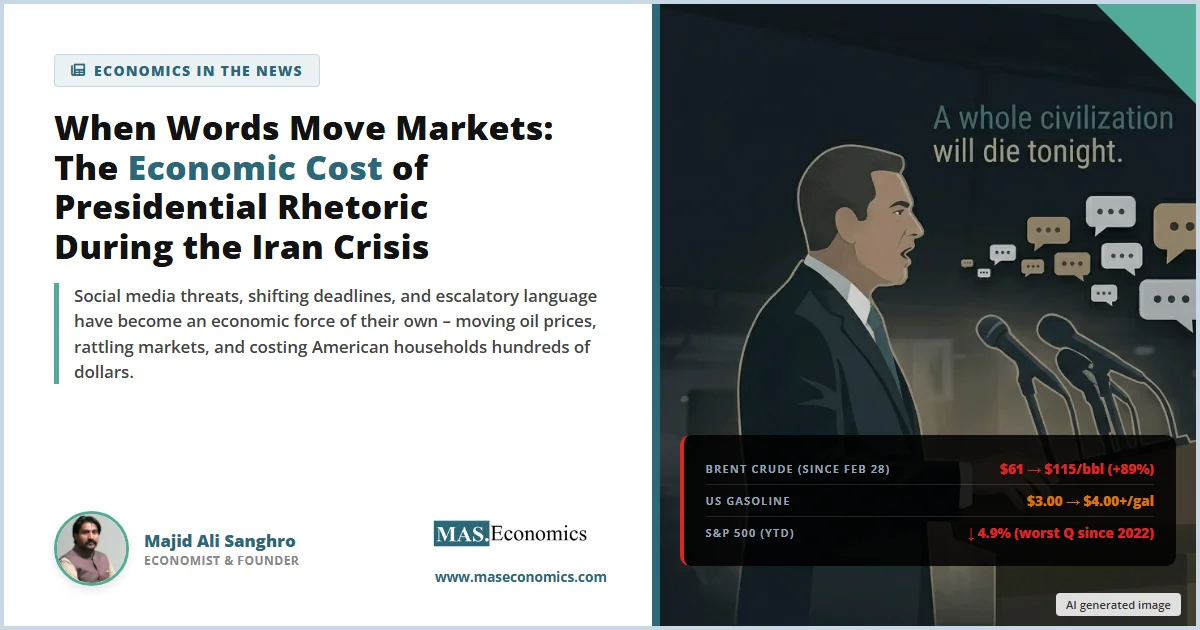

On April 7, 2026, the President of the United States posted seven words on social media that sent oil prices surging, rattled financial markets across three continents, and added billions of dollars to the global cost of energy: “A whole civilization will die tonight.” Within hours, Brent crude climbed above $115 per barrel, US crude futures hit $116.22, and traders across the world scrambled to price in the possibility that the largest oil supply disruption in history could get dramatically worse.

This article is not about the politics of the US-Iran conflict. It is about a question that every economist, investor, and household should be asking: what happens to an economy when the most powerful leader in the world uses social media as a tool of economic brinkmanship, and when every post, threat, and shifting deadline becomes a market-moving event?

The answer, as the data shows, is that words have become an economic force of their own, one that is costing American families hundreds of dollars, pushing inflation higher, and creating a level of market uncertainty that traditional economic models were never designed to handle.

How Presidential Posts Moved Markets

Since the US-Israeli strikes on Iran began on February 28, 2026, a clear pattern has emerged. Presidential statements on Truth Social and in press briefings have consistently preceded sharp movements in oil prices, stock indices, and currency markets. Each escalation in rhetoric has corresponded to a measurable economic impact.

Key Communication Events and Market Responses (February – April 2026)

| Date | Statement / Event | Brent Crude Response | Market Impact |

|---|---|---|---|

| Feb 28 | Operation Epic Fury launched; 900 targets struck | $61 → $83 (+36%) | Dow fell 400+ pts; S&P 500 down 0.7% |

| Mar 4 | Iran declares full Strait of Hormuz blockade | Pierced $100/bbl | Global indices fell 1-2%; gold surged |

| Mar 12 | President threatens to “finish the job” on social media | $100 → $114 | California gas exceeded $5/gal |

| Mar 23 | Optimistic comments on negotiations | $114 → $102 (-10.5%) | Brief stock rally; consumer sentiment ticked up |

| Apr 1 | “Hit them extremely hard… bring them back to the Stone Ages” | +6.7% to $108; WTI +6.2% | Dow fell 600 pts; worst day in weeks |

| Apr 5 | Easter post: “Open the F***ing Strait, you crazy bastards” | $109 → $112 | Futures sank; Asian markets opened sharply lower |

| Apr 7 | “A whole civilization will die tonight” | $110 → $116 (intraday) | WTI hit $116.22; thin liquidity amplified swings |

|

|||

The pattern is unmistakable. Escalatory language drives oil prices higher. Conciliatory signals bring them down. Shifting deadlines and ambiguous messaging, “maybe something revolutionarily wonderful can happen, WHO KNOWS?”, inject uncertainty that Bloomberg describes as “exaggerated by thin liquidity amid headlines signaling conflicting narratives.”

The Economics of “Jawboning”

Economists have long understood that words from powerful institutions can function as economic instruments. Central banks use “forward guidance”, carefully crafted public statements about future policy intentions, to influence interest rates, inflation expectations, and investment decisions without changing a single number. When a Federal Reserve chair says “we anticipate maintaining the current rate,” markets respond as if a policy decision has been made, because in economic terms, it has.

This practice, known colloquially as “jawboning,” works because credible, consistent communication reduces uncertainty. Market participants can form expectations, price assets accordingly, and make informed decisions. The predictability itself has economic value.

What the Iran crisis has demonstrated is what happens when the same principle operates in reverse. Instead of reducing uncertainty, presidential communication has become the single largest source of uncertainty in global energy markets. Each social media post functions as an unscheduled policy announcement with no institutional review, no consistency framework, and no forward guidance about what comes next. The result is a “rhetoric premium” embedded in every barrel of oil, every stock trade, and every mortgage application processed since late February.

According to CNBC, independent oil analyst Tom Kloza called the April 1 national address “a disaster” for markets, not because of any military action, but because the speech failed to provide the clarity that investors and supply chain managers needed to plan ahead.

The Cost to American Households

The economic damage is not abstract. It is arriving in the budgets of ordinary American families through three direct channels: gasoline prices, food costs, and housing.

Gasoline

US gasoline prices have risen from approximately $3.00 per gallon before the conflict to over $4.00 nationally, with California exceeding $5.00 per gallon as early as the second week of March. According to economists at the Stanford Institute for Economic Policy Research, the average American household will spend an additional $740 on gasoline this year as a direct result of the oil price surge.

Data from the Bank of America Institute shows that gasoline spending was up more than 14% year over year during the second week of March alone. Their economists warned that this rise “could potentially dampen consumers’ ability to spend on discretionary categories,” meaning less money for restaurants, entertainment, clothing, and other sectors that employ millions of Americans.

Food Prices

The Strait of Hormuz does not just carry oil. Up to 30% of globally traded fertilisers normally transit this waterway. With the Strait effectively closed since early March, fertiliser prices have surged, threatening agricultural input costs for the upcoming growing season. The British think tank The Food Policy Institute has warned of long-term food price increases as fuel and fertiliser disruptions work through the supply chain. Brazil, which supplies nearly 60% of global soybean exports, is almost entirely dependent on imported fertilisers, nearly half of which transit the strait.

Housing

The war’s impact on housing is less visible but potentially more damaging in the long run. According to NBC News, the average 30-year fixed mortgage rate has climbed a full half percentage point since the war began, from just under 6% to 6.53%. For a family purchasing a $400,000 home, that increase adds roughly $120 per month to their mortgage payment, or nearly $43,000 over the life of the loan.

The mechanism is straightforward. Higher oil prices feed into inflation expectations. Higher inflation expectations push bond yields up. Higher bond yields raise mortgage rates. Every escalatory social media post that spikes oil prices by a few dollars per barrel contributes to this chain, a chain that ultimately arrives at the doorstep of a young couple trying to buy their first home.

Measuring the Damage

Source: EIA, CNBC, Bloomberg. Data as of April 7, 2026.

The numbers tell a story of an economy under strain. The table below summarises the key economic indicators that have deteriorated since the conflict began.

Economic Impact Dashboard: US-Iran Crisis (February 28 – April 7, 2026)

| Indicator | Pre-War Level | Current Level | Change |

|---|---|---|---|

| Brent Crude Oil | $61/barrel | $115/barrel | +89% |

| US Gasoline (National Avg) | $3.00/gallon | $4.00+/gallon | +33% |

| California Gasoline | $3.80/gallon | $5.00+/gallon | +32% |

| S&P 500 (YTD) | Positive start | -4.9% | Worst quarter since 2022 |

| 30-Year Mortgage Rate | ~6.00% | 6.53% | +53 basis points |

| Goldman Sachs Recession Odds | ~15% | 30% | Doubled |

| Unemployment Forecast (End 2026) | 4.2% | 4.6% | +0.4 percentage points |

| Additional Household Gas Spend | – | $740/year | Direct cost to families |

|

|||

“Warflation” and the Stagflation Risk

The term “warflation“, inflation driven by wartime supply disruptions, has entered the lexicon of financial analysts in 2026. The concern is not just that prices are rising. It is that they are rising at precisely the moment when economic growth is slowing, creating the conditions for stagflation, a toxic combination of stagnant growth and persistent inflation that central banks find extremely difficult to combat.

Morgan Stanley has warned that if oil prices remain elevated long enough to seep into inflation expectations, the Federal Reserve will have no choice but to keep interest rates higher for longer. This would squeeze borrowers, slow investment, and increase the risk of a recession. Their research indicates that real consumer spending typically begins to decline two to three months after an oil price shock and can remain depressed for five to six months.

The US Energy Information Administration confirmed in its latest quarterly report that Brent crude prices surged from $61 to $118 per barrel during the first quarter of 2026, the largest quarterly price increase on an inflation-adjusted basis since records began in 1988.

Goldman Sachs has raised its probability of a US recession over the next 12 months to 30%, driven primarily by the oil price surge. The bank also expects the unemployment rate to rise to 4.6% by year-end, up from 4.4% in February. Several Wall Street firms now project inflation running closer to 3% this year rather than 2%, eroding disposable incomes and weighing on job creation.

The Impact on US Allies

The economic shockwave is not confined to American borders. US allies in Europe, the UK, and Canada are experiencing their own versions of the same crisis.

Europe receives 12-14% of its liquefied natural gas from Qatar, all of which transits the Strait of Hormuz. With those supplies cut off, European energy prices have spiked, compounding the inflationary pressures that the continent has been fighting since the 2022 Russia-Ukraine energy shock. The European Central Bank, which had begun cutting rates, has been forced to pause as energy-driven inflation threatens to reverse its progress.

The United Kingdom faces a particularly difficult position. The UK announced that it will not allow US forces to use British bases for operations targeting civilian infrastructure, a diplomatic stance that reflects the economic as well as moral calculus. Higher energy costs are already feeding into UK inflation, which had been falling toward the Bank of England’s 2% target. With Brent crude above $110, that progress is at serious risk.

Canada, as a net energy exporter, benefits from higher oil prices in its energy sector but suffers from the same consumer-level impacts: higher gasoline costs, rising food prices, and increased uncertainty that dampens business investment. The Bank of Canada faces the same impossible choice as the Fed: cut rates to support growth, or hold them to fight inflation.

Why This Crisis Is Different

What distinguishes the 2026 oil shock from previous energy crises is the role of social media as a direct channel between presidential rhetoric and market pricing. During the 1973 Arab oil embargo or the 1990 Gulf War, markets responded to events, actual supply disruptions, military actions, and diplomatic outcomes. Communication from leaders was filtered through press conferences, prepared statements, and institutional channels that provided some degree of predictability.

In 2026, the filtering mechanism has been removed. A single social media post at 8:00 a.m. can move billions of dollars in market capitalisation before traditional media has even processed the content. The post does not go through economic advisors, national security review, or communications strategy. It arrives raw, unfiltered, and often contradictory, and markets must price it in real time.

This creates what economists call “radical uncertainty”, a state in which market participants cannot even assign probabilities to future outcomes because the decision-making process itself is unpredictable. Traditional risk models assume that policy follows some logical framework, even if the specifics are unknown. When that assumption breaks down, the uncertainty premium embedded in every asset price rises dramatically.

As Bloomberg noted on April 7, many traders have simply left the market entirely because of the extreme volatility, further reducing liquidity and amplifying the impact of each new headline. This is a feedback loop: rhetoric creates volatility, volatility drives traders out, and reduced liquidity amplifies the next round of rhetoric-driven price swings.

What Comes Next

Possible Scenarios and Economic Consequences

| Scenario | Probability | Oil Price Outcome | Economic Impact |

|---|---|---|---|

| Diplomatic resolution within 2 weeks | Low-Medium | $80-$90/bbl within months | Inflation moderates; recession avoided; markets recover |

| Prolonged conflict with partial strait reopening | Medium | $100-$120/bbl sustained | Inflation runs 3%+; Fed holds rates; growth slows to 1-2% |

| Escalation to infrastructure destruction | Medium | $130-$150/bbl or higher | Global recession risk; stagflation; long-term energy restructuring |

| Full regional war involving Gulf states | Low | $150+/bbl; supply crisis | Severe global recession; food crisis; humanitarian emergency |

|

|||

The International Energy Agency has warned that April will be worse than March because the last tankers that transited the strait before the blockade have now arrived at their destinations. From April onwards, there is “nothing” in the pipeline, according to IEA Executive Director Fatih Birol, who called this “the biggest disruption in history.”

Even in the most optimistic scenario, the EIA cautions that Middle East oil production will not return close to pre-conflict levels until late 2026. The damage to infrastructure, the depletion of strategic petroleum reserves, and the structural shift in energy security thinking will keep prices elevated and uncertainty high for months, regardless of how the diplomatic situation resolves.

A New Normal for Markets

Three structural changes are likely to outlast the current crisis.

First, energy security is being repriced permanently. Countries that depend on Middle Eastern oil and gas are accelerating their diversification strategies. Saudi Arabia’s East-West pipeline to the Red Sea port of Yanbu is operating at maximum capacity. The US has temporarily lifted sanctions on Russian oil tankers to shore up global supply. These emergency measures will reshape trade flows for years.

Second, the concept of a “geopolitical risk premium” in oil markets is being recalibrated upward. Before February 2026, analysts typically estimated this premium at $3-$5 per barrel. After the Hormuz blockade, it may settle at $10-$15 permanently, as markets price in the demonstrated willingness of state actors to weaponise critical trade routes.

Third, the relationship between presidential communication and market stability has been exposed as a vulnerability in the global economic system. When a single social media account can move oil prices by 5-10% in a morning, the traditional assumptions about policy predictability that underpin trillions of dollars in asset pricing are fundamentally challenged.

MASEconomics Explains

Conclusion

The 2026 Iran crisis has revealed something that economic textbooks rarely address: the economic power of communication from the highest levels of government. Central bankers spend decades building credibility so that their words can stabilise markets. The current crisis demonstrates what happens when words from the most powerful office in the world do the opposite, when they inject uncertainty, amplify volatility, and transmit costs directly to the households least equipped to absorb them.

The average American family is now paying $740 more per year for gasoline. Mortgage rates have risen half a percentage point. The S&P 500 has posted its worst quarter since 2022. Goldman Sachs has doubled its recession probability to 30%. And the IEA warns that the worst of the supply crunch is still ahead.

These are not political judgments. They are economic measurements. And they underscore a principle that economists have always known but rarely had to demonstrate so vividly: in a globally interconnected economy, words are not just words. They are economic events. And their costs are borne not by the person who speaks them, but by the families, workers, and businesses who must live with their consequences.

The question facing the global economy now is not whether the Strait of Hormuz will reopen; eventually, economic gravity will demand it. The question is how much damage will be inflicted in the interim, and whether the institutions designed to provide economic stability can withstand the strain of operating in an environment where the rules of communication have fundamentally changed.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.