A single semiconductor fabrication plant costs $20 billion to build, takes three years to complete, and requires technology so advanced that only three companies on the entire planet can manufacture the most cutting-edge chips. The machines that make these chips, produced exclusively by the Dutch company ASML, cost $380 million each and are so complex that they must be shipped in 40 freight containers and assembled on-site by a team of 250 engineers.

Semiconductors are the foundation of the modern economy. They power smartphones, cars, data centres, medical devices, military systems, and the artificial intelligence revolution that is reshaping every industry. The global semiconductor market generated $574 billion in revenue in 2023 and is projected to surpass $1 trillion by 2030, according to the Semiconductor Industry Association. Yet this enormous industry is concentrated in the hands of remarkably few players, making it one of the most strategically vulnerable supply chains in the world.

How Chips Became the Most Important Product on Earth

The semiconductor industry was born in Silicon Valley in the late 1950s, when companies like Fairchild Semiconductor and Texas Instruments developed the first integrated circuits. For decades, the industry followed a vertically integrated model: companies like Intel designed chips and manufactured them in their own factories, known as fabs.

The economics of the industry changed dramatically in the 1980s and 1990s with the rise of the “fabless” model. Companies like Qualcomm, Nvidia, and AMD realised they could design chips without owning factories, outsourcing the manufacturing to specialised foundries. This separation of design from fabrication created enormous efficiencies, but it also created enormous concentration. One company, Taiwan Semiconductor Manufacturing Company (TSMC), came to dominate contract chip manufacturing. Today, TSMC produces roughly 90% of the world’s most advanced semiconductors, all from a small island 160 kilometres off the coast of mainland China.

The COVID-19 pandemic exposed the fragility of this concentration. When lockdowns disrupted production and demand for electronics surged simultaneously, the resulting chip shortage shut down automobile factories from Detroit to Stuttgart, delayed consumer electronics for months, and cost the global economy an estimated $240 billion in lost output. Suddenly, governments around the world recognised that semiconductor supply chain security was not just an economic issue. It was a national security imperative.

The timeline below captures the key events that shaped the modern semiconductor economy.

The Semiconductor Industry: A Timeline of Strategic Milestones

| Year | Event | Economic Significance |

|---|---|---|

| 1958 | First integrated circuit invented (Texas Instruments / Fairchild) | Birth of the semiconductor industry; Moore’s Law trajectory begins |

| 1987 | TSMC founded in Taiwan as world’s first dedicated chip foundry | The fabless revolution begins; design separates from manufacturing |

| 2000s | China begins massive investment in domestic chip manufacturing | State subsidies exceeds $150 billion; creates global subsidy competition |

| 2020-2021 | Global chip shortage triggered by COVID-19 pandemic | Auto industry loses $210 billion in revenue; supply chain vulnerability exposed |

| Aug 2022 | US CHIPS and Science Act signed ($280 billion, including $52B for manufacturing) | Largest US industrial policy intervention since the space race |

| Oct 2022 | US imposes sweeping export controls on advanced chips to China | Cuts China off from leading-edge technology; fragments global supply chain |

| 2023 | EU Chips Act allocates €43 billion for European semiconductor capacity | Europe attempts to double its global chip production share from 10% to 20% |

| 2024-2025 | AI boom drives explosive demand for advanced chips (Nvidia, AMD) | Nvidia’s market cap surpasses $3 trillion; data centre chip revenue doubles |

| 2025-2026 | TSMC Arizona fab begins production; Intel foundry services expand | First major shift in leading-edge manufacturing away from East Asia in decades |

|

||

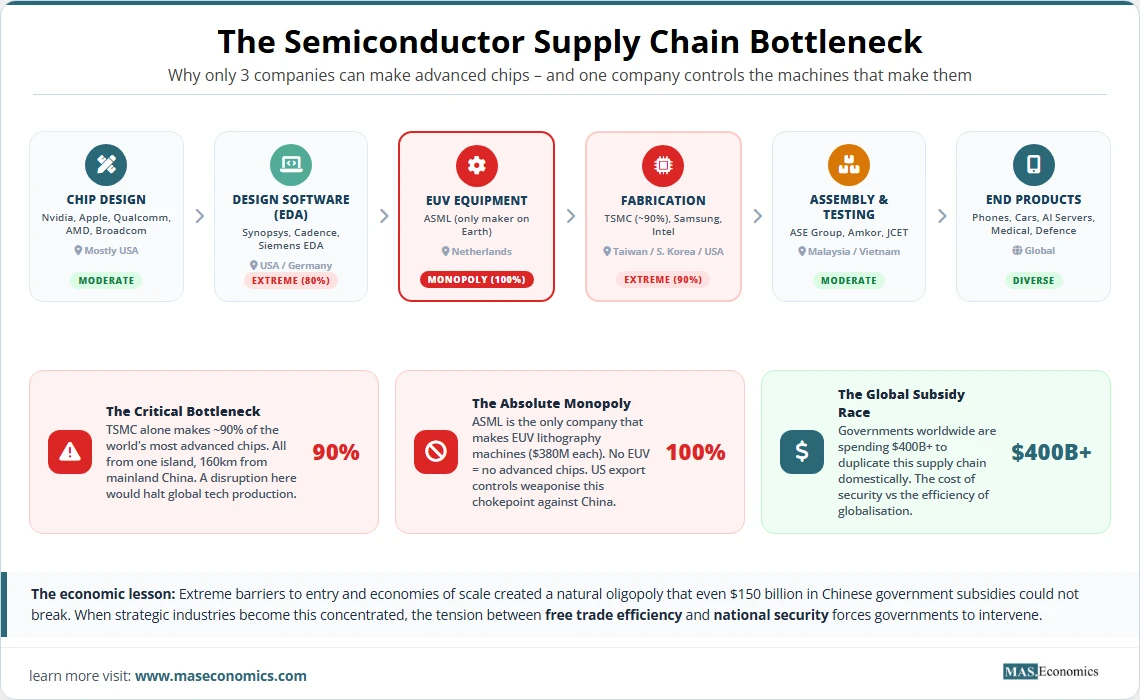

Why Only Three Companies Can Make Advanced Chips

The semiconductor industry is a masterclass in how extreme barriers to entry, economies of scale, and strategic government intervention create a market structure unlike almost any other. Four core economic concepts explain the industry’s unusual characteristics.

Oligopoly and Extreme Barriers to Entry

The advanced semiconductor manufacturing market is one of the tightest oligopolies in any industry on Earth. Only three companies, TSMC, Samsung, and Intel, can fabricate chips at the most advanced process nodes (below 7 nanometres). In the equipment layer, the concentration is even more extreme: ASML holds a 100% monopoly on extreme ultraviolet (EUV) lithography machines, the technology required for all cutting-edge chip production.

The barriers to entry are staggering. A state-of-the-art fab costs $20-30 billion to build. The R&D required to develop each new process node runs into tens of billions more. Intel has spent over $100 billion on capital expenditure and R&D in the last five years alone. These costs create natural barriers that prevent new entrants from challenging the incumbents. Even China, despite spending an estimated $150 billion in government subsidies over two decades, remains roughly two generations behind in leading-edge manufacturing technology.

This is not a market where a clever startup can disrupt the incumbents. The capital requirements, the accumulated knowledge, and the equipment monopolies create what economists call structural barriers to entry, obstacles that exist not because of government regulation but because of the fundamental economics of production.

Economies of Scale and the Learning Curve

Semiconductor manufacturing exhibits some of the strongest economies of scale of any industry. The fixed costs of building and equipping a fab are enormous, but once operational, the marginal cost of producing each additional chip is relatively low. This means that companies with higher production volumes can spread their fixed costs over more units, achieving lower average costs per chip.

TSMC’s dominance is partly explained by this dynamic. Because TSMC manufactures chips for hundreds of different clients, including Apple, Nvidia, AMD, and Qualcomm, it achieves production volumes that no single integrated manufacturer can match. This volume advantage drives down its per-unit costs, which allows it to invest more in R&D, which keeps it ahead technologically, which attracts more clients. It is a self-reinforcing cycle that economists recognise as a form of increasing returns to scale.

The learning curve effect amplifies this advantage. Each new process generation requires solving thousands of manufacturing defects. The company that ramps production fastest accumulates manufacturing experience (known as “yield learning”) that competitors cannot easily replicate. TSMC’s decades of accumulated yield data represent an intangible asset worth billions, an asset that no amount of government subsidies can instantly recreate.

Government Subsidies and Industrial Policy: The New Arms Race

The semiconductor industry is now the centrepiece of the most aggressive industrial policy competition since the Cold War. The United States, European Union, Japan, South Korea, India, and China are collectively spending more than $400 billion in subsidies, tax incentives, and infrastructure investments to attract or retain chip manufacturing on their soil.

The US CHIPS and Science Act (2022) committed $280 billion in total funding, with $52 billion specifically for semiconductor manufacturing incentives. TSMC is building three fabs in Arizona, with the first beginning production in 2025. Intel is constructing new fabs in Ohio and expanding in Arizona with over $100 billion in planned investment. Samsung is building a $17 billion fab in Texas.

From an economics perspective, these subsidies are justified by the concept of positive externalities. Semiconductor manufacturing generates benefits that extend far beyond the chip companies themselves: national security, technological leadership, high-paying jobs, and spillover innovation to other industries. Because private companies cannot capture these external benefits through market prices alone, they underinvest relative to the socially optimal level. Government subsidies, in theory, correct this market failure by bridging the gap between private returns and social returns.

The risk, however, is subsidy competition, a race to the bottom where governments outbid each other with increasingly generous incentive packages. If every major economy builds enough fab capacity to satisfy domestic demand, the result could be global oversupply, falling chip prices, and taxpayer losses on investments that never earn a commercial return. This is the classic dilemma of industrial policy: the benefits of correcting a market failure must be weighed against the costs of government picking winners.

Global Value Chains and Geopolitical Fragmentation

The semiconductor supply chain is the most geographically fragmented and interdependent of any major industry. A typical advanced chip might be designed in the United States (by Nvidia or Apple), fabricated in Taiwan (by TSMC), using equipment from the Netherlands (ASML), Japan (Tokyo Electron), and the United States (Applied Materials), packaged and tested in Malaysia or Vietnam, and finally assembled into a product in China. No single country controls the entire chain.

This interdependence was once celebrated as a triumph of globalisation and comparative advantage. Each country specialised in what it did best, and the result was a system that produced extraordinarily complex products at remarkably low cost. But the US-China technology competition has transformed this interdependence from a strength into a vulnerability. The US export controls imposed in October 2022 cut China off from EUV lithography machines and the most advanced chips, weaponising the supply chain as a tool of geopolitical competition.

The fragmentation of the global chip supply chain into rival blocs, sometimes called “techno-nationalism,” represents a fundamental challenge to the economic theory of free trade. The efficiency gains from specialisation and comparative advantage are real, but so are the strategic risks of dependence on a single point of failure. Economists are increasingly recognising that national security externalities can justify departures from free trade principles, even if those departures carry real economic costs in the form of higher prices and slower innovation.

The Numbers Behind the Chip Industry

The concentration of the semiconductor industry becomes strikingly clear when you examine market share data. The chart below shows the global semiconductor revenue share by country of origin for chip companies.

Global Semiconductor Revenue Share by Headquarters Country (2023)

Source: Semiconductor Industry Association and Statista. Measured by company headquarters, not manufacturing location.

The subsidy race between major economies is unprecedented in scale. The chart below compares the announced government semiconductor investments by country.

Government Semiconductor Subsidies and Incentives by Country (Announced, $ Billions)

Source: SIA, NIST, European Commission, various government announcements. Figures include direct subsidies, tax incentives, and infrastructure commitments. China figure is cumulative over two decades.

The following table summarises the key players in the semiconductor value chain, illustrating the extreme concentration at each stage.

Semiconductor Value Chain: Key Players and Market Concentration

| Value Chain Stage | Dominant Players | Concentration | Barriers to Entry |

|---|---|---|---|

| Chip Design (Fabless) | Nvidia, Qualcomm, AMD, Apple, Broadcom | Moderate (top 5 hold ~40%) | High (IP, talent, R&D costs) |

| Manufacturing (Leading-Edge) | TSMC, Samsung, Intel | Extreme (TSMC alone: ~90%) | Extreme ($20-30B per fab) |

| EUV Lithography Equipment | ASML (Netherlands) | Monopoly (100%) | Absolute (no competitors exist) |

| Other Fab Equipment | Applied Materials, Tokyo Electron, Lam Research | High (top 3 hold ~55%) | Very High (specialised engineering) |

| Assembly, Testing & Packaging | ASE Group, Amkor, JCET | Moderate (top 3 hold ~45%) | Moderate (labour & capital intensive) |

| Electronic Design Automation (EDA) | Synopsys, Cadence, Siemens EDA | Extreme (top 3 hold ~80%) | Very High (decades of IP) |

|

|||

The Stakes of the Chip War

The Winners

TSMC and its shareholders have been the biggest beneficiaries of the AI boom. The company’s revenue surged 26% in 2024 as demand for advanced AI chips from Nvidia and Apple drove record orders. TSMC’s stock price has more than tripled since 2020, and its market capitalisation exceeds $800 billion.

The United States has reasserted its leadership in chip design and is rebuilding its manufacturing base. American companies, led by Nvidia, now capture nearly half of all global semiconductor revenue. The CHIPS Act is bringing hundreds of billions in private investment to Arizona, Ohio, and Texas, creating tens of thousands of high-paying engineering and manufacturing jobs.

Countries with fab equipment industries, particularly the Netherlands (ASML), Japan (Tokyo Electron), and the United States (Applied Materials), control critical chokepoints in the supply chain. Their leverage has increased as geopolitical tensions make equipment access a tool of strategic competition.

The Losers

China’s semiconductor ambitions have been severely set back by US export controls. Despite massive government investment, Chinese chipmakers like SMIC remain roughly two technology generations behind TSMC. The export controls prevent China from purchasing EUV machines, cutting off the technological pathway to the most advanced chips. China’s Huawei, once a leading smartphone manufacturer, has been forced to develop workaround chip designs that are costlier and less powerful than competitors’ products.

Consumers face higher prices as the industry fragments. Building duplicate fab capacity in multiple countries is inherently less efficient than concentrating production where it is cheapest. The Boston Consulting Group has estimated that fully onshoring the semiconductor supply chain would raise chip prices by 35-65%. Some portion of these costs will inevitably be passed through to consumers in the form of more expensive electronics, cars, and appliances.

Smaller nations in the supply chain, particularly Malaysia, Vietnam, and the Philippines, which specialise in chip assembly and testing, face uncertainty as reshoring incentives pull manufacturing activity back toward wealthy nations. These countries have built entire regional economies around semiconductor back-end processing, and a shift away from globalised supply chains threatens their economic development model.

What the Chip Industry Teaches About Modern Economics

The semiconductor industry challenges several comfortable assumptions of economic theory. Free trade and comparative advantage produce the most efficient outcomes in most markets, but when a single product is essential to national security, military capability, and technological sovereignty, the calculus changes. The willingness of governments to spend hundreds of billions on subsidies reflects a judgment that the strategic risks of dependence outweigh the efficiency costs of duplication.

The chip industry also demonstrates how extreme economies of scale and learning curve effects can create natural oligopolies that are virtually impossible to challenge, even with massive government support. China has spent more on semiconductor subsidies than any other country, yet it remains technologically behind. Capital alone cannot substitute for decades of accumulated manufacturing knowledge.

The semiconductor industry is the ultimate case study in how market structure, trade theory, industrial policy, and geopolitics intersect in a single global industry. The decisions being made today about chips, subsidies, and export controls will shape the balance of economic power for the rest of the century.

MASEconomics Explains

Conclusion

The semiconductor industry sits at the intersection of economics, technology, and geopolitics in a way that no other industry can match. It is an oligopoly with barriers to entry so extreme that even nation-states struggle to overcome them. It is a supply chain so globally interdependent that a single factory shutdown in Taiwan could halt automobile production on four continents. And it is now the arena for the most expensive industrial policy competition in modern history, with governments collectively committing over $400 billion to reshape an industry that was once left almost entirely to market forces.

The economics of semiconductors teach us that efficiency and security are sometimes in tension, that comparative advantage can become strategic vulnerability, and that some markets are simply too important and too concentrated to be governed by market forces alone. The chips that power your phone, your car, and your world are the product of extraordinary human ingenuity. The question now is who will control that ingenuity, and at what cost.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.