When a steel mill faces a 30 percent wage increase, two questions decide whether it survives: how much can it shift from labor to capital, and at what cost? The answer is not contained in the production function alone. It depends on the curvature of the firm’s isoquants, the geometry of how easily one input replaces another along the same level of output. That single property has a name. The elasticity of substitution measures how readily a firm can swap one input for another when relative input prices change, and it sits at the center of nearly every quantitative model of production, trade, and growth.

The concept was formalized by John Hicks in The Theory of Wages (1932) and reworked by Joan Robinson and others into the form used today. It is not an abstract object. It tells policymakers how much the factor share will move when wages rise. It tells trade economists whether comparative advantage will widen or compress. It tells growth modelers whether capital deepening will keep paying off or run into diminishing returns. A small number, often written as the Greek letter sigma, carries an unusual amount of weight.

Definition of Elasticity of Substitution

The elasticity of substitution is the percentage change in the capital-to-labor ratio divided by the percentage change in the marginal rate of technical substitution, holding output fixed. Stripped of formalism, it answers a single question: when the relative price of labor rises by one percent, by what percent does the firm adjust its input mix?

If the firm can substitute easily, a small change in relative prices produces a large change in the input ratio. The elasticity is high. If the firm cannot substitute, perhaps because production requires a fixed proportion of operators per machine, the input ratio barely moves even when relative prices swing sharply. The elasticity is low.

DEFINITION

The marginal rate of technical substitution, written MRTS, is the slope of the isoquant. Under cost minimization, it equals the ratio of input prices, so a one-percent rise in the wage-rental ratio \( w/r \) translates directly into a one-percent change in MRTS. The elasticity, therefore, tells us how much the cost-minimizing input ratio responds to a change in factor prices. It is a property of technology, not of any particular firm’s behavior.

Because both numerator and denominator are measured in logarithms, sigma is a pure number. It carries no units. A sigma of 0.5 means the same thing for a steel mill in Pittsburgh and a textile factory in Karachi.

Isoquant Curvature

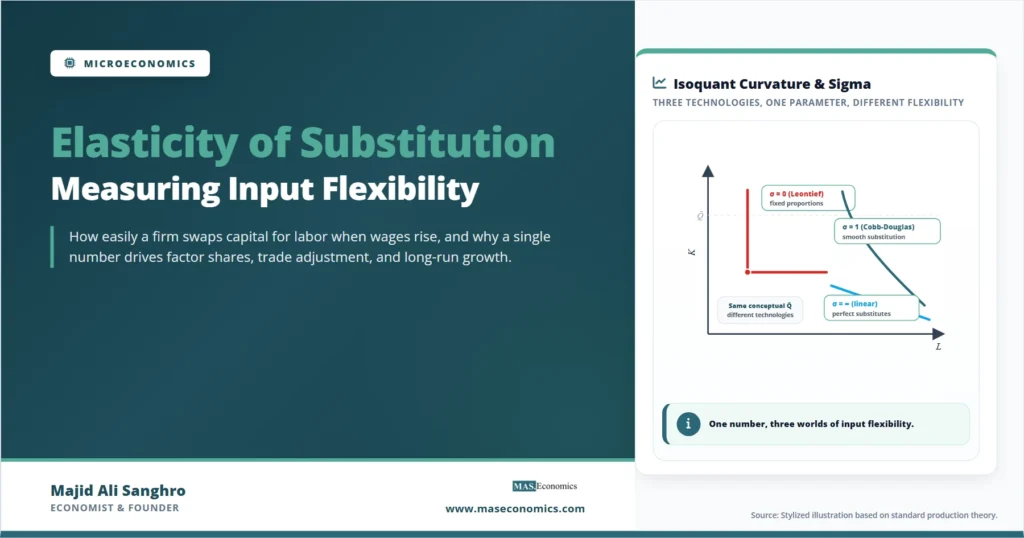

The cleanest way to see what sigma does is to look at the shape of an isoquant. An isoquant collects all input combinations that produce a given level of output. Its curvature carries the substitution story.

A nearly straight isoquant indicates high substitutability. Inputs are close to interchangeable, so the firm slides along the isoquant with little resistance as relative prices change. A sharply bent, L-shaped isoquant indicates the opposite. The firm must use inputs in something close to fixed proportions, and shifting along the curve requires a large change in MRTS for even a small change in the input ratio. Sigma captures this curvature in a single number that is comparable across industries and time periods.

Three benchmark cases anchor intuition. When sigma is zero, the isoquant is L-shaped. The Leontief technology used to model fixed-recipe production, one operator per machine, one driver per truck, has this property. A wage increase does not move the input ratio at all. When sigma is one, the isoquant has the smooth hyperbolic shape produced by the Cobb-Douglas production function. Factor shares are constant, which is the empirical regularity that made the Cobb-Douglas form attractive to economists in the first place. When sigma is infinite, the isoquant is a straight line. Inputs are perfect substitutes, and the firm chooses entirely on the basis of which is cheaper per unit of marginal product.

The CES Production Function

The constant elasticity of substitution (CES) function, introduced by Arrow, Chenery, Minhas, and Solow in 1961, generalizes the three benchmarks into a single family. Output Q is produced from labor L and capital K according to:

CES PRODUCTION FUNCTION

The parameter rho governs everything. When rho approaches 1, sigma goes to infinity, and the function becomes linear. When rho approaches 0, sigma approaches 1, and the function collapses to Cobb-Douglas. When rho approaches negative infinity, sigma approaches 0, and the function becomes Leontief. The CES function is the only functional form that holds sigma constant along the entire isoquant, which is why it became the workhorse of modern growth and trade theory. The original paper, Arrow, Chenery, Minhas, and Solow (1961), fit the form to international cross-section data and found sigma values clustered around but not equal to one, enough to challenge the universal Cobb-Douglas assumption.

Estimating sigma is not straightforward. The CES function is nonlinear in its parameters, so direct nonlinear least squares is sensitive to starting values. A standard alternative is the Kmenta approximation, a second-order Taylor expansion that linearizes the model around sigma equal to one. Another is to estimate the first-order condition for cost minimization directly: the log of the capital-labor ratio is a linear function of the log of the factor-price ratio, with sigma as the slope coefficient.

Implications of Benchmark Values

Sigma takes any non-negative value, but three benchmark values carry the bulk of the intuition. Each implies a different world for cost-minimization, factor shares, and the burden of input-price shocks.

| Sigma value | Technology | Isoquant shape | Factor share when wages rise | Example |

|---|---|---|---|---|

| σ = 0 | Leontief (fixed proportions) | L-shaped, right angle | Labor share rises one-for-one with wages | One operator per machine, one driver per truck |

| 0 < σ < 1 | Limited substitution | Sharply curved | Labor share rises modestly | Skilled-unskilled labor in manufacturing |

| σ = 1 | Cobb-Douglas | Smooth hyperbolic | Labor share unchanged | Aggregate economy benchmark |

| σ > 1 | Strong substitution | Gently curved | Labor share falls | Routine work and automation |

| σ = ∞ | Perfect substitutes | Straight line | Firm uses cheaper input only | Different brands of an identical commodity |

|

Source: MASEconomics editorial synthesis based on Arrow, Chenery, Minhas, and Solow (1961) and standard producer-theory results.

|

||||

The middle row of that table is the one most economists worry about. A sigma between zero and one means labor and capital are gross complements: a wage increase raises the labor share of income. A sigma above one means they are gross substitutes: a wage increase pushes capital in and lowers the labor share. The distinction is empirical, and it determines whether minimum-wage policies, payroll taxes, and skill-biased technical change widen or compress the wage distribution.

Factor Shares and Income Distribution

The link between sigma and the distribution of income runs through a single identity. The labor share of national income is the wage bill divided by total output. When the wage rises, and the capital-labor ratio adjusts, what happens to that ratio depends on sigma.

FACTOR SHARE RESPONSE

This is why Thomas Piketty’s argument in Capital in the Twenty-First Century rests on a number. Piketty argued that sigma between capital and labor in the modern economy is greater than one, so as capital accumulates and the relative price of labor rises, the capital share grows and the labor share shrinks. Several authors disputed the magnitude that Matthew Rognlie and others put on aggregate sigma, putting it closer to 0.5, but the analytical engine is the same. A single elasticity parameter governs whether the long-run distribution of income tilts toward labor or capital.

The same logic operates inside trade theory. In the Heckscher-Ohlin model, opening to trade shifts relative goods prices and, through the Stolper-Samuelson theorem, relative factor prices. The size of the wage response depends on how easily firms substitute between skilled and unskilled labor within sectors. A higher sigma dampens the wage gap. A lower sigma amplifies it. Studies of trade exposure and labor-market adjustment from the late 1990s onward repeatedly tripped on this parameter, with estimates differing across industries, countries, and time horizons.

Short-Run and Long-Run Elasticities

One of the most useful distinctions in applied work is between short-run and long-run elasticities. In the short run, capital is fixed, and only flexible inputs adjust. Sigma measured this way is small. In the long run, the firm can redesign its plant, retrain workers, and retool production lines. Sigma is larger, sometimes much larger.

Note. The same industry can show a short-run sigma near 0.2 and a long-run sigma above 1.0. The short-run number governs the response to a temporary shock. The long-run number governs the response to a permanent structural change. Conflating the two is a common source of overstated or understated policy effects.

Empirical studies of energy and capital provide the clearest illustration. After the 1973 and 1979 oil shocks, manufacturing firms in OECD countries showed almost no immediate substitution away from energy. Plant designs assumed cheap fuel, and re-engineering takes years. Over the following decade and a half, however, energy use per unit of output fell sharply as old plants were retired and new ones built around efficient designs. The implied long-run elasticity between energy and capital was several times the short-run value.

The same pattern shows up in the response of capital-labor ratios to permanent wage changes. Berman, Bound, and Griliches’s work on skill-biased technical change, and later research on automation, suggests that the elasticity of substitution between routine labor and machinery has risen over time as the relative price of computing power has collapsed. What was once complementary has, in many tasks, become a substitute.

Empirical Estimation Methods

The cleanest estimating equation for sigma comes directly from cost-minimization. Setting MRTS equal to the factor-price ratio and taking logs gives:

The equation is deceptively simple. Three difficulties complicate it in practice. First, both K/L and w/r are jointly determined by firm-level shocks, which creates endogeneity. Second, the rental rate of capital is rarely observed and must be constructed from depreciation, interest rates, and tax parameters. Jorgenson’s user-cost-of-capital formula is the standard approach. Third, sigma may differ across industries, regions, and time periods, so pooled estimates conflate heterogeneous parameters.

The economics literature has generated a wide range of estimates. Karabarbounis and Neiman, in their influential study of the global decline in labor share, used cross-country panel data and found sigma well above one. Oberfield and Raval, using US manufacturing microdata, found sigma at the plant level closer to 0.5, with the higher aggregate value emerging from substitution between firms rather than within them. The resolution of that gap remains open. It matters because the two pictures imply different policy responses to falling labor shares.

Extensions Beyond Producer Theory

Although elasticity of substitution was born in production theory, the same mathematical structure recurs throughout modern economics. In consumer theory, the elasticity of substitution between two goods in the utility function governs how readily households reallocate spending when relative prices change. In trade theory, the Armington elasticity governs substitution between domestic and imported varieties of the same good, and it sits at the center of nearly every quantitative trade model. In macroeconomics, the elasticity of substitution between consumption today and consumption tomorrow, the inverse of the intertemporal substitution parameter, governs how aggregate saving responds to changes in real interest rates.

In each case, the underlying logic is the same: a single parameter measures how easily one option replaces another when relative prices change. The interpretation shifts with the context, but the diagnostic question does not. A high elasticity says the system is flexible. A low elasticity says the system is rigid. The Solow-Swan growth model, when generalized from Cobb-Douglas to a CES production function, illustrates the consequence directly: a sigma below one bounds long-run growth from capital deepening alone, while a sigma above one allows capital accumulation to sustain growth without technological progress. The functional form is the same; the parameter changes the steady state.

Common Misunderstandings

Three confusions appear often enough to flag explicitly. The first is between the elasticity of substitution and the price elasticity of demand or supply. The two are different concepts measured in different ways. Elasticity of substitution holds output constant and measures input-mix responsiveness along a single isoquant. Price elasticity of demand holds preferences constant and measures quantity responsiveness to price along a demand curve. The symbols are similar, but the objects are not.

The second confusion is between sigma and the share parameter alpha in the CES function. Alpha is a distribution parameter that determines factor shares when sigma equals one; it has no separate substitutability content. Two CES functions can have identical alphas but very different sigmas, and they will behave entirely differently in response to factor-price changes.

The third confusion is treating sigma as if it were universal. The elasticity of substitution is industry-specific, often technology-specific, and frequently time-varying. Aggregate sigma is a weighted average of many micro elasticities, and the weights themselves shift as the composition of output changes. Quoting “the” elasticity of substitution without specifying what is being substituted, at what level of aggregation, and over what horizon, is a frequent source of error in empirical economics.

Explains

Three concepts that connect directly to input flexibility

Continue building your microeconomics foundation with related explainers.

Explore the MASEconomics BlogConclusion

The elasticity of substitution compresses the entire question of input flexibility into a single number, and that compression is what makes it useful. It tells policymakers how factor shares respond to wage changes, tells trade economists how comparative advantage translates into wage dispersion, and tells growth modelers whether capital deepening will sustain long-run growth or run into diminishing returns. The CES production function, by holding sigma constant along the isoquant, gave macroeconomics and trade a tractable way to take the concept to data.

The number is also harder to pin down than the formula suggests. Short-run estimates differ from long-run estimates by an order of magnitude. Plant-level studies and country-level studies disagree by similar margins. The empirical answer in any given case depends on what is being substituted, at what level of aggregation, and over what horizon. For applied work, the value of the concept lies less in the headline number than in the discipline it imposes: stating sigma explicitly, defending its magnitude, and tracing the consequences when it changes. The geometry behind it, the curvature of an isoquant, is simple. The numbers behind it carry, as Hicks understood from the start, a great deal of economic weight.

Frequently Asked Questions

What does an elasticity of substitution of 1 mean?

A sigma of one corresponds to the Cobb-Douglas production function. It means that a one percent change in the wage-rental ratio produces exactly a one percent change in the capital-labor ratio, and factor shares of national income remain constant regardless of relative input prices. It is the benchmark case against which other elasticity values are interpreted.

How is sigma different from price elasticity of demand?

Elasticity of substitution measures how easily a producer swaps one input for another along a single isoquant, holding output constant. Price elasticity of demand measures how the quantity demanded of a good changes in response to its own price. The two share a similar mathematical structure but apply to different problems: input choice in production versus consumer response to price changes.

Why does the elasticity of substitution matter for income distribution?

The change in labor’s share of income in response to a wage increase equals one minus sigma. If sigma is below one, the labor share rises when wages rise. If sigma is above one, the labor share falls. This single parameter therefore governs whether capital accumulation and skill-biased technical change widen or compress the functional distribution of income, which is why it sits at the center of debates over rising inequality.

What is the CES production function?

The constant elasticity of substitution (CES) function, introduced by Arrow, Chenery, Minhas, and Solow in 1961, is a flexible production function in which sigma is constant along every isoquant. It nests Leontief (sigma equals zero), Cobb-Douglas (sigma equals one), and linear technology (sigma equals infinity) as special cases, and it is the standard functional form used in quantitative growth, trade, and macroeconomic models.

Why are short-run and long-run elasticities so different?

In the short run, plant designs, machinery, and worker skills are largely fixed, so a firm cannot easily change its input mix even when relative prices shift. In the long run, plants can be re-engineered, machinery replaced, and workers retrained. Empirical estimates of long-run sigma are therefore commonly several times larger than short-run estimates. Treating them as the same number is a frequent source of misleading policy conclusions.

How do economists actually estimate the elasticity of substitution?

The most common approach regresses the log of the capital-labor ratio on the log of the wage-rental ratio under the assumption of cost minimization; sigma is the slope coefficient. In practice, economists must construct the rental rate of capital using user-cost formulas, deal with the joint determination of inputs and prices, and account for heterogeneity across industries and regions. Estimates therefore range widely, and modern work increasingly uses microdata and instrumental variables to identify sigma more reliably.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics