustainable borrowing, the central bank becomes the financier of last resort.

Fiscal Dominance and Seigniorage

Sargent and Wallace (1981) outlined “Some Unpleasant Monetarist Arithmetic” in the Minneapolis Fed Quarterly Review. Their model shows that when fiscal policy is dominant, the central bank loses control over inflation. If the government runs persistent primary deficits, and if the real interest rate exceeds the growth rate of the economy, the debt-to-GDP ratio will rise without bound. Markets will eventually refuse to buy that debt. The central bank must then monetize the deficit. The present value of future seigniorage must equal the present value of future deficits. Argentina violated this constraint repeatedly. The Banco Central de la República Argentina (BCRA) transferred pesos to the Treasury via adelantos transitorios, expanding the monetary base. The money supply growth fed directly into price level increases, a process that accelerated under the Fernández administration and has been the explicit target of the Milei stabilisation: a zero-deficit fiscal rule combined with a strict cap on net domestic assets.

Original Sin

Eichengreen and Hausmann (1999) defined original sin as the inability of emerging markets to borrow abroad in their own currency. Argentine sovereign debt has been overwhelmingly dollar-denominated. This structural feature converts a currency crisis into a debt crisis automatically. When the peso depreciates, the local-currency value of dollar debt rises. A devaluation that might otherwise restore export competitiveness instead bankrupts the government, the banking system, and the corporate sector at once. The 2001 crisis followed this exact pattern. The devaluation from 1:1 to 4:1 quadrupled the peso cost of dollar debt. The government could not pay. Default was the mechanical consequence of sovereign debt sustainability failing under the weight of original sin. Every monetary regime Argentina has adopted since has struggled against this constraint, and the 2025 currency-band design is itself an attempt to manage it.

Sovereign-Debt Models

Eaton and Gersovitz (1981, Review of Economic Studies) and Arellano (2008, American Economic Review) model sovereign default as a strategic choice under incomplete markets. Countries default when the cost of repaying exceeds the reputational cost of losing market access. The cost of repayment is highest during recessions, when output is low and tax revenues fall. Default is therefore procyclical, deepening the recession that triggered it. Arellano’s model predicts that default probabilities rise sharply as debt approaches a threshold determined by output volatility. Argentine output volatility, driven by commodity price swings and policy instability, has kept this threshold low. The country hits the default boundary frequently because its income is unstable and its debt is denominated in a currency it cannot print.

Hyperinflation Transmission

Cagan (1956, Studies in the Quantity Theory of Money) provided the foundational model of hyperinflation dynamics. The Cagan money-demand function specifies that the log of real money demand is a linear, decreasing function of expected inflation.

Here, \( M \) is the nominal money supply, \( P \) is the price level, \( \pi^e \) is expected inflation, and \( b \) is the semi-elasticity of money demand. When the government finances deficits by printing money, \( M \) rises. If \( \pi^e \) adjusts upward, real money demand \( M/P \) falls. To extract the same real seigniorage revenue from a shrinking real money demand base, the government must print even faster. This creates a vicious circle. Argentina traversed the wrong side of the seigniorage Laffer curve in 1989 and again in 2023. The inflation tax became the primary revenue source when other tax collection mechanisms failed. The transition from moderate inflation to hyperinflation episodes occurs when expectations shift faster than the fiscal authority can adjust its primary balance. The reverse mechanism also held in 2024-2025: with money-base growth halted, real money demand recovered, and inflation expectations re-anchored downward.

Sudden Stops

Calvo (1998, Journal of Applied Economics) formalized the sudden-stop mechanism. Capital-flow reversals in dollarized emerging economies trigger debt crises because the current account deficit must adjust instantly. Domestic absorption must fall, causing a recession. The recession reduces tax revenue, worsening the fiscal position. The central bank loses reserves defending the peg, and when reserves are exhausted, the currency collapses. Argentina has experienced sudden stops in 1995 after the Tequila Crisis, in 2001, in 2018, and again in September 2025 ahead of the midterm vote. The 2025 episode is instructive. As the Peronist opposition won the Buenos Aires provincial poll, peso outflows accelerated, and the BCRA burned through reserves to defend the band. The US Treasury’s intervention in October 2025 ended the run, but only by replacing one external lender with another. The central bank balance sheet still requires reserve accumulation to make the regime self-sustaining.

The Macroeconomic Data

The data reveals a clear pattern. Every sovereign default coincides with an inflation surge. The relationship is not coincidental. It is the mechanical outcome of fiscal dominance. When Argentina loses market access, the BCRA steps in to fund the Treasury. The monetary base expands, the peso depreciates, and inflation accelerates. The 1989 hyperinflation peaked at 3,079%, reflecting complete fiscal-monetary collapse. The 2001 default produced lower inflation because the Convertibility Law physically prevented the BCRA from printing, but the regime collapsed entirely. Post-convertibility inflation in 2002 reached 25.9% as the peso floated and depreciated sharply. The 2020 default was followed by the most aggressive monetary expansion, driving 2023 inflation to 211.4%.

The reverse trajectory under Milei is just as informative. Annual inflation fell from 211.4% in 2023 to 117.8% in 2024 and 31.5% in 2025, with monthly readings dipping to 1.5% in June 2025 before drifting back up to around 2.4-2.8% in late 2025. Real GDP rebounded by 4.4% in 2025 after contracting in 2024, and the World Bank projects 3.6% growth for 2026. Poverty, which spiked to about 57% in early 2024 as the devaluation hit real wages, fell to 14.7% in 2025 on the World Bank’s USD 8.30/day measure as disinflation restored purchasing power. Argentina’s trajectory shows that restructuring alone does not solve hyperinflation vs deflation dynamics if the fiscal root cause remains untreated. Stop the deficit, and the inflation engine stalls. Argentina has now done that for two consecutive years for the first time in this century.

The debt dynamics tell a parallel story. External debt rose steadily under convertibility because the government could not print pesos and chose to borrow dollars instead. The debt-to-GDP ratio reached 53% in 2001. After the default and devaluation, the ratio spiked higher in peso terms before restructuring brought it down. The 2020 restructuring addressed the stock, but the flow of new deficits quickly rebuilt the pressure. The April 2025 IMF programme of USD 20 billion, supplemented by USD 12 billion from the World Bank and USD 10 billion from the Inter-American Development Bank, refinances roughly USD 42 billion in obligations. Argentina faces almost USD 20 billion in debt repayments in 2026 alone. The next test is whether reserve accumulation, a precondition of the IMF deal, can be achieved without choking off the recovery.

Five sovereign-default events in 38 years coincided with five inflation surges. The 1989 hyperinflation peaked at 3,079%; the 2023 surge at 211.4%. By 2025 inflation had fallen back to 31.5%. Sources: INDEC; IMF World Economic Outlook October 2025; World Bank.

| Year | Default Type | Debt Affected (USD bn) | Restructuring Outcome |

|---|---|---|---|

| 1982 | External, post-Falklands | 43 | Brady Plan 1992 |

| 1989 | Domestic + hyperinflation | 60 | Bonex Plan 1989 |

| 2001 | External, full default | 95 | 65% haircut, 2005/2010 |

| 2014 | Selective, NML ruling | 1.3 | Settled 2016, USD 9.3 bn |

| 2020 | External | 65 | 99% participation, Aug 2020 |

| |||

What the Argentina Case Means for the Future

A peg without fiscal discipline is a slow-motion default mechanism. The Convertibility Plan ended hyperinflation by removing the printing press, but it left the government with only debt to finance deficits. Since the debt was in dollars, and the government could not print dollars, default was inevitable. Fixed exchange rates require fiscal subordination. Argentina never achieved that under convertibility. The lesson applies to any country considering a hard peg or dollarisation. Monetary anchors cannot substitute for fiscal anchors. The 2025 currency-band design tries to learn the lesson by combining a flexible exchange rate inside a corridor with an explicit zero-deficit rule.

Dollar-denominated debt converts a currency crisis into a debt crisis automatically. Original sin means that depreciation, the standard adjustment mechanism for current account deficits, becomes catastrophic. The local-currency value of debt rises proportionally to the devaluation. For Argentina, the 2001 devaluation from 1:1 to 4:1 quadrupled the peso cost of external debt. Countries that cannot borrow in their own currency must maintain reserve buffers large enough to survive sudden stops, or they must limit external debt to levels sustainable even after a maximum plausible devaluation. Argentina did neither in the 2001 cycle, and the 2018 Macri programme repeated the mistake. The 2025 IMF deal addresses the buffer side of the equation but not the structural composition of debt.

Reputational costs of default decline with repetition. The Eaton-Gersovitz model assumes that default triggers exclusion from capital markets, a penalty strong enough to deter strategic default. The Argentine record shows that the penalty erodes. After nine defaults, markets price in the probability of default continuously. Argentine borrowing costs never returned to emerging-market averages after 2001. Investors demanded high coupons to compensate for the known default risk, and those high coupons made the debt burden heavier, which made the next default more likely. The reputational mechanism broke down because the market learned that Argentina would default, and Argentina learned that the market would lend again after a restructuring.

Holdout creditors and pari passu litigation shape modern restructuring outcomes. The NML v. Argentina case established that holdout creditors can use pari passu clauses to block payments to restructured bondholders. This ruling shifted power from sovereign debtors to creditors. Future restructurings will be shaped by the legal precedent. Collective action clauses, which bind all bondholders if a supermajority agrees, have become standard in sovereign bond contracts to prevent holdout disruptions. The Argentine legal saga was the catalyst for this structural change in international finance.

Stabilisation requires three legs: a fiscal anchor, a monetary regime change, and exchange-rate regime credibility. The Convertibility Plan had a monetary and exchange-rate anchor but no fiscal anchor. The Milei programme has all three by early 2026: a fiscal surplus held for two years, a monetary aggregate target backed by the IMF, and a peso band supported by the IMF and US Treasury swap lines. Monetary regime credibility is being built in real time. Stabilisation is not complete until inflation expectations are re-anchored, which requires consistent fiscal discipline over many years. The Argentine record suggests that achieving all three legs at the same time is rare and that removing any one leg causes the stool to collapse.

MASEconomics Explains

4 economic concepts behind Argentina’s Recurrent Defaults

Conclusion

Argentina’s Recurrent Defaults form the most replicated sovereign-debt crisis sequence in modern economic history. The country moved through five distinct phases: a currency peg that ended hyperinflation but enabled debt accumulation, the largest sovereign default in history in 2001, a protracted legal battle with holdout creditors that reshaped sovereign-debt contracts, a selective default in 2014, and a ninth default in 2020, followed by a surge to 211.4% annual inflation. Theoretical frameworks explain the mechanics: Sargent and Wallace’s fiscal dominance describes why the central bank monetises deficits, Eichengreen and Hausmann’s original sin explains why devaluation triggers default, and Cagan’s hyperinflation model captures the accelerating price spiral when real money demand collapses. The Milei programme has now run for over two years. Annual inflation closed 2025 at 31.5% and stood at 32.6% in March 2026. Real GDP expanded by 4.4% in 2025, poverty fell to 14.7%, and the country received a 23rd IMF arrangement of USD 20 billion in April 2025, supplemented by a USD 20 billion US Treasury swap line in October 2025.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.