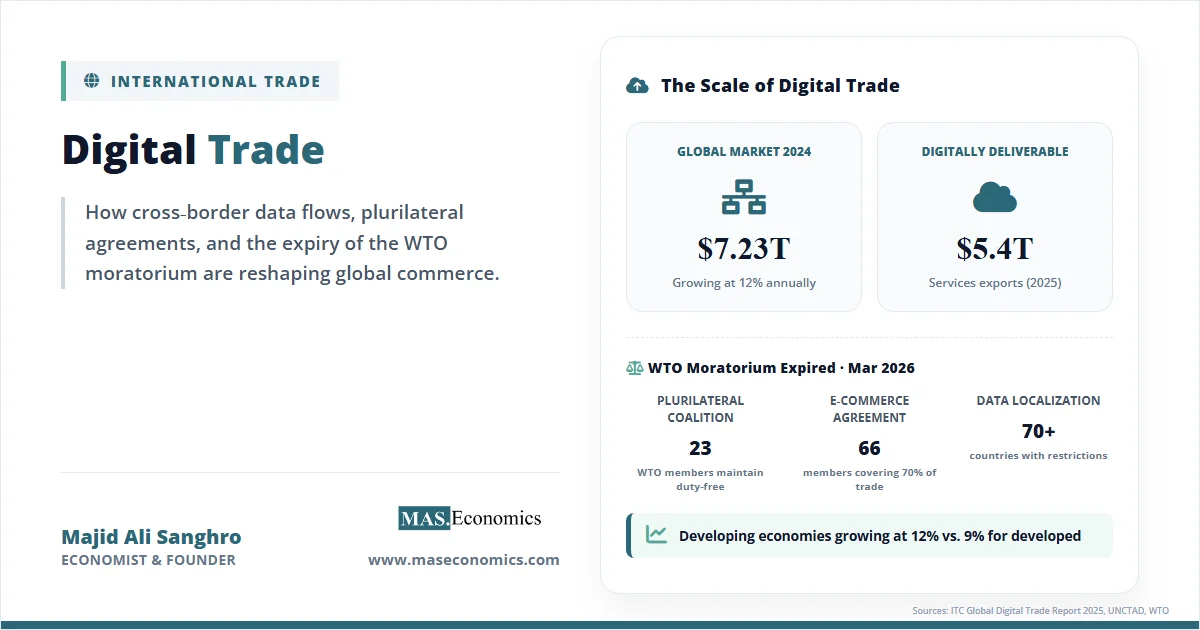

A software developer in Bangalore uploads code to a repository hosted in California. A manufacturer in Stuttgart runs a digital twin of its factory on cloud servers in Singapore. A small fashion brand in Lagos sells directly to consumers in London through a platform that handles payments, logistics, and customs documentation. None of these transactions involves shipping containers, bills of lading, or customs brokers in the traditional sense. Yet all of them constitute international trade. Digital trade, the cross‑border exchange of goods and services enabled by electronic means, has grown to $7.23 trillion in 2024, expanding at 12% annually, roughly twice the pace of traditional trade. It now accounts for approximately 22% of all international commerce, a share that understates its true economic significance, given that digitally enabled services increasingly underpin manufacturing and logistics.[reference:0]

Digital trade is not a niche category within international commerce. It is the connective tissue of the modern global economy. In 2025, digitally deliverable services, everything from cloud computing and financial services to software licensing and consulting, accounted for $5.4 trillion in global exports, a 10% increase over the previous year. Three‑quarters of these exports originated from developed economies, valued at roughly $4.1 trillion, while developing economies exported an estimated $1.3 trillion. The growth rate in developing economies, however, reached 12%, notably faster than the 9% recorded in advanced economies.[reference:1] Cross‑border e‑commerce platforms now facilitate between $500 billion and $1 trillion in annual transactions, a figure projected to expand significantly as mobile‑first adoption accelerates across Southeast Asia, Africa, and Latin America.

Digital trade has moved from a niche concern to a central front in the broader debate over the future of globalization. The same forces reshaping physical global supply chains are also fragmenting the digital economy along geopolitical lines. Understanding this shift requires examining the scale of digital trade, the fracturing of the global regulatory landscape following the expiry of the WTO e‑commerce moratorium, the divergent approaches of the United States, European Union, and China, and the implications for developing economies seeking to capture a larger share of digitally delivered value.

The Scale of Digital Trade

Measuring digital trade presents unique statistical challenges. The International Trade Centre, working with the IMF, OECD, UNCTAD, and WTO, has developed a framework that distinguishes between digitally ordered trade (e‑commerce), digitally delivered trade (services transmitted electronically), and digital platforms that facilitate transactions. The Global Digital Trade Development Report 2025 finds that digital trade grew from $4.59 trillion in 2020 to $7.23 trillion in 2024, an average annual increase of 12.1%, exceeding the 9.7% growth rate of traditional trade.[reference:2] Digitally delivered services, which include financial services, telecommunications, computer and information services, intellectual property charges, and research and development, have shown particular resilience, with exports rising for a third consecutive year.

Services trade overall expanded strongly in 2025. Telecommunications, computer, and information services exports grew by 11% in 2025, marking the third consecutive year of double‑digit expansion. Financial, insurance, and other business services exports gained 10% as digitally tradable products become ever more internationally traded. In contrast, transport services, the backbone of traditional goods trade, grew by a modest 2% amid tariff changes and shipping‑route security concerns.[reference:3] This divergence between digital and physical trade underscores a structural shift: the fastest‑growing components of international commerce no longer require container ships or cargo planes.

Regional disparities in digital trade participation remain stark. Developed economies account for three‑quarters of digitally deliverable exports, with knowledge‑intensive services comprising roughly 65% of European services exports and nearly 70% of North American services exports. Asia and Oceania show greater diversification, with travel and transport representing about 45% of total services exports. Africa and Latin America remain heavily reliant on travel and transport, which account for over 60% of services exports in Africa and just under 60% in Latin America and the Caribbean.[reference:4] This pattern reflects persistent gaps in digital infrastructure, skills, and regulatory frameworks that limit the ability of developing economies to compete in knowledge‑intensive digital services.

The digital trade ecosystem extends beyond direct services exports. E‑commerce platforms, cloud infrastructure providers, payment processors, and logistics networks form an interconnected architecture that enables even small firms to access global markets. The ITC report highlights that digital trade is no longer a complement to traditional trade but a key driver of innovation, competitiveness, and inclusive growth.[reference:5] Services value added now represents more than one‑third of the content embedded in manufacturing exports, underscoring the centrality of design, logistics, and digital functions in modern competitiveness. The evidence suggests that deglobalization is not occurring; rather, trade is being rewired along digital pathways.

| Region | Digitally Deliverable Exports 2025 ($B) | YoY Growth (%) | Knowledge‑Intensive Share of Services Exports (%) |

|---|---|---|---|

| Developed Economies | ~4,100 | 9 | 65–70 |

| Developing Economies | ~1,300 | 12 | Variable (Asia higher, Africa lower) |

| Europe | ~1,600 (est.) | 8–10 | ~65 |

| North America | ~1,800 (est.) | 8–10 | ~70 |

| Asia and Oceania | ~900 (est.) | 10–12 | ~55 (ex‑travel/transport) |

| Latin America & Caribbean | ~200 (est.) | 6–8 | <40 |

| Africa | ~100 (est.) | 5–7 | <35 |

|

|||

The End of the WTO E‑Commerce Moratorium

For nearly three decades, the WTO moratorium on customs duties on electronic transmissions provided a stable, predictable environment for digital trade. First adopted in 1998 and renewed biennially, the moratorium prohibited WTO members from imposing tariffs on digital products, cloud services, software downloads, e‑books, streaming services, and the countless other intangible goods that traverse borders electronically. On March 31, 2026, that era ended. The moratorium officially expired following the failure of members to reach consensus at the 14th WTO Ministerial Conference in Yaoundé, Cameroon.[reference:6]

The impasse reflected deep divisions between developed and developing economies. Brazil, supported by India and several other developing countries, opposed a lengthy extension, arguing that the moratorium denies them potential tax revenue estimated in the billions of dollars annually that could be invested in domestic digital infrastructure. The United States pushed for a longer extension of five years, while other members sought a four‑year renewal. In the end, no consensus emerged.[reference:7] The failure to extend the moratorium also led to the expiry of the safeguard against non‑violation complaints under the TRIPS Agreement.

In the absence of a multilateral agreement, a fragmented plurilateral approach is emerging. A group of 23 WTO members, including the United States, the United Kingdom, the European Union, Singapore, Australia, South Korea, and Japan, has agreed among themselves to maintain a duty‑free regime on digital trade.[reference:8] This “coalition of the willing” operates outside the WTO consensus framework, effectively creating a two‑tier system where some countries guarantee duty‑free digital trade while others retain the legal right to impose tariffs.

Source: ITC Global Digital Trade Development Report 2025, UNCTAD (2026) | MASEconomics.com

Three Competing Visions

The expiry of the WTO moratorium accelerates a broader trend: the fragmentation of digital trade governance along geopolitical lines. The OECD’s Digital Services Trade Restrictiveness Index catalogues regulations affecting digital trade in 129 countries, showing broad heterogeneity in regulatory restrictiveness across countries and regions. Digital trade policy is increasingly tied to national security, supply chain resilience, and geopolitical alignment, not just economic efficiency. Three distinct approaches have emerged.

The United States has pursued a strategy of promoting open digital markets combined with aggressive restrictions on data flows involving perceived adversaries. In 2025, the U.S. introduced new regulatory regimes restricting cross‑border data flows involving China and other “countries of concern.” Executive Order 14117 and the Protecting Americans’ Data from Foreign Adversaries Act have redefined export restrictions on bulk data transfers and data brokerage.[reference:11] At the same time, the U.S. has championed the WTO E‑Commerce Agreement and joined the 23‑member plurilateral coalition maintaining duty‑free digital trade. This dual‑track approach, promoting liberalization among allies while restricting flows with adversaries, reflects the securitization of digital trade policy.

The European Union occupies a middle ground. The EU’s Digital Omnibus Package, published in November 2025, signals a shift toward simplifying the EU’s digital regulatory framework to enhance competitiveness and foster innovation. The package includes a Data Union Strategy aimed at increasing high‑quality data availability for AI development, streamlining EU data rules, and strengthening the EU’s global position on international data flows.[reference:12] Simultaneously, the EU has advanced binding digital trade agreements that ensure free data flows while preserving regulatory autonomy. The EU‑Singapore Digital Trade Agreement, which entered into force on February 1, 2026, includes provisions ensuring the free flow of data across borders for business purposes while prohibiting data localization requirements.

China’s approach represents a third model: state‑led digital development with controlled liberalization. China has eased cross‑border data flow restrictions through Free Trade Zone “negative lists” and issued extensive new rules on data security and cross‑border transfers. At the same time, China is aggressively expanding its digital trade footprint through platforms like Shein, Temu, and Alibaba, which have captured significant shares of global e‑commerce. China’s digital trade surplus exceeded $1 trillion in 2025, and the country hosted the Fourth Global Digital Trade Expo in Hangzhou, signaling its ambition to shape global digital trade norms.

The divergence in regulatory approaches has direct implications for exchange rates and capital flows. As policy paths among the Federal Reserve, European Central Bank, and People’s Bank of China diverge, digital trade flows are increasingly influenced by monetary policy spillovers transmitted through currency markets.

The New Frontier of Trade Policy

At the center of digital trade governance lies the question of cross‑border data flows. Data has been described as the oil of the digital economy, but unlike oil, data is non‑rivalrous; its use by one party does not diminish its availability to others. This characteristic makes data flows fundamentally different from trade in physical goods, and it explains why data governance has become one of the most contentious issues in international economic relations.

The global trend, however, is toward greater restriction. The number of data localization measures requirements that data be stored and processed within national borders has increased sharply over the past five years. As of 2025, more than 70 countries have enacted some form of data localization requirement. India’s data protection framework, Vietnam’s cybersecurity law, and Indonesia’s personal data protection law all impose varying degrees of localization. Even liberal economies are introducing restrictions: the UK’s Data (Use and Access) Act 2025 introduces a new risk‑based test for international transfers, while the U.S. has restricted data flows involving China. These measures reflect genuine concerns about privacy, national security, and law enforcement access, but they also fragment the global digital marketplace, raising costs and creating compliance burdens that fall disproportionately on smaller firms.

The Indo‑Pacific region has become a laboratory for competing digital trade frameworks. The Comprehensive and Progressive Agreement for Trans‑Pacific Partnership (CPTPP) includes high‑standard digital trade provisions that explicitly prohibit customs duties on electronic transmissions and establish disciplines on data localization. The Digital Economy Partnership Agreement (DEPA), initiated by Singapore, Chile, and New Zealand, provides a modular framework for digital trade cooperation that other countries can join incrementally. ASEAN’s Digital Economy Framework Agreement, negotiations for which were substantially concluded in 2025, aims to harmonize digital trade rules across ten Southeast Asian economies.

The proliferation of overlapping frameworks creates both opportunities and risks. On the one hand, it allows like‑minded countries to advance digital trade liberalization without waiting for a universal consensus. On the other hand, it creates a patchwork of incompatible standards that increases compliance costs and fragments the global digital marketplace. These developments reflect a broader shift toward economic integration at the regional rather than multilateral level, a pattern visible across both digital and physical trade.

Developing Economies and the Digital Divide

For developing economies, digital trade presents both unprecedented opportunity and significant risk of exclusion. The ITC report finds that digital trade growth is being driven by online orders of goods and services delivered over the internet, with participation widening but persistent gaps in connectivity, payments, logistics, and compliance. Some developing countries have made notable progress. India and the Philippines have strengthened their positions in business‑process and digital‑service exports. Several African economies have expanded their digital service export capabilities, though from a low base.

UNCTAD’s 2025 report on accelerating e‑commerce and digital trade reform finds that while reform is moving from assessment to action, implementation remains slow and uneven. Approximately 70% of assessed countries have adopted national e‑commerce or digital economy strategies, but fewer than half have established formal implementation and monitoring mechanisms. Roughly 40% of developing countries lack data protection or privacy laws, and about one‑third lack comprehensive electronic signature and transaction laws. The digital divide manifests not only in infrastructure but in institutional capacity.

Regional initiatives offer a partial solution. The African Continental Free Trade Area’s e‑commerce protocol aims to harmonize digital trade rules across the continent and promote cross‑border payment systems. The Pacific Islands Forum has developed a regional digital economy strategy enabling small island states to share data center infrastructure. ASEAN’s Digital Economy Framework Agreement provides a template for Southeast Asian integration. These regional approaches allow smaller economies to pool resources, harmonize standards, and amplify their voice in global negotiations.

Services trade offers a potential pathway for developing economies to diversify their export baskets beyond commodities and low‑value manufacturing. The “servicification” of manufacturing means that even countries without advanced digital sectors can benefit from digital trade by improving the efficiency of their logistics, design, and business services. The challenge is to build the institutional and human capital required to compete in knowledge‑intensive services, a challenge that requires sustained investment in education, digital infrastructure, and regulatory reform.

Artificial Intelligence and the Next Wave of Digital Trade

Artificial intelligence is emerging as a transformative force in digital trade. The ITC report highlights AI as the new frontier, with advances in open‑source models lowering barriers for small firms and revamping supply chains, pricing, and customer service. AI‑driven services require global markets to scale, but fragmented regulations can become barriers to market access. The United States is pushing commercialization, Europe is prioritizing regulation, and China is betting on scale approaches that will shape the competitive landscape for years to come.[reference:13]

The integration of AI into digital trade raises new regulatory questions. How should AI‑generated content be treated under intellectual property rules? What data governance frameworks are needed to facilitate cross‑border AI training while protecting privacy and security? Should AI services be subject to the same trade rules as other digitally delivered services, or do they require specialized provisions? These questions are only beginning to be addressed in trade agreements. The WTO E‑Commerce Agreement does not specifically address AI, and regional agreements have taken divergent approaches.

AI also has the potential to reduce barriers to digital trade participation. Machine translation tools lower language barriers. AI‑powered logistics optimization reduces shipping costs. Automated customs documentation and compliance tools simplify cross‑border transactions. AI‑driven market intelligence helps small firms identify export opportunities. These applications could democratize access to global markets, particularly for micro, small, and medium‑sized enterprises in developing economies. The broader economic impact of AI remains uncertain, as explored in our analysis of the AI productivity paradox.

MASEconomics Explains

Four concepts behind digital trade

Digitally Deliverable Services

Services that can be delivered remotely over computer networks, including financial services, telecommunications, computer and information services, intellectual property charges, and professional services. In 2025, global exports of digitally deliverable services reached $5.4 trillion, growing at 10% annually.

WTO E‑Commerce Moratorium

A commitment by WTO members, first adopted in 1998 and renewed biennially, not to impose customs duties on electronic transmissions. The moratorium expired in March 2026 after members failed to reach consensus on extension. Twenty‑three members have formed a plurilateral coalition to maintain duty‑free digital trade among themselves.

Data Localization

Requirements that data be stored and processed within national borders rather than transferred internationally. More than 70 countries have enacted some form of data localization requirement, reflecting concerns about privacy, national security, and law enforcement access. Such measures raise costs and fragment the global digital marketplace.

Plurilateral Agreement

A trade agreement among a subset of WTO members rather than all 166 members. The WTO E‑Commerce Agreement, adopted by 66 members covering 70% of global trade, uses interim arrangements to bring digital trade rules into force without requiring full consensus. Plurilateral agreements allow like‑minded countries to advance liberalization while consensus remains elusive.

Key Takeaway and Conclusion

Digital trade reached $7.23 trillion in 2024, growing at 12% annually — twice the pace of traditional trade. Digitally deliverable services account for $5.4 trillion in exports, with developing economies growing at 12% versus 9% for developed economies. Africa and Latin America remain reliant on travel and transport services, while Europe and North America dominate knowledge‑intensive digital exports.

The WTO e‑commerce moratorium expired in March 2026, introducing legal uncertainty and potential tariff exposure. In response, 23 WTO members formed a plurilateral coalition to maintain duty‑free digital trade, and 66 members are advancing the WTO E‑Commerce Agreement through interim arrangements.

Regulatory fragmentation is accelerating. The US combines open digital markets with restrictions on data flows to adversaries. The EU pursues free data flows while simplifying its digital rulebook. China expands digital trade through state‑led development and controlled liberalization. Over 70 countries have enacted data localization requirements. The Indo‑Pacific hosts competing frameworks: CPTPP, DEPA, and ASEAN’s Digital Economy Framework Agreement.

Implementation of digital trade reforms remains slow. Fewer than half of countries with e‑commerce strategies have formal implementation mechanisms; roughly 40% lack basic data protection laws. Regional initiatives offer partial solutions, but multilateral cooperation is necessary to prevent fragmentation from imposing disproportionate costs on smaller economies.

Digital trade is the defining force of globalization’s next phase.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.