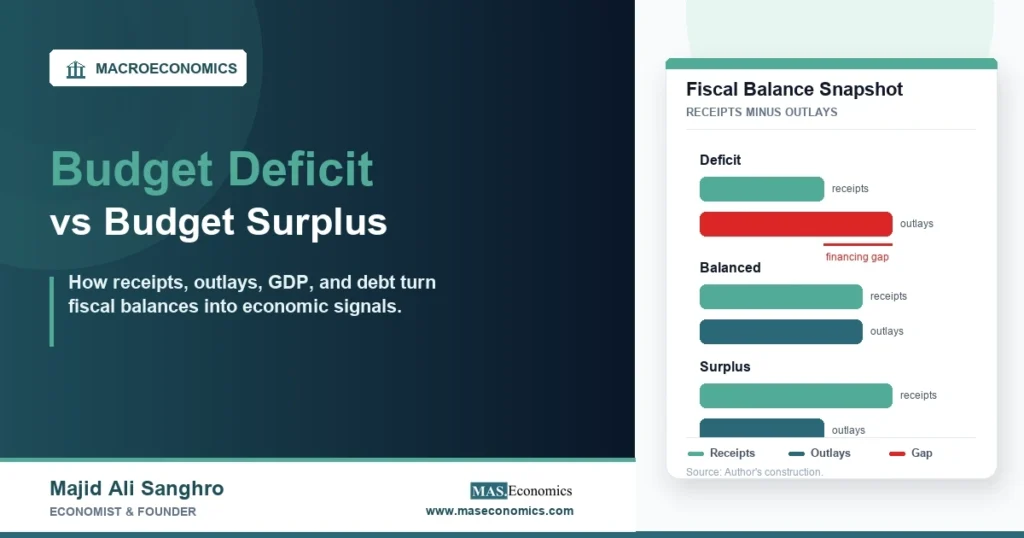

Every fiscal year, governments compare the money they collect with the money they spend, and that comparison produces a balance. A budget deficit means outlays are greater than revenues. A budget surplus means revenues are greater than outlays. A balanced budget means the two sides are equal for the period being measured.

The idea sounds simple, but the meaning of a deficit or surplus depends on what is counted, how the economy is performing, whether interest payments are included, and whether the balance is being compared with GDP. A deficit is not automatically bad, and a surplus is not automatically good. Each one has to be read through the economic conditions and fiscal choices behind it.

The Budget Balance Is a Flow

A government budget balance is a flow, not a stock. It measures the difference between revenues and outlays over a period such as a month, quarter, or fiscal year. Debt is a stock. It measures the accumulated obligations outstanding at a point in time. Confusing the two is one of the most common mistakes in fiscal-policy discussions.

If the result is negative, the government has a deficit. If the result is positive, the government has a surplus. If the result is zero, the budget is balanced. The OECD general government deficit indicator defines the government balance as the balance of income and expenditure, including capital income and capital expenditures, and measures it as a share of GDP. That percentage-of-GDP framing is useful because a $50 billion deficit has a different meaning in a small economy than in a very large one.

The IMF Government Finance Statistics Manual is the broader statistical reference for comparing fiscal accounts across countries. It matters because countries do not always use identical budget boundaries. Some report central government balances, some report general government balances, and some separate cash accounting from accrual accounting. A careful reader asks which government units are included before comparing one country with another.

A Deficit Means Borrowing or Financing Is Needed

A deficit means the government spent more than it collected during the period. The gap has to be financed. In most modern economies, that financing comes mainly from issuing government debt, drawing down cash balances, using accumulated financial assets, or receiving external financing. The MASEconomics article on how governments borrow explains why bonds, bills, and other debt instruments are central to public finance.

Deficits add to debt when they are financed through borrowing, but the relationship is not a perfect one-for-one rule in every accounting system. Timing differences, valuation changes, asset transactions, and off-budget treatment can affect the exact change in reported debt. Still, the core intuition is sound: repeated borrowing to cover budget gaps raises the stock of government liabilities over time.

This is where the MASEconomics guide to debt in the economy becomes relevant. Debt is not only a burden. It is also a claim held by investors, households, banks, pension funds, central banks, or foreign institutions. The same government bond that appears as a liability for the public sector appears as an asset for the holder.

A deficit may finance public investment, wartime spending, disaster response, unemployment benefits, tax cuts, interest payments, or ordinary recurring programs. The economic meaning differs across those cases. Borrowing to build productive infrastructure is not the same as borrowing to cover permanently mismatched recurring spending. The fiscal balance tells that a gap exists. It does not explain the quality of the spending or the durability of the revenue base.

A Surplus Means the Government Takes In More Than It Spends

A surplus means revenues exceed outlays over the period. The surplus can reduce borrowing needs, retire debt, build public financial assets, replenish stabilization funds, or finance future obligations. A surplus can also withdraw purchasing power from the economy because the public sector is taking in more than it is paying out.

Surpluses can arise from strong tax receipts during expansions, temporary revenue windfalls from commodities or asset sales, deliberate spending restraint, tax increases, or underspending caused by administrative delays. The label does not identify the cause. It only records that inflows exceeded outflows for the measured government unit.

A surplus can be sensible when an economy is running hot, inflation pressure is high, debt service is heavy, or a government wants to rebuild fiscal space after a shock. It can be damaging if it is achieved by cutting productive investment, delaying maintenance, underfunding public health, or raising taxes in a weak economy. The economic judgment depends on timing, composition, and the government’s starting position.

Receipts and Outlays Are Not the Same as Policy Intent

Budget outcomes reflect both policy choices and economic conditions. A government can pass a tax cut, raise spending, and widen the deficit by choice. A recession can also widen the deficit even if no new law is passed, because tax receipts fall and safety-net spending rises. A strong expansion can narrow the deficit as incomes, profits, consumption, and employment improve the revenue base.

The Congressional Budget Office budget data separates historical budget data, 10-year projections, long-term projections, revenue projections, spending projections, and estimates of automatic stabilizers. That structure points to a key distinction: observed deficits mix deliberate fiscal policy with the automatic response of the budget to the business cycle.

Automatic stabilizers are built-in budget responses. Income taxes collect less when incomes fall. Unemployment benefits and some transfers rise when labor markets weaken. During expansions, the reverse tends to happen. This is one reason a deficit can widen during a downturn without a new stimulus bill. The MASEconomics article on fiscal policy explains how taxation and spending affect demand, distribution, and long-run capacity.

| Measure | What it includes | Why economists use it |

|---|---|---|

| Headline balance | Total revenues minus total outlays | Shows the reported deficit, surplus, or balance for the period |

| Primary balance | Revenues minus noninterest outlays | Separates current policy from interest costs on past debt |

| Cyclically adjusted balance | Balance adjusted for the business cycle | Helps distinguish temporary cyclical effects from underlying fiscal position |

| General government balance | Central, state, local, and social security funds where applicable | Improves cross-country comparison when government is decentralized |

| Balance as a share of GDP | Budget balance divided by national output | Scales the balance to the size of the economy |

|

|

||

The Primary Balance Separates Interest From Current Choices

The headline deficit includes interest payments on existing debt. That is useful because interest is a real government outlay. But it can blur the difference between current fiscal choices and debt accumulated in earlier years. The primary balance subtracts interest payments from outlays before comparing revenues with spending.

A government can run a headline deficit but a primary surplus if its revenues exceed noninterest spending while interest payments push the total balance below zero. That situation often appears in high-debt economies. It means current taxes and program spending are not the only issue. The inherited debt stock and interest rate environment are also shaping the deficit.

This distinction connects directly to debt sustainability. Debt sustainability is not determined by one year’s deficit alone. It depends on the interest rate on government debt, economic growth, inflation, the primary balance, investor confidence, currency structure, and the maturity profile of borrowing. A small deficit in a stagnant economy can be harder to sustain than a larger deficit in a fast-growing economy with low interest costs.

Deficits Can Stabilize Output, But They Can Also Create Risk

Deficits can support demand during a recession. When households and firms cut spending, public borrowing can prevent a deeper fall in income and employment. This is the countercyclical logic behind fiscal policy. It is also why many governments tolerate larger deficits during wars, financial crises, pandemics, and severe downturns.

Yet persistent deficits can create fiscal risk when they are large relative to the economy and not matched by future revenue capacity or growth. Interest payments can absorb more budget space. Investors may demand higher yields. A government may face less room to respond to the next shock. In countries that borrow in foreign currency or lack monetary credibility, deficit financing can also feed exchange-rate pressure and inflation.

The IMF Fiscal Monitor tracks public finance developments and fiscal risks across countries. Its role is not to declare every deficit dangerous. It is to assess how fiscal positions interact with debt, growth, interest rates, spending pressures, and policy credibility.

The MASEconomics article on fiscal policy vs monetary policy explains this division of tools. Fiscal policy works through taxes, spending, transfers, and borrowing. Monetary policy works through interest rates, liquidity, and central bank balance sheets. Deficits become especially sensitive when fiscal choices begin to constrain monetary credibility or interest-rate decisions.

Debt, GDP, and Inflation Change the Interpretation

A deficit is usually scaled by GDP because GDP approximates the economy’s income base. The MASEconomics guide to gross domestic product explains why GDP is used as a broad measure of output. When analysts say a deficit is 4 percent of GDP, they mean the annual fiscal gap equals 4 percent of annual national output.

That ratio matters because governments service debt from future revenues, and future revenues usually depend on the size and growth of the economy. A growing economy can carry more nominal debt without a rising debt-to-GDP ratio if growth outpaces the effective interest burden and the primary balance is not too weak. A shrinking or slow-growing economy has less room.

Inflation also affects interpretation. Moderate inflation can raise nominal tax receipts and reduce the real value of fixed-rate debt, but high or unstable inflation can raise borrowing costs, weaken confidence, and distort fiscal planning. The MASEconomics article on inflation covers the price-level side of that story.

The World Bank cash surplus or deficit indicator reports fiscal balances as a share of GDP for cross-country comparison. The appeal of that format is simple: it makes large and small economies comparable without pretending that their institutions, currencies, tax bases, and borrowing conditions are identical.

A Surplus Does Not Always Reduce Debt Immediately

A surplus often lowers borrowing needs, but the effect on debt can be complicated. A government may use a surplus to build cash balances, buy financial assets, or reduce outstanding debt. It may also have debt maturing from earlier borrowing that has to be refinanced even during a surplus year. The timing of cash flows and debt management matters.

Public debt management is therefore separate from the annual budget balance. The MASEconomics article on central banks and public debt management explains why maturity structure, market liquidity, interest-rate risk, and institutional coordination affect how borrowing is handled. A country can improve its fiscal balance and still face debt-management pressure if large debts mature soon or interest rates rise sharply.

Surpluses can also coexist with private-sector stress. If the government is taking in more than it spends, some other sector must be spending more than it receives or reducing its net financial assets, once the external sector is included. That accounting identity does not settle policy debates, but it reminds readers that one sector’s balance is connected to the rest of the economy.

How to Read a Deficit or Surplus Carefully

The first question is whether the number is central government or general government. The second is whether it is cash or accrual. The third is whether it is headline, primary, or cyclically adjusted. The fourth is whether the number is reported in currency units or as a share of GDP. Without those details, fiscal comparisons can mislead.

The next question is composition. A deficit caused by a temporary recession is different from a deficit caused by a permanent gap between tax law and promised spending. A surplus caused by efficient revenue collection is different from a surplus caused by cutting maintenance and public investment. The same headline number can hide different economic stories.

The final question is sustainability. A deficit is easier to justify when it finances high-return investment, supports the economy during a downturn, or responds to an emergency. It is harder to justify when it persists during full employment, raises interest costs faster than revenues, or relies on optimistic growth assumptions. A surplus is easier to defend when it rebuilds fiscal space or cools excess demand. It is harder to defend when it weakens growth or pushes costs into the future.

MASEconomics Explains

4 economic concepts behind government balances

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Budget deficit is the term for a negative fiscal balance, while a budget surplus is the term for a positive one. The basic calculation is simple: compare government revenues with government outlays over a specific period.

The interpretation is harder. A deficit can reflect recession, investment, emergency spending, interest costs, or a persistent mismatch between taxes and programs. A surplus can reflect fiscal discipline, a strong economy, temporary windfalls, or underspending that stores problems for later. The relevant economic question is not whether the sign is negative or positive. It is whether the balance fits the economy’s cycle, debt position, policy goals, and long-run revenue capacity.

Frequently Asked Questions

What is a budget deficit?

A budget deficit occurs when government outlays exceed government revenues during a measured period. The gap usually has to be financed through borrowing, cash balances, asset sales, or external support.

What is the difference between a budget deficit and government debt?

A budget deficit is a flow measured over a period, such as a fiscal year. Government debt is a stock measured at a point in time. Repeated deficits can add to debt, but the annual deficit and total debt are not the same number.

Is a budget surplus always good?

No. A surplus can reduce borrowing needs and rebuild fiscal space, but it can also weaken demand or reflect cuts to useful public investment. Its meaning depends on economic conditions, spending quality, revenue sources, and debt pressure.

Why do deficits rise during recessions?

Deficits often rise during recessions because tax receipts fall and some transfer payments rise automatically. Governments may also choose temporary stimulus measures to support income, employment, and demand.

Why is the budget deficit measured as a percentage of GDP?

The deficit-to-GDP ratio scales the fiscal gap to the size of the economy. This makes countries and periods easier to compare because the same currency amount can be small for one economy and large for another.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics