A food delivery rider in Shanghai completes fourteen orders during a nine-hour shift, guided by an algorithm that determines every route, every pickup, and every payout. Across the Atlantic, a driver in California switches between three platforms to piece together a living, classified as an independent contractor under a state proposition that remains contested a decade after its passage. In Delhi, gig workers navigate an opaque wage structure where weekly incentive targets shift without notice. These scenarios reflect the central reality of the gig economy in 2026: it has grown into a multi-trillion-dollar global industry, yet the rules governing it remain fragmented, contested, and increasingly shaped by algorithmic systems that operate largely beyond public scrutiny.

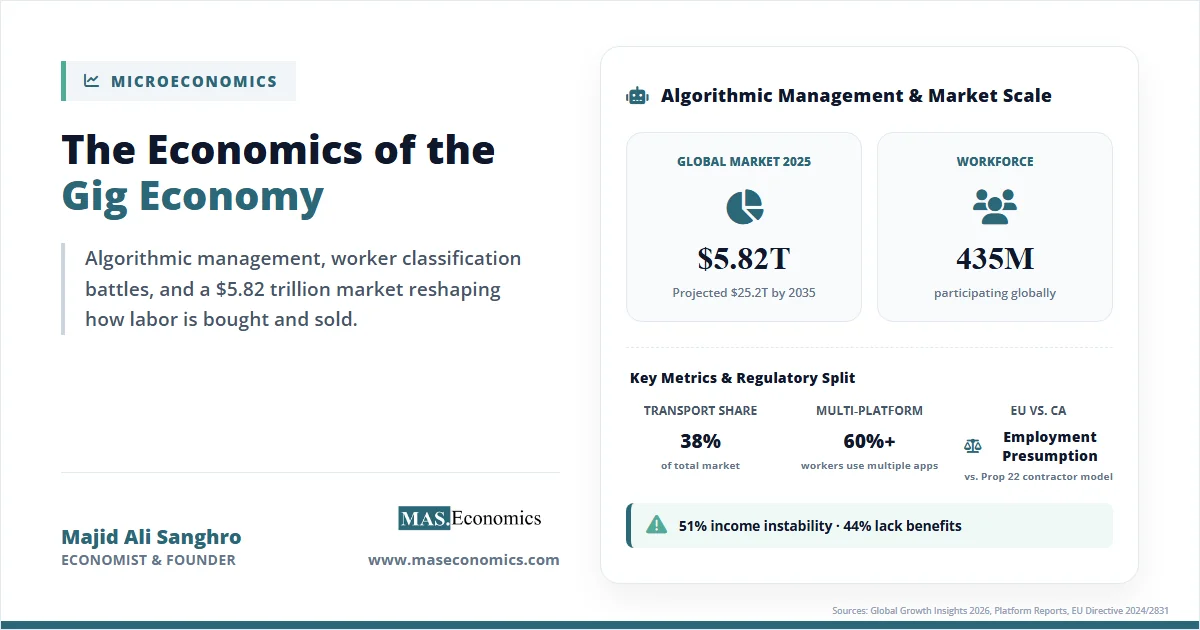

The economics of the gig economy represent one of the most significant transformations in labor markets since the Industrial Revolution. What began as a niche arrangement for freelancers and creative professionals has expanded into a dominant mode of work organization across transportation, delivery, professional services, and household tasks. The global gig economy was valued at $5.82 trillion in 2025 and is projected to reach $25.22 trillion by 2035, growing at a compound annual rate of 15.79%. This expansion is driven by digital platform adoption, with nearly 60% of gig workers participating across multiple platforms and approximately 52% of consumers regularly using on-demand services.

Understanding the economics of the gig economy requires examining three interconnected dimensions: the scale and structure of gig labor markets, the algorithmic systems that allocate work and set wages, and the regulatory battles over worker classification that will determine whether the gig economy evolves toward greater worker protections or deeper precarity.

The Scale and Structure of the Gig Labor Market

The gig economy encompasses a diverse range of work arrangements, from ride-hailing and food delivery to freelance professional services and microtask platforms. This heterogeneity makes precise measurement challenging. The McKinsey Global Institute estimates that the independent workforce is some 162 million people, or up to 30% of the working-age population in the United States and most of Europe. Online gig work accounts for approximately 4.4% to 12.5% of the global labor force, with the gig workforce growing three times as fast as traditional employment.

Geographically, the gig economy is concentrated in three major regions. North America accounts for 34% of the global market ($1.98 trillion in 2025), driven by high platform utilization and flexible labor participation. The Asia-Pacific region represents 31% of the market ($1.80 trillion), fueled by rapid smartphone penetration and digital payment adoption. Europe holds a 27% share ($1.57 trillion), with strong freelance participation in skilled professional services. The Middle East and Africa account for the remaining 8% ($466 billion).

Sectoral composition reveals the dominance of transportation and delivery services. Transportation accounts for 38% of the gig economy ($2.21 trillion in 2025), encompassing ride-hailing, food delivery, and last-mile logistics. Professional services, including IT, design, consulting, and marketing freelancers, represent 24% of the market. Asset-sharing platforms, such as short-term accommodation rentals, contribute 22%. Household and miscellaneous services make up 10%.

Demographic patterns show pronounced generational differences. Millennials constitute 45% of the gig workforce, Gen X 27%, Gen Z 15%, and Baby Boomers 9%. In the United States, McKinsey’s 2023 American Opportunity Survey found that 36% of employed respondents, equivalent to 58 million Americans identify as independent workers. About 10.2% of U.S. workers rely on gig work as their primary income source, while the majority (over 60%) use it to supplement other earnings. Two-thirds of gig workers report monthly earnings below $2,500, though more than 20% earn over $100,000 annually in high-skill professional services.

| Platform | Primary Sector | 2025 Gross Bookings/Revenue | Active Workers | Business Model |

|---|---|---|---|---|

| Uber | Ride-hailing, Delivery | $193B gross bookings | 9.7M active drivers | Commission (driver payout $854B) |

| DoorDash | Food delivery | $3.4B Q3 2025 revenue | ~2M active dashers | Commission + delivery fees |

| Lyft | Ride-hailing | $1.7B Q3 2025 revenue | ~1.4M active drivers | Commission |

| Airbnb | Accommodation sharing | $12.2B 2025 revenue | ~5M hosts | Host + guest service fees |

| Upwork | Freelance professional | $3.8B 2025 revenue | 18M+ freelancers | Commission (10-20% sliding scale) |

|

||||

The financial scale of leading gig platforms underscores their economic significance. Uber, the largest platform globally, generated $193 billion in gross bookings in 2025 with 202 million monthly active users and 9.7 million active drivers. Driver payouts, the single largest cost category, reached $854 billion. Uber’s adjusted operating profit margin approached 10%, reflecting the maturation of its platform economics. DoorDash and Lyft have followed similar trajectories, with DoorDash generating $3.4 billion in Q3 2025 revenue and Lyft delivering $1.7 billion in the same quarter. These platforms achieved profitability not primarily through operational efficiency but through sophisticated pricing algorithms that extract surplus based on real-time demand signals.

Algorithmic Management

The defining feature of gig economy labor markets is not flexibility but algorithmic control. Unlike traditional employment, where managers set schedules, evaluate performance, and determine compensation, platform workers are managed by automated systems that allocate tasks, monitor behavior, set prices, and calculate wages. This shift from human supervision to algorithmic governance has profound implications for labor market efficiency, worker autonomy, and income distribution.

Research on algorithmic management reveals a consistent pattern. A longitudinal study of 1.5 million Uber trips across 258 drivers in the United Kingdom found that after the introduction of dynamic pricing, driver pay decreased, Uber’s commission share increased, job allocation became less predictable, earnings inequality between drivers widened, and drivers spent more time waiting for assignments. The study concluded that the platform’s promise of flexibility was contingent on drivers’ ability to anticipate algorithmic behavior, a task for which platforms provide limited transparency.

The mechanisms of algorithmic control extend beyond pricing. Platforms deploy automated monitoring systems that track worker location, speed, acceptance rates, and customer ratings. These metrics feed into opaque scoring systems that determine which workers receive priority access to high-value assignments and which face reduced opportunities or account deactivation. Research on food delivery riders in China found that algorithmic control erodes workers’ sense of career sustainability and autonomy while tightening the link between pay and performance.

The information asymmetry between platforms and workers is stark. Wages are determined algorithmically, fluctuating according to variables that platforms choose to prioritize. Workers receive little to no explanation of how their earnings are calculated, what factors influence task allocation, or why incentives change. This opacity leaves workers unable to optimize their labor supply strategically and limits their ability to contest unfavorable outcomes.

Algorithmic management also produces gender-based disparities. A ZEW study of over 23,000 online workers found that women earn around 30% less per hour from online freelancing than men, a gap wider than in traditional job markets. The gender earnings gap persists across all platform types, with women concentrated in already gender-biased occupations such as childcare and tutoring. Algorithmic biases and safety concerns further constrain women’s participation in higher-paying sectors such as ride-hailing and delivery.

Source: Global Growth Insights (2026) | MASEconomics.com

The Classification Battleground

The most contentious economic question in the gig economy concerns worker classification. Traditional labor law distinguishes between employees, who are entitled to minimum wage, overtime pay, unemployment insurance, workers’ compensation, and collective bargaining rights, and independent contractors, who receive none of these protections. Gig platforms have built their business models on classifying workers as independent contractors, a designation that shifts the costs of benefits, insurance, and tax compliance onto workers themselves while insulating platforms from employment-related liabilities.

Two jurisdictions illustrate the divergent paths that classification debates have taken: the European Union and California. The EU has moved decisively toward a presumption of employment for platform workers. The EU Platform Work Directive (Directive (EU) 2024/2831), adopted on October 23, 2024, establishes a legal presumption that platform workers are employees unless platforms can prove otherwise. Member states must transpose the Directive into national law by December 2, 2026. The Directive operates through three pillars: determining correct employment status, ensuring transparency and human oversight in algorithmic management, and improving transparency for cross-border work. Under the new regime, the platform, not the worker, must disprove the existence of an employment relationship.

California represents the opposite trajectory. Proposition 22, passed by voters in 2020 and upheld unanimously by the California Supreme Court in 2025, classifies app-based drivers as independent contractors rather than employees. The measure was a direct response to Assembly Bill 5 (AB5), which had codified a strict “ABC test” for employment classification that would have required platforms to treat drivers as employees. Proposition 22 carved out an exception for transportation network companies, allowing them to maintain independent contractor classification while providing limited benefits, including a minimum earnings guarantee and health insurance subsidies for drivers who work sufficient hours.

The economic stakes of classification are substantial. Approximately 51% of gig workers report income instability as their primary concern, and 44% cite limited access to benefits, including health insurance, paid leave, and retirement support. Misclassification deprives workers of protections that employees receive by default: minimum wage guarantees, overtime compensation, unemployment benefits, and workers’ compensation for job-related injuries. For platforms, employee classification would fundamentally alter their cost structure. Uber’s driver payouts of $854 billion in 2025 represent the largest single cost category; adding employer payroll taxes, benefits contributions, and overtime obligations would substantially reduce platform profitability.

Flexibility Versus Precarity

The gig economy’s most frequently cited benefit is flexibility. Workers can choose when, where, and how much to work, a feature that approximately 65% of gig workers identify as a primary motivation for participating in platform labor. This flexibility is particularly valued by workers with caregiving responsibilities, students balancing work and education, and individuals seeking supplemental income. About 20% of full-time U.S. independent workers serve clients abroad, reflecting the global reach of platform-mediated labor markets.

However, flexibility comes with significant economic trade-offs. Approximately 51% of gig workers face unpredictable income streams, 44% lack access to employment benefits, and 33% encounter compliance issues related to tax obligations and worker classification. The financial unpredictability of gig work requires workers to build emergency savings, budget carefully, manage their own tax payments, and create independent retirement plans. In developing countries, half have no retirement plan, and in some regions, over 70% have no personal savings to rely upon during income disruptions.

Productivity effects are similarly mixed. Digital platforms improve matching efficiency between workers and tasks, reducing search costs and idle time relative to traditional labor markets. Approximately 57% of businesses report that gig arrangements enable faster scaling and specialized talent access. Labor flexibility supports productivity improvements of approximately 39%, driving higher platform engagement and cross-industry participation. Yet the short-term nature of gig assignments can reduce worker engagement and firm-specific human capital accumulation, potentially lowering long-term productivity growth.

The economic significance of the gig economy extends beyond direct employment effects. From an economic perspective, the gig economy reduces transaction costs, enables labor market adaptability, and fosters entrepreneurship. It allows firms to convert fixed labor costs into variable costs, increasing operational flexibility and reducing financial risk during demand fluctuations. The gig economy also serves as a buffer during economic transitions, absorbing workers displaced from traditional sectors and providing income during job searches. However, it simultaneously contributes to the erosion of job security, weakens collective bargaining power, and increases income volatility. For a deeper analysis of how gig work intersects with broader digital inequalities, see our article on the gig economy and the digital divide.

What Comes Next: Automation, Regulation, and the Future of Gig Work

The gig economy stands at an inflection point. Three forces will determine its trajectory over the next decade: automation, regulatory convergence, and the evolution of worker organization.

Automation represents the most significant long-term disruption to gig labor markets. Uber is actively integrating autonomous vehicles into its platform, with plans to offer driverless rides in 15 cities globally by the end of 2026 and a goal of becoming the largest autonomous ride-hailing platform by 2029. The company has partnered with over 20 autonomous vehicle developers, positioning itself as an aggregator of self-driving technology rather than a manufacturer. This strategy allows Uber to leverage its existing user base, routing algorithms, and payment infrastructure while gradually replacing human drivers with autonomous fleets.

Regulatory convergence is accelerating. The EU Platform Work Directive establishes a template for jurisdictions seeking to extend employment protections to gig workers while preserving platform flexibility. Its presumption of employment, algorithmic transparency requirements, and cross-border applicability create a regulatory floor that will influence legislation globally. The International Labour Organization has also agreed to develop binding global standards on decent work in the platform economy, a significant step toward international regulatory coordination.

The gig economy’s growth trajectory remains robust. With a projected market size of $25.22 trillion by 2035 and a workforce that will likely exceed half a billion participants, platform-mediated work has become a permanent feature of global labor markets. The economic challenge is to design regulatory frameworks that preserve the efficiency gains and flexibility that platforms enable while ensuring that workers receive adequate protections, predictable incomes, and pathways to economic security.

MASEconomics Explains

Four concepts behind the economics of the gig economy

Algorithmic Management

The use of automated systems to allocate tasks, monitor performance, set prices, and calculate wages. Unlike traditional managerial supervision, algorithmic management operates at scale with limited transparency. Research shows it can increase efficiency while eroding worker autonomy, reducing pay predictability, and widening earnings inequality.

Worker Classification

The legal determination of whether a worker is an employee (entitled to minimum wage, benefits, and protections) or an independent contractor (bearing their own costs and risks). The EU Platform Work Directive presumes employment unless platforms prove otherwise. California’s Proposition 22 preserves contractor status while granting limited collective bargaining rights.

Information Asymmetry

A situation where one party in a transaction possesses more or better information than the other. In gig markets, platforms control the algorithms that determine task allocation and wages, while workers receive little transparency into how these decisions are made. This asymmetry enables platforms to extract surplus and leaves workers unable to optimize their earnings strategically.

Precarity

A condition of economic insecurity characterized by unpredictable income, lack of employment benefits, and absence of long-term stability. Approximately 51% of gig workers report income instability, and 44% lack access to benefits. Precarity is the primary economic cost of gig work arrangements, offsetting the flexibility gains that attract workers to platforms.

Key Takeaway and Conclusion

The economics of the gig economy reveals a fundamental tension between efficiency and equity. Digital platforms have reduced transaction costs, improved labor market matching, and created flexible work opportunities for hundreds of millions of workers globally. The sector’s growth from $5.82 trillion in 2025 to a projected $25.22 trillion by 2035 reflects genuine economic demand for on-demand services and flexible labor arrangements. Platforms have achieved profitability through algorithmic systems that extract surplus based on real-time demand signals and information asymmetries that favor platform owners over workers.

Algorithmic management represents the most significant departure from traditional employment relationships. Research consistently demonstrates that while automated systems improve operational efficiency, they also reduce pay predictability, widen earnings inequality, and intensify work effort. The opacity of algorithmic decision-making prevents workers from optimizing their labor supply strategically and limits their ability to contest unfavorable outcomes. Regulatory interventions such as the EU Platform Work Directive and California’s hybrid classification model represent efforts to rebalance power between platforms and workers.

The classification debate remains unresolved. The EU’s presumption of employment and California’s contractor-plus-bargaining model offer competing visions of how to extend protections to gig workers. The outcomes of these regulatory experiments will shape labor policy globally over the next decade. Automation adds another layer of uncertainty. The gradual replacement of human drivers with autonomous vehicles will eliminate millions of gig work opportunities while improving platform profitability.

The gig economy is not a temporary phenomenon but a permanent restructuring of labor markets. Its economic significance extends beyond direct employment effects to encompass productivity growth, income distribution, and the balance of power between capital and labor in the digital age. The challenge is to harness the efficiency gains of platform-mediated work while ensuring that the benefits are broadly shared and that workers retain meaningful economic security.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.