In November 1961, the American Economic Review published a six-page paper by Robert Mundell titled “A Theory of Optimum Currency Areas”. It became the foundation of every subsequent debate over the euro, dollarisation, and the costs of monetary integration. Mundell received the 1999 Nobel Prize in Economics partly for this work, the same year the euro was introduced.

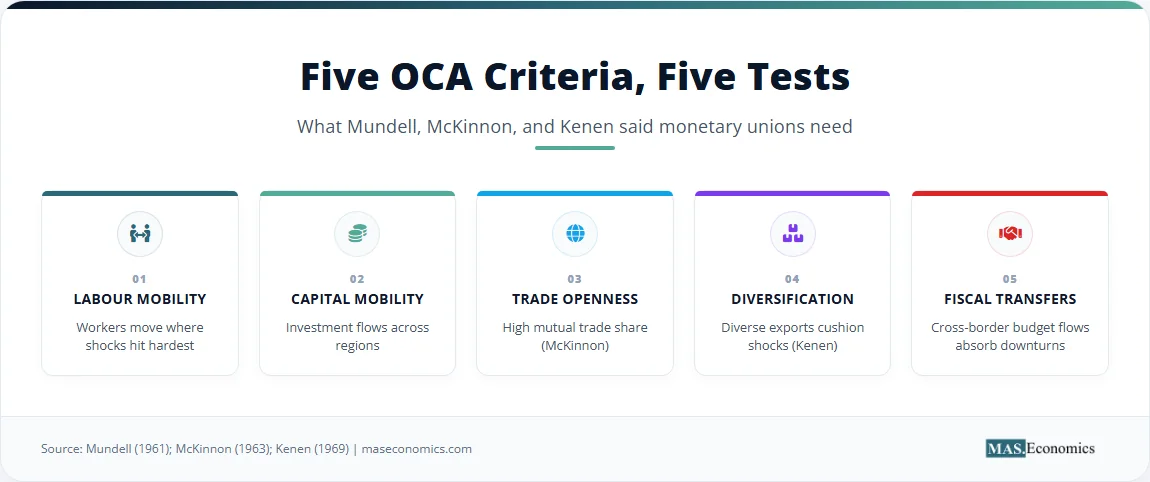

Optimum Currency Area Theory sets out the conditions under which a group of countries gains more from sharing a common currency than it loses by giving up an independent exchange rate. Five criteria (labour mobility, capital mobility, trade openness, export diversification, and cross-border fiscal transfers) determine whether the trade benefits of a single currency outweigh the cost of losing exchange rate adjustment to asymmetric shocks.

What follows derives the OCA loss function, presents the five criteria from Mundell, McKinnon, and Kenen, surveys the empirical record on the euro area, and shows how the framework explains the 2010–2012 European debt crisis and the survival of the CFA franc zone.

What Optimum Currency Area Theory Means

Before 1961, the economics of exchange rates was dominated by the debate between fixed and flexible regimes. The post-war Bretton Woods system relied on fixed exchange rates, with occasional devaluations when balance-of-payments pressures became unsustainable. Advocates of fixed rates pointed to the stability they provided for trade and investment. Advocates of flexible rates argued that they allowed countries to adjust to economic shocks without suffering mass unemployment. The debate treated the national economy as the natural unit of analysis. The question was whether a country should fix its currency or let it float.

Mundell shifted the terms of the debate entirely. He asked not whether fixed or flexible rates were better in the abstract, but what geographic area should share a common currency. The question was spatial: what are the optimal boundaries of a currency zone? It implied that national borders and currency areas need not coincide. A region spanning parts of several countries might be an optimal currency area, while a single country containing very different regional economies might not.

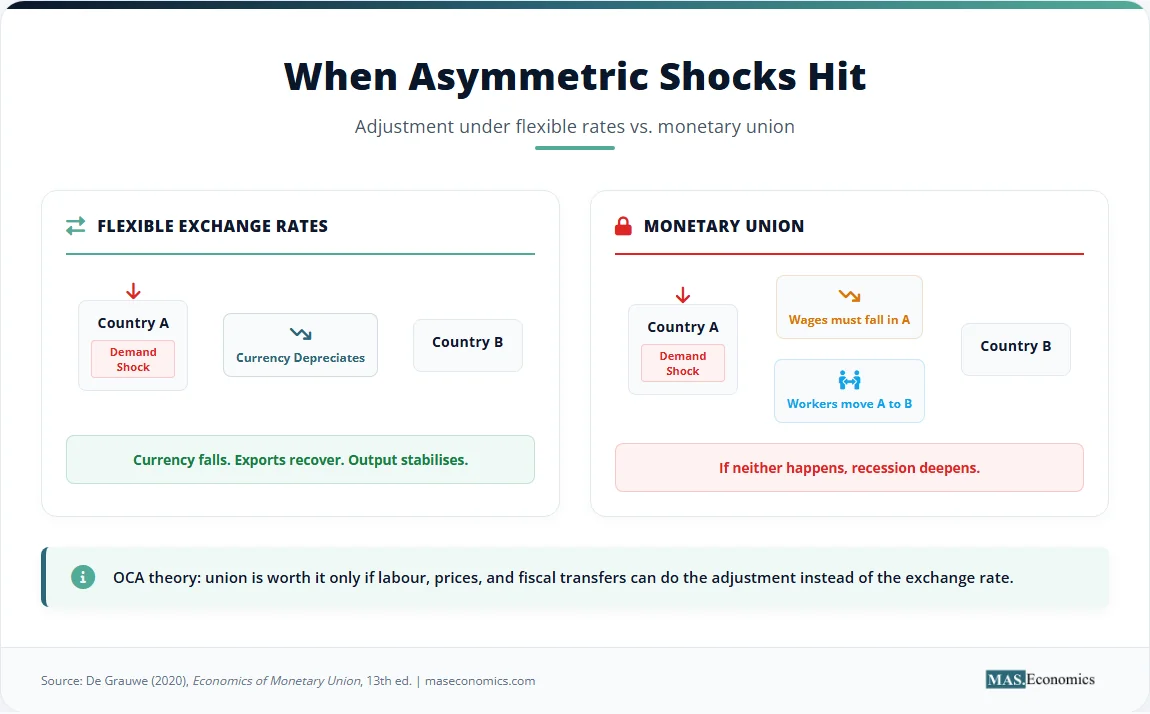

Mundell’s insight was that the value of a common currency depends on the economic characteristics of the regions adopting it. A common currency eliminates transaction costs and exchange-rate uncertainty, which boosts trade and investment. These are the microeconomic benefits. It also eliminates the exchange rate as a tool for macroeconomic adjustment. If two regions share a currency, and demand shifts from region A to region B, region A cannot devalue its currency to regain competitiveness. It must adjust through internal devaluation (falling wages and prices) or through factor reallocation (workers and capital moving from A to B).

The trade-off is clear. If the regions face similar economic shocks, they need the same monetary policy, and the loss of the exchange rate is irrelevant. If they face different shocks, or asymmetric shocks, the loss of the exchange rate is costly. Mundell identified labour mobility as the key factor tipping the balance. If workers move freely from the declining region to the expanding region, unemployment does not rise in the declining region, and the adjustment cost is minimal. A region with high labour mobility can safely share a currency, even if it faces asymmetric shocks. A region with low labour mobility cannot.

Subsequent economists added more criteria. Ronald McKinnon argued in his 1963 paper “Optimum Currency Areas” that open economies (those with a high ratio of trade to GDP) benefit more from a common currency because the transaction-cost savings are larger. Peter Kenen argued in his 1969 paper “The Theory of Optimum Currency Areas: An Eclectic View” that diversified economies are better candidates for monetary union because a shock to one industry is offset by stability in others, reducing the overall asymmetry of shocks. Kenen also introduced the idea that cross-border fiscal transfers can substitute for labour mobility, stabilising a region hit by a downturn without requiring its workers to leave. The combination of these criteria (labour mobility, capital mobility, trade openness, product diversification, and fiscal transfers) defines Optimum Currency Area Theory.

Optimum Currency Area Theory in Equations

The OCA framework is built around the trade-off between the microeconomic gains from a common currency and the macroeconomic cost of losing an independent monetary policy and exchange rate. For two regions A and B contemplating monetary union, define an asymmetric demand shock as a shift in relative demand from A’s goods to B’s goods. Under flexible exchange rates, A’s currency depreciates against B’s, restoring competitiveness. Under a common currency, this adjustment must occur through internal devaluation or factor reallocation.

Denote the welfare loss from an asymmetric shock under monetary union as \( L(\sigma, \mu, \phi, \tau) \), where \( \sigma \) is the standard deviation of asymmetric shocks, \( \mu \) is labour mobility, \( \phi \) is wage-price flexibility, and \( \tau \) is the size of cross-border fiscal transfers. The standard OCA loss function is decreasing in \( \mu \), \( \phi \), and \( \tau \), and increasing in \( \sigma \). A simplified illustrative form following De Grauwe (2020) is:

This equation captures the central intuition of the theory. The numerator contains the variance of the shocks, \( \sigma^2 \). When asymmetric shocks are large, the welfare loss from sharing a currency is also large, because the single monetary policy cannot address the divergent needs of the two regions. The denominator contains the sum of the alternative adjustment mechanisms: labour mobility, wage flexibility, and fiscal transfers. When these mechanisms are strong, the loss from giving up the exchange rate is small, because the economy has other ways to absorb the shock. The loss function formalises the idea that a monetary union is costly only when shocks are asymmetric and adjustment mechanisms are weak.

The benefit of monetary union, mainly transaction-cost saving and the removal of exchange-rate uncertainty, is increasing in trade integration \( \theta \) between the two regions:

Here, \( \beta \) is the marginal benefit of integration. A monetary union is welfare-improving for A and B when the benefits exceed the losses:

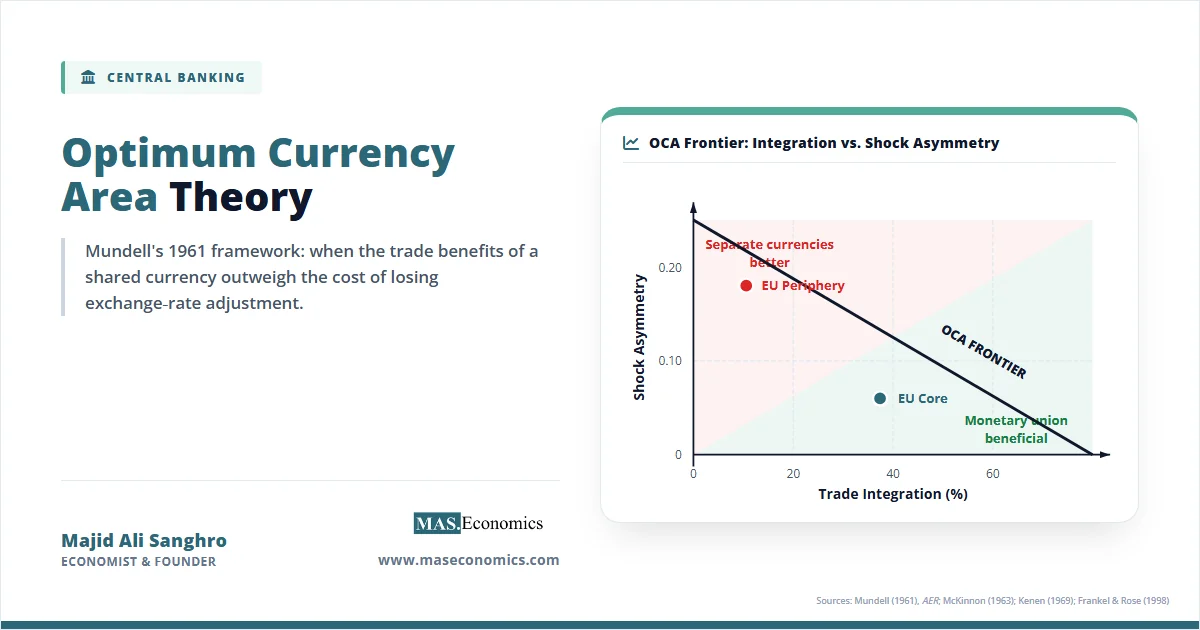

This inequality produces the OCA frontier in trade-integration and asymmetric-shock-variance space. Above the frontier, the union is welfare-improving. Below the frontier, separate currencies are better. Frankel and Rose (1998) added the endogeneity insight: \( \theta \) and \( \sigma \) are not independent. Joining a currency union raises trade integration and may itself reduce shock asymmetry, shifting countries up and to the left of the frontier ex post.

Consider a worked example. Suppose two regions have \( \mu + \phi + \tau = 0.5 \), \( \sigma = 0.1 \), and \( \beta = 0.4 \). The loss from monetary union is \( L = (0.1)^2 / 2(0.5) = 0.01 \). Monetary union is welfare-improving when trade integration \( \theta > 0.025 \). For two regions with low labour mobility and fiscal transfers, where \( \mu + \phi + \tau = 0.1 \), facing the same shocks, the threshold rises to \( \theta > 0.125 \). The required level of trade integration is five times higher. This arithmetic shows why the OCA criteria matter. Without adjustment mechanisms, a monetary union requires an extremely high level of trade integration to be viable.

| # | Criterion | Source Paper | What It Measures | Eurozone Score (1999) |

|---|---|---|---|---|

| 1 | Labour mobility | Mundell (1961) | Cross-border migration as share of population | Low (0.3% vs. US 2.4%) |

| 2 | Capital mobility | Mundell (1961) | Cross-border investment flows | High |

| 3 | Trade openness | McKinnon (1963) | Trade / GDP | High (>30%) |

| 4 | Product diversification | Kenen (1969) | Variety of exports | High |

| 5 | Fiscal transfers | Kenen (1969) | Cross-border fiscal flows / GDP | Low (≈ 1% EU budget) |

|

||||

Key Assumptions and Limitations

Optimum Currency Area Theory rests on five central assumptions. First, it assumes that exchange-rate adjustment is the main alternative to OCA membership. If a region keeps its own currency, it can devalue to absorb an asymmetric shock. This assumption downplays the possibility that countries with flexible rates might avoid devaluation due to fear of inflation or capital flight, rendering the exchange-rate tool ineffective in practice.

Second, the model assumes that labour and capital mobility are exogenous. They are treated as fixed parameters that determine the adjustment capacity of the union. In reality, mobility is itself shaped by institutions, language barriers, and the legal environment. Monetary union might even alter mobility over time by changing migration incentives.

Third, the framework assumes wage-price flexibility is exogenous. The parameter \( \phi \) is treated as a given. In practice, wage-setting institutions differ radically across countries. Southern European economies historically had more rigid wage-setting mechanisms than Northern European economies, making internal devaluation much harder.

Fourth, the theory assumes that fiscal transfers exist or do not exist by political fiat. The parameter \( \tau \) is set outside the model. The OCA framework does not explain how a fiscal union emerges, what political conditions allow it, or why a union might fail to create one. This omission is particularly glaring in the European case, where the absence of a central fiscal capacity was a deliberate political choice, not an economic constraint.

Fifth, the model assumes that shocks are either symmetric or asymmetric and that the distribution of these shocks is known. Policymakers can observe \( \sigma \) and decide accordingly. In reality, shock variance changes over time. Financial crises, pandemics, and geopolitical shocks alter the correlation of business cycles in unpredictable ways.

The most important limitation of the OCA framework is that it is static. It evaluates the costs and benefits of monetary union at a point in time, given existing economic structures. It ignores the political economy of monetary union, the role of common safe-asset provision, and the lender-of-last-resort function. The Eurozone discovered this limitation painfully in 2010–2012. When sovereign-debt crises hit Greece, Ireland, and Portugal, the absence of a central lender of last resort forced the European Central Bank to improvise.

A deeper limitation involves the long-term dynamics of economic structure. Paul Krugman argued in his 1993 paper “Lessons of Massachusetts for EMU” that monetary union might increase asymmetric shocks if it leads to regional specialisation. The logic is straightforward. If a common currency encourages regions to specialise in their comparative-advantage industries, the industrial structure becomes more concentrated. Specialised regions are more vulnerable to industry-specific shocks. This is the opposite of the Frankel-Rose endogeneity claim. Frankel and Rose argued that joining a currency union increases trade integration, which raises business-cycle correlation and reduces shock asymmetry. Krugman argued that lower trade barriers and a common currency encourage regional specialisation based on comparative advantage, which reduces diversification and increases shock asymmetry. The United States is highly integrated but also highly diversified within regions. The Eurozone, however, might see core manufacturing in Germany and the Low Countries diverge from periphery tourism and agriculture in Greece and Portugal. The static OCA model cannot resolve which force dominates. The actual outcome depends on whether trade creation leads to intra-industry trade, which favours correlation, or inter-industry trade, which favours specialisation and divergence.

Evidence for Optimum Currency Area Theory

Empirical testing of Optimum Currency Area Theory has focused on three questions: whether the OCA criteria are endogenous, whether geographic regions cluster into core and periphery, and whether monetary unions actually reduce shock asymmetry over time.

Jeffrey Frankel and Andrew Rose provided the most influential empirical test in their 1998 Economic Journal paper, “The Endogeneity of the Optimum Currency Area Criteria”. They examined bilateral trade and business-cycle correlations across OECD country pairs from 1959 to 1993. Frankel and Rose found a strong positive relationship. Countries that trade more with each other have more highly correlated business cycles. This result is critical because it suggests that OCA criteria can be self-fulfilling. Two countries might not meet the OCA criteria before forming a monetary union, but the act of joining raises trade integration, which raises cycle correlation, which reduces shock asymmetry. The countries endogenously become an optimum currency area after they join. The Frankel-Rose result provided intellectual cover for the creation of the euro, though later critics noted that trade creation was only part of the story, and financial integration might amplify asymmetric shocks.

Tamim Bayoumi and Barry Eichengreen applied the OCA framework directly to Europe in their 1993 study, “Shocking Aspects of European Monetary Unification”. They used VAR decompositions to identify supply and demand shocks across European countries from 1960 to 1988. Bayoumi and Eichengreen found a striking geographic clustering. An EU “core”, consisting of Germany, France, Belgium, the Netherlands, and Denmark, faced highly symmetric shocks. These countries had similar industrial structures, heavily weighted toward advanced manufacturing, and their business cycles moved in tandem. A EU “periphery”, consisting of Italy, Spain, Portugal, Greece, and Ireland, faced very different shocks. The periphery economies were more reliant on agriculture, tourism, and lower-value manufacturing. The correlation of shocks within the core was high. The correlation between the core and the periphery was low. This finding foreshadowed the 2010–2012 crisis. When asymmetric shocks hit the periphery, the common monetary policy was too tight for them, exacerbating the downturn.

Georg Beck, Kirstin Hubrich, and Massimiliano Marcellino examined the post-creation reality of the euro in their 2009 Economic Policy paper, “On the Importance of Sectoral and Regional Shocks for Price-Setting”. They measured regional inflation differentials within the euro area and found persistent divergence. Some countries, like Greece and Spain, consistently experienced higher inflation than the euro-area average. Others, like Germany, consistently experienced lower inflation. Persistent inflation differentials mean that the real exchange rate, adjusted for purchasing power parity, diverges within the monetary union. High-inflation countries lose competitiveness year after year, building up internal imbalances that eventually require a sharp correction. The Beck et al. finding suggested that the euro area was further from being an OCA than the founders believed.

Pairs above the OCA frontier (top-left) need separate currencies; pairs below the frontier (bottom-right) gain from monetary union. The Eurozone periphery sat above the frontier in 1999 and the 2010–2012 crisis revealed the cost. Source: Bayoumi & Eichengreen (1993); Frankel & Rose (1998); MASEconomics calculation.

How Optimum Currency Area Theory Matters

Optimum Currency Area Theory is the standard framework for evaluating monetary unions because it isolates the central trade-off: a common currency pays off when its trade benefits exceed the cost of losing exchange-rate adjustment. Three applications show how it still applies.

The creation of the euro is the most important application of the OCA framework. When the Maastricht Treaty was signed in 1992, many economists warned that Europe did not meet the OCA criteria. Labour mobility across European countries was a fraction of US interstate migration. Language barriers, cultural differences, and pension-portability rules prevented workers from moving from high-unemployment countries to low-unemployment countries. The EU budget was around one percent of GDP, compared to roughly twenty percent for US federal transfers, leaving no mechanism for cross-border fiscal stabilisation. The European debt crisis of 2010–2012 was a textbook OCA failure. Asymmetric shocks hit the periphery. Housing markets collapsed in Spain and Ireland. A sovereign-debt crisis engulfed Greece. The common monetary policy, set by the European Central Bank for the entire euro area, was too loose for the core during the boom and too tight for the periphery during the bust. Without the ability to devalue their currencies, the peripheral countries were forced into internal devaluation. Wages and prices had to fall to restore competitiveness. The social cost was enormous. Greek real GDP fell by roughly 25 percent between 2008 and 2016. Spanish unemployment peaked at 26.9 percent in early 2013, and youth unemployment exceeded 55 percent. The European Central Bank raised interest rates in 2011 due to inflation fears in the core, exactly the wrong policy for the collapsing periphery. It took until July 2012, when ECB President Mario Draghi promised to do “whatever it takes” to preserve the euro, for the central bank to effectively act as the lender of last resort the OCA framework had ignored. The crisis proved that the OCA criteria were not merely academic. Ignoring them imposed massive economic suffering. The crisis also exposed the importance of the lender-of-last-resort function, an issue the static OCA framework largely ignored, but which the central bank independence literature had long emphasised.

Dollarisation and currency boards provide another test of the OCA framework. Ecuador adopted the US dollar in 2000 after hyperinflation destroyed the sucre. El Salvador followed in 2001. Panama has used the dollar for over a century. These countries have very low labour mobility with the United States, face very different economic shocks, and receive no fiscal transfers from Washington. By strict OCA criteria, they are poor candidates for monetary union with the US. They adopted the dollar anyway, betting that the monetary credibility and lower inflation the dollar brings outweigh the cost of losing exchange-rate adjustment. The trade-off is real. Ecuador suffered a deep recession when oil prices collapsed in 2014–2016, because it could not devalue its currency to cushion the shock. The government was forced to cut public spending sharply, leading to protests and political instability. The alternative (a domestically issued currency managed by institutions with a history of inflation) was arguably worse. An IMF working paper on full dollarisation documents the credibility-cost trade-off in detail. Argentina’s currency board, which pegged the peso one-to-one to the dollar from 1991 to 2001, collapsed for different reasons. Like Ecuador, Argentina faced a massive asymmetric shock when the Brazilian devaluation of 1999 made Argentine exports uncompetitive. Unlike Ecuador, Argentina’s internal devaluation was politically impossible. Wage rigidities, powerful trade unions, and a fiscal deficit prevented the necessary adjustment. Without fiscal transfers from the currency anchor and without the ability to devalue, the country suffered four years of grinding recession. Unemployment rose to nearly 20 percent. The result was a sovereign default, a violent economic collapse, and the abandonment of the peg in 2001. The Argentine case is the classic illustration of the OCA cost of losing the exchange rate when alternative adjustment mechanisms are absent. The Mundell trilemma and exchange rate dynamics models explain why the peg failed to survive the shock.

Africa’s CFA franc zone is a surprising counterpoint. The zone has survived for over seventy-five years, despite low labour mobility and great shock asymmetry among its member states. The CFA franc is pegged to the euro, and France guarantees the convertibility of the currency. This guarantee functions as a fiscal-transfer mechanism, exactly the kind of institution Kenen identified as necessary for a monetary union. When a member state faces a balance-of-payments crisis, France provides financial support, smoothing the adjustment. The CFA franc zone survives not because it meets the labour-mobility or wage-flexibility criteria, but because it satisfies the fiscal-transfer criterion. The fiscal-monetary coordination provided by the French treasury substitutes for the missing adjustment mechanisms. The OCA framework explains the survival of the CFA zone, even as it predicts the difficulties of the euro area.

The theory also informs the modern debate over policy assignments in the Mundell-Fleming model and the IS-LM framework. In a world of high capital mobility, fixed exchange rates require monetary policy to target the exchange rate, leaving fiscal policy to manage domestic demand. In a monetary union, the exchange rate is irrevocably fixed, and monetary policy is set centrally. The OCA framework shows that this arrangement works only if the other adjustment mechanisms (labour mobility and fiscal transfers) are available to the member states. The framework is a diagnostic tool. It shows policymakers where the vulnerabilities of a monetary union lie.

MASEconomics Explains

4 economic concepts behind Optimum Currency Area Theory

Conclusion

Optimum Currency Area Theory is the standard framework for evaluating monetary unions: a common currency pays off when its trade benefits exceed the cost of losing exchange-rate adjustment to asymmetric shocks. The five criteria (labour mobility, capital mobility, trade openness, product diversification, and fiscal transfers) determine where that boundary lies. The Eurozone failed two of the most important criteria, limited labour mobility and minimal fiscal transfers, and the 2010–2012 debt crisis exposed the cost of that failure. The CFA franc zone survives because French fiscal guarantees substitute for the missing adjustment mechanisms.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.