A shipment can be legal in the exporter’s country, legal in the buyer’s country, and still become commercially impossible if a bank refuses to process the payment, a shipping insurer withdraws cover, or a logistics company fears being cut off from the dollar system. That is the practical power of secondary sanctions international trade policy: it reaches beyond the sanctioned target and changes the behavior of firms that may not be located in the sanctioning country at all.

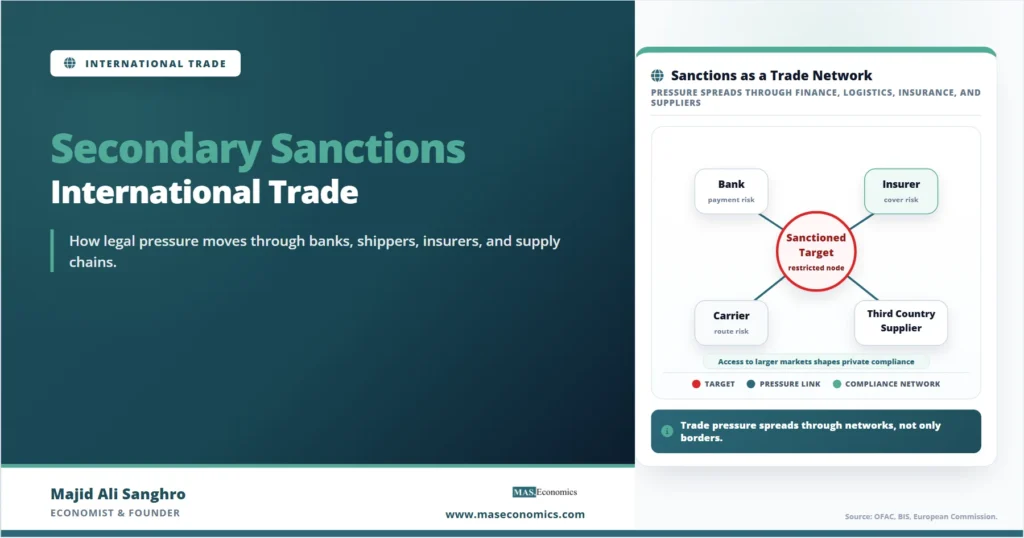

Sanctions are often discussed as if they are simple bans. In practice, they operate like a network of legal, financial, and logistical constraints. They do not only ask whether a product may be sold. They ask who owns the buyer, who controls the shipping company, which currency is used, which bank clears the payment, which technology is embedded in the product, which port handles the cargo, and whether any party in the chain is exposed to a sanctions authority.

Trade Channel Beyond the Border

A standard trade transaction involves more than a buyer and seller. It usually requires a bank to process payment, a freight forwarder to arrange movement, a carrier to transport the goods, an insurer to cover cargo and liability, a customs broker to prepare documentation, and sometimes a certification body, port operator, or export-control officer. Sanctions can target any of these links.

This is why sanctions enforcement often works before a shipment reaches the border. A bank may reject a payment because one party resembles a sanctioned entity. A shipping insurer may refuse cover if a vessel appears linked to a restricted fleet. A freight forwarder may ask for end-use declarations before accepting cargo. A supplier may refuse a sale if the buyer cannot prove that the goods will not be re-exported to a prohibited destination.

Trade sanctions therefore operate through private compliance systems as much as through customs inspections. Firms screen names against lists, monitor beneficial ownership, check product classifications, track vessel movements, review invoices, and ask whether a transaction contains a prohibited nexus. The legal rule may be written by a government, but the daily enforcement burden is carried by private actors that do not want to lose market access, banking relationships, or insurance cover.

Core idea. A sanctions regime does not need to inspect every container. It can change trade behavior by making banks, insurers, shippers, and suppliers treat certain transactions as too risky to touch.

Primary Sanctions Block Direct Exposure

Primary sanctions apply to persons and transactions that fall within the jurisdiction of the sanctioning authority. For US sanctions, this usually means US persons, transactions that involve the United States, dollar clearing, US-origin goods or technology, or property subject to US jurisdiction. For EU sanctions, it usually means EU persons, EU territory, EU-incorporated firms, and transactions with an EU jurisdictional link.

Primary sanctions are the first layer of restriction. If a country prohibits exports of certain goods to a target state, domestic exporters cannot ship those goods. If a person appears on a blocked-person list, domestic banks and firms must avoid dealing with that person and often must freeze property within their control. If an export control rule restricts advanced technology, a firm may need a license before sending the item abroad.

The trade-policy mechanics are familiar: a government restricts exports, imports, finance, investment, or services connected to a target. The difference is that sanctions often attach to identity and ownership, not only product type. A shipment may be prohibited because the buyer is blocked, because the vessel is blocked, because a majority-owned subsidiary is treated as blocked, or because the product has a military or dual-use end use.

| Channel | What is restricted | Trade effect | Typical compliance question |

|---|---|---|---|

| Export ban | Specified goods, technology, or services | Stops outbound supply to the target | Is the product controlled? |

| Import ban | Goods from a sanctioned origin | Removes a market for the target’s exports | Where was the good produced? |

| Asset freeze | Property of a listed person or entity | Blocks payments and commercial dealings | Is any party listed or majority owned by a listed person? |

| Financial restriction | Banking, securities, loans, or payment services | Disrupts settlement and trade finance | Which bank clears the transaction? |

| Transport restriction | Vessels, aircraft, ports, insurance, logistics | Raises delivery risk or stops shipment | Who owns, operates, insures, or charters the vessel? |

|

Source: MASEconomics editorial synthesis based on official US, EU, and UK sanctions guidance.

|

|||

Secondary Sanctions Pressure Third‑Country Firms

Secondary sanctions are different. They threaten consequences against non-domestic persons that engage in certain dealings with a sanctioned target, even when the transaction itself has no ordinary domestic link to the sanctioning country. A firm in a third country may not be directly subject to the sanctioning state’s primary jurisdiction, but it may still face penalties, designation, loss of market access, or exclusion from the financial system if it supports prohibited trade.

The power of secondary sanctions comes from dependence. Many international firms need access to dollar clearing, US financial institutions, EU markets, global insurers, correspondent banking, shipping registries, cloud services, technology suppliers, or multinational customers. If a sanctions authority can credibly threaten that access, a third-country firm may comply even when its own government has not imposed the same restrictions.

In trade terms, secondary sanctions create a forced choice. A shipping company, commodity trader, electronics distributor, or bank may ask: is the revenue from the sanctioned transaction worth the risk of losing access to a larger market? Often the answer is no. The result is overcompliance, de-risking, and self-sanctioning, where firms avoid even lawful transactions because the penalty risk is difficult to measure.

Caveat. Secondary sanctions are powerful because they rely on network dependence. They are also controversial because they extend one country’s policy preferences into the commercial decisions of firms located elsewhere.

Extraterritorial Reach Through Chokepoints

Secondary sanctions do not require a government to control every factory, port, or customs office. They work through chokepoints in global commerce. The most important chokepoint is finance. Cross-border trade usually needs payment, credit, guarantees, insurance, or settlement. When banks face sanctions risk, they can block a transaction before any goods move.

A second chokepoint is transport. Shipping involves vessel ownership, flag registries, port services, classification societies, cargo insurance, protection and indemnity cover, brokers, and maritime data. A sanctions authority can target vessels, owners, operators, or insurers. Even if a shipment is physically possible, losing insurance or port access can make it commercially unviable.

A third chokepoint is technology. Export controls often interact with sanctions when goods contain controlled components, software, semiconductors, machine tools, telecommunications equipment, or dual-use technology. A third-country distributor may not be free to re-export controlled items if the original technology falls under a sanctioning country’s export-control rules.

A fourth chokepoint is corporate ownership. Sanctions screening does not stop at the visible name on an invoice. Firms must ask whether a counterparty is owned or controlled by a blocked person. OFAC’s 50 Percent Rule, for example, treats entities that are owned 50 percent or more by blocked persons as blocked even when the entity itself is not separately listed. That rule turns ownership mapping into a trade-compliance problem.

Sanctions as a Supply‑Chain Problem

Traditional customs enforcement asks what crosses the border. Sanctions enforcement asks a wider set of questions. Who benefits from the transaction? Where will the goods end up? Are the goods routed through a third country to hide the final destination? Are invoice values realistic? Does the shipment pattern match ordinary trade, or does it suggest circumvention?

This turns sanctions into a supply-chain governance problem. Firms must monitor not only direct customers, but also distributors, resellers, brokers, end users, and re-export routes. The compliance challenge becomes harder when goods are standard commercial items with possible military or restricted uses, such as electronics, machine tools, drones, navigation equipment, chemicals, or industrial components.

The EU’s “no re-export to Russia” clause illustrates this shift. Instead of relying only on border bans, the EU has required exporters of certain sensitive goods to include contractual language preventing re-export to Russia. The mechanism pushes sanctions compliance into private contracts with third-country buyers. It does not merely restrict the original export. It tries to control what happens after the goods leave the EU.

For firms, the implication is practical. A sale to a low-risk country can become high risk if the buyer has no clear end-use documentation, if the goods match priority diversion codes, or if the customer’s trade pattern changed sharply after sanctions were imposed. Sanctions compliance therefore increasingly resembles supply-chain due diligence.

Circumvention Creates Trade Diversion

Sanctions rarely stop all trade. They often redirect it. When direct exports to a sanctioned economy fall, indirect flows through third countries may rise. Some of this diversion is lawful substitution. Some may reflect re-export, transshipment, or concealment. The difference matters, but it is not always easy to observe from trade data alone.

A sanctioned economy may replace direct imports from sanctioning countries with imports from non-sanctioning countries. Intermediaries may relabel goods, split shipments, change documentation, or route products through free zones. Firms may use smaller banks, alternative currencies, ship-to-ship transfers, or complex ownership structures. Enforcement agencies respond by expanding lists, publishing red flags, targeting facilitators, and warning financial institutions about evasion risk.

This is where sanctions overlap with rules of origin and trade deflection. Rules of origin ask whether a product qualifies for a tariff preference or whether it is being routed to exploit a trade agreement. Sanctions enforcement asks whether goods, money, or services are being routed to avoid a restriction. The documentary logic is different, but both depend on tracing origin, ownership, route, and end use.

| Episode | Main restriction channel | Trade mechanism | Compliance pressure point |

|---|---|---|---|

| Iran oil and financial sanctions | Energy exports, banking, shipping, insurance | Reduced access to buyers, dollar finance, and maritime services | Foreign banks and oil purchasers |

| Russia sanctions after 2022 | Export controls, financial sanctions, energy restrictions, maritime measures | Restricted high-priority goods, finance, technology, and services | Third-country diversion networks and shipping services |

| Advanced technology controls on China-linked end uses | Export controls on semiconductors, equipment, software, and technology | Limits access to strategic inputs and production capability | Product classification, end use, end user, and foreign direct product rules |

|

Source: MASEconomics editorial synthesis based on official US, EU, and UK sanctions and export-control guidance.

|

|||

Financial Institutions and Market Access

Banks are central to sanctions because they convert legal restrictions into payment reality. A firm may be willing to ship, and a buyer may be willing to pay, but a bank can stop the transaction if it identifies sanctions exposure. This is especially important in dollar transactions because dollar clearing creates a US nexus even when neither the buyer nor seller is physically located in the United States.

Financial institutions also face reputational and regulatory risk. They must screen customers, beneficial owners, counterparties, vessels, payment messages, and transaction purpose. If they fail, they may face penalties, remediation costs, monitors, loss of correspondent relationships, or restrictions on future activity. That risk makes banks conservative.

The same logic extends to insurers and shipping services. A commodity cargo may require marine insurance, protection and indemnity cover, chartering services, inspection, certification, and port access. If those service providers withdraw, the shipment becomes harder to execute even if the physical commodity still exists and a buyer still wants it.

This is why sanctions can have effects that look larger than the written legal prohibition. Private actors often avoid the grey zone. They may refuse lawful humanitarian, medical, or food-related trade if documentation risk is high or if banks fear accidental exposure. Policymakers often issue general licenses, humanitarian exemptions, or guidance to reduce this problem, but the chilling effect can remain.

Export Controls and Sanctions Convergence

Sanctions and export controls are legally distinct, but in modern trade policy they increasingly work together. Sanctions identify restricted persons, sectors, territories, or activities. Export controls identify sensitive goods, software, technology, and end uses. When combined, they can restrict both who may receive a product and what kind of product may move.

This matters most for dual-use goods. A semiconductor, drone component, sensor, machine tool, navigation device, or chemical input may have civilian uses but also military or strategic applications. The transaction cannot be judged only by the product description on an invoice. Compliance depends on classification, technical specifications, destination, end user, and end use.

The US Bureau of Industry and Security’s Russia and Belarus guidance illustrates the enforcement model. It highlights export controls, high-priority items, diversion-risk parties, and industry guidance designed to prevent evasion. The point is not only to ban direct exports. It is to stop controlled items from reaching restricted users through intermediaries.

For trade economists, the important mechanism is that technology controls can operate like a bottleneck. A sanctioned or restricted economy may still have demand, labor, and capital, but lose access to a specific input that is hard to substitute quickly. That can reduce output in targeted sectors without requiring a complete trade embargo.

Uneven Economic Costs

Sanctions create costs for the target, but also for firms and countries that adjust around the restriction. Exporters lose markets. Importers lose suppliers. Banks spend more on compliance. Shipping routes lengthen. Traders pay higher insurance and documentation costs. Buyers may switch to less efficient suppliers. Some intermediaries profit from rerouting, while compliant firms may exit completely.

These costs are not evenly distributed. Large multinational firms can maintain screening systems, legal teams, and due diligence procedures. Small exporters may find the compliance burden too expensive. Developing-country firms may be caught between conflicting sanctions regimes, especially when they need access to both the sanctioning country’s financial system and the sanctioned market’s demand.

There is also a measurement problem. Official trade data may show that direct exports fell sharply, but it may not show whether demand disappeared, moved to substitutes, or shifted through third countries. A fall in direct bilateral trade is not the same as full economic isolation. For this reason, sanctions impact analysis must track trade flows, prices, routes, ownership, finance, and enforcement behavior together.

This connects sanctions to the broader discussion of supply chain economics. Sanctions encourage firms to redesign supplier networks not only for cost and reliability, but also for legal and geopolitical exposure. In that sense, sanctions are part of the same policy environment that has made friendshoring, resilience, and trusted supplier networks more important.

Effective and Destabilizing Secondary Sanctions

The strongest case for secondary sanctions is that they reduce evasion. If only domestic firms are prohibited from trading with a target, third-country firms may fill the gap. Secondary sanctions try to close that route by making facilitation costly. They can make sanctions more credible because they target the network that keeps trade and finance moving.

The criticism is equally serious. Secondary sanctions can conflict with the policy choices of other governments, raise compliance costs for neutral countries, and create legal uncertainty for firms caught between different regulatory systems. They can also encourage sanctioned states and their partners to build alternative payment systems, shipping networks, insurance arrangements, and currency channels.

Over time, this can fragment global commerce. Firms may not simply ask which supplier is cheapest. They may ask which supplier is politically safe, which bank is acceptable, which currency is less exposed, which route is insurable, and which jurisdiction can enforce penalties. Trade becomes less frictionless because legal risk becomes part of the price.

Risk to watch. The more sanctions rely on extraterritorial pressure, the more firms may redesign trade networks around legal exposure rather than productive efficiency.

Managing Sanctions Risk

Firms manage sanctions risk by building compliance into the transaction before shipment. The first step is party screening: names, aliases, beneficial owners, directors, banks, vessels, and insurers must be checked against sanctions lists. The second step is product classification: the firm must know whether goods, software, or technology are controlled. The third step is destination and end-use review: the final buyer and final use matter, not only the immediate customer.

Documentation is central. Firms need purchase orders, invoices, shipping documents, end-user certificates, contractual re-export clauses, ownership records, and payment instructions that are consistent with the claimed transaction. Gaps, vague descriptions, sudden route changes, mismatched prices, or unusual intermediaries become red flags.

Large firms often use automated screening tools, but judgment remains necessary. A false positive can stop legitimate trade. A false negative can create legal exposure. The compliance system must therefore combine data, legal interpretation, and commercial knowledge. In sanctions-heavy sectors, the sales department, logistics team, finance team, and legal team cannot operate separately.

This is also why sanctions risk belongs in the same conversation as trade finance. A letter of credit, documentary collection, or bank guarantee is only useful if banks are willing to process the transaction. Payment security and sanctions compliance are now linked parts of cross-border trade.

Explains

Three concepts help explain why sanctions affect trade beyond the written legal ban.

Explore more MASEconomics articles on international trade, sanctions, trade finance, and supply-chain risk.

Explore the MASEconomics BlogConclusion

Secondary sanctions international trade policy matters because modern commerce depends on networks. Goods move through ports, carriers, insurers, banks, brokers, software systems, certification bodies, and payment channels. A sanction that reaches these networks can change trade behavior far beyond the border of the sanctioning country.

The economic mechanism is not simply prohibition. It is risk reallocation. Primary sanctions restrict direct dealings. Secondary sanctions pressure outsiders by threatening access to valuable markets, finance, technology, or services. The result is a system in which firms may exit transactions not because the goods are physically impossible to ship, but because the legal and financial exposure is too large.

The central trade‑policy lesson is that sanctions now operate as network instruments. They can restrict strategic goods, weaken target sectors, and reduce evasion, but they can also raise compliance costs, reroute trade, fragment supply chains, and extend one jurisdiction’s policy choices into global commerce. Their power lies in the same interdependence that makes international trade possible.

Frequently Asked Questions

What are secondary sanctions in international trade?

Secondary sanctions are measures that threaten penalties against third-country firms or financial institutions that deal with a sanctioned target. In trade, they can discourage banks, shippers, insurers, and suppliers from supporting transactions even when those firms are outside the sanctioning country.

How are secondary sanctions different from primary sanctions?

Primary sanctions apply to persons and transactions under the sanctioning authority’s jurisdiction. Secondary sanctions pressure outsiders by threatening consequences such as designation, market exclusion, or loss of financial access if they support restricted activity.

Why do banks play such a large role in sanctions enforcement?

Banks process payments, provide trade finance, maintain customer records, and depend on correspondent relationships. Because they face penalties for sanctions violations, they often stop risky transactions before goods are shipped.

Do sanctions always reduce trade with the target country?

They usually reduce direct legal trade in restricted goods, services, or finance, but they may also redirect trade through substitutes or third countries. That is why enforcement agencies focus on circumvention, transshipment, ownership structures, and end-use verification.

Are secondary sanctions controversial?

Yes. Supporters argue that they reduce evasion and make sanctions more effective. Critics argue that they extend one country’s law into other jurisdictions, raise compliance costs, and can fragment international trade networks.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics