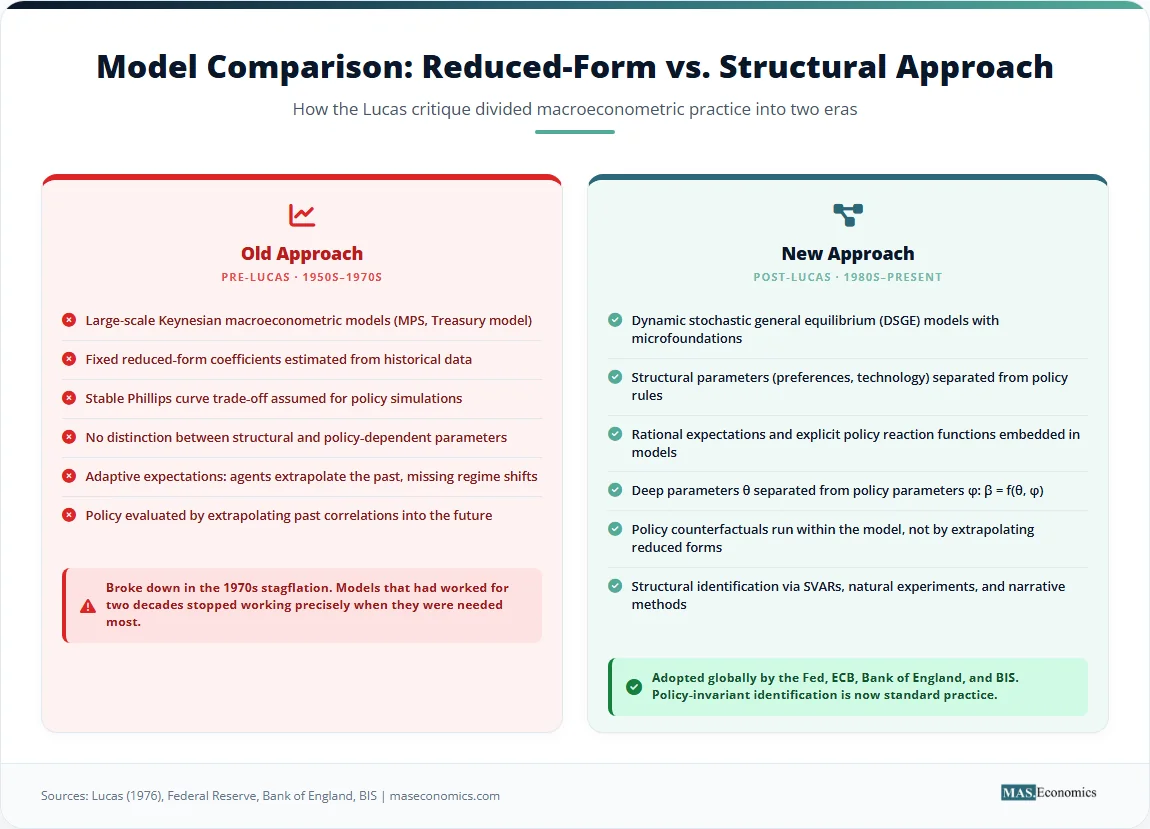

In 1976, Robert E. Lucas Jr. published a paper that forced economists to rethink the entire enterprise of macroeconomic policy evaluation. The Lucas critique argued that the statistical relationships estimated from historical data, the equations used by central banks, treasuries, and international agencies to forecast the effects of policy, would themselves change when the policy rule changed. A Phillips curve estimated under one monetary regime could not be used to predict unemployment under a different one, because the behaviour of workers and firms would adapt. A consumption function fitted to data before a tax reform would fail after the reform, because households would rearrange their spending. The critique was not a technical footnote. It was an indictment of the large-scale macroeconometric models that dominated policymaking in the 1960s and 1970s, and it reshaped how macroeconomics is done.

The core of the argument was simple, but its consequences ran deep. Econometric models of the day treated the past as a guide to the future, assuming that the coefficients linking policy instruments to economic outcomes were stable, or structural. Lucas showed that these coefficients were not structural at all. They were reduced-form parameters: mixtures of deep behavioural constants, policy-rule parameters, and the expectations that the policy rule itself shaped. When the policy rule changed, those mixtures changed. The same deep preferences could produce a different observed relationship between inflation and unemployment, or between tax rates and output, if the government altered the systematic part of its behaviour. The breakthrough was to put rational expectations at the centre of policy analysis, showing that what policymakers thought they knew from the data was in part an artifact of their own past choices.

The critique was born out of the stagflation crisis of the 1970s. Standard Keynesian models, with their stable Phillips curve trade-off between inflation and unemployment, predicted that an expansionary policy could buy lower unemployment at the cost of only a modest rise in inflation. But when the United States, the United Kingdom, and other advanced economies ran expansionary demand policies against the oil-price shocks of 1973 and 1979, the trade-off vanished. Inflation and unemployment rose together. The models that had worked for two decades stopped working in the very period they were needed most. Lucas’s argument explained why: the prevailing policy regime had conditioned expectations, and the attempt to exploit the old relationships changed those expectations in ways that the models could not capture.

What the Critique Says, Formally

Consider a simple macroeconometric relationship of the kind that populated the Federal Reserve Board’s MPS model or the United Kingdom’s Treasury model. An outcome variable \( y_t \), say inflation, output, or unemployment, is regressed on a policy instrument \( x_t \) and a set of control variables \( z_t \). The estimated equation is a reduced form:

The parameter \( \beta \) is interpreted as the effect of policy on the outcome. If the government or central bank changes \( x_t \) by a unit, \( y_t \) is expected to change by \( \beta \) units. This interpretation underpinned the counterfactual simulations that policymakers used to decide on tax rates, government spending, and interest rates between the 1950s and 1970s.

Lucas’s point was that \( \beta \) is not a structural parameter. It is the product of a deeper decision process. The behaviour of the private agents generating \( y_t \) depends on their expectations about future policy, which in turn depend on the systematic component of \( x_t \). Suppose the policy authority follows a rule of the form:

where \( E_{t-1}[y_t] \) is the expected value of the outcome based on last period’s information and \( \phi \) is a policy response parameter. The reduced-form coefficient \( \beta \) estimated from the historical joint distribution of \( y_t \) and \( x_t \) will embed \( \phi \). If the authority decides to change \( \phi \), for example, to respond more aggressively to output gaps or to ignore expected inflation, private agents will observe the new rule and adjust their expectation formation. The historical \( \beta \) no longer describes the new regime. A regression that was stable under the old policy rule becomes misspecified under the new one.

The distinction between deep structural parameters and reduced-form parameters is the analytical core of the critique. Deep structural parameters describe preferences, technology, and constraints: things like the curvature of utility, the elasticity of substitution between capital and labour, or the degree of nominal rigidity. These are invariant to policy rules. Reduced-form parameters are the coefficients obtained by solving the agent’s optimisation problem given a particular policy rule. They are functions of both the deep parameters and the policy parameters:

where \( \theta \) denotes the vector of deep parameters. When \( \phi \) changes, \( \beta \) changes, even though \( \theta \) remains constant. The policy simulation that treats \( \beta \) as fixed is therefore built on a logical contradiction: it assumes that the very agents whose behaviour generated \( \beta \) will not notice that the rule has changed.

This can be illustrated with the expectations-augmented Phillips curve, the most famous example of the critique in action. Let inflation \( \pi_t \) be determined by:

where \( u_t \) is unemployment, \( u_n \) is the natural rate, and \( \varepsilon_t \) is a supply shock. The parameter \( \lambda \) measures the sensitivity of inflation to the unemployment gap, a structural parameter reflecting wage and price flexibility. Under adaptive expectations, \( E_{t-1}[\pi_t] \) was modelled as a distributed lag of past inflation, yielding a stable negative relationship between inflation and unemployment, the Phillips curve. Under rational expectations, however, the expected inflation term depends on the entire structure of the economy, including the monetary policy rule. If the central bank targets an inflation rate \( \pi_t^* \) with interest rate adjustments, the reduced-form relationship between \( \pi_t \) and \( u_t \) depends on the monetary rule’s parameters. A central bank committed to low inflation will produce a different empirical correlation than a central bank that systematically accommodates price increases, even if \( \lambda \) and \( u_n \) are unchanged.

The formal distinction generalises. For any dynamic stochastic general equilibrium setup, the solution of the model under a particular policy rule takes the form of a state-space representation. The observationally relevant reduced form is:

where \( A(\phi) \) and \( B(\phi) \) are matrices that depend on the policy parameter vector \( \phi \). Econometric estimation of \( A \) and \( B \) from a period in which \( \phi \) was constant will recover the equilibrium of that specific policy regime. Using those estimates to predict the economy under a different \( \phi \) is invalid unless the analyst has separately identified the deep parameters \( \theta \) that underlie the mapping from \( \phi \) to \( A \) and \( B \). This is the structural identification problem that the Lucas critique imposed on macroeconometrics.

Assumptions and Boundaries

The Lucas critique is built on strong assumptions, and its force depends on how fully they are satisfied. The central assumption is that private agents form expectations rationally, using all available information, including knowledge of the policy rule. If agents are backward-looking, using only past data to form expectations, the coefficients of reduced-form relationships remain stable when policy rules change, at least until the new data eventually alter the adaptive scheme. The critique is then weaker in the short run and may apply with a lag. Behavioural macroeconomics has documented persistent deviations from full rationality, from inertial expectations to diagnostic expectations, that soften the knife-edge of the Lucas argument.

A second assumption is that the policy regime change is understood and believed. A change in the interest-rate rule that the private sector does not perceive, or does not trust to be permanent, will not immediately alter behaviour. The speed and completeness of learning matter. The literature on central bank credibility is in part about how quickly agents internalise a new regime. The Volcker disinflation of 1979–1982 is a classic case. The Federal Reserve’s shift to tight money was initially met with scepticism; wage and price setters continued to expect high inflation for several years, and only after the recession of 1982 did inflation expectations fall sharply. The Lucas critique operated with a credibility lag.

A third boundary is that not all estimated relationships are vulnerable. Relationships that are truly structural, those describing technological constraints, demographic patterns, or laws of nature, are immune. The capital-output ratio in a Cobb-Douglas production function, the Solow residual, or the elasticity of substitution between skilled and unskilled labour are not directly altered by a shift in the monetary policy rule. The critique targets behavioural relationships that embed expectations: consumption functions, investment equations, wage-setting rules, money-demand equations, and any other equation where a decision-maker’s forecast of the future enters explicitly or implicitly.

The critique also requires that the policy rule be systematic. Purely random policy shocks, as opposed to changes in the systematic component, do not alter the reduced-form coefficients in a fundamental way; they are part of the error term and can be handled with standard econometric methods. The problem arises when the systematic part of policy changes, because then the entire correlation structure between instruments and outcomes shifts. This distinction has practical force. A temporary fiscal stimulus in a recession affects the economy but does not change the long-run relationship between taxes and output if the public expects the tax structure to revert. A permanent shift in the marginal tax rate, by contrast, can alter labour supply, saving behaviour, and the measured multiplier on government spending.

Finally, the critique assumes that agents’ decisions embed the entire future path of policy. In realistic settings, decision-making is boundedly rational, and agents use simple heuristics. The formal DSGE models that emerged after Lucas incorporate rational expectations but also recognise that frictions and limited information can dampen the effects the critique describes. The empirical force of the critique is thus a matter of degree, not an all-or-nothing proposition.

Evidence Supporting the Lucas Critique

The Lucas critique has been tested in several major policy episodes, and the balance of evidence supports its central insight, though with significant variation across contexts.

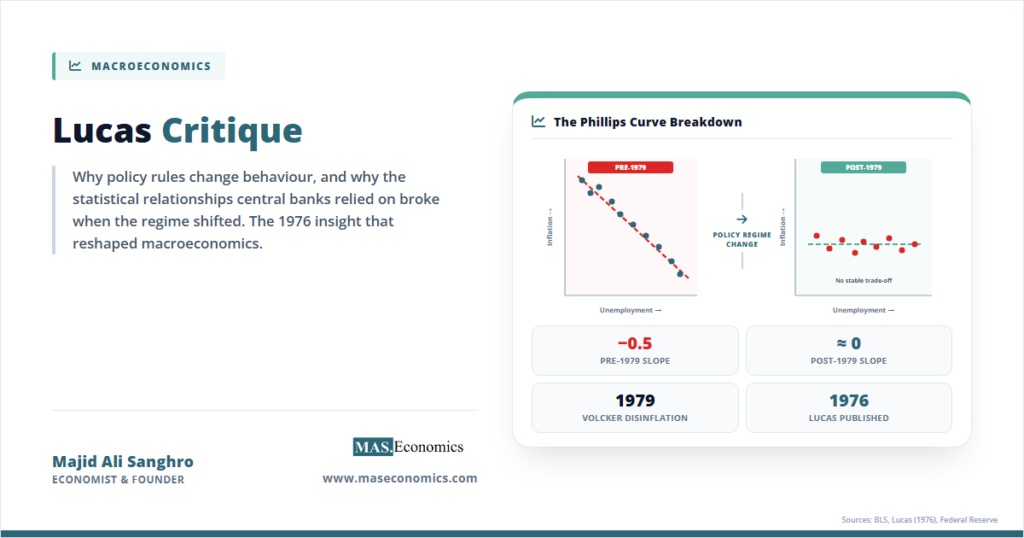

The most famous test is the Phillips curve itself. Chart 1 plots annual US inflation and unemployment from 1960 to 1999, split into two regimes: the pre-1979 period and the post-1979 period after Paul Volcker’s monetary regime change. The pre-1979 data show the classic negative Phillips curve correlation; the post-1979 data show no such correlation, with low inflation coexisting with a range of unemployment rates. The curve that appeared stable under the old regime was not a structural law. It was a reduced form conditioned on a particular monetary policy rule, an accommodative one, that broke when the rule changed.

Source: U.S. Bureau of Labor Statistics. Annual averages of the Consumer Price Index (CPI-U) and the civilian unemployment rate. The break in the Phillips curve correlation after the 1979 monetary regime shift is a central piece of evidence for the Lucas critique.

The table below summarises additional key episodes where the Lucas critique was tested. The common pattern is that large, clearly communicated shifts in policy rules, monetary regime changes, tax reforms, and changes in transfer programmes are associated with the breakdown of previously estimated reduced-form relationships. Smaller or less credible changes produce more ambiguous results, as the theory would predict.

| Policy regime shift | Estimated relationship that broke | Evidence |

|---|---|---|

| Volcker disinflation, 1979–1982 | Phillips curve trade-off (inflation–unemployment) | Curve flattened; subsequent low inflation without permanently high unemployment |

| US Tax Reform Act, 1986 | Consumption–income relationship | Marginal propensity to consume out of current income shifted as households adjusted portfolios |

| United Kingdom inflation targeting, 1992 | Wage-setting equations | Reduced-form wage equation parameters changed; forward-looking expectations became more important |

| Canada’s Goods and Services Tax, 1991 | Spending equations by category | Intertemporal substitution in durable goods altered measured income elasticities |

| Swedish pension reform, 1994–1998 | Saving rate function | Shift from defined-benefit to notional defined-contribution altered aggregate saving behaviour |

|

||

Selected policy regime shifts and associated breakdowns of estimated reduced-form relationships. The examples illustrate the core Lucasian argument that policy-rule changes alter the parameters of standard macroeconometric equations.

The consumption function provides another instructive test. Pre-1970s Keynesian consumption functions related aggregate consumption to current income with a high marginal propensity to consume. The permanent income hypothesis and the life-cycle theory had already suggested this relationship was not structural, but the Lucas critique showed why: the observed relationship depended on the stochastic process for income, which in turn depended on fiscal and monetary policy. When tax policy shifted under the 1986 Tax Reform Act in the United States, the correlation between measured current income and spending changed. Similarly, the 2001 and 2008 tax rebates in the United States produced marginal propensities to consume that differed markedly from those estimated in earlier periods, consistent with the Lucas prediction that the measured effect of fiscal policy is regime-dependent. Recent work by the International Monetary Fund using narrative-based fiscal shocks has confirmed that the estimated impact of tax changes is sensitive to the broader policy configuration, exactly as the critique implies.

Empirical tests differ in their verdict, however, when the policy change is not clearly communicated or is not believed to be permanent. Christopher Sims’s work on policy regime shifts found that some reduced-form relationships remained stable across historical breaks. The literature on identified vector autoregressions has tended to find that imposing structural restrictions from theory, a direct response to the Lucas critique, improves model robustness, confirming the critique’s practical relevance for econometric modelling.

How the Lucas Critique Reshaped Macroeconomics

The Lucas critique did more than point out a flaw in 1960s-era macroeconometrics. It launched a research programme that transformed the way macroeconomists build models, evaluate policy, and interpret data. The shift was toward models with explicit microfoundations, where the parameters that govern individual behaviour, tastes, and technology are separated from the parameters that describe the policy rule. That shift produced the modern dynamic stochastic general equilibrium framework, which, whatever its well-known limitations, is a direct descendant of the Lucas reparative programme.

The first concrete effect was on the design of monetary policy. Before the critique, central banks used estimated Phillips curves to calculate the unemployment cost of disinflation and the output gain from expansion. The Lucas critique showed that these calculations were unreliable unless the central bank’s own reaction function was taken into account. The response was the rational expectations policy literature of the 1980s and the eventual adoption of inflation targeting. A well-understood, predictable monetary policy rule stabilises expectations and reduces the volatility of output and inflation, but it also renders the historical correlations between those variables uninformative about the effects of deviating from the rule. The Phillips curve is a case in point: the low-inflation era after 1990 is consistent with a flat Phillips curve precisely because central banks have kept inflation expectations anchored, a regime-dependent outcome that the models of the 1960s could not have produced.

The critique also reshaped fiscal policy analysis. The idea that tax cuts “pay for themselves” through enhanced growth depends on a parameter, the elasticity of taxable income with respect to tax rates, that is itself a function of the tax system. Large tax reforms change this elasticity, so estimates from one tax regime may not apply to another. The debate over the revenue effects of the US Tax Cuts and Jobs Act of 2017 directly hinged on this Lucasian point. The Congressional Budget Office and Office for Budget Responsibility in the United Kingdom now make explicit judgments about how behavioural responses to tax changes depend on the design of the tax system rather than applying fixed elasticities. The construction of structural fiscal multipliers, separating the cyclical component of the deficit from the structural component, similarly draws on the critique’s logic, as the relationship between the deficit and output depends on the fiscal policy rule in place.

The international macroeconomics literature absorbed the critique through the analysis of exchange rate regimes. The relationship between money supply changes and exchange rate movements depends on whether the central bank follows a fixed or floating exchange rate rule. Mundell-Fleming results that applied under capital controls no longer held when capital mobility changed, and the parameters of exchange rate equations shifted with the adoption of inflation targeting and the abandonment of intermediate regimes. The ERM crisis of 1992–1993 and the emerging-market currency crises of the 1990s were studied through the lens of the Lucas critique, with an emphasis on how the perceived commitment to a peg altered the dynamics of speculative attacks.

At the level of econometric practice, the critique drove the development of structural vector autoregressions, which attempt to identify deep shocks that are invariant to policy regimes. It also motivated the use of natural experiments and narrative-based identification strategies in macroeconomics. If reduced-form correlations are regime-dependent, the only reliable way to estimate policy effects is to find episodes where the policy change was clearly exogenous, a fiscal reform driven by ideology rather than by the state of the economy, or a monetary regime change imposed by an external event. The work of Christina Romer and David Romer on narrative identification of US tax changes, and the subsequent growth of micro-based macroeconomics, is the intellectual grandchild of the Lucas critique.

The critique also influenced financial regulation. The stress-testing frameworks used by the Federal Reserve, the European Central Bank, and the Bank of England are built on structural models of bank behaviour that incorporate the feedback from the regulatory environment to bank actions. A stress test based on a historical correlation between asset prices and bank lending would be vulnerable to the Lucas objection: the test itself, by changing banks’ expectations about regulatory tolerance, would alter their behaviour in a crisis, rendering the historical correlation obsolete. The Basel III reforms and the move toward countercyclical capital buffers reflect an appreciation that the relationship between capital ratios and lending is not policy-invariant.

In macroeconomics, the critique remains foundational even as its implications continue to be debated. The New Keynesian model, the workhorse of modern central banking, incorporates rational expectations and explicit policy rules precisely so that the Lucas critique is respected. The model’s parameters, the slope of the Phillips curve, the intertemporal elasticity of substitution, and the degree of price stickiness are intended to be structural. Policy counterfactuals are then conducted within the model rather than by extrapolating from a historical reduced form. The global adoption of this methodology across the advanced-economy central banking community is perhaps the deepest testament to the critique’s influence.

The power of the argument has also extended beyond macroeconomics. The analysis of labour market programmes, education reforms, and health insurance expansions increasingly acknowledges that the measured effect of a programme depends on the scale and permanence of the intervention. An experiment that gives a small group of workers a wage subsidy will not generalise to a nationwide programme if firms and workers alter their equilibrium responses. The literature on policy evaluation now routinely invokes the “external validity” problem, which is a direct analogue of the Lucas critique: the treatment effect is not a fixed constant but a parameter that depends on the policy environment in which it is embedded.

MASEconomics Explains

Four economic concepts behind the Lucas critique

Conclusion

The Lucas critique stands as one of the most consequential arguments in the history of macroeconomic thought because it demonstrated that the statistical relationships on which policy had been based were not fixed laws of nature but regime-contingent correlations. The insight forced economists to distinguish structural parameters from reduced-form parameters and to build models that could survive a change in the policy rule. The shift to micro-founded macroeconomics, the adoption of structural econometric techniques, and the global spread of inflation targeting and rule-based fiscal frameworks all trace a line back to Lucas’s 1976 paper. The critique did not end disagreement about the effects of policy, but it changed the terms of the debate. A forecast that does not account for the regime in which it is made is no longer considered a forecast; it is considered a category mistake.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.