Welcome to MASEconomics, your guide to the world of economics. Explore the diverse field of economics through our blog series—perfect for learners, students, and enthusiasts.

Let’s begin with our first post, “Introduction to Economics.”

What is Economics?

Economics is a social science discipline that investigates how individuals, businesses, governments, and societies allocate scarce resources to satisfy their unlimited desires and needs. This field of study encompasses a vast array of subjects, from the decisions we make every day to the macroeconomic trends that shape entire economies. Understanding economics is crucial for deciphering the intricate interactions underpinning our economic systems.

Definition of Economics

Let’s consider definitions provided by some of the most reputable economists in history:

Adam Smith is often called the “Father of Economics.” He believed that economics is about how people and businesses make decisions about using limited resources to get what they want. He thought it was it’s essential to be efficient in using resources.

Alfred Marshall had a different view of economics. He thought it was about how people use money and other things to improve their lives. He believed that supply and demand, how much people want something and how much it costs to make it, are essential factors in how much things cost.

John Maynard Keynes was one of the most influential economists of the 20th century. He believed that economics is about how people make choices when they don’t have enough of something they need. He thought that the government should help out during tough times.

Milton Friedman was another vital economist. He agreed with Keynes that economics is about making choices when you don’t have enough of something. But he thought the government should stay out of the way and let people and businesses make their own choices.

Finally, Paul Samuelson thought that economics is how people use resources to make things they want and need. He believed it’s essential to think about how we’ll use things in the future, not just today.

These economists had different ideas about what economics is and how it works. But they all agreed that it’s an important subject that helps us understand how the world works.

Let’s understand whether economics is a science or an art.

To determine whether economics qualifies as a science, we can assess it against a set of essential characteristics:

| Criterion | Explanation |

|---|---|

| Systematic Body of Knowledge | Economics encompasses a structured and organized body of knowledge that is systematically taught and studied. |

| Cause & Effect Relationship | Similar to other sciences, economics explores relationships between cause and effect. Concepts like the Law of Demand illustrate these relationships. |

| Capable of Measurement | Economics uses tangible measures like money to quantify and analyze economic phenomena, enhancing its scientific nature. |

| Methodological Apparatus | Economics employs methods such as induction and deduction, showcasing its methodological apparatus and scientific approach. |

| Ability to Forecast | Economics often involves forecasting future trends and events, demonstrating its practical application and scientific validation. |

|

|

Hence, economics indeed qualifies as a science. But our exploration doesn’t end here. Economics embraces positive and normative perspectives, creating a dynamic and multifaceted discipline.

In economics, we often encounter two types of statements: Positive Economic Statements and Normative Economic Statements. Understanding the difference between them is crucial for objectively analyzing economic phenomena.

Positive Economic Statements

The Factual Perspective

Positive economic statements are statements about how the economy actually works. They are based on observable data and are verifiable. Positive economic statements do not express opinions or make judgments about what should be.

For example, the statement “An increase in the minimum wage led to a decrease in employment among low-skilled workers in the fast-food industry” is a positive economic statement. It is based on data that shows that the minimum wage was increased and that employment among low-skilled workers in the fast-food industry decreased.

Normative Economic Statements

The Value-Based Perspective

Normative economic statements are statements about how the economy should work. They are based on values and opinions, and they cannot be verified. Normative economic statements express what ought to be desirable in the economic world.

For example, the statement “The government should provide free healthcare to all citizens as a basic human right” is a normative economic statement. It is based on the value that healthcare is a basic human right, and it cannot be verified because it is a matter of opinion.

Positive vs. Normative Economic Statements

| Positive Economic Statements | Normative Economic Statements |

|---|---|

| Facts and data-based statements about economic phenomena. | Value judgments and opinions about how things should be in the economy. |

| Can be objectively tested and verified. | Cannot be objectively tested and verified; depends on individual perspectives. |

| Descriptive and focused on what is. | Prescriptive and focused on what ought to be. |

| Example: “Unemployment rate is 5%.” | Example: “Government should increase minimum wage.” |

|

|

|

It is important to distinguish between positive and normative economic statements because they have different implications. Positive economic statements can be used to make predictions about how the economy will change. Normative economic statements cannot be used to make predictions, but they can be used to make decisions about how to improve the economy.

Economic Models

Economic models are simplified representations of the economy that help economists understand how different parts of the economy relate to each other and how they might change.

Just as a map helps us navigate a physical space, an economic model helps us navigate the economic landscape. Economic models are like blueprints for the economy. They show the essential parts of the economy (or variables) and how they connect. They visually explain economic ideas and results using math, graphs, and diagrams.

For example, if a government decides to change a policy, economists can use a model to predict what might happen next. This is like predicting what will happen to your house if you move a wall – you’d look at your blueprint first!

Some of the most common economic models include:

- The supply and demand model explains how the price of a good is determined by the interaction of how much people are willing to buy (demand) and how much is available to be bought (supply).

- The circular flow model shows how money, goods, and services flow through an economy. It has two main sectors: households and businesses. Households provide factors of production (land, labor, capital, and entrepreneurship) to businesses in exchange for income. Businesses use these factors of production to produce goods and services, which they sell to households in exchange for money.

The production possibility curve: This model shows the maximum combinations of goods and services that an economy can produce given its scarce resources.

The game theory model: This model studies how people interact strategically in situations where their choices affect each other.

Economic models are not perfect. They make assumptions to simplify the real world. However, they are still useful tools for understanding the economy. By understanding the assumptions of a model, we can better interpret its results.

Economic Models Assumptions

| Assumption | Description |

|---|---|

| Ceteris Paribus | This Latin phrase, translating to “all other things being equal,” is frequently used by economists to isolate the impact of a specific variable while holding other variables constant. |

| Rational Behavior | Numerous economic models rest on the assumption that individuals and firms behave rationally, maximizing their utility or profits. Although this assumption streamlines decision-making, it may not always mirror real-world behavior. |

| Perfect Information | Some models presuppose that all economic agents possess complete and accurate market information, enabling optimal decisions. In reality, information could be limited or asymmetric. |

| Fixed Preferences | Models might assume that individuals’ preferences remain unchanging over time, despite the fact that preferences can evolve due to various factors. |

| No Externalities | Certain models overlook externalities or spillover effects resulting from economic activities, even though such externalities are commonplace in real-world markets. |

|

|

|

Microeconomics and Macroeconomics

Microeconomics and macroeconomics are two branches of economics that help us understand how economies work. They’re like two sides of a coin, each focusing on different aspects of the economy but interlinked in many ways.

Microeconomics

The Close-Up View

Microeconomics is like using a microscope to examine individual parts of an economy. It focuses on how households, consumers, businesses, and industries decide how to use their limited resources. Here are some key concepts in microeconomics:

Macroeconomics

The Big Picture

Macroeconomics is like looking at the economy from a bird’s eye view. It studies the overall economy, focusing on national income, output, unemployment, inflation, and economic growth. Here are some key concepts in macroeconomics:

The Interplay Between Microeconomics and Macroeconomics

The decisions individuals and firms make in microeconomics shape the big picture macroeconomics looks at. For example, the total supply of goods and services in the economy (a macroeconomic concept) depends on the production decisions of individual firms (a microeconomic concept).

Microeconomics vs. Macroeconomics

| Aspect | Microeconomics | Macroeconomics |

|---|---|---|

| Focus | Individuals, firms, markets | Economy as a whole |

| Scope | Specific behavior and decisions | Aggregate economic trends |

| Price Level | Individual prices | Average price level |

| Unemployment | Individual job markets | Overall unemployment rate |

| Inflation | Price changes of specific goods | Overall inflation rate |

| Income Distribution | Individual income distribution | National income distribution |

| Policy Focus | Market behavior, individual choices | Monetary, fiscal policies |

| Example | Demand for a specific product | National GDP growth |

|

|

||

Scarcity and opportunity cost are two of the most important concepts in economics. They shape the way individuals, businesses, and societies decide how to use their limited resources.

Scarcity

The Dilemma of Limited Resources

Scarcity is the fundamental economic problem that arises from the fact that resources are limited, but our wants and needs are unlimited. This means that we have to make choices about how to use our resources.

For example, a farmer has a limited amount of land, labor, and capital. The farmer can use these resources to grow corn, wheat, or soybeans. However, the farmer cannot grow all three crops at the same time. The farmer must make a choice about which crop to grow.

Opportunity Cost

The Value of What You Give Up

The opportunity cost of something is the value of the next best alternative that we give up when we choose that thing. In the case of the farmer, the opportunity cost of growing corn is the potential profits from growing wheat or soybeans.

Here are some other examples:

Schooling vs. Work: A student who decides to study instead of work gives up the wages they could have earned. These lost wages are the opportunity cost of studying.

Time Management: If you spend an hour studying instead of doing something fun, the opportunity cost is the enjoyment you give up.

Investment Decisions: If you invest in stocks instead of bonds, the opportunity cost is the potential profit you could have made from bonds.

Trade-Offs and Rational Decision-Making

Because of scarcity and opportunity cost, we always have to make trade-offs. We weigh the benefits and costs of our options and choose the one that offers the most net benefit or utility. This is what economists call rational decision-making.

In the case of the farmer, the farmer must decide which crop to grow based on the expected profits from each crop. The farmer will choose the crop that offers the highest expected profit.

In the world of economics, NOTHING IS FREE!

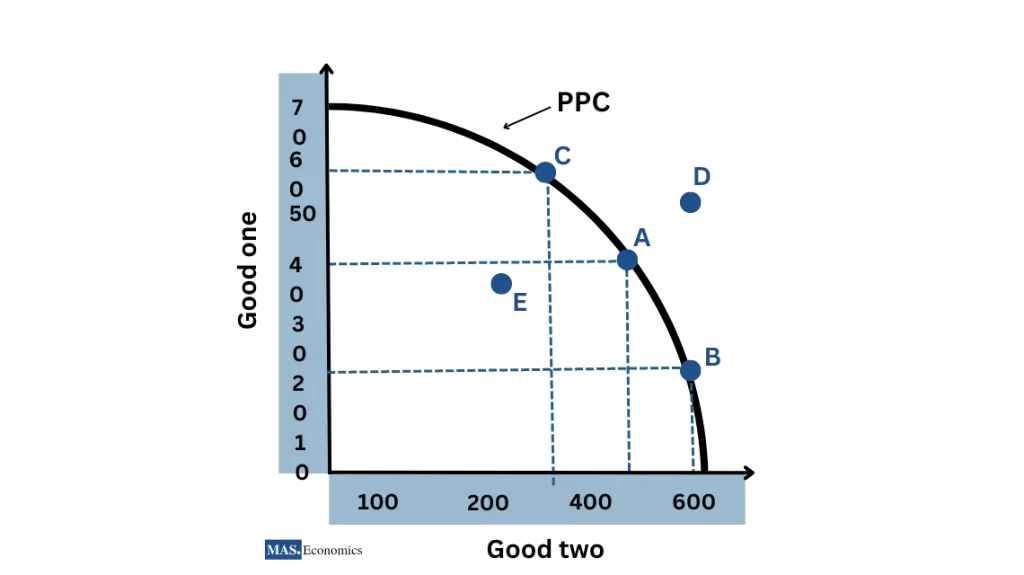

The Production Possibility Curve (PPC)

The production possibility curve (PPC) is a graphical representation of the possible combinations of goods and services that can be produced by an economy given its scarce resources and technology.

The PPC slopes downward from left to right, indicating that the production of one good must decrease as the production of the other good increases.

The PPC can be used to illustrate the concepts of scarcity, opportunity cost, and trade-offs.

For example, if an economy is producing at point A on the PPC, it is producing the maximum amount of both goods. However, if the economy wants to produce more of one good, it must produce less of the other good. This is because the economy’s resources are limited.

Economic Systems and Resource Allocation

Different economic systems handle scarcity in different ways. Market economies use prices and individual decisions to allocate resources. Planned economies use central control. The efficiency of resource allocation depends on how well these systems consider opportunity costs and trade-offs.

Economic Systems

Economic systems are like game rules that societies use to produce and distribute goods and services. They help answer three big questions: What to produce? How to produce? For whom to produce?

| Types of Economic Systems | |

|---|---|

| Market Economy (Capitalism): Here, private individuals and businesses make most of the decisions. The forces of supply and demand guide how resources are used. Prices play a key role in this system, helping everyone coordinate their actions. | |

| Planned Economy (Socialism or Communism): In this type of economy, the government makes most of the decisions. They decide what to produce based on a central plan. The goal is to reduce inequality and ensure everyone has access to basic needs. | |

| Mixed Economy: This is a combination of market and planned economies. Governments intervene to regulate markets, provide public services, and ensure income distribution. | |

| Islamic Economy: Based on Islamic principles, emphasizing justice, fairness, and ethical considerations in economic activities. Aims to create equitable wealth distribution and adhere to Islamic teachings. | |

|

|

|

Fundamental Economic Questions

What to Produce?

- Societies utilize resources to fabricate an array of goods and services.

- These decisions, influenced by cultural, technological, and economic factors, are steered by the needs and wants of the population.

How to Produce?

- Refers to the methodologies and technologies used in production.

- Societies must strike a balance between labor, capital, land, and entrepreneurship, considering factors like automation level and efficiency of production techniques.

For Whom to Produce?

- This question addresses the distribution of goods and services among societal members.

- Decisions revolve around allocation based on income, wealth, need, merit, or contribution, contingent on the economic system in operation.

Comparing Economic Systems: Answering Fundamental Questions

| Aspect | Market Economy | Planned Economy | Mixed Economy | Islamic Economy |

|---|---|---|---|---|

| What to Produce | Driven by consumer demand and preferences. | Determined by central authority’s priorities. | Influenced by demand and government priorities. | Based on Islamic principles and ethical considerations. |

| How to Produce | Decided by individual firms based on efficiency. | Central authority selects methods. | Private firms optimize with government regulations. | Efficient and ethical production methods. |

| For Whom to Produce | Goods for those with purchasing power. | Allocated by central authority’s decisions. | Blend of market access and essential services. | Equitable distribution as per Islamic teachings. |

|

|

||||

Every economic system has its advantages and disadvantages. Market economies promote efficiency and innovation but can result in inequality. Planned economies strive for fairness but may face inefficiencies.

Economic systems can evolve due to societal, political, and technological changes. Nowadays, many economies are hybrids, incorporating market mechanisms and government intervention. This combination helps strike a balance between efficiency and equity.

Thanks for reading! Get ready for our next blog on microeconomics! If you enjoyed this series, spread the knowledge by sharing it with friends and on social media.

Happy learning with MASEconomics!