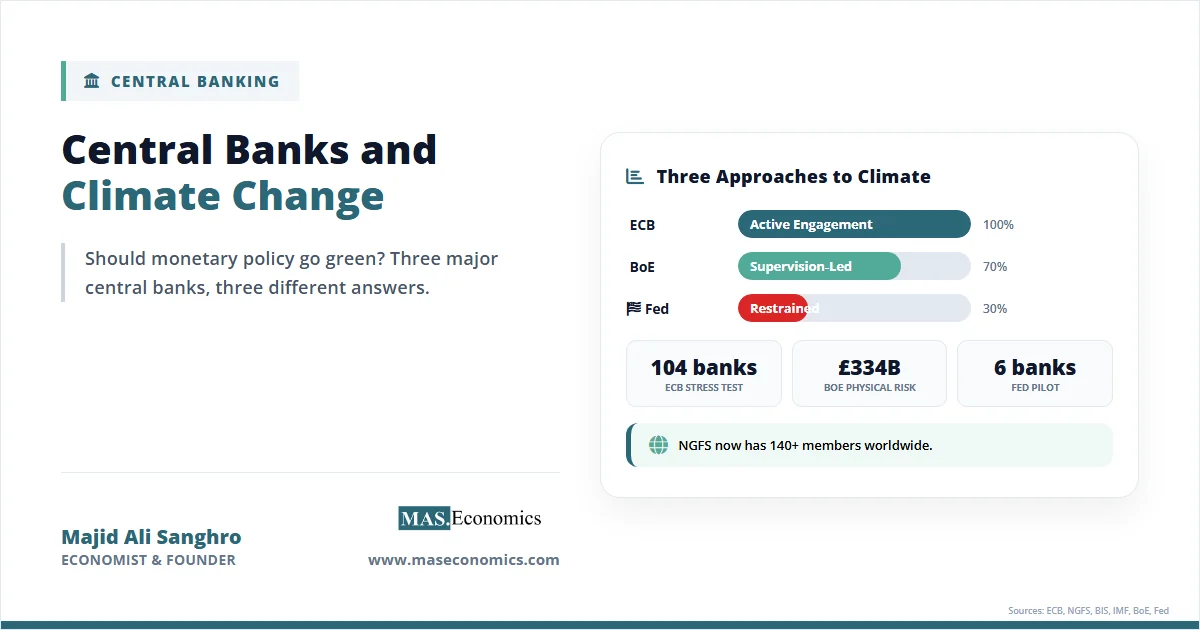

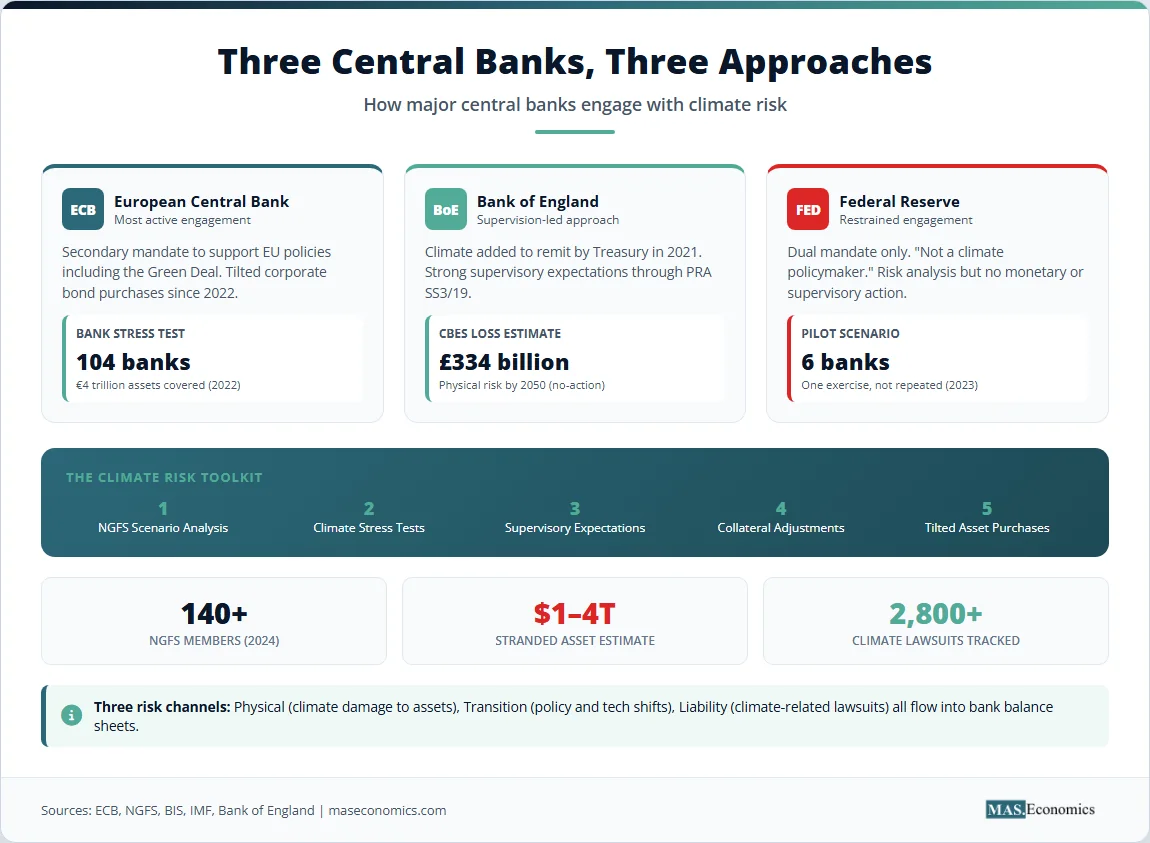

In July 2022, the European Central Bank announced it would tilt its corporate bond portfolio toward issuers with better climate performance, becoming the first major central bank to integrate climate considerations directly into monetary policy operations. By 2024, the Bank of England had completed two rounds of climate stress tests covering banks and insurers worth trillions in assets. The Federal Reserve, meanwhile, ran a pilot scenario analysis with six large US banks but stopped short of integrating climate into supervision. Central banks climate change policy now sits at the intersection of financial stability, monetary mandates, and democratic legitimacy, and the three institutions that anchor the global financial system have arrived at sharply different answers.

The pressure is no longer theoretical. The Network for Greening the Financial System (NGFS), launched in 2017 with eight members, now counts more than 140 central banks and supervisors. Climate-related insurance losses crossed $100 billion annually for the fourth consecutive year in 2024. Stranded fossil fuel assets sit on bank balance sheets worth somewhere between $1 trillion and $4 trillion, depending on the transition scenario. The question is no longer whether climate matters for financial stability. It is how far a central bank can go before it stops being a central bank.

The Tension Driving the Debate

Independent central banks were built on a narrow promise: deliver price stability, free from political pressure, and let elected governments handle distributional choices. Climate policy breaks that boundary. Decarbonisation requires reallocating capital away from carbon-intensive sectors, which is a distributional choice with winners and losers. When a central bank decides which bonds to buy, which collateral to accept, or which banks to penalise in a stress test, it is no longer neutral with respect to the green transition.

This creates a three-way split among major central banks. The ECB has moved most aggressively, citing its secondary mandate to support EU policies, including the European Green Deal. The Bank of England has focused on supervision and stress testing while staying cautious about asset purchases. The Federal Reserve has taken the most restrained position, treating climate purely as a financial risk and refusing to use monetary tools to influence the energy transition. The People’s Bank of China, by contrast, has built one of the world’s largest green credit programmes, driven by industrial policy rather than independence concerns.

The disagreement is not about whether climate change matters. It is about whether unelected technocrats should make the trade-offs that climate policy demands. As discussed in our analysis of green macroeconomics, the boundary between fiscal and monetary policy is already blurring. Climate adds a new layer of complication.

What Climate Risk Actually Means

For central banks, climate change is not primarily an environmental problem. It is a source of financial risk that can destabilise banks, insurers, and the broader system. The NGFS framework, now adopted by most major supervisors, divides this risk into three categories that are worth understanding precisely.

Physical Risk

Physical risk is the direct damage from climate-related events: floods that destroy mortgaged property, droughts that bankrupt agricultural borrowers, hurricanes that wipe out insured assets, and gradual changes such as sea-level rise that erode coastal real estate values. The Bank of England’s 2021 Climate Biennial Exploratory Scenario found that physical risk losses for UK banks and insurers could reach £334 billion under a no-additional-action pathway by 2050. The IMF’s 2023 Global Financial Stability Report estimated that physical risk could reduce bank capital by up to 4% in vulnerable economies.

Physical risk has a particular feature that makes it dangerous for financial stability. It is non-linear. A 2°C warming scenario does not produce twice the damage of a 1°C scenario. Tipping points, such as ice sheet collapse or Amazon dieback, can produce step changes in damage that no historical data can predict. Standard risk and uncertainty models built on normal distributions systematically underestimate these tail events.

Transition Risk

Transition risk is the financial damage caused by the shift to a low-carbon economy. Coal-fired power plants become uneconomic when carbon prices rise. Oil reserves become stranded if vehicle electrification accelerates. Steel mills using blast furnaces lose value if green hydrogen alternatives become viable. The faster and more disorderly the transition, the larger the losses for holders of these assets.

Transition risk is partly a policy choice. A government that imposes a sudden carbon tax creates large transition losses overnight. A government that signals a slow, predictable phase-out creates smaller losses spread over decades. This is precisely why central banks find transition risk politically uncomfortable. By stress-testing for it, they implicitly take a view on what climate policy will look like, and that view shapes which firms appear risky.

Liability Risk

Liability risk arises when parties harmed by climate change seek compensation through the courts. The Sabin Center at Columbia tracks more than 2,800 climate-related lawsuits globally as of 2024, up from a few dozen in 2010. Cases against fossil fuel companies, insurers, and pension funds for failing to disclose or manage climate risk have produced settlements and rulings that change how these firms value their liabilities. For banks lending to defendants in such cases, liability risk translates directly into credit risk.

Why This Matters for Stability

Financial stability is the central bank’s most defensible reason for engaging with climate. If climate risks are not properly priced, they accumulate quietly on bank balance sheets until they trigger losses large enough to cause bank failures, credit crunches, and recessions. The 2008 crisis showed how mispriced risk in one corner of the system, in that case, subprime mortgages, could spread through interconnections to produce a global meltdown. Climate risks could follow a similar pattern, except they are larger, more correlated across geographies, and partly irreversible.

The Bank for International Settlements coined the term “green swan” in 2020 to describe this category of risk: events that are highly uncertain, potentially catastrophic, and not captured by standard models. Green swans differ from the financial black swans of 2008 because they are predictable in direction, even if not in timing. We know warming will continue. We do not know exactly when a tipping point will trigger a sudden repricing of climate-exposed assets.

The link to systemic financial stability is what gives central banks an entry point. Financial stability is part of every major central bank’s mandate, either explicitly (as for the ECB and BoE) or implicitly through their lender-of-last-resort function (as for the Fed). If climate threatens stability, central banks have a duty to act.

The Climate Toolkit Today

Central banks have developed a set of tools that operate at different levels of intervention. Listed roughly from least to most interventionist, they include scenario analysis, climate stress tests, supervisory expectations, collateral framework adjustments, and tilted asset purchases. Each tool raises distinct questions about mandate and effectiveness.

NGFS Scenarios

The NGFS publishes a set of standardised climate scenarios that central banks use as inputs to stress tests and risk analyses. The scenarios cover three families: orderly transition (early, predictable policy action), disorderly transition (late, sudden action), and hot-house world (insufficient action, severe physical risk). Each scenario specifies pathways for carbon prices, energy mix, GDP, and temperature out to 2100.

The scenarios are useful because they let supervisors compare risks across institutions using common assumptions. They are also limited because they assume policy paths that may not materialise and use macroeconomic models that struggle with the non-linearities discussed above. The NGFS itself acknowledges that its scenarios likely understate physical risk in high-warming pathways because the underlying integrated assessment models do not capture tipping points well.

Climate Stress Tests

Climate stress tests apply NGFS or custom scenarios to bank and insurer balance sheets to estimate losses under different climate pathways. The Bank of England ran the first comprehensive exercise in 2021, covering seven banks and ten insurers. The ECB followed with its 2022 stress test of 104 banks. The Fed completed a smaller pilot scenario analysis with six banks in 2023.

Results have been broadly consistent across jurisdictions. Banks face larger losses under disorderly transition than orderly transition, both are smaller than physical risk losses under a hot house scenario, and current capital levels are mostly sufficient to absorb the modelled losses. The honest reading of these results is that they are reassuring on average and worrying in the tails. Average losses are manageable. Concentrated exposures, such as banks with large mortgage books in flood-prone regions, are not.

Collateral Frameworks and Asset Purchases

Collateral frameworks govern which assets a central bank accepts when lending to commercial banks. Adjustments here have been the most contested tool. The ECB announced in 2022 that it would limit the share of high-emission corporate assets accepted as collateral and tilt new purchases under its corporate sector purchase programme toward greener issuers. The Bank of England has incorporated climate into its corporate bond purchase scheme as it unwinds its stock under quantitative easing reversal. The Fed has done neither and has stated it will not.

The contestation is straightforward. Tilting purchases toward green issuers means tilting away from brown issuers, which raises borrowing costs for the latter and lowers them for the former. That is industrial policy. Defenders argue it merely corrects for an existing bias in market neutrality, since standard purchase rules effectively favour high-emission firms that issue more bonds. Critics argue that whatever the justification, the effect is to substitute the central bank’s judgment for elected officials’ judgment on which industries should shrink.

Supervisory Expectations

Supervisory expectations are perhaps the most consequential tool because they reach inside individual banks. Both the ECB and BoE now require supervised institutions to integrate climate risk into governance, strategy, risk management, and disclosure. Banks that fall short face capital add-ons, restrictions on activities, and reputational consequences. The ECB has imposed capital surcharges on banks judged to have weak climate risk practices. The Fed’s approach has been more modest, focused on guidance for the largest banks rather than enforceable expectations.

Three Approaches Compared

The differences between the major central banks are not just stylistic. They reflect different views on the boundaries of monetary policy, different legal mandates, and different political contexts. The branded table below summarises the key dimensions.

| Dimension | ECB | Bank of England | Federal Reserve | People’s Bank of China |

|---|---|---|---|---|

| Mandate basis | Secondary mandate to support EU policies including Green Deal | Secondary objective on climate added by HM Treasury in 2021 | Dual mandate (employment, prices); financial stability via FSOC | Multiple objectives including industrial development |

| Climate stress tests | Top-down 2022 plus bottom-up integration in SREP | Biennial Exploratory Scenario 2021; ongoing supervisory work | Pilot scenario analysis 2023 with 6 banks; not repeated | Required for major banks since 2021 |

| Asset purchase tilting | Yes, since 2022 in corporate bond holdings | Yes, in CBPS unwind decisions | No | Targeted refinancing for green projects |

| Collateral framework | Climate-related limits introduced in 2024 | Risk-based haircuts under review | No climate-specific adjustments | Green bond eligibility expanded |

| Supervisory expectations | Mandatory; capital add-ons for non-compliance | Mandatory through PRA supervisory statement | Guidance for large banks; no formal requirements | Mandatory disclosure and lending targets |

| Green lending facilities | None directly | None directly | None | Carbon Emission Reduction Facility |

|

||||

Sources: ECB monetary policy strategy review (2021, 2024 updates); Bank of England PRA SS3/19; Federal Reserve pilot scenario analysis (2023); People’s Bank of China Green Finance Reports.

The European Central Bank

The ECB’s position is shaped by its dual mandate structure. Its primary mandate is price stability. Its secondary mandate, often overlooked outside European policy circles, requires it to support the general economic policies of the European Union without prejudice to price stability. The European Green Deal, adopted in 2019, makes climate a central EU policy. The ECB’s legal services concluded that integrating climate considerations is therefore not optional but required, provided it does not conflict with price stability.

This legal foundation gave the ECB room to move further than its peers. Its 2021 monetary policy strategy review formally incorporated climate considerations. Its 2022 stress test was the largest ever conducted, covering 104 banks and 4 trillion euros in assets. Its tilted bond purchases, while small in scale relative to overall holdings, were precedent-setting. The 2024 update tightened collateral rules further.

The Bank of England

The BoE has taken a middle path, with supervision more developed than monetary policy interventions. Its remit was updated by the Treasury in 2021 to include support for the government’s climate goals, providing political cover that the Fed lacks. The Climate Biennial Exploratory Scenario produced detailed firm-level results that have shaped supervisory expectations. The Prudential Regulation Authority’s supervisory statement SS3/19 sets binding expectations on climate risk management.

Where the BoE has held back is on the more interventionist tools. Greg Carney, then BoE Governor, championed climate work in his final years, but successor Andrew Bailey has emphasised that the BoE’s primary contribution is risk management rather than transition policy. The unwind of the Corporate Bond Purchase Scheme has incorporated climate criteria, but the BoE has not introduced green lending facilities or substantially altered its core monetary operations.

The Federal Reserve

The Fed’s position is the most restrictive of the major Western central banks. Chair Jerome Powell has stated repeatedly that the Fed is “not and will not be a climate policymaker.” This position rests on three arguments. First, the Fed’s dual mandate from Congress covers maximum employment and price stability, with no climate language. Second, climate policy is the prerogative of elected branches of government, not the central bank. Third, expanding into climate would risk politicising the Fed and undermining its independence.

The Fed has nonetheless engaged with climate as a financial risk. It’s 2023 pilot scenario analysis with six large banks produced detailed loss estimates. It joined the NGFS in 2020. It participates in international supervisory work. But it has stopped firmly short of integrating climate into monetary operations or imposing climate-specific supervisory requirements. As discussed in recent analysis of Fed independence, this restraint is partly defensive: in a polarised political environment, climate engagement provides ammunition to critics who want to constrain the Fed’s autonomy.

The People’s Bank of China

The PBoC operates under a different model entirely. Chinese central bank independence is limited, and monetary policy is used explicitly as a tool of industrial policy. The Carbon Emission Reduction Facility, launched in 2021, provides cheap refinancing to commercial banks that lend to qualifying low-carbon projects. By 2024, the facility had supported more than 1.2 trillion yuan in green loans. The PBoC also incorporates green credit into its macroprudential assessment of banks. This is what climate-aligned monetary policy looks like without the constraints of independence, and it produces faster green capital flows but also more political control.

The Growth of Climate Action

The number of climate-related actions by central banks has grown rapidly since the NGFS was founded. The chart below shows the cumulative count of major climate-related measures across the four institutions discussed above.

Source: NGFS progress reports (2018-2024), individual central bank publications. Measures include stress tests, supervisory statements, collateral framework changes, and asset purchase adjustments.

The pattern is informative. The ECB, BoE, and PBoC have moved on roughly parallel trajectories, accumulating more than a dozen major climate-related measures each by 2024. The Fed has moved much more slowly, with most of its actions concentrated in the technical area of scenario analysis rather than supervisory or monetary intervention. This divergence is consistent with broader patterns of central bank divergence on multiple dimensions of policy.

The Mandate Debate

The most contentious question in this area is whether central bank mandates should be reinterpreted to include climate explicitly, or whether climate engagement should remain limited to financial stability concerns. Five distinct positions have emerged in the academic and policy debate.

The first is the strict price stability view, associated with figures such as former Bundesbank president Jens Weidmann and Fed officials, including Powell. On this view, central banks should focus on their core mandate of inflation control and treat climate only as a source of risk to that objective. Anything more politicises monetary policy and threatens independence.

The second is the financial stability view, which now commands broad consensus across most major central banks. Climate change creates risks to financial stability, and central banks have a duty to ensure that banks and insurers can absorb those risks. This view supports stress testing, supervision, and risk-based collateral adjustments but stops short of using monetary tools to influence the transition.

The third is the market neutrality correction view, advanced by ECB officials and academic economists such as Dirk Schoenmaker. On this view, standard monetary operations are not actually neutral because they replicate market biases. The corporate bond market is dominated by carbon-intensive firms because they issue more bonds. Buying in proportion to issuance, therefore, amplifies the carbon footprint of the central bank’s balance sheet. Tilting purchases toward greener issuers does not introduce a bias; it removes one.

The fourth is the secondary mandate view, which holds that central banks with secondary mandates to support broader economic objectives (as in the EU and UK) are required to consider climate, while those without (such as the Fed) are not. This view emphasises legal and democratic legitimacy as the determining factor.

The fifth is the activist view, advanced by figures including Adam Tooze and various NGOs, which holds that the climate emergency justifies using all available tools, including monetary policy, even if this stretches mandates. Critics call this position the road to politicisation. Defenders call it the road to survival.

Democratic Legitimacy Concerns

Behind the technical debate lies a constitutional question. Central banks are powerful but unelected institutions whose legitimacy depends on a narrow remit clearly delegated by elected legislatures. Climate policy is one of the most contested political domains. If central banks decide which industries get cheaper credit and which face capital surcharges, they are making distributional choices that traditionally belong to elected officials.

This concern has weight even for those sympathetic to climate action. Three risks stand out. The first is mission creep. Once a central bank engages with one major societal challenge, it becomes harder to refuse engagement with others, from inequality to housing affordability to demographic decline. The second is capability. Central bankers are trained in monetary economics and financial supervision, not energy systems or climate science. Their judgments on the green transition may be confidently wrong. The third is accountability. If climate-related interventions produce bad outcomes, voters cannot remove central bankers the way they can remove politicians.

The defenders of climate engagement have responses to each. On mission creep, they argue that climate is unique in its threat to financial stability, which is already a core central bank function. On capability, they note that central banks rely on outside expertise (climate scientists, energy analysts) just as they rely on labour economists for unemployment forecasts. On accountability, they point to the long history of independent central banks operating with formal oversight from legislatures and courts.

The honest assessment is that both sides have a point. Central bank independence was a hard-won institutional achievement of the late twentieth century, and it should not be treated lightly. At the same time, refusing to engage with a quantifiable financial risk because the topic is politically sensitive would itself be a political choice, just one disguised as restraint.

What Climate Engagement Cannot Do?

Even the most ambitious climate-aligned monetary policy cannot substitute for fiscal action. A central bank that tilts its corporate bond portfolio toward green issuers shifts borrowing costs at the margin. A government that imposes a carbon tax of $100 per tonne changes the relative price of every fossil fuel transaction in the economy. The fiscal lever is orders of magnitude larger than the monetary one.

This matters because climate engagement by central banks can create the illusion of action that substitutes for the real thing. If voters and legislators see the ECB tilting bond purchases and conclude that the climate problem is being handled, they may apply less pressure for the carbon taxes, regulations, and public investment that actually drive decarbonisation. The 2024 IMF working paper on this topic estimated that even fully optimised central bank climate policies would deliver less than 5% of the emissions reductions needed to meet Paris targets.

A second limitation is the trade-off with primary mandates. If pursuing climate objectives forces a central bank to keep policy looser or tighter than price stability requires, the cost is paid in inflation or unemployment. The inflationary effects of green energy policies show that the transition itself is not costless in terms of prices, and central banks may face uncomfortable choices when transition shocks push inflation up.

A third limitation is uncertainty. The NGFS scenarios, for all their sophistication, encode large assumptions about future policy, technology, and behaviour. A central bank that designs its operations around specific scenarios risks being wrongfooted when reality diverges, as it almost certainly will. The history of monetary policy suggests that humility about forecast accuracy is well placed.

Where the Debate Is Heading

Several developments will shape this area over the next few years. The ECB’s strategy review in 2025-2026 will determine whether the institution doubles down on climate integration or pulls back under political pressure. The BoE’s third climate stress test, scheduled for 2025, will refine the methodology and expand coverage. The Fed under future leadership may either maintain its current restraint or shift, depending on the political environment and judicial constraints. As discussed in our analysis of central bank balance sheets, the line between monetary and fiscal action continues to blur in ways that will affect climate policy.

On the supervisory side, the convergence around NGFS scenarios and Basel-coordinated standards is likely to continue, even if monetary tools remain divergent. International cooperation on climate-related disclosure, through the IFRS Sustainability Standards Board and the Financial Stability Board’s task force, will reduce the scope for regulatory arbitrage and make it easier for central banks to compare risks across jurisdictions. The work on climate adaptation economics is also feeding directly into supervisory frameworks, particularly on the physical risk side.

The bigger question is whether the political economy of climate will allow central banks to maintain even their current positions. In Europe, opposition to climate-aligned monetary policy has come mainly from the political right, which has gained ground in several member states. In the US, climate engagement by financial regulators has become a partisan flashpoint, with state-level pushback against ESG-aligned investment policies. A future Fed that engaged with climate would face determined political opposition; a future ECB that stepped back from climate would face the opposite.

MASEconomics Explains

Four economic concepts behind central banks and climate change

Conclusion

Central banks climate change policy now sits on a spectrum from active engagement (ECB, PBoC) to deliberate restraint (Fed), with the BoE somewhere in between. Each position reflects a defensible reading of mandate, risk, and democratic legitimacy. The technical case for treating climate as a financial risk is strong and is now broadly accepted across the major central banking community. The case for using monetary tools to influence the transition is more contested and turns on legal mandates, political context, and assessments of effectiveness.

The empirical record supports three conclusions. First, climate stress tests reveal real concentrations of risk that warrant supervisory attention. Second, the marginal impact of monetary tools on the transition is small compared with fiscal policy. Third, the divergence among major central banks reflects genuine differences in mandate and politics rather than just different views on climate science. The choice each central bank has made is consistent with its institutional environment, even when those choices conflict.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.