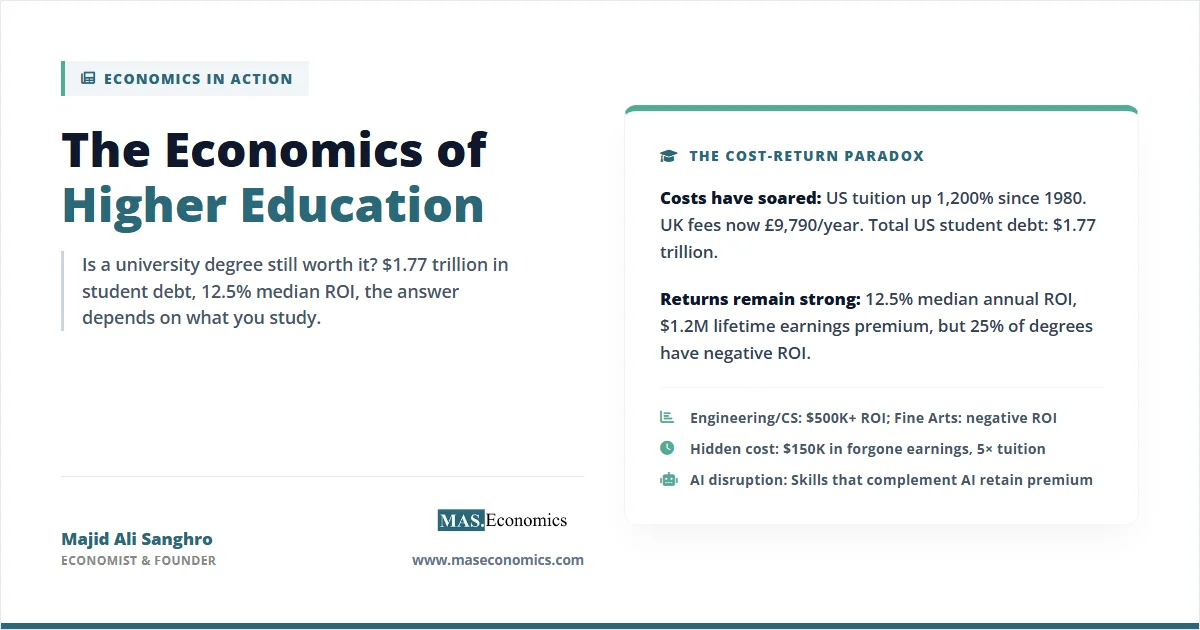

Total student loan debt in the United States has surpassed $1.77 trillion, owed by 43 million borrowers. Average tuition at a four-year public university has risen 1,200% since 1980, far outpacing inflation, wage growth, and the price of virtually every other consumer good. In the United Kingdom, the tuition fee cap rose to £9,790 for the 2026–2027 academic year, the first meaningful increase since 2017, while the average English graduate leaves university with over £40,000 in debt. In Canada, undergraduate tuition averages CAD $7,076 per year, with international students paying four times more.

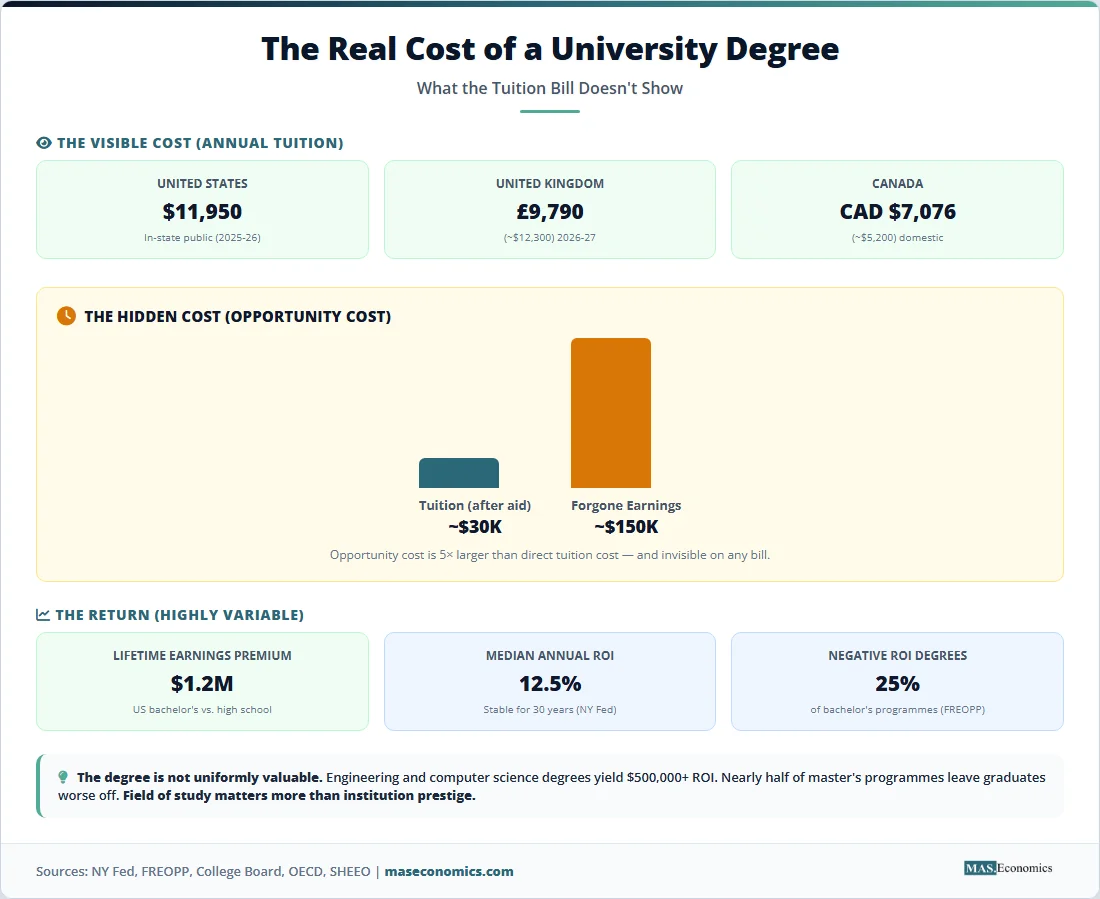

Yet the economics of higher education produce a paradox. Despite these costs, the Federal Reserve Bank of New York estimates the median return on investment for a bachelor’s degree at 12.5% annually, a figure that has remained remarkably stable for three decades. College graduates earn $1.2 million more over a lifetime than those with only a high school diploma. The unemployment rate for degree holders is roughly half that of non-graduates. The degree premium, in aggregate, has never been larger.

The tension between soaring costs and persistent returns defines the economics of higher education. The answer to whether a degree is “worth it” depends entirely on which degree, at which institution, in which field, and at what price.

From Public Good to Consumer Product

Higher education was once treated as a public good in most developed economies. In the United States, the GI Bill (1944) sent 8 million veterans to college at government expense, creating the world’s first mass-educated workforce. State legislatures funded public universities generously, keeping tuition negligible. The University of California charged no tuition at all until 1970. In the United Kingdom, the government paid tuition fees and provided maintenance grants until 1998. Germany, Norway, and several other European nations still charge zero or near-zero tuition for domestic students.

The transformation began in the 1980s. Governments in the US and UK shifted the cost burden from taxpayers to students, based on the argument that the primary beneficiary of a degree is the individual graduate, not society. US state funding per student at public universities fell by 30% in real terms between 2000 and 2020, according to the State Higher Education Executive Officers Association (SHEEO). Universities compensated by raising tuition. In England, the introduction of £1,000 tuition fees in 1998, rising to £3,000 in 2006 and £9,000 in 2012, represented a fundamental shift in how society valued and financed higher education.

The federal student loan system in the United States enabled this cost escalation. Because loans were guaranteed by the government and available to virtually all students regardless of the programme’s quality or economic value, universities faced little market pressure to control costs. Economists call this the Bennett Hypothesis: increases in financial aid allow institutions to raise tuition, capturing the subsidy rather than passing it through to students. The result is a system where tuition has grown at roughly 4–5% per year for four decades, compounding into the $1.77 trillion debt burden visible today.

Table 1. The Cost of Higher Education: Key Milestones (1944–2026)

| Year | Event | Economic Significance |

|---|---|---|

| 1944 | US GI Bill signed into law | 8 million veterans attend college; creates first mass-educated workforce |

| 1965 | US Higher Education Act establishes federal student loan programme | Democratises access but begins the cycle of debt-financed tuition growth |

| 1998 | UK introduces £1,000 tuition fees (England) | Ends free university education; shifts cost from state to student |

| 2006 | UK raises fees to £3,000; income-contingent loans introduced | Graduates repay 9% of earnings above threshold; debt written off after 25–30 years |

| 2010 | US student debt surpasses credit card debt for the first time ($830 billion) | Student loans become the second-largest category of household debt after mortgages |

| 2012 | UK triples fees to £9,000 per year | Most graduates will never repay in full; government absorbs the subsidy cost |

| 2017–2024 | UK tuition fees frozen at £9,250 (7 years) | Real-terms value falls to ~£5,860 in 2012 prices; universities face funding crisis |

| 2023 | US student debt reaches $1.77 trillion; 43 million borrowers | Medical debt bankruptcy overtaken by student debt as a driver of financial distress |

| 2025 | US federal tax credit for EV purchases eliminated; parallels debated for education subsidies | Policy uncertainty around loan forgiveness creates demand volatility |

| 2026 | UK raises tuition cap to £9,790; Plan 2 threshold frozen until 2030 | Graduates repay more through fiscal drag; universities gain £390 million in new revenue |

|

||

The Economics of the Degree Premium

The economic analysis of higher education rests on four interconnected concepts that explain why costs keep rising, why returns remain high on average, and why the variance in outcomes is so wide.

Human Capital Theory

The foundational framework for understanding education’s economic value is human capital theory, developed by Gary Becker and Theodore Schultz in the 1960s. The theory treats education as an investment: students forgo current earnings and pay tuition in exchange for higher future productivity and wages. The “degree premium,” the earnings gap between graduates and non-graduates, is the return on this investment.

The data from the US Bureau of Labor Statistics confirms a persistent and widening premium. In 2024, the median weekly earnings for a worker with a bachelor’s degree were $1,541, compared to $916 for a high school graduate, a 68% premium. The unemployment rate for degree holders was 2.2%, versus 3.9% for those with only a high school diploma. Over a 40-year career, this compounds into the $1.2 million lifetime earnings advantage that economists consistently find.

However, the aggregate premium masks enormous variation. A 2026 study by FREOPP analysing 53,000 degree programmes found that the median bachelor’s degree ROI is $160,000, but engineering and computer science degrees yield $500,000 or more, while nearly half of all master’s degree programmes leave graduates financially worse off than if they had not enrolled. The degree is not uniformly valuable. The field of study is.

Signalling vs. Human Capital

A competing theory, first proposed by Michael Spence in 1973, argues that much of the degree premium reflects signalling rather than genuine skill development. In this model, a university degree does not primarily make graduates more productive. Instead, it serves as a signal to employers that the graduate possesses desirable traits: intelligence, discipline, and the ability to complete a multi-year project. The degree is a sorting mechanism, not a training programme.

The empirical evidence suggests both theories contribute. The “sheepskin effect,” the observed jump in earnings at the point of degree completion that exceeds what would be predicted by years of education alone, supports the signalling hypothesis. A worker with three years of university education but no degree earns significantly less than one who completed the fourth year and graduated, despite having acquired nearly identical knowledge. Bryan Caplan’s research, published in “The Case Against Education” (2018), estimates that roughly 80% of the return to education comes from signalling, not skill-building.

The distinction carries significant policy implications. If degrees primarily build human capital, then expanding university access is socially beneficial because it increases total productivity. If degrees primarily signal existing ability, then expanding access merely inflates the credentials required for jobs that previously did not need them, a process economists call credential inflation, without increasing aggregate productivity.

The AI Disruption and the Changing Premium

The emergence of artificial intelligence as a general-purpose technology is reshaping the economics of higher education in ways that are only beginning to be understood. AI tools can now perform tasks that previously required years of specialised training: legal research, financial analysis, medical image interpretation, software coding, translation, and content creation. Goldman Sachs estimates that 300 million jobs globally are exposed to AI automation, with knowledge-work occupations, precisely the roles that university graduates fill, among the most affected.

The impact on the degree premium is ambiguous. In the short term, AI may increase demand for graduates who can work with and manage AI systems, reinforcing the premium. In the longer term, if AI can replicate the cognitive skills that degrees certify, the signalling value of a degree may erode. The strategic interaction between employers, educational institutions, and technology is creating a period of deep uncertainty about which skills will retain value and which will be automated away.

Early evidence from the labour market suggests polarisation. Demand is growing rapidly for graduates with skills that complement AI: data science, machine learning engineering, prompt engineering, AI ethics, and cybersecurity. Simultaneously, demand is weakening for roles where AI can substitute: entry-level legal research, basic financial reporting, routine software testing, and administrative functions. The degree premium may not decline in aggregate, but the variance across fields is likely to widen further.

The Opportunity Cost and the Dropout Problem

The full economic cost of a degree includes not just tuition but the opportunity cost: the earnings forgone while studying. The New York Federal Reserve estimates the total cost of a bachelor’s degree at roughly $180,000, comprising approximately $30,000 in direct costs (after financial aid) and $150,000 in forgone earnings. This opportunity cost is invisible on any tuition bill, but it is the largest single component of the investment.

The most financially devastating outcome in higher education is starting a degree and not finishing. The six-year completion rate for bachelor’s degrees in the United States is 61.1%, according to the National Student Clearinghouse Research Center. Nearly 40% of students who enrol do not graduate within six years. These non-completers bear the worst of both worlds: they accumulated debt and forgone earnings without obtaining the credential that unlocks the wage premium. Default rates among non-completers are two to three times higher than among graduates.

In the United Kingdom, completion rates are significantly higher at roughly 87%, partly because three-year degrees are standard and partly because admission is more selective. Canada’s completion rates fall between the US and the UK. The cross-country variation suggests that institutional design, not student ability, is a primary determinant of whether the investment pays off.

Returns by Field and Country

The aggregate degree premium conceals dramatic variation by field of study. The chart below shows median lifetime ROI for the most common bachelor’s degree fields in the United States, revealing the gulf between the highest-return and lowest-return programmes.

Median Lifetime ROI by Bachelor’s Degree Field (United States)

Source: FREOPP, “Does College Pay Off?” (January 2026). ROI calculated as increase in lifetime earnings minus total cost of degree, including opportunity cost. Risk-adjusted for non-completion.

The cross-country comparison reveals how different systems produce different outcomes. The chart below compares the cost structure and graduate earnings premium across five major higher education systems.

Higher Education Cost and Graduate Earnings Premium: International Comparison

Source: OECD Education at a Glance 2025 and national statistics agencies. Graduate premium = % by which graduate median earnings exceed non-graduate median earnings, workers aged 25–64.

The following table summarises the key metrics that define the higher education economy in the three largest English-speaking markets.

Table 2. Higher Education Economics: US, UK, and Canada Compared (2025–2026)

| Metric | United States | United Kingdom | Canada |

|---|---|---|---|

| Average Annual Tuition (Public/Domestic) | $11,950 (in-state) | £9,790 (≈$12,300) | CAD $7,076 (≈$5,200) |

| Average Graduate Debt | $29,300 | £40,000+ (≈$50,000) | CAD $28,000 (≈$20,600) |

| Total National Student Debt | $1.77 trillion | £236 billion (≈$297 billion) | CAD $42 billion (≈$31 billion) |

| Degree Completion Rate (6-year) | 61.1% | ~87% | ~75% |

| Graduate Earnings Premium | 68% ($1,541 vs $916/week) | 52% | 48% |

| Median Degree ROI (Annual) | 12.5% (NY Fed) | Variable (IFS estimates) | Variable by province |

| Repayment Model | Fixed monthly payments | Income-contingent (9% above threshold) | Fixed payments (6-month grace period) |

| Loan Forgiveness | After 20–25 years (IDR plans) | After 40 years (Plan 5) | Provincial assistance programmes |

|

|

|||

Lessons and the Future of the Degree

Five lessons emerge from the economics of higher education, each with implications that extend far beyond the campus.

First, the degree premium is real but unevenly distributed. On average, a bachelor’s degree remains one of the strongest investments an individual can make, with a median annual return of 12.5%. But “on average” is doing enormous work. Engineering, computer science, and nursing graduates earn returns exceeding $500,000. Fine arts and social work graduates may earn negative returns. The decision is not whether to go to university, but which programme at which price.

Second, the financing model in the United States is structurally broken. A system that lends unlimited government-backed money to 18-year-olds, regardless of the economic value of the programme they enrol in, creates perverse incentives at every level. Universities face no downside for admitting students into low-return programmes because the loans are guaranteed. Students lack the information and experience to evaluate ROI before committing. The UK’s income-contingent repayment model, where graduates repay only 9% of earnings above a threshold, and the remaining debt is written off after 30–40 years, transfers the risk from the individual to the state, a fundamentally different allocation of risk with different incentive effects.

Third, AI will reshape but not eliminate the degree premium. The cognitive tasks that AI automates most effectively, routine analysis, pattern recognition, and information retrieval, are precisely the tasks that many degree programmes train graduates to perform. The degrees that retain value will be those that develop skills AI cannot replicate: complex judgment, ethical reasoning, creative synthesis, and the ability to manage AI-augmented workflows. Institutions that adapt their curricula will thrive. Those who continue teaching 20th-century skills will produce graduates whose degrees depreciate rapidly.

Fourth, the opportunity cost of a degree is its largest and least visible component. The $150,000 in forgone earnings during four years of full-time study is five times larger than the average direct cost after financial aid. This cost is particularly acute for students from lower-income families, where four years of lost earnings can mean the difference between household stability and financial distress. Shorter degree formats, such as the UK’s three-year bachelor’s, reduce this cost substantially.

Fifth, the cross-country evidence demonstrates that institutional design matters as much as individual choice. Germany’s zero-tuition model produces graduates with no debt and a 55% earnings premium. The UK’s income-contingent system protects graduates from crushing repayments during low-earning years. The US system, with its combination of high tuition, fixed repayment schedules, and limited quality controls, produces the highest returns for those who choose well and the most devastating outcomes for those who do not.

MASEconomics Explains

Conclusion

The economics of higher education reveals a market where the aggregate statistics and the individual experience diverge sharply. A bachelor’s degree, on average, remains a strong investment, with a median annual return of 12.5% and a lifetime earnings premium of $1.2 million. But that average conceals a distribution where engineering and computer science graduates capture returns exceeding half a million dollars, while nearly half of all master’s programmes deliver negative value. In a world being reshaped by artificial intelligence, the premium attached to specific skills will shift faster than university curricula can adapt. The degree itself is not disappearing, but the assumption that any degree from any institution in any field justifies its cost is no longer supported by the data.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.