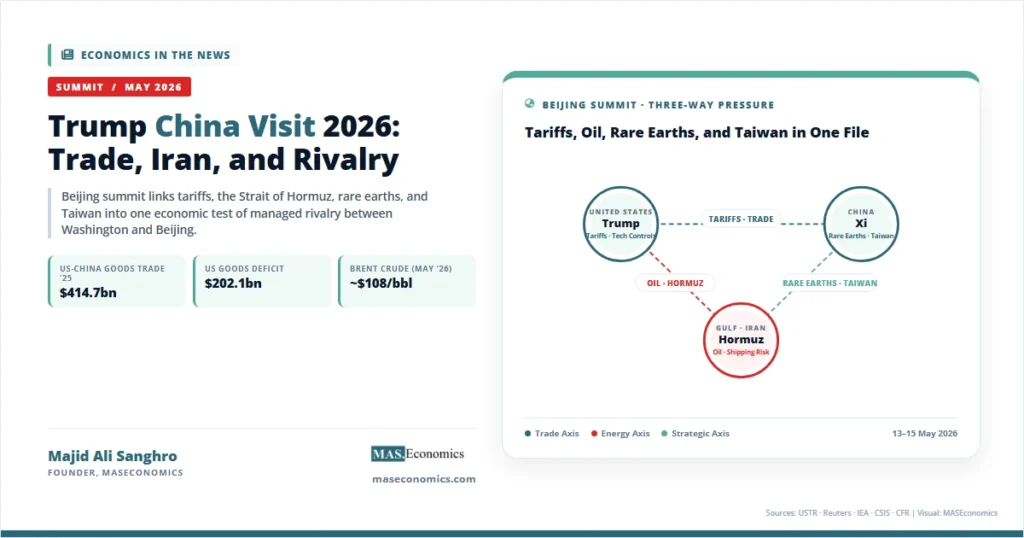

Donald Trump landed in Beijing on 13 May 2026 for a two-day summit with Xi Jinping as the Trump China visit 2026 became a test of three linked pressures: a damaged US-China trade relationship, the ongoing war with Iran, and the macroeconomic risk circling the Strait of Hormuz. Reuters reported that the leaders met with trade, Taiwan, artificial intelligence, rare earths, and Iran on the agenda, while China signalled limited goodwill by renewing export licences for hundreds of US beef processing plants in the days before the meeting.

The visit matters because US-China relations are no longer only about tariffs. They now sit at the intersection of energy security, supply chains, sanctions enforcement, financial markets, military escalation, and domestic inflation. The United States wants China to buy more American goods, reduce pressure on strategic supply chains, and use its leverage with Iran. China wants tariff relief, technology access, recognition of its regional red lines, and a more stable external environment for its own slowing economy.

The economic question is not whether one summit can repair the relationship. It cannot. The question is narrower: whether Beijing and Washington can move from tariff escalation to managed rivalry while a Middle East war threatens oil flows, shipping insurance, and inflation expectations.

Beijing Summit Meets Oil Shock

The 2026 Beijing summit unfolded under different conditions from Trump’s 2017 state visit. In 2017, the central issue was a bilateral goods deficit and a US administration preparing to confront China’s trade practices. In 2026, the agenda is wider. The trade war has already damaged bilateral goods flows, China has tightened its grip on rare earth supply chains, the United States has expanded technology controls, and the Iran war has turned the Strait of Hormuz into a global macroeconomic risk.

The Council on Foreign Relations framed this shift bluntly. Writing days before the summit, senior fellow Heidi Crebo-Rediker argued that the centre of gravity in US-China economic competition has moved away from tariffs and toward something more structural: China’s control over critical minerals, rare earths, and the magnet supply chains that underpin modern military capability. CSIS Trustee Chair Scott Kennedy added that China feels remarkably more confident than at the 2017 summit, in part because Beijing successfully used rare earth export controls to push back when tariffs spiked past 140 percent in 2025. That confidence sets the bargaining frame.

A first sign of limited movement came before the leaders met. China renewed licences for more than 400 US beef processing plants, a step Reuters interpreted as a goodwill signal. The practical effect is narrow but the signal is broader. Agriculture has long been the easiest area for leaders to announce purchases because it produces visible gains for US farm states and gives China a non-strategic way to show cooperation. The same logic shaped the 2020 Phase One agreement, when China’s agricultural purchase commitments became central to the political presentation of that deal, and the October 2025 Busan agreement, where tariffs were cut to 47 percent in exchange for resumed US soybean purchases.

Energy is more complicated. Reuters reported that the summit included efforts to revive US LNG and crude oil exports to China after tariffs sharply reduced some flows. A deal involving US energy would serve two purposes. It could give Trump a headline export win. It could also help China diversify away from Gulf supply during the Iran war. The economics, however, are not straightforward. Chinese LNG demand has been weak, tariff relief may not be enough to redirect long-term contracts, and China’s refiners have spent years building flexibility across Russian, Iranian, Brazilian, Canadian, and Middle Eastern supply.

The Iran dimension adds another layer. The Strait of Hormuz is not only a military chokepoint. It is a price-setting artery for crude oil, LNG, shipping insurance, fertilizer, and petrochemical feedstocks. China’s position is constrained by its own energy dependence. The US Energy Information Administration’s China country analysis lists Russia and Saudi Arabia as China’s top crude oil suppliers in 2024, with Iran having the largest single-country increase in crude exports to China. Al Jazeera reported that China buys more than 80 percent of Iran’s shipped crude exports, making Beijing by far Tehran’s largest energy customer. That position creates leverage over Iran while also exposing China to any disruption in Gulf shipping.

Fifty Years of Strategic Bargaining

US-China relations have always mixed economic bargaining with security calculations. The modern relationship began with strategic necessity, not commercial friendship. The US Department of State’s Office of the Historian records that rapprochement with China in 1972 followed a period in which Sino-Soviet tension encouraged Beijing to seek a new opening, and Washington eased travel and trade restrictions dating from the Korean War period.

Nixon’s 1972 visit produced the Shanghai Communiqué, which did not resolve the Taiwan issue but created a framework for managing disagreement. The document recognised that the two countries had deep differences, yet it opened the way for economic exchange. The economic relationship that followed was gradual at first. China was still poor, inward-looking, and politically closed. Its later transformation came from reform and opening, the growth of export manufacturing, accession to the World Trade Organization in 2001, and integration into global value chains.

The relationship then shifted from strategic alignment against the Soviet Union to commercial interdependence. US firms saw China as a production base and a consumer market. Chinese policymakers saw US demand, technology, and capital as accelerators of industrialisation. The economic gains were large but not evenly distributed. American consumers benefited from lower prices. Multinational corporations benefited from efficient supply chains. Chinese workers and exporters benefited from global market access. Some US manufacturing regions experienced job losses and political backlash. That distributional conflict later became central to the trade war.

MASEconomics has discussed this broader tension in The Global Tariff War of 2025-2026, where tariff escalation is treated as a change in the operating system of global trade rather than a temporary policy dispute. The same framework applies here. The Beijing visit is not a return to the pre-2018 world. It is an attempt to stabilise a relationship after both governments accepted that full economic integration had become politically unsafe. The deeper structural story is covered in Is Deglobalization Real?, which shows that global trade has not collapsed but has reorganised around strategic blocs.

The history also explains why presidential visits to China carry unusual weight. They are not routine diplomatic stops. They tend to occur when the relationship needs resetting, reframing, or crisis management. Nixon opened the door. Reagan expanded economic ties despite ideological hostility. Clinton tried to combine engagement with public pressure on human rights. George W. Bush managed China’s WTO-era rise and later attended the 2008 Beijing Olympics. Obama worked with Xi on climate diplomacy while tensions rose over cyber issues and the South China Sea. Trump’s first visit in 2017 came before the trade war hardened. His 2026 visit comes after the trade war has already reshaped flows.

| Visit | Economic Context | Strategic Context | Legacy |

|---|---|---|---|

| Richard Nixon, 1972 | Limited direct commerce after decades of separation | Sino-Soviet split and Cold War realignment | Shanghai Communiqué and diplomatic opening |

| Ronald Reagan, 1984 | Early reform-era trade expansion | Anti-Soviet alignment with ideological tension | Normalisation deepened despite political differences |

| Bill Clinton, 1998 | China moving toward WTO accession | Engagement mixed with human rights pressure | Commercial integration gained political momentum |

| George W. Bush, 2001–2008 | China became a major WTO-era export platform | Counterterrorism, Taiwan, and Olympics diplomacy | Supply chain dependence deepened |

| Barack Obama, 2009–2016 | China became central to global demand and climate diplomacy | South China Sea and cyber tensions rose | Cooperation and rivalry became simultaneous |

| Donald Trump, 2017 and 2026 | Trade deficit, tariffs, energy, agriculture, technology controls | Taiwan, Iran, rare earths, and strategic rivalry | Managed rivalry replaced engagement optimism |

|

|||

Sources: US Department of State Office of the Historian; US presidential travel records. Table: MASEconomics.

Crisis-Management Visit in Partial Decoupling

Presidential visits to China have usually marked transitions in the global economy. Nixon’s visit marked the start of the strategic opening. Reagan’s visit came as China’s reforms were beginning to connect the country to world markets. Clinton’s visit came when the United States was debating whether economic engagement would change China’s domestic and international behaviour. George W. Bush’s visits came when China’s WTO accession was transforming global manufacturing. Obama’s visits came when China had become too large to treat as a developing-country add-on to the world economy.

Trump’s 2026 visit belongs to a different category. It is not an opening visit, an engagement visit, or a reform-era commercial visit. It is a crisis-management visit in an age of partial decoupling. The United States is not trying to integrate China more deeply into every strategic sector. China is not trying to appear as a passive beneficiary of US-led globalisation. Both sides are trying to reduce damage while preserving leverage. CSIS senior adviser Edgard Kagan captured the new normal in his summit preview: during Trump’s trip, the United States is focused on the economy and Iran, while China is focused on stability and progress on Taiwan. The two priority sets do not align, but they overlap enough to make a deal possible.

That distinction is key. In earlier decades, a successful summit often meant more integration: more trade, more investment, more educational exchange, more joint ventures, and more official dialogue. In 2026, a successful summit may mean fewer shocks: fewer tariff jumps, fewer export-control surprises, fewer rare earth disruptions, fewer sudden sanctions, and fewer oil-market shocks linked to Iran. Stability itself has become the deliverable.

The history of summits also shows why the Taiwan issue returns in every major reset. The Shanghai Communiqué left room for diplomatic ambiguity. That ambiguity helped preserve stability, but it also ensured that Taiwan would remain the most sensitive issue in the relationship. In 2026, Taiwan matters not only as a security question but also as a semiconductor question. MASEconomics has treated chips as a central economic power asset in The Economics of the Semiconductor Industry. Any US-China deterioration around Taiwan would affect advanced chips, capital goods, AI systems, insurance pricing, and risk premia across Asian markets.

China sees this clearly. Beijing’s message to Washington is that trade concessions cannot be separated from security respect. The United States sees the opposite risk: economic concessions to China may strengthen a strategic rival if they relax controls around advanced technologies. That is why the 2026 summit focuses on less sensitive goods, agriculture, energy, tourism, health, and investment procedures rather than a broad reopening of technology flows.

Trade War Rewrites Interdependence

The economic core of the summit is the trade war. The United States began imposing major tariffs on Chinese goods during Trump’s first term. The Biden administration preserved many of those measures and added technology restrictions. Trump’s second term escalated the tariff framework again, peaking above 140 percent before the October 2025 Busan agreement cut the rate to 47 percent in exchange for rare-earth flow commitments and resumed soybean purchases. In February 2026, the US Supreme Court ruled that the International Emergency Economic Powers Act does not authorize presidential tariffs, prompting the administration to fall back on a temporary 10 percent global surcharge under Section 122 of the Trade Act of 1974, alongside existing Section 301 measures. The result is a trading relationship that remains large but is no longer expanding naturally.

Official US data show the scale of the change. The Office of the US Trade Representative reports that US goods and services trade with China totalled an estimated $658.9 billion in 2024. It also reports that US goods trade with China fell to an estimated $414.7 billion in 2025, with US goods exports to China at $106.3 billion and imports from China at $308.4 billion. The US goods deficit with China fell to $202.1 billion in 2025, down from 2024, but that reduction reflected lower trade volumes rather than a clean improvement in competitiveness.

This distinction matters for economic interpretation. A smaller bilateral deficit can result from stronger exports, weaker imports, recession, tariffs, supply-chain diversion, or statistical rerouting through third countries. In 2025, the sharp fall in both exports and imports points to trade compression. That can reduce the headline deficit while still hurting producers, consumers, and firms that rely on intermediate inputs.

The logic of tariff incidence is covered in MASEconomics’ consumer tariff burden analysis. Tariffs do not automatically punish only foreign exporters. Depending on elasticities, exchange rates, market power, and supply-chain structure, the burden can fall on foreign firms, domestic importers, consumers, or downstream producers. That is why tariff wars create political tension inside the country imposing them. They protect some firms while raising costs for others.

The trade war also changed global supply chains. US firms shifted some assembly to Vietnam, Mexico, India, and other locations. Chinese firms moved outward to protect market access. Consumers still bought goods with Chinese content, but some goods entered through different routes. MASEconomics’ work on nearshoring and friendshoring shows that trade policy does not simply reduce imports; it changes where production is booked, where final assembly occurs, and which country captures the visible export statistic.

The Beijing summit’s reported discussion of a managed trade mechanism reflects this new environment. Reuters reported that officials were considering reciprocal tariff cuts on a limited set of non-sensitive goods, possibly in the $30 billion to $50 billion range. Salvador Santino Regilme, writing for Al Jazeera, expected a comprehensive trade deal to remain out of reach because the structural sources of rivalry are unresolved, and predicted instead a limited package involving tariff pauses, purchase commitments, rare earth arrangements, or a framework for future negotiations. That managed approach would not restore free trade. It would create a controlled channel for goods that both governments consider economically useful and politically tolerable.

Hormuz Turns Trade Into Security

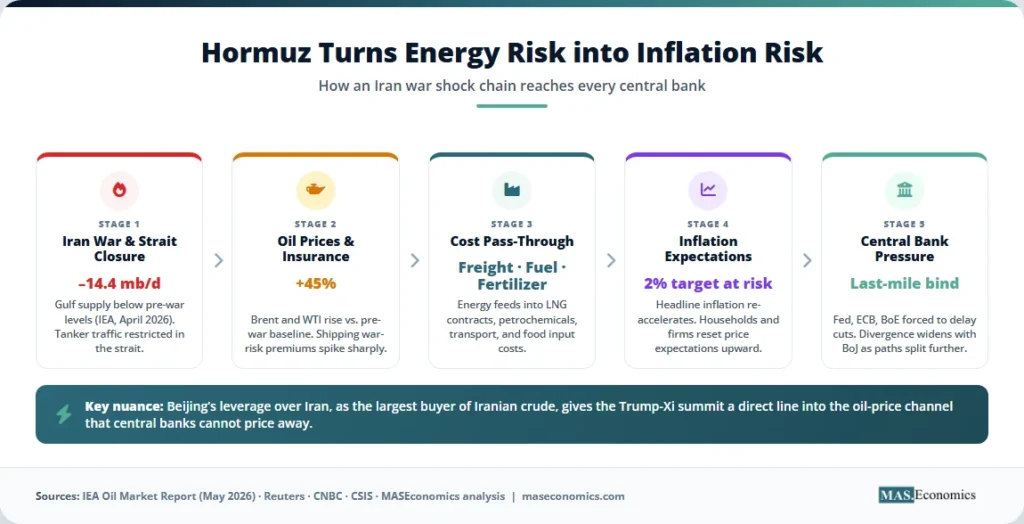

The Iran war changes the meaning of the Trump-Xi meeting because energy risk has entered the trade conversation. The Strait of Hormuz is the narrow maritime passage between Iran and Oman through which a large share of Gulf oil and LNG normally moves. MASEconomics has treated the Strait as a global chokepoint in The Strait of Hormuz and has analysed the inflation channel in Oil Price Shocks.

The numbers are now extreme. The International Energy Agency’s May 2026 Oil Market Report records that output from Gulf countries affected by the closure of the Strait was 14.4 million barrels per day below pre-war levels in April, with cumulative supply losses from Gulf producers exceeding one billion barrels since the war began on 28 February. Brent crude closed at $107.77 per barrel on 12 May (CNBC) after trading as high as $120 in April. WTI and Brent are both up more than 45 percent since the start of the war. Saudi Aramco chief executive Amin Nasser warned that the oil market would take until 2027 to normalise if the Strait stayed blocked beyond mid-June.

China’s stance on Hormuz is shaped by three facts. First, China is a major crude importer. Second, a large share of its Gulf-linked energy supply depends on secure shipping routes. Third, China has deep oil ties with Iran while also needing stable trade with the United States, Europe, and Asian importers. That mix produces a strong preference for de-escalation, but not necessarily alignment with Washington.

Beijing’s foreign ministry stated in May 2026 that the tense situation in the Strait required an early and full ceasefire, respect for the sovereignty and security of coastal countries, attention to regional concerns, and protection of the legitimate interests of the international community. The wording is deliberately broad. It does not endorse US military pressure. It does not fully endorse Iran’s actions. It places China in the position of stability broker while preserving its relationship with Tehran. CSIS confirmed that ahead of the summit, Iranian Foreign Minister Abbas Araghchi visited Beijing, and the resulting readout positioned China as having already weighed in with Iran about reopening the Strait.

That stance is consistent with China’s wider Middle East strategy. Beijing wants access to energy, diplomatic influence, and commercial contracts without becoming the region’s security guarantor. It has cultivated relations with Iran, Saudi Arabia, the Gulf states, Iraq, and Pakistan. Its 2023 role in supporting Saudi-Iranian diplomatic normalisation showed that China can act as a diplomatic convenor when the incentives fit. The Iran war is different because it involves the United States directly and because oil-market stress feeds back into China’s own economy.

For Trump, China’s Iran leverage is attractive but difficult to activate. Dan Grazier, senior fellow at the Stimson Center, told Al Jazeera he had no doubt Trump would try to enlist Xi to press Iran to settle, but warned that the US-led naval blockade of Iranian ports complicates the picture: as the leaders met, the US Navy was intercepting tankers bound for China, Tehran’s largest crude buyer. Trump’s “Project Freedom” naval escort operation, announced after Brent briefly broke $114, attempted to guide commercial vessels through the strait, but shipping companies have remained hesitant to transit even under US Navy cover.

This is where economic sanctions meet great-power bargaining. Sanctions are not only legal restrictions. They are systems of enforcement, evasion, insurance, shipping, finance, and diplomatic signalling. China’s role in Iranian oil trade gives Washington a reason to press Beijing. It also gives Beijing a bargaining chip. The economic cost of escalation is also visible in MASEconomics’ analysis of presidential rhetoric during the Iran crisis, where market volatility tracked statement-by-statement risk.

| Issue | US Objective | China Objective | Economic Channel |

|---|---|---|---|

| Tariffs | Open selected Chinese markets and reduce the bilateral deficit | Lower US tariffs without changing the state-led model | Import prices, export orders, supply-chain routing |

| Agriculture | Boost farm exports and show visible trade wins | Offer goodwill in non-strategic goods | Beef, soybeans, feed grains, rural incomes |

| Energy | Revive LNG and crude exports to China | Diversify supply during Gulf disruption | Oil prices, LNG contracts, shipping insurance |

| Iran and Hormuz | Use Chinese leverage to pressure Tehran | Preserve Iranian ties while avoiding oil shock | Crude flows, sanctions evasion, inflation expectations |

| Rare earths | Reduce vulnerability in strategic minerals | Maintain leverage over critical inputs | EVs, defence systems, electronics, clean energy |

| Taiwan | Preserve deterrence and semiconductor security | Limit US support for Taipei | Chip supply, risk premia, Asian investment |

|

|

|||

Xi Reads Leverage Through Risk

China is approaching the visit from a position that mixes confidence with economic pressure. On one side, Beijing has more leverage than it had during earlier phases of the relationship. It dominates parts of the rare earth supply chain, remains central to global manufacturing, buys large amounts of energy and commodities, and has built alternative financial and diplomatic channels with sanctioned economies. On the other side, China’s own economy faces property-sector weakness, demographic pressure, weak household confidence, youth labour-market stress, and export dependence at a time when advanced economies are rethinking supply-chain exposure.

Julian Evans-Pritchard, head of China economics at Capital Economics, summarised Beijing’s calculation on rare earths as a determination to maintain as much of that strategic position as possible. The Chinese Ministry of Commerce’s December 2025 rule, which requires foreign suppliers to secure Chinese approval before exporting any product containing 0.1 percent or more Chinese rare-earth content, made that point structural. The same logic applies to the broader summit. Xi’s view is not simply that China can resist the United States. It is that China manage the relationship without appearing to concede. A stable US market remains valuable. Access to advanced technology remains important. The dollar system still shapes global finance. American allies still matter for high-end capital goods, chips, software, aviation, finance, and research networks. China can absorb pain, but it cannot ignore the US-led system without cost.

That is why Beijing’s public message emphasises dignity, stability, and reciprocity. China wants Washington to accept that competition must be bound. It wants trade relief without conceding that its industrial policy is illegitimate. It wants cooperation on Iran and energy without becoming an American subcontractor. It wants economic engagement without surrendering its position on Taiwan.

Domestic politics also matter. Xi cannot appear weak before a US president who has used tariffs as a central policy instrument. Trump cannot appear to reward China without a visible concession. That makes symbolic outcomes important. Beef licences, aircraft purchases, energy contracts, tourism channels, business delegation meetings, and a possible investment board can all create the appearance of progress while leaving deeper conflicts unresolved.

The risk is that symbolic progress becomes a substitute for structural clarity. The core disputes remain: subsidies, state-owned enterprises, forced technology transfer allegations, cyber risk, export controls, Taiwan, rare earths, AI chips, shipping lanes, sanctions evasion, and military posture. A summit can reduce immediate risk, but it cannot remove the incentives that created the rivalry.

Three Scenarios from the Beijing Table

The most likely economic outcome is selective stabilisation rather than a grand bargain. Heidi Crebo-Rediker described the best realistic outcome as a tacit extension of the current truce with some deliverables on agriculture, aerospace, and investment. A realistic package could therefore include renewed agricultural access, limited tariff exclusions, energy purchase discussions, technical talks on investment screening, new channels for export-control communication, and joint language on avoiding escalation around Hormuz. Such a package would be economically useful, but it would not end the trade war.

A stronger outcome would include a credible mechanism for reducing tariffs on a defined basket of non-sensitive goods. That would help importers, exporters, and some consumers. It would also lower uncertainty for firms planning supply chains. Even a tariff mechanism would face verification problems. Managed trade depends on targets, exclusions, product definitions, rules of origin, and political compliance. The Phase One experience showed that purchase targets are vulnerable to macro shocks, market conditions, and diplomatic breakdown.

A weaker outcome would be a summit with ceremony but little economic substance. That would still matter if it prevents immediate escalation. Financial markets often price the absence of bad news as a positive result when the starting point is tense. It would leave businesses with little clarity on tariffs, rare earths, energy contracts, and sanctions enforcement.

The Iran channel has the highest macroeconomic stakes. If China can help keep Hormuz partially open, push for ceasefire language, or protect energy flows without direct alignment with Washington, the market effect could be meaningful. Lower oil-risk premia would reduce pressure on gasoline, freight costs, fertilizer, and inflation expectations. That matters for central banks because energy shocks complicate the final stage of disinflation. MASEconomics has discussed this monetary-policy tension in Sticky Services Inflation and Central Bank Divergence in 2026.

There is also a fiscal dimension. War, tariffs, and subsidy races all interact with public debt. Higher defence spending, tariff compensation for affected sectors, industrial policy subsidies, and energy-price relief can widen fiscal pressures. That links the summit to the broader issue of sovereign debt sustainability. Great-power rivalry is not free. It shifts costs through budgets, prices, and risk premia.

Risks After the Beijing Summit

The first risk is that trade relief becomes too narrow to matter. If tariff reductions apply only to a small basket of goods, the political announcement will be larger than the economic effect. Firms will still face uncertainty over strategic sectors, export controls, customs enforcement, and future escalation.

The second risk is that Iran’s diplomacy becomes linked to Taiwan in ways that create new instability. If China expects restraint on Taiwan in exchange for pressure on Tehran, Washington will face a hard trade-off. Any perceived weakening of US support for Taiwan could raise risk premia in semiconductor markets and unsettle Asian allies. Any refusal to discuss Taiwan could reduce China’s willingness to help on Iran.

The third risk is that Hormuz disruption feeds into inflation before diplomacy works. Energy shocks move quickly. Trade negotiations move slowly. If shipping insurance costs stay elevated, tanker availability falls, and crude prices remain above $100, the summit’s diplomatic language will not be enough to prevent pass-through into fuel, freight, and food prices.

The fourth risk is that both governments use the summit to buy time while preparing for further confrontation. Managed rivalry can be stable if both sides believe rules are durable. It becomes unstable if each side treats the pause as an opportunity to strengthen its position before the next escalation. Rare earths, AI chips, shipping lanes, and sanctions enforcement are all areas where that risk is high.

MASEconomics Explains

4 economic concepts behind the Beijing summit

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Trump China visit 2026 is a crisis-management summit within a larger shift from economic engagement to managed rivalry. The visit links the main pressures now shaping the world economy: tariff fatigue, supply-chain restructuring, energy insecurity, sanctions enforcement, rare earth dependence, Taiwan risk, and the inflationary consequences of the Iran war. A successful summit will not restore the old US-China model. It will create limited channels for trade, reduce immediate escalation risk, and test whether China can help stabilise the Strait of Hormuz without abandoning its own strategic interests. The durable result is a more conditional form of interdependence in which trade continues, but every major economic flow carries a security calculation.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics