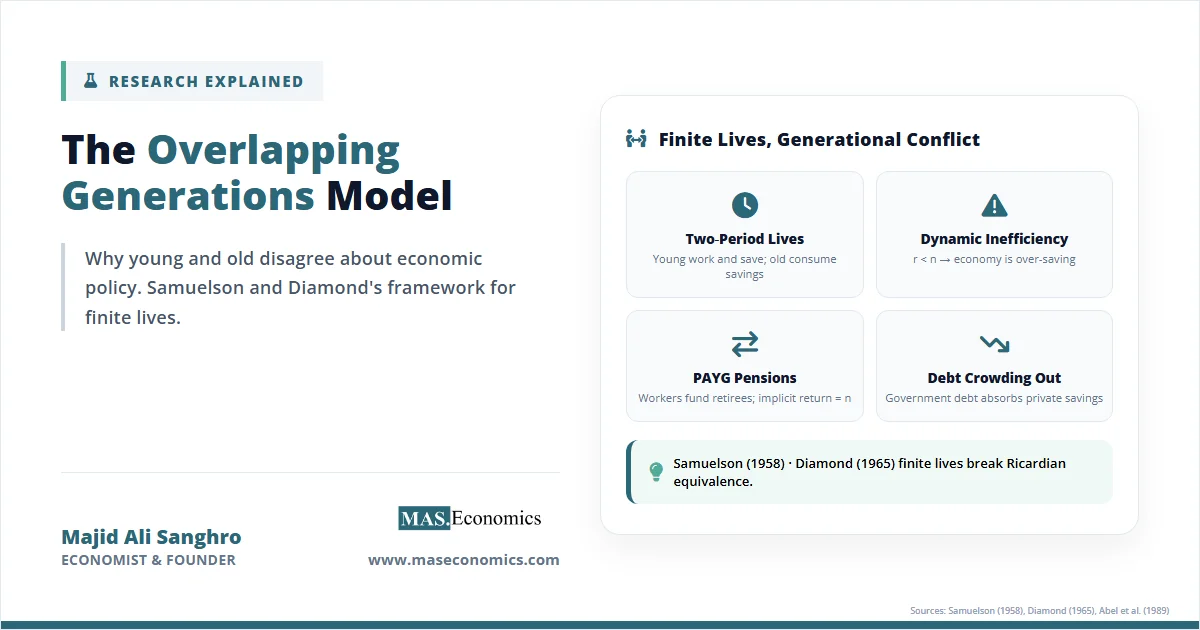

In 2024, a 28-year-old software engineer in Toronto pays roughly 32% of her gross salary into income tax, federal contributions, and provincial pension premiums. Her 72-year-old grandfather collects Canada Pension Plan benefits, Old Age Security, and a Guaranteed Income Supplement top-up. He votes consistently for parties promising indexed pension increases. She votes for parties promising student debt relief and a wealth tax to fund university expansion. Neither is irrational. They are simply at different points in the life cycle, and the overlapping generations model economics explains why their interests diverge so sharply.

The model was pioneered by Paul Samuelson in 1958 and given its modern form by Peter Diamond in 1965. It rebuilt macroeconomics on a simple insight: people do not live forever. They are born, work, save, retire, and die. Generations overlap but do not last. That finite horizon changes everything about how economies accumulate capital, how government debt circulates, and why political coalitions form along age lines.

Three policy debates rest squarely on this framework. Pay-as-you-go pension systems work as transfers from working-age cohorts to retired ones. Government debt issued today shifts consumption from future taxpayers to current bondholders. Climate mitigation costs fall on people alive now to benefit those born later. None of these can be analysed without a model where generations are distinct economic actors with conflicting interests.

The Logic of Overlapping Generations

The simplest overlapping generations model has agents living for exactly two periods. In the first period, an individual works, earns a wage, consumes part of it, and saves the rest. In the second period, the same individual is retired, supplies no labour, and lives off accumulated savings plus interest. At every point in time, two cohorts coexist: the young who are working and the old who are spending down their wealth.

This setup looks innocuous. It is not. The Ramsey-Cass-Koopmans model that dominates graduate macroeconomics assumes a representative household with an infinite planning horizon. That assumption forces capital accumulation toward a unique steady state defined by the modified golden rule, where the marginal product of capital equals the discount rate plus the growth rate of population. Ricardian equivalence holds: a tax cut financed by debt has no effect on consumption because households know future taxes will rise to repay it. There is no role for unfunded social security and no possibility of over-saving.

The OLG framework breaks all three results. Because each cohort lives only two periods, savings decisions are made by individuals who will not be alive to pay future taxes. A debt-financed tax cut today benefits the current young, who consume more, and burdens the unborn, who must service the debt. Generational accounting matters in a way it never can in models with immortal agents. Capital can be over-accumulated relative to the golden rule, producing dynamic inefficiency where everyone could be made better off by consuming more and saving less. Pay-as-you-go pensions, which look like a Ponzi scheme in the Ramsey world, can be Pareto-improving in an OLG economy stuck in dynamic inefficiency.

Samuelson’s original 1958 paper used a pure endowment economy with no production. Diamond’s 1965 extension added a neoclassical production function and capital accumulation, producing the model that bears his name and sits at the centre of public finance and growth theory.

OLG Model in Equations

The Diamond version starts with a representative young agent born at time \( t \) who maximises lifetime utility over two periods of consumption. The objective function is:

where \( c_{1,t} \) is consumption when young, \( c_{2,t+1} \) is consumption when old, and \( \beta \in (0,1) \) is the discount factor. The young agent earns a competitive wage \( w_t \), saves an amount \( s_t \), and consumes the rest. When old, the agent receives the savings plus interest at the rate \( r_{t+1} \).

The two budget constraints are:

The first-order condition gives the standard Euler equation:

This pins down the savings function \( s_t = s(w_t, r_{t+1}) \). With log utility, savings become independent of the interest rate and equal a constant fraction of the wage: \( s_t = \frac{\beta}{1+\beta} w_t \).

On the production side, firms operate a constant-returns technology \( Y_t = F(K_t, L_t) \). In intensive form with \( k_t = K_t / L_t \), the wage and rental rate are:

where \( \delta \) is the depreciation rate. Population grows at rate \( n \), so \( L_{t+1} = (1+n) L_t \). The crucial market-clearing condition is that the capital stock used in production tomorrow is exactly the savings of the young today. Aggregate savings equal \( s(w_t, r_{t+1}) L_t \), and these become tomorrow’s capital:

Dividing by \( L_{t+1} \) gives the capital accumulation equation in per-worker terms:

The steady state \( k^* \) satisfies \( k^* (1+n) = s(w(k^*), r(k^*)) \). This expression has no closed form for general utility functions, and crucially, it can produce multiple equilibria, instability, or oscillations. The OLG model is mathematically richer than Ramsey precisely because the dynamics depend on the wage-saving-capital chain.

The golden rule level of capital, \( k_{GR} \), is defined as the capital stock that maximises steady-state consumption per worker. It satisfies:

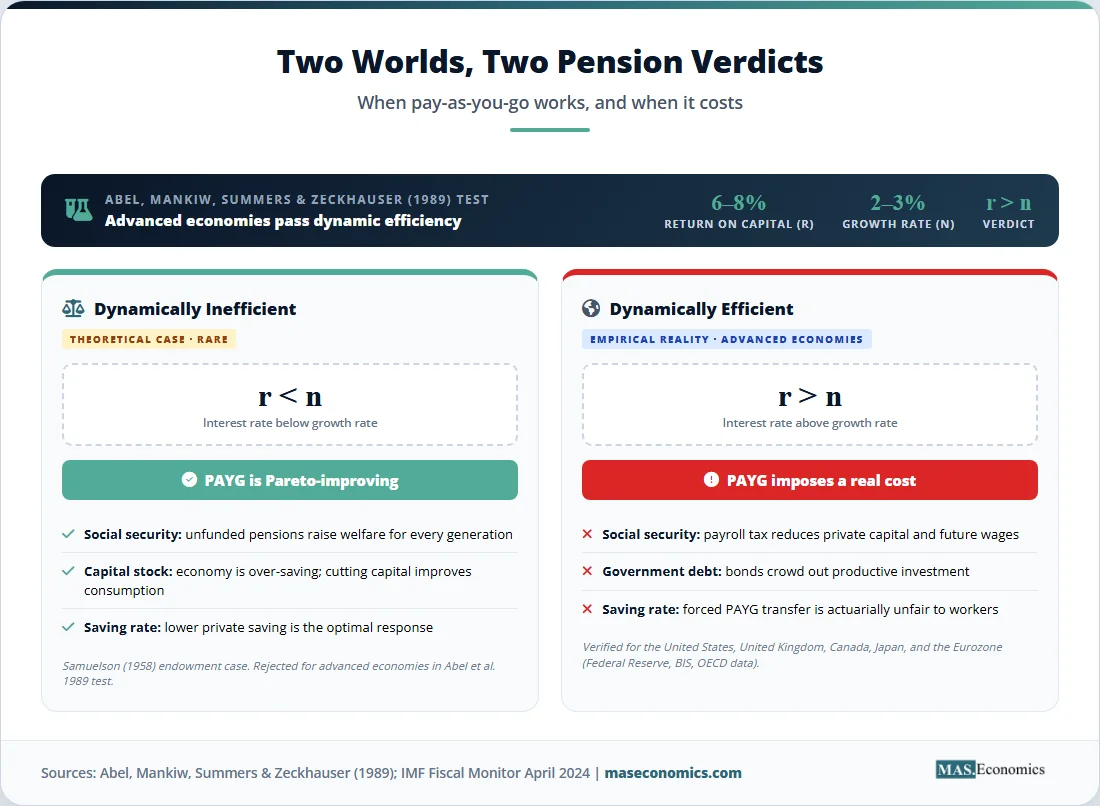

Equivalently, \( r_{GR} = n \). The economy is dynamically inefficient when \( k^* > k_{GR} \), which corresponds to:

When the steady-state interest rate is below the population growth rate, agents are saving too much. Reducing capital and consuming the difference would raise consumption for every generation, present and future. This Pareto improvement is impossible in the Ramsey model but standard in OLG.

| Symbol | Meaning | Typical Value or Sign |

|---|---|---|

| \( c_{1,t} \) | Consumption when young in period t | Positive |

| \( c_{2,t+1} \) | Consumption when old in period t+1 | Positive |

| \( w_t \) | Real wage in period t | Equals marginal product of labour |

| \( r_{t+1} \) | Real interest rate in period t+1 | Equals marginal product of capital minus depreciation |

| \( s_t \) | Savings of young agent | \( w_t – c_{1,t} \) |

| \( \beta \) | Subjective discount factor | 0.95 to 0.99 per year, lower across two-period blocks |

| \( n \) | Population growth rate | 0.5% to 2% in advanced economies |

| \( \delta \) | Capital depreciation rate | 4% to 8% per year |

| \( k^* \) | Steady-state capital per worker | Determined by savings and growth |

| \( k_{GR} \) | Golden rule capital per worker | Maximises steady-state consumption |

| ||

Adding government debt or pay-as-you-go pensions modifies the savings equation. With a pension contribution \( \tau \) paid by the young and a benefit \( b_{t+1} = (1+n) \tau \) received when old, the budget constraints become \( c_{1,t} = w_t – \tau – s_t \) and \( c_{2,t+1} = (1+r_{t+1}) s_t + (1+n) \tau \). The implicit return on the pension contribution is \( n \). When \( n > r \), pay-as-you-go beats private saving, and the pension makes every generation better off.

Key Assumptions and Their Limits

The Diamond OLG model rests on assumptions that make the algebra tractable but limit realism. Agents live for two periods, which compresses an entire 60-year working life and 25-year retirement into two snapshots. There are no bequests, so wealth disappears at death rather than transferring to children. All agents within a cohort are identical, ruling out within-generation inequality. Markets are perfectly competitive with no frictions. Information is complete and certain.

The two-period restriction has been relaxed in the Auerbach-Kotlikoff multi-period framework, developed in their 1987 book. That model has 55 or more overlapping cohorts, calibrated to demographic data, and forms the basis of IMF and OECD simulations of pension reform and fiscal consolidation. The qualitative results survive the extension, but quantitative estimates of generational burdens require the multi-period setup.

The no-bequest assumption matters because Robert Barro showed in 1974 that altruistic parents who care about their children’s welfare make the OLG economy behave like the Ramsey model. If every generation leaves a bequest, dynasties become effectively infinite, Ricardian equivalence is restored, and government debt loses its real effects. Empirical work by Laurence Kotlikoff and Lawrence Summers found that bequests account for 30% to 80% of US wealth, depending on the definition, but most of these transfers are not motivated by pure altruism. Accidental bequests from uncertain lifespans, strategic bequests to extract care from children, and warm-glow bequests where parents value the act of giving rather than children’s utility all break the Barro equivalence even when transfers are large.

Within-cohort heterogeneity has been added through OLG models with idiosyncratic earnings shocks, building on work by Mark Huggett and Aiyagari. These models combine generational analysis with wealth distribution analysis and are now standard for studying inequality and tax progressivity. The cost is computational: closed-form solutions disappear, and simulations require careful calibration.

The OLG and Ramsey models complement rather than compete. Ramsey works well for questions where the long-run trade-off between investment and consumption matters most and where intergenerational distribution can be ignored. OLG is necessary for questions where life-cycle savings, pension design, and debt dynamics across cohorts drive the answer. Most modern quantitative public finance uses OLG.

What the Data Shows

Testing OLG predictions empirically has produced mixed results, with the most influential test concerning dynamic inefficiency. Andrew Abel, Gregory Mankiw, Lawrence Summers, and Richard Zeckhauser developed a sufficient statistic test in their 1989 Review of Economic Studies paper. Their criterion: an economy is dynamically efficient if the corporate sector is a net payer of dividends to shareholders rather than a net absorber of new equity. Applied to the United States and six other advanced economies for the postwar period, the test rejected dynamic inefficiency. Capital income exceeded gross investment in every country examined, meaning the marginal product of capital was above the growth rate.

The Abel et al. result has held up in updates. Federal Reserve research in the 2010s found returns to capital running 6% to 8% in the United States while population plus productivity growth was 2% to 3%, leaving a comfortable margin of dynamic efficiency. The implication is that pay-as-you-go pensions, while still socially valuable for insurance reasons, are not a Pareto improvement on private saving in the actuarial sense Samuelson described.

The asset market meltdown hypothesis, advanced by James Poterba and others in the early 2000s, predicted that baby boomer retirements would force massive sales of equities and bonds, depressing asset prices and depleting retirement savings. OLG simulations supported the prediction. The empirical realisation has been more muted. Equity prices have continued rising through the boomer retirement wave, partly because demographic effects work slowly, partly because foreign demand from younger emerging-market savers has filled the gap, and partly because returns to capital have stayed elevated. Demographic asset pricing remains a live research area, with work by John Geanakoplos and Andrew Abel showing that cohort size affects expected returns even if the meltdown scale was overstated.

Generational accounting, developed by Alan Auerbach, Jagadeesh Gokhale, and Laurence Kotlikoff in the early 1990s, applies OLG logic to government accounts. The method computes the present value of taxes minus transfers for each cohort and asks whether current fiscal policy implies a sustainable balance across generations. Most advanced economies fail the test by wide margins. OECD long-term fiscal projections show that maintaining current pension and healthcare commitments would require future generations in the United States, Italy, and Japan to pay 50% to 100% more in net taxes than current cohorts. Whether this is politically sustainable is the central fiscal question of the next two decades.

Public debt experiments provide a cleaner OLG test. Following the 2008 crisis, advanced economies issued massive new debt. IMF tracking of intergenerational impacts found patterns consistent with OLG predictions: current cohorts gained from stimulus spending, while younger and unborn cohorts will service the debt through higher future taxes. The Ricardian prediction that households would offset debt issuance with higher savings was decisively rejected. US household savings rates fell during deficit-financed tax cuts in 2017 and rose modestly during pandemic transfers in 2020 and 2021, but never enough to neutralise the fiscal stance.

The chart below traces capital stock dynamics in a calibrated OLG simulation under three different pay-as-you-go pension tax rates, illustrating the crowding-out of private capital that Diamond’s model predicts.

Source: Author calculations based on Diamond (1965) OLG framework, calibrated with Cobb-Douglas production, log utility, β=0.96, n=0.01, δ=0.05.

OLG’s Policy Relevance

The OLG model is the working framework for almost every serious analysis of social security, sovereign debt, and intergenerational policy. Its predictions shape how finance ministries cost pension reforms and how central banks think about the long-run fiscal stance.

Social security reform is the clearest application. The United States Social Security Trust Fund is projected to deplete its reserves around 2033, after which scheduled benefits would face an automatic 23% cut unless Congress raises the payroll tax, lifts the taxable wage cap, or trims benefits. Each option has different effects on each cohort, and an OLG model is the only way to compute them. Auerbach-Kotlikoff style simulations from the Congressional Budget Office show that delaying reform by ten years roughly doubles the burden on future generations, because the affected cohorts narrow as boomers exit the system. Similar logic applies to the UK State Pension, the German pension system, facing the demographic transition described in the silver economy, and Japan’s deeply stressed pension scheme.

Sovereign debt sustainability rests on OLG foundations. The standard debt sustainability analysis framework asks whether the present value of future primary surpluses covers current debt. In an OLG world, that question becomes: which generations will be taxed enough to repay? Sovereign debt analyses for the United States, Italy, France, and Japan show that current debt trajectories require future cohorts to accept either higher taxes or lower transfers than current ones. Whether that intergenerational bargain holds is a political question more than an economic one. The OLG model identifies the trade-off; democratic politics resolves it.

Climate policy is increasingly framed in OLG terms. Mitigation costs fall on people alive today. Avoided damages accrue to people not yet born. Standard cost-benefit analysis using a representative agent obscures the transfer; OLG analysis makes it explicit. William Nordhaus’s DICE model and Nicholas Stern’s review reach different policy conclusions partly because they treat intergenerational discounting differently. In an OLG framework, the choice of discount rate is not just a technical parameter but a statement about how much weight to give to the unborn. Economies that adopt aggressive climate policy are explicitly choosing to tax current generations to benefit future ones, exactly the kind of redistribution OLG models were built to analyse.

Government debt and capital crowding out matter for advanced economies even when they pass dynamic efficiency tests. Fiscal policy that issues debt to finance current consumption raises the equilibrium interest rate, reduces private capital accumulation, and lowers wages for future workers. The Penn Wharton Budget Model and similar OLG simulations suggest that the United States debt trajectory could lower long-run output by 4% to 8% relative to a balanced-budget path, with most of the loss falling on workers born after 2000. The mechanism is exactly what Diamond derived in 1965: government debt absorbs savings that would otherwise become productive capital.

Quantitative easing and unconventional monetary policy create intergenerational transfers that OLG models capture, and representative-agent models miss. When central banks buy long-duration bonds, they raise asset prices held disproportionately by older cohorts and lower returns on safe assets held disproportionately by younger savers. BIS research using OLG simulations finds that quantitative easing shifts wealth toward older households by 5% to 15% on average, with the largest gains accruing to the wealthiest retirees. Whether this is an intended policy or an unwanted side effect, it explains some of the political friction around central bank balance sheet expansion.

The policy reach of OLG extends beyond direct fiscal questions. Healthcare financing splits cohorts because younger workers fund Medicare and similar systems through payroll taxes while older cohorts consume the benefits. Education spending runs in reverse: working-age and older voters fund schools that benefit children. Tax progressivity has age dimensions that OLG models capture through life-cycle income paths. Even labour market regulation has an OLG flavour, since employment protection laws favour incumbents over new entrants.

The unifying insight, traceable to Samuelson’s 1958 paper, is that finite lives create economic problems that infinite-horizon models cannot see. Whenever a policy transfers resources across time in ways that affect different cohorts differently, OLG analysis is needed to evaluate the trade-off properly.

MASEconomics Explains

Four economic concepts behind the OLG model

Conclusion

The overlapping generations model economics framework reframes macroeconomics around a fact that representative-agent models hide: people are born, age, and die, and their economic interests change with their position in the life cycle. Samuelson’s 1958 paper and Diamond’s 1965 extension showed that finite lives produce dynamic inefficiency, break Ricardian equivalence, and give pay-as-you-go pensions a real economic role. The mathematics is harder than the Ramsey model, but the policy questions it answers are the ones that actually divide modern democracies.

Empirical evidence has refined the original predictions. The Abel et al. dynamic efficiency test found advanced economies operating below the golden rule, weakening the Pareto case for unfunded pensions. Generational accounting exposes large unfunded liabilities in most advanced economies. Asset market dynamics during the boomer retirement wave have been less dramatic than early simulations predicted, but still consistent with cohort-driven returns.

The model continues to anchor policy analysis on social security, sovereign debt, climate change, and central bank balance sheets. Auerbach-Kotlikoff multi-period extensions, Barro dynasty models, and OLG models with within-cohort heterogeneity have all expanded the framework without dislodging its central insight. Generations overlap, but they do not last, and that fact shapes the politics and economics of nearly every long-run policy choice.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.