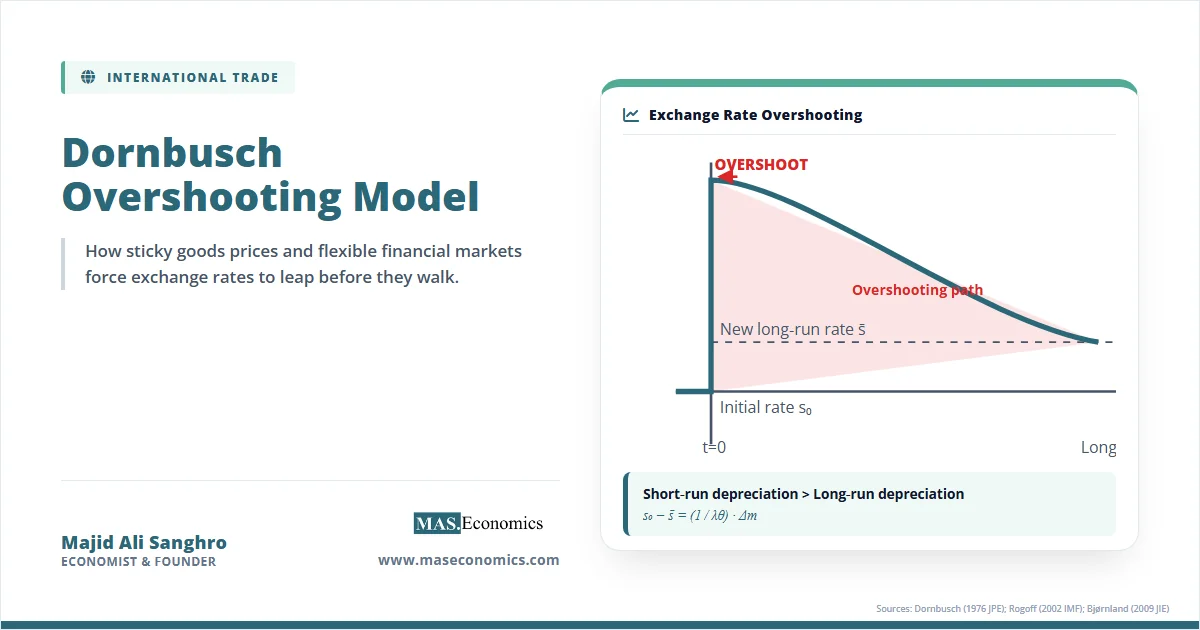

The Dornbusch overshooting model demonstrates that when goods prices are sticky but financial markets adjust instantly, an unanticipated monetary expansion causes the exchange rate to depreciate more in the short run than in the long run, then gradually appreciate back to its new equilibrium. Published by Rüdiger Dornbusch in 1976 in the Journal of Political Economy, this framework solved one of the most puzzling phenomena in post-Bretton Woods macroeconomics. Dornbusch extended the Mundell-Fleming framework to explain why floating exchange rates exhibited volatility that was roughly ten times greater than the volatility of underlying price levels and money supplies. Standard monetarist models predicted smooth, proportional adjustments, but observed exchange rate dynamics were wildly erratic. Dornbusch showed that this erratic behaviour was not a market failure but the logical outcome of differential adjustment speeds across markets. Ken Rogoff (2002) later called the paper “the birth of modern international macroeconomics.”

What the Dornbusch Model Shows

Before Dornbusch’s contribution, the dominant approach to exchange rate determination was the flexible-price monetary model. Under that framework, a 1 percent increase in the money supply led to an immediate 1 percent depreciation of the currency. Purchasing power parity held continuously, and exchange rates moved in lockstep with relative money supplies. The model failed spectacularly when confronted with data from the 1970s. Exchange rates jumped, oscillated, and moved far more than any reasonable assessment of fundamental shocks would suggest. The disconnect between the smooth predictions of monetary models and the jagged reality of foreign exchange markets created a crisis in international finance.

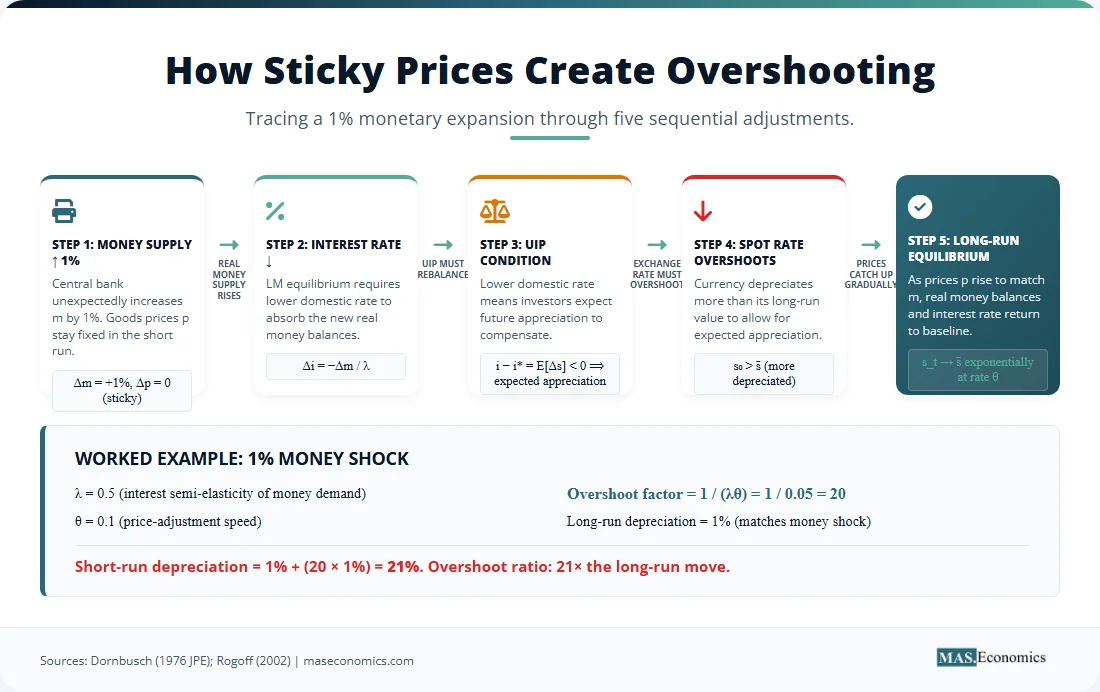

Dornbusch resolved this puzzle by introducing a single, realistic friction: sticky goods prices. In his framework, financial markets, including the foreign exchange market, adjust instantaneously because asset prices can jump to clear the market. Goods markets, however, adjust slowly because firms face menu costs, long-term contracts, and coordination problems that prevent instantaneous price changes. When a central bank expands the money supply, the domestic price level cannot rise immediately to absorb the new liquidity. Because prices are stuck, the real money supply increases. To restore money market equilibrium, the domestic interest rate must fall.

Through the uncovered interest parity condition, a lower domestic interest rate means that investors expect the domestic currency to appreciate in the future. For the currency to be expected to appreciate from tomorrow onwards, it must depreciate beyond its long-run equilibrium today. The exchange rate overshoots its ultimate target, moving too far and too fast, before slowly reversing course as goods prices catch up. This elegant mechanism showed that exchange rate volatility is not evidence of irrationality or speculation; it is the inevitable result of rational arbitrage connecting fast-moving asset markets to slow-moving goods markets.

Dornbusch Model in Equations

The Dornbusch model formalises the overshooting mechanism through four key equations that link the money market, the foreign exchange market, price adjustment, and aggregate demand. The derivation proceeds step-by-step to reveal exactly why the exchange rate must overshoot.

Equation 1: Money Market Equilibrium

The demand for real money balances depends positively on output and negatively on the domestic interest rate:

where \( m_t \) is the log of the nominal money supply, \( p_t \) is the log of the price level, \( y_t \) is the log of output, and \( i_t \) is the domestic nominal interest rate. The parameters \( \phi \) and \( \lambda \) are the income elasticity and interest semi-elasticity of money demand, respectively.

Equation 2: Uncovered Interest Parity

Under perfect capital mobility and risk neutrality, the domestic interest rate equals the foreign interest rate plus the expected rate of depreciation of the domestic currency:

where \( s_t \) is the log of the nominal exchange rate (domestic currency per foreign currency) and \( i_t^* \) is the foreign interest rate, taken as given for a small open economy.

Equation 3: Regressive Expectations

Dornbusch assumed that agents have perfect foresight in continuous time and expect the exchange rate to converge to its long-run equilibrium \( \bar{s} \) at speed \( \theta \):

If the current exchange rate is more depreciated than its long-run level (that is, \( s_t > \bar{s} \)), agents expect future appreciation, so \( \dot{s}_t < 0 \). The parameter \( \theta \) reflects the speed of price adjustment in the goods market.

Equation 4: Price Adjustment

Goods prices adjust gradually in response to excess demand, following a Phillips-curve-type process:

where \( y^d_t \) is aggregate demand, \( \bar{y} \) is potential output, and \( \pi \) is the speed of price adjustment. Aggregate demand depends positively on the real exchange rate (which improves competitiveness) and negatively on the interest rate:

Long-Run Equilibrium and Neutrality

In the long run, prices are fully flexible, the economy operates at potential output, and the interest rate returns to its initial level. Money is neutral: a 1 percent permanent increase in \( m \) leads to a 1 percent increase in \( p \) and a 1 percent depreciation in \( \bar{s} \). The long-run exchange rate moves proportionally to the money supply, consistent with the purchasing power parity hypothesis.

Deriving the Overshooting Result Step-by-Step

The overshooting result emerges from combining the money market equilibrium, UIP, and regressive expectations. Start with the money market equation. In the short run, prices are fixed at \( p_0 \). Output is also fixed at its long-run level \( \bar{y} \) because the model assumes full employment. When the money supply increases by \( \Delta m \), the money market equilibrium requires the interest rate to fall to absorb the excess real money balances:

Next, substitute this interest rate change into the uncovered interest parity condition. UIP states that the domestic interest rate equals the foreign rate plus expected depreciation. With the foreign rate unchanged, a fall in the domestic rate means expected depreciation must turn into expected appreciation:

Since \( i_t \) has fallen below \( i_t^* \), the right side must be negative, meaning agents expect the domestic currency to appreciate.

Now use the regressive expectations rule to express this expected appreciation in terms of the current exchange rate gap. In continuous time, the expected change in the exchange rate equals \( -\theta (s_t – \bar{s}) \). Substituting into UIP:

Before the shock, the system was in long-run equilibrium, so \( s_t = \bar{s} \) and \( i_t = i_t^* \). After the shock, the interest differential equals \( \Delta i = -\frac{1}{\lambda} \Delta m \). The new long-run exchange rate has depreciated by \( \Delta \bar{s} = \Delta m \). Plugging the post-shock interest differential into the modified UIP equation:

Solving for the short-run exchange rate \( s_0 \):

Because \( \lambda > 0 \), \( \theta > 0 \), and \( \Delta m > 0 \), the initial exchange rate \( s_0 \) lies beyond the new long-run rate \( \bar{s}_{new} \). The exchange rate overshoots by the factor \( \frac{1}{\lambda \theta} \).

Numerical Example

Consider a calibrated model with \( \lambda = 0.5 \) (the interest semi-elasticity of money demand) and \( \theta = 0.1 \) (the speed of price adjustment). A 1 percent unanticipated monetary expansion produces a short-run depreciation of:

The currency depreciates 20 percent on impact, then gradually appreciates back to a 1 percent long-run depreciation as goods prices rise. The short-run move is twenty times the long-run adjustment. This mechanism explains why observed exchange rate volatility vastly exceeds the volatility of the underlying monetary fundamentals.

Key Assumptions and Limitations

The Dornbusch model relies on five core assumptions. First, goods prices are sticky while asset prices are flexible. Second, uncovered interest parity holds. Third, agents have rational expectations or perfect foresight. Fourth, money supply changes are unanticipated and permanent. Fifth, money is neutral in the long run.

Several important limitations challenge these assumptions. First, UIP is empirically rejected in short-run, high-frequency data. The “forward premium puzzle,” documented by Fama (1984) and many subsequent researchers, shows that high-interest-rate currencies tend to appreciate rather than depreciate, contradicting the UIP condition that underlies the overshooting mechanism. If UIP fails, the channel through which interest rate changes drive exchange rate expectations breaks down.

Second, empirical research by Eichenbaum and Evans (1995) found “delayed overshooting.” Their structural VAR analysis of US data showed that the peak exchange rate appreciation following a monetary contraction takes 24 to 39 months to materialise, rather than occurring instantaneously as the Dornbusch model predicts. The theoretical model assumes instantaneous adjustment in financial markets, but actual foreign exchange markets appear to exhibit gradual adjustment dynamics.

Third, the Meese-Rogoff (1983) finding that structural exchange rate models, including the Dornbusch framework, cannot outperform a simple random walk at short horizons remains a challenge. If the model accurately captured short-run dynamics, it should beat the random walk in out-of-sample forecasting, but it typically does not.

Fourth, the model assumes a small open economy facing exogenous foreign interest rates, limiting its direct applicability to large economies like the United States or the Eurozone, which influence global financial conditions. Fifth, the framework does not handle real shocks, such as productivity or terms-of-trade changes, and it abstracts from time-varying risk premia that may dominate exchange rate movements during periods of financial stress.

Empirical Evidence for Overshooting

The empirical literature on the Dornbusch overshooting model spans nearly five decades and has produced mixed but broadly supportive results. Dornbusch’s original 1976 paper was primarily theoretical, but the qualitative prediction that exchange rates are more volatile than fundamentals has been overwhelmingly confirmed. The BIS Triennial Survey consistently shows daily foreign exchange turnover exceeding $7 trillion, and the resulting price volatility far exceeds what changes in money supplies or price levels would justify.

Rogoff’s 2002 retrospective for the IMF acknowledged the model’s empirical difficulties but defended its qualitative insights. Eichenbaum and Evans (1995) documented delayed overshooting for the US, challenging the instantaneous adjustment prediction. However, Bjørnland (2009) revisited the question using a structural VAR with long-run restrictions for Australia, Canada, New Zealand, and Sweden. Her findings supported the Dornbusch prediction more closely: the exchange rate does overshoot on impact following a monetary shock, and the subsequent reversal aligns with the model’s qualitative trajectory. She concluded that “Dornbusch was right after all,” arguing that earlier findings of delayed overshooting were artefacts of inappropriate identification restrictions.

The Meese-Rogoff (1983) challenge remains the most formidable empirical hurdle. Their analysis showed that no structural exchange rate model, including the Dornbusch overshooting model, could outperform a naive random walk model in out-of-sample forecasting at horizons of up to one year. The random walk benchmark is difficult to beat because exchange rates incorporate all available information instantaneously, making them inherently unpredictable in the short run. Structural models add theoretical restrictions that introduce misspecification errors, which often outweigh the benefits of the economic structure they impose. Parameter instability, omitted variables, and measurement errors in money demand and output gaps further degrade forecasting performance. The Dornbusch model, while conceptually powerful, suffers from these same limitations when translated into a forecasting tool.

Bjørnland’s (2009) success in finding overshooting where others failed stems from her identification strategy. Previous studies used short-run restrictions, typically Cholesky orderings, to identify monetary policy shocks. These restrictions impose arbitrary assumptions about the timing of exchange rate responses. Bjørnland instead used long-run restrictions, following the Blanchard-Quah methodology, which identifies monetary policy shocks by assuming they have no permanent effect on output. This approach allows the exchange rate to respond freely in the short run, capturing the immediate jump predicted by Dornbusch. Her results showed that the exchange rate jumps sharply on impact and then gradually reverts, matching the theoretical impulse response function. The key lesson is that the Dornbusch model’s empirical validity depends critically on how monetary shocks are identified.

Capistrán, Chiquiar, and Hernández (2019) provided further support using Mexican data. Their structural VEC model showed that the Mexican peso overshoots following US monetary policy shocks, consistent with the Dornbusch mechanism operating in an emerging market context.

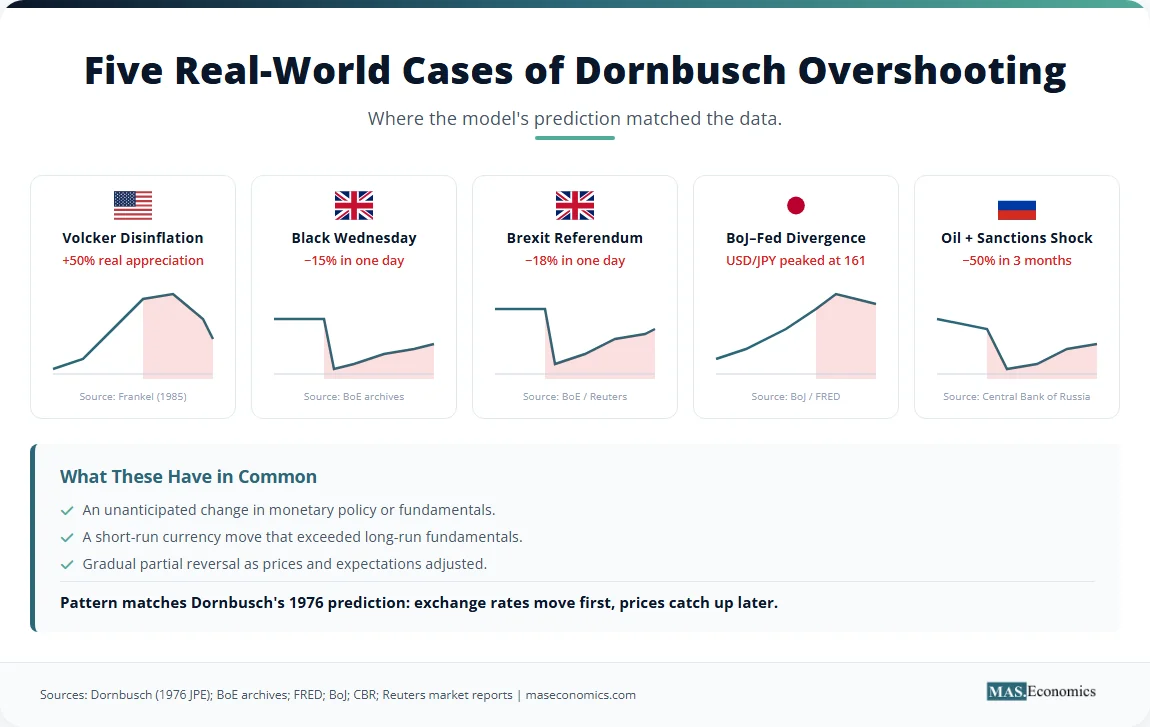

Recent monetary episodes provide informal support. The 2022–2023 Federal Reserve tightening cycle saw the DXY index appreciate 19 percent from January to October 2022 amid aggressive rate hikes. This rapid appreciation overshot most estimates of the dollar’s fundamental value based on purchasing power parity, before partially reversing in late 2023 as markets anticipated the end of the tightening cycle. Sterling’s depreciation following the June 2016 Brexit referendum, an 18 percent drop in a single day, far exceeded any reasonable reassessment of the UK’s long-run trading position, and the pound subsequently recovered some ground as the initial shock subsided.

Sources: Dornbusch (1976, JPE); Bjørnland (2009, JIE) for Australia 1985–2008.

| Episode | Trigger | Initial Overshoot | Long-Run Move | Time to Adjust | Source |

|---|---|---|---|---|---|

| US Dollar 1980–1985 | Volcker tightening | +50% real appreciation | +20% | 5 years | Frankel (1985) |

| Sterling Black Wed. 1992 | ERM exit | -15% (1 day) | -7% | 18 months | BoE archives |

| GBP post-Brexit 2016 | Referendum result | -18% (1 day) | -10% | 2 years | BoE / FT |

| USD/JPY 2022–2024 | Fed-BoJ divergence | +50% peak | ~+15% | Pending | BoJ / Reuters |

| RUB 2014 | Oil shock + sanctions | -50% (3 months) | -25% | 3 years | CBR |

|

|||||

How the Overshooting Model Matters

The Dornbusch overshooting model is more than a clever theoretical exercise; it is the conceptual foundation for understanding how monetary policy transmits to the open economy. Its implications extend from academic theory to the daily operations of central banks and the strategies of currency traders.

First, the model provided the foundation for modern open-economy macroeconomics. Obstfeld and Rogoff’s 1995 “Exchange Rate Dynamics Redux” paper generalised Dornbusch’s insight into a fully microfounded New Open Economy Macroeconomics (NOEM) framework. Their model preserved the overshooting mechanism but grounded it in explicit consumer optimisation, imperfect competition, and nominal rigidities. Every subsequent generation of open-economy model, from the New Keynesian open-economy frameworks used by central banks to the DSGE models employed by the IMF, traces its intellectual lineage to Dornbusch’s 1976 insight.

Second, the model explains the exchange rate disconnect puzzle, the empirical observation that exchange rates are far more volatile than the macroeconomic fundamentals that should theoretically drive them. If the burden of short-run adjustment falls disproportionately on the exchange rate because goods prices are slow to move, then even small changes in monetary policy can generate large, temporary swings in currency values. This explanation resolved a deep inconsistency between theory and data that had plagued international economics since the collapse of the Bretton Woods system.

Third, the model has important implications for the central bank’s communications strategy. Because expected future monetary policy moves the exchange rate today through the UIP condition, central banks practice careful forward guidance to manage the exchange rate channel of monetary transmission. When the Federal Reserve signals that rates will remain higher for longer, the dollar appreciates immediately, far more than the current interest rate differential alone would justify. The Dornbusch framework shows that this market reaction is rational: the exchange rate is adjusting not just to today’s policy but to the entire expected future path of policy.

Fourth, the overshooting framework explains the dynamics of emerging market crises with striking precision. When investors suddenly withdraw capital from an emerging market, the currency depreciates sharply, often by 30 to 50 percent within months. The 1997 Thai baht crisis illustrates this mechanism step-by-step. Before the crisis, Thailand maintained a de facto peg to the US dollar while allowing substantial capital mobility. When export growth slowed and the current account deficit widened, speculators attacked the peg. The Bank of Thailand exhausted its foreign reserves defending the baht and was forced to float the currency in July 1997. The baht depreciated from 25 to 56 per dollar within six months, a move that far exceeded any reasonable reassessment of Thailand’s long-run purchasing power parity. The Dornbusch model explains why: with the peg abandoned and capital fleeing, the burden of adjustment fell entirely on the exchange rate. Goods prices, especially non-tradable services, adjusted slowly, so the real exchange rate overshot its long-run equilibrium. The resulting real depreciation improved competitiveness, provided the Marshall-Lerner condition holds, but the adjustment was often preceded by a J-curve effect where the trade balance worsens before improving. The 2018 Turkish lira crisis followed a similar pattern: the lira lost 40 percent of its value against the dollar in a matter of months, far overshooting the long-run fundamental adjustment, before partially recovering as the initial panic subsided and prices adjusted. Balance of payments disequilibrium forces the exchange rate to absorb the full shock, producing overshooting.

Fifth, the model illuminates the dollar’s strength during the 2022–2025 Fed tightening and quantitative easing cycles. As the Federal Reserve raised rates aggressively to combat inflation, the DXY index surged. The dollar appreciated far beyond what changes in relative price levels would suggest, consistent with the Dornbusch prediction that interest rate differentials drive short-run exchange rate overshooting. As markets began to anticipate rate cuts in late 2023 and 2024, the dollar partially reversed, exactly as the model’s dynamic adjustment path predicts. The divergence between the Fed and other central banks amplified this mechanism.

Sixth, Japan’s yen weakness in 2022–2024 provides a textbook case. The Bank of Japan maintained ultra-easy monetary policy while the Federal Reserve tightened aggressively. The resulting interest rate differential caused the yen to depreciate by over 50 percent against the dollar, peaking at 161 yen per dollar in July 2024. This depreciation far exceeded any reasonable estimate of the long-run fundamental value, and the yen subsequently began to recover as markets anticipated an eventual normalisation of BoJ policy. The episode perfectly illustrates the Dornbusch mechanism: the currency overshoots because the interest differential must be compensated by expected future appreciation, which requires the currency to be undervalued today.

Seventh, the 2016 Brexit vote produced a classic overshooting event. Sterling fell 18 percent on the morning after the referendum, far exceeding any fundamental reassessment of the UK’s long-run economic position. Over the following two years, as the initial panic subsided and goods prices adjusted, the pound partially recovered. The Dornbusch model explains this pattern: the exchange rate absorbed the full impact of the shock instantly, while goods markets adjusted only gradually.

Eighth, carry trade economics rest on Dornbusch’s insight that interest rate differentials drive temporary overshoots. Carry traders borrow in low-interest-rate currencies, such as the Japanese yen, and invest in high-interest-rate currencies, such as the Australian dollar, profiting from the interest differential as long as the high-yield currency does not depreciate enough to offset the carry. The Dornbusch model provides the theoretical basis for why this strategy works in normal times. Under UIP, a high interest rate should be offset by expected depreciation, leaving no net return. Empirically, however, high-interest-rate currencies tend to appreciate or remain stable in the short run, violating UIP and generating positive carry trade returns. This “forward premium puzzle” is a direct empirical consequence of the overshooting mechanism: when a central bank raises rates, the currency appreciates beyond its long-run value, and the subsequent slow appreciation back toward equilibrium offsets the interest differential less than UIP predicts. Carry traders capture this wedge. The Dornbusch framework shows that this profit opportunity arises precisely because goods prices adjust slowly while financial markets adjust instantly.

Ninth, policy transmission in small open economies depends critically on the Dornbusch channel. The Bank of Canada, the Reserve Bank of Australia, and the Reserve Bank of New Zealand explicitly track the exchange rate channel in their monetary policy models. When these central banks cut rates, they expect the currency to depreciate, stimulating exports and closing the output gap. The magnitude and timing of this response are directly governed by the overshooting logic.

Tenth, emerging markets use capital controls and macroprudential policies to dampen Dornbusch-style overshooting after external shocks. When the Federal Reserve tightens policy, emerging market currencies face depreciation pressure that often exceeds fundamental values. Brazil’s use of the Imposto sobre Operações Financeiras (IOF) tax provides a specific example. In 2010 and again in 2015, Brazil imposed taxes on foreign exchange derivatives and fixed-income investments to slow capital outflows and reduce the volatility of the real. The IOF tax effectively introduced a transaction cost that widened the risk premium in the UIP equation, breaking the tight link between interest rate differentials and exchange rate movements. By increasing the friction on capital flows, Brazil prevented the exchange rate from bearing the full burden of short-run adjustment, reducing the magnitude of overshooting. This policy response is a direct application of the overshooting framework, recognising that the friction between fast financial markets and slow goods markets creates destructive volatility.

MASEconomics Explains

4 economic concepts behind the Dornbusch model

Conclusion

Dornbusch overshooting model theory explains why floating exchange rates exhibit volatility that vastly exceeds the volatility of underlying fundamentals, resting on the asymmetry between flexible asset markets and sticky goods markets. The model remains the workhorse framework for thinking about monetary policy spillovers, central bank communication, and exchange rate dynamics. While it faces ongoing empirical challenges around the timing of overshooting and the failure of uncovered interest parity in short-run data, its qualitative prediction that exchange rates move first and adjust back as prices catch up has been confirmed by post-1973 data across advanced and emerging economies. From the Volcker dollar to Brexit sterling to the yen’s roller coaster, the Dornbusch mechanism continues to provide the key lens for understanding why exchange rates move too far, too fast.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.