On 31 December 2025, the enhanced premium tax credits that had subsidised 24.3 million Americans on Affordable Care Act marketplaces expired. KFF estimates that without congressional action, average net premium payments for subsidised enrollees will rise 114% in 2026, from USD 888 to USD 1,904 per year. The Urban Institute projects 4.8 million more uninsured. The Congressional Budget Office puts the ten-year coverage loss at over 14 million. Insurers, anticipating that healthier enrollees would drop out, set 2026 rates roughly 4 percentage points higher than they otherwise would have.

The Economics of Health Insurance is the study of how insurance contracts pool medical risk under asymmetric information. The story now playing out in the United States is a textbook adverse-selection cycle, the same one Kenneth Arrow and Mark Pauly described in the 1960s. Two failures dominate the field: adverse selection, where the insured knows more about their risk than the insurer, and moral hazard, where coverage itself raises the use of care. Every functioning health system, public or private, is an answer to those two problems.

What follows defines the contract structure, derives the two failures from foundational theory, examines the live 2026 American test case, surveys design responses in the United States, the United Kingdom, and Germany, reviews the empirical record from the RAND and Oregon experiments, and explains why these information failures matter far beyond medicine. The differences in design are why rising healthcare costs vary so sharply across countries with otherwise similar income levels.

What Health Insurance Is

Health insurance is a risk-pooling contract. Individuals face uncertain medical expenditures that can move from zero in a healthy year to several hundred thousand dollars in a year of serious illness. Without insurance, a household must either save a large precautionary balance or face bankruptcy. Insurance solves this by collecting premiums from a large group and paying the medical costs of the few who fall ill. The mechanism rests on the law of large numbers. As the pool grows, actual claims converge toward expected claims, allowing the insurer to set a premium that covers expected costs plus an administrative loading factor.

This structure separates insurance from a simple prepayment scheme. Prepayment means paying in advance for care a household expects to use. Insurance protects against catastrophic costs that the household hopes to avoid. When the pool includes both healthy and sick individuals, a cross-subsidy occurs. Healthy members pay more in premiums than they receive in claims, while sick members receive more than they pay. The role of risk pooling is precisely to enable this cross-subsidy under predictable conditions, and the size of the willingness to pay for it follows directly from risk aversion.

Every health system manages the cross-subsidy differently. Some pool the entire population through taxation. Others pool through regulated competition between sickness funds. Others rely on voluntary private contracts with employer-based pools. All must confront the same two information failures that threaten the stability of any pool that does not include everyone.

How Health Insurance Operates

Four actors populate the health insurance market: the insurer, the insured, the provider, and the regulator. The insurer sets premiums based on expected loss. For a basic contract, the premium \( P \) equals the expected loss \( E[L] \) plus a loading factor \( \lambda \) to cover administrative costs and profit.

The system works when the insurer can estimate \( E[L] \) accurately for each pool. Asymmetric information distorts this estimate. The insured possesses private knowledge about their health status, lifestyle, and risk tolerance that the insurer cannot observe at the same cost. The regulator sets rules about what insurers can ask, what they must cover, and how prices can vary. The provider, paid separately, has its own incentives to recommend more or less care depending on the payment model. This four-way interaction creates two distinct market failures, each first formalised in the 1960s and still central to health policy today.

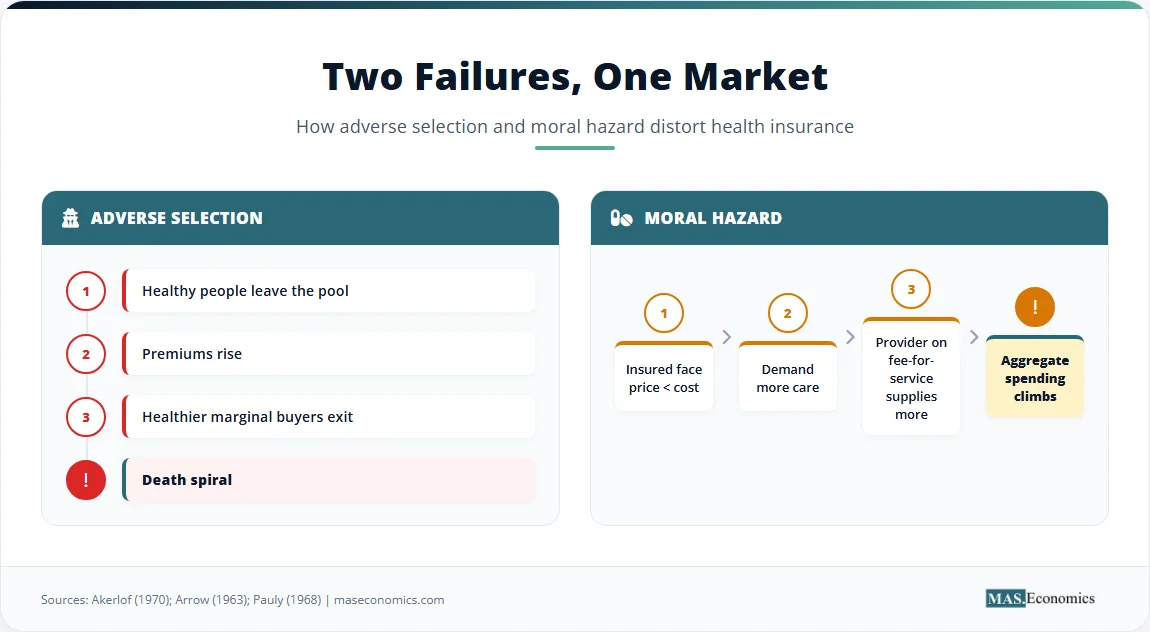

Adverse Selection

Adverse selection occurs when individuals with higher expected medical costs are more likely to purchase insurance at any given premium. Because the insurer cannot perfectly distinguish high-risk from low-risk applicants, the premium must reflect the average risk of the entire pool. Low-risk individuals find this average premium too high relative to their expected costs. They exit the pool. As low-risk members leave, the average risk of the remaining pool rises, forcing the insurer to raise premiums again. This drives out the next tier of relatively healthy members.

This is Akerlof’s market for lemons applied to healthcare. The logic predicts a death spiral. Premiums climb until only the sickest individuals remain, at which point the market collapses. Kenneth Arrow identified this cycle in his 1963 American Economic Review paper, noting that competitive insurance markets systematically underproduce coverage when individual risk is private. The same logic underpins the broader study of information economics and connects directly to the signalling literature, where informed parties seek credible ways to reveal type. In healthcare, signalling is largely impossible: a healthy person cannot credibly prove they are healthy without expensive medical examinations, and even then, private information about lifestyle and family history remains.

Moral Hazard

Moral hazard arises after the contract is signed. Once insured, the marginal cost of seeking medical care drops for the patient. A visit that would cost USD 200 out of pocket might cost only USD 20 with a copay. The insured individual consumes care up to the point where personal marginal benefit equals personal marginal cost, even when the social marginal cost far exceeds that benefit. Mark Pauly formalised this in his 1968 American Economic Review article, showing that welfare losses from overconsumption can offset the gains from risk protection.

The patient faces price \( P_{patient} \), which is less than the true cost \( P_{provider} \). Quantity consumed \( Q \) rises above the efficient level.

Supply-side moral hazard compounds the problem. Physicians paid on a fee-for-service basis face incentives to increase volume. When the patient is insulated from the cost, the physician can recommend additional tests or procedures with little resistance. The two effects compound. Demand-side moral hazard pushes patients to seek more care; supply-side moral hazard pushes providers to deliver more once the patient arrives. Together, they drive aggregate spending upward and form a core mechanism behind the cost growth documented in the analysis of why medical costs keep rising. Both failures are textbook examples of market failure caused by information asymmetry rather than externalities, which means the policy response cannot be limited to taxes or property rights alone.

The 2026 American Cliff

The expiration of enhanced premium tax credits at the end of 2025 created a live test of adverse-selection theory at national scale. Understanding what is happening requires the contractual background. The Affordable Care Act of 2010 established marketplaces with guaranteed issue, meaning insurers cannot deny coverage based on pre-existing conditions, and required community rating, meaning premiums can vary only by age, geography, family size, and tobacco use. These rules eliminated medical underwriting. With underwriting gone, the only defence against adverse selection was the individual mandate, which required everyone to buy coverage or pay a tax penalty.

The Tax Cuts and Jobs Act zeroed out the mandate penalty starting in 2019. The American Rescue Plan Act of 2021 then replaced the lost discipline with a carrot rather than a stick. Enhanced premium tax credits capped what enrollees paid at 8.5% of household income, with lower-income households paying nothing for a benchmark plan. The Inflation Reduction Act extended these subsidies through 2025. The combination of guaranteed issue plus generous subsidies pulled healthy enrollees into the pool. ACA marketplace enrollment rose from 11.4 million in 2020 to 24.2 million in 2025. The uninsured rate fell to a historic low of 7.6% in 2023.

When Congress let the enhanced subsidies expire on 31 December 2025, it removed the mechanism that had been keeping the pool diverse. Insurers, modelling the predictable response, raised 2026 sticker premiums by a median of 18% across 312 marketplace insurers. Internal rate filings cited adverse selection explicitly. United Healthcare, in its Maryland filing, wrote that healthier members would leave at a disproportionately higher rate, “increasing market morbidity in 2026.” Across the country, insurers added a roughly 4-percentage-point margin specifically to cover the expected sicker pool. KFF’s follow-up survey of 1,117 marketplace enrollees in early 2026 found that 9% had already become uninsured and 28% had switched to thinner plans. Among enrollees aged 18 to 29, half had left the marketplace entirely. The age distribution of the exits matters: younger, healthier people leave first, exactly as Arrow predicted in 1963. The remaining pool is older and sicker, justifying still higher premiums next year if no policy correction follows.

This sequence is not a side effect of the policy change. It is the policy change. Subsidies were not just a transfer to low-income households. They were the mechanism that solved the adverse-selection problem created by guaranteed issue. Removing them while keeping guaranteed issue in place is exactly the design configuration Akerlof’s model says cannot hold together.

How Three Systems Pool Their Risk

The American system is one of four broad designs in advanced economies. Each solves the two information failures differently, and each pays a different price for its solution.

The United Kingdom took the most direct path with the National Health Service. Founded in 1948, the NHS eliminates adverse selection entirely through mandatory universal coverage funded by general taxation. Everyone is in the pool by default. No one opts out, so no death spiral can occur. To control moral hazard, the NHS relies on structural mechanisms rather than financial ones. General practitioners act as gatekeepers. A patient cannot see a specialist or receive an expensive diagnostic test without a GP referral. The system delivers care at 11.3% of GDP, less than two-thirds of the US figure of 17.6%, but at the cost of long waits for non-emergency procedures. As of November 2025, 7.31 million people were on NHS waiting lists in England. The NHS converted financial rationing into time rationing.

Germany uses a social health insurance model. Statutory sickness funds cover roughly 90% of the population. Community rating prevents funds from charging higher premiums to sicker enrollees. To stop funds from competing by attracting only healthy members, Germany introduced the morbi-RSA risk equalisation mechanism in 2009. This mechanism design transfers money from funds with below-average risk to funds with above-average risk, removing the incentive for cream-skimming. The system spends 12.7% of GDP, between the US and UK levels, and offers shorter waits than the NHS while preserving universal coverage. On the moral hazard side, Germany uses reference pricing for pharmaceuticals, modest copayments, and sectoral budget caps to restrain spending. The contrast with private bargaining solutions like Coasian bargaining is sharp: in healthcare, regulators step in because transaction costs and information asymmetries make private negotiation impossible at scale.

The United States runs a hybrid. Employer-sponsored coverage handles roughly 55% of the population. Medicare covers Americans aged 65 and over, Medicaid covers low-income households, and the ACA marketplaces cover the remaining individual market. Each segment solves adverse selection differently. Employer pools work because employees join for the job, not the insurance, mixing healthy and sick by accident of hiring. Medicare and Medicaid work because everyone in the eligible group is automatically pooled. The marketplaces are the weakest link. They depend on regulatory tools, such as guaranteed issue, community rating, and subsidies, to mimic the universal-pool effect. When any of those tools weaken, the pool destabilises, which is the dynamic now playing out in 2026.

Health Insurance in Data

Figure 1. Spending levels reflect design choices: single-payer systems control aggregate cost through gatekeeping, social-insurance systems through community rating and risk equalisation, private-dominant systems through cost-sharing. Sources: OECD Health Statistics 2024; CMS National Health Expenditure Accounts.

| Archetype | Country Example | Adverse Selection Solution | Moral Hazard Solution |

|---|---|---|---|

| Single-payer tax-funded | UK NHS, Canada Medicare | Mandatory universal pool | GP gatekeeping, waiting lists |

| Social health insurance | Germany, France, Japan | Community rating + risk equalisation | Reference pricing, copays |

| Regulated private mandate | Switzerland, Netherlands, ACA marketplaces | Individual mandate, guaranteed issue | Cost-sharing, network design |

| Voluntary private | US pre-ACA individual market | Underwriting (now restricted) | Deductibles, coinsurance |

| |||

The four archetypes are not just descriptive labels. Each is a distinct equilibrium between coverage breadth, cost control, and consumer choice. The single-payer model maximises coverage and aggregate cost control at the expense of choice and waiting times. The voluntary private model maximises choice and quality flexibility at the expense of coverage. The regulated mandate and social insurance models sit in between, attempting to combine elements of both through layered regulation. None achieves all three goals simultaneously, which is the closest thing to a free lunch the field offers.

Where the Standard Model Breaks Down

The standard model of adverse selection and moral hazard is powerful but incomplete. Behavioural evidence complicates the predictions. Research by Baicker, Mullainathan, and Schwartzstein in the Quarterly Journal of Economics (2015) shows that individuals misjudge their own risk in both directions. Some healthy people overestimate their risk and buy generous coverage. Some sick people underestimate their risk and remain uninsured. These errors blunt the clean death-spiral prediction of Akerlof’s model and explain why some markets that should have collapsed in theory have remained stable in practice. Behavioural inertia also matters: people often stay in plans they would not actively choose today simply because changing requires effort, which slows the death-spiral dynamic.

The empirical magnitude of moral hazard also falls short of theoretical predictions. The RAND Health Insurance Experiment, running from 1974 to 1982, randomly assigned families to plans with different cost-sharing levels. It found that higher copays reduced medical use, but the reduction came largely from fewer doctor visits and hospitalisations, including appropriate care. Health outcomes for the average enrollee did not significantly worsen, though they did for low-income participants with chronic conditions. The Oregon Medicaid Experiment, led by Amy Finkelstein and published in the Quarterly Journal of Economics in 2012, used a state lottery as a natural experiment. Expanding Medicaid increased hospital admissions and prescription drug use but did not significantly reduce emergency department visits for non-emergency conditions, contrary to the prediction that better access would substitute primary care for emergency care. Mental health and self-reported financial security improved sharply; physical health markers like blood pressure and cholesterol did not.

Supply-side moral hazard likely dominates demand-side effects in the aggregate. In fee-for-service systems, physicians control the volume of care. When a third-party payer covers the bill, the physician has little financial incentive to restrain ordering. This supply-side dynamic explains why cost-sharing alone rarely controls aggregate spending in any country. It is also why payment reform, capitation, bundled payments, and value-based contracts have become a larger focus of US policy debate than patient cost-sharing.

Universal coverage systems still face constraints. They do not eliminate scarcity. They ration through queues, clinical guidelines, and formulary restrictions rather than prices. Implicit rationing is a feature of the design, not a bug, and explains why universal-coverage countries continue to debate access even after solving adverse selection. The question is never whether to ration. It is who rations and on what basis.

Why Health Insurance Lessons Travel

The framework developed in health insurance shapes thinking far beyond medicine. Adverse selection appears in any market where buyers know more than sellers about the quality of what is being traded, or vice versa. Used-car markets, life insurance, credit, and labour contracts all face versions of the lemons problem. Moral hazard appears wherever a contract changes the incentives of one party in ways the other cannot observe or police, from deposit insurance changing bank risk-taking to disability benefits changing job-search effort.

The policy responses developed in healthcare also generalise. Mandates address adverse selection; cost-sharing addresses moral hazard; risk equalisation prevents cream-skimming in any regulated market with mandatory coverage. The financial regulator who designs deposit insurance is solving the same kind of problem as the health regulator who designs marketplace rules. Both must combine universal coverage with incentive discipline, and both must accept that imperfect information makes a fully efficient outcome impossible.

This is why the 2026 American test case is being watched so closely beyond healthcare circles. If a sufficiently generous subsidy can hold a guaranteed-issue pool together, then regulated private markets in many other domains can be designed the same way. If the pool unravels predictably as soon as the subsidy fades, the lesson is that universal coverage requires either a universal pool by tax or a universal mandate with permanent fiscal commitment behind it. The middle ground turns out to be more fragile than its designers hoped.

MASEconomics Explains

3 economic concepts behind health insurance

Conclusion

The Economics of Health Insurance centres on two information failures, and the live evidence in the United States in 2026 is showing what happens when one of those failures is left unaddressed. Adverse selection threatens the existence of the market by driving low-risk individuals out of the pool. Moral hazard threatens the efficiency of the market by encouraging overconsumption of care. The four main insurance-design archetypes are all attempts to solve these failures through mandates, risk equalisation, cost-sharing, and gatekeeping. Empirical evidence from the RAND and Oregon experiments shows that moral hazard effects are smaller than pure theory predicts for high-value care, while supply-side incentives and behavioural biases play a larger role than the standard model assumes. Every functioning health system, whether the NHS in the United Kingdom, the statutory sickness funds in Germany, or the ACA marketplaces in the United States, acknowledges these constraints and enforces rationing through either prices, queues, or clinical limits. The frameworks developed for health insurance now shape policy in deposit insurance, unemployment systems, and any other domain where contracts must function under asymmetric information.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.