In 1926, the statistician George Udny Yule presented a puzzle to the Royal Statistical Society. Between 1866 and 1911, the share of marriages in England performed by the Church of England fell steadily, and over the same decades the national mortality rate fell steadily too. Run a correlation between the two and you get 0.95, a figure so high that any conventional test would call it overwhelmingly significant. Yet no one believes that civil weddings kept people alive, or that church weddings killed them. The two series had nothing to do with each other. They simply drifted downward together across the same half-century, and that shared drift was enough to manufacture a correlation that looked like a discovery. This is the classic illustration of spurious regression: a statistically significant relationship between variables that are not actually related, produced by the way each variable moves over time rather than by any genuine connection between them.

The problem is not a curiosity from the early history of statistics. It is one of the most common ways that time-series analysis goes wrong, and it is dangerous precisely because the symptoms mimic success. A spurious regression typically produces a large t-statistic, a high R-squared, and a coefficient that looks economically meaningful. Everything the analyst was trained to look for as evidence of a real effect is present, and all of it is an illusion. Understanding why this happens, and how to detect it, is one of the foundations of working with economic time series.

Why Trending Series Correlate by Accident

The root of the problem is that many economic time series are nonstationary. A stationary series fluctuates around a constant mean with a stable variance, so that its statistical behavior today looks like its behavior a decade ago. A nonstationary series does not. The most important case is the random walk, where each value equals the previous value plus a random shock, so that shocks accumulate permanently rather than dying out.

Random Walk With Drift

Consider two independent random walks generated by completely separate streams of random shocks. By construction, they have no relationship whatsoever. But each one wanders away from its starting point and tends to keep moving in whatever direction its accumulated shocks have pushed it. Over any given sample, one will probably drift upward while the other drifts upward too, or both downward, or one up and one down. Whatever the pattern, a straight line fitted between them will usually find apparent structure, because two series that both trend will line up against each other far more often than chance would suggest for two stationary series.

The reason this fools the standard regression machinery is subtle. Ordinary least squares assumes the regression errors are well behaved, in particular that they do not themselves carry a trend. When both the dependent and independent variables are nonstationary and unrelated, the regression residuals inherit the nonstationarity. The errors are not random noise around the fitted line; they are themselves a wandering, trending series. This violates the assumptions that make the usual t-statistics and standard errors valid, and the violation is not mild. The whole inferential apparatus breaks.

The Statistics That Should Warn You, and Why They Do Not

The deepest result in this area is that the diagnostic tools an analyst would normally trust point in exactly the wrong direction under spurious regression. Granger and Newbold demonstrated this with simulations in their 1974 paper, and Peter Phillips later proved the asymptotic theory behind it. The finding is that the conventional t-statistic and F-statistic from a regression of one independent random walk on another do not settle down to stable distributions as the sample grows. They diverge. The larger the sample, the larger the t-statistic tends to become, which means that collecting more data makes a false relationship look more convincing rather than less.

This inverts the intuition that more data is always safer. With stationary series, a larger sample sharpens estimates and exposes relationships that are not real as statistically insignificant. With nonstationary series in a spurious regression, a larger sample inflates the apparent significance of a relationship that does not exist. The t-statistic that would normally reassure the analyst is, in this setting, the very thing producing the false confidence.

| Diagnostic | Genuine relationship (stationary) | Spurious regression (two random walks) |

|---|---|---|

| R-squared | Reflects true explanatory power | Often high, but meaningless |

| t-statistic | Stabilizes; falls toward zero if no effect | Diverges; grows with sample size |

| Durbin-Watson statistic | Near 2 when errors are clean | Near 0, signalling trending residuals |

| Residuals | Stationary noise around the line | Nonstationary; wander and trend |

| Reliable conclusion | Standard inference valid | Standard inference invalid |

|

Source: Properties summarised from Granger and Newbold (1974) and Phillips (1986).

|

||

The Durbin-Watson statistic deserves a special mention, because it is the one diagnostic that does sound the alarm. A Durbin-Watson value far below 2, particularly close to 0, indicates strongly autocorrelated residuals, which is the fingerprint of trending errors. Granger and Newbold proposed a memorable rule of thumb: if the R-squared exceeds the Durbin-Watson statistic, the regression should be treated with deep suspicion. A high R-squared paired with a very low Durbin-Watson is the combination that should make an analyst stop rather than celebrate.

Warning. A high R-squared is not evidence of a real relationship when the series are nonstationary. In a spurious regression the R-squared is often higher than in many genuine economic relationships. The size of the fit tells you nothing about whether the relationship is real; the behavior of the residuals does.

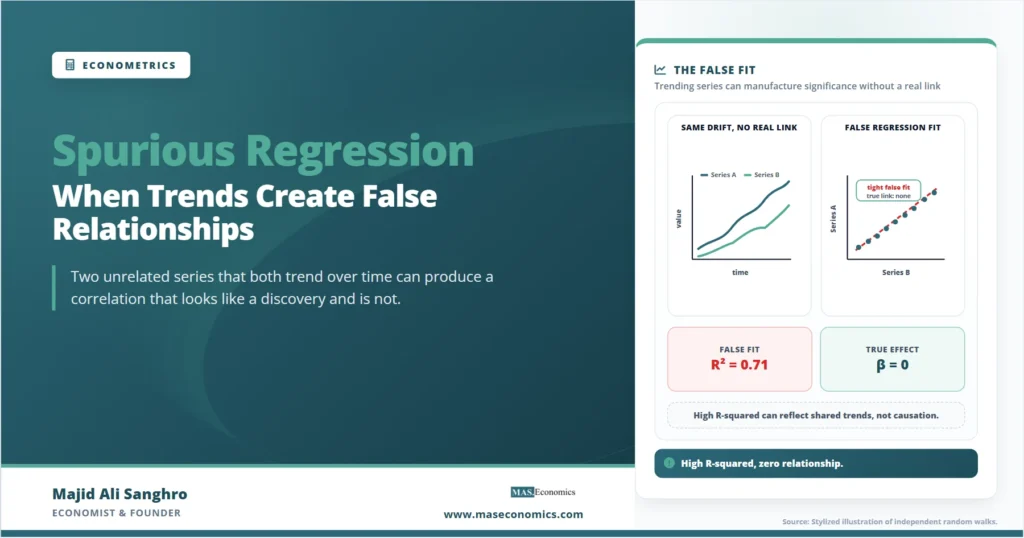

A Worked Example: Two Series That Share Nothing

Consider a stylized example with internally consistent numbers. Two series are generated as independent random walks, each from its own separate set of random shocks, so that the true relationship between them is exactly zero. An analyst who did not know how the data were generated regresses the first on the second and reads off the output.

| Output statistic | Value | How it looks | What is actually true |

|---|---|---|---|

| Slope coefficient \(\hat{\beta}\) | 0.82*** | Large and highly significant | True value is zero |

| Standard error | (0.06) | Tight, suggesting precision | Invalid; based on broken assumptions |

| t-statistic | 13.7 | Far beyond any critical value | Diverges with sample size |

| R-squared | 0.71 | Strong fit | Explains nothing real |

| Durbin-Watson | 0.18 | The one red flag | Confirms trending residuals |

| Verdict | — | Looks like a strong result | Entirely spurious |

|

Source: Stylized example based on standard formulas. Numbers chosen for illustration.

|

|||

Every headline number in this output is the kind that an empirical economist would normally treat as a finding worth reporting. The coefficient is large, the t-statistic is enormous, and the R-squared is high. Only the Durbin-Watson statistic, sitting at 0.18 against an ideal of around 2, betrays the truth. The residuals are not clean noise; they are a wandering series that trends along with the regressors. The relationship is an artifact of two series drifting through the same window of time, and nothing more.

Unit Roots: The Source of the Trouble

The formal language for this problem is the unit root. A series has a unit root when the coefficient on its own lagged value equals one, which is exactly the random-walk case where shocks accumulate without decay. A series with a unit root is integrated of order one, written \(I(1)\), meaning it must be differenced once to become stationary. Spurious regression arises specifically when two \(I(1)\) series that are not genuinely linked are regressed on each other in levels.

This is why the diagnosis runs through testing for unit roots before running a levels regression. The question to ask of any economic time series is whether it is stationary or whether it contains a unit root, and the answer determines whether ordinary regression in levels is even permissible. The properties that make a series safe or dangerous for regression are exactly the properties covered in the treatment of stationarity in time-series econometrics. A series that is stationary can be regressed on another stationary series with the usual tools. A pair of unit-root series cannot, unless a further condition holds.

Detecting and Avoiding the Trap

The practical workflow has a clear order. The first step is to test each series for a unit root before running any regression in levels. The standard tool is the Augmented Dickey-Fuller test, which tests the null hypothesis that a series contains a unit root against the alternative that it is stationary. If the test fails to reject the null for both series, the analyst is in dangerous territory and must not interpret a levels regression at face value.

The most common fix is to difference the series. Taking first differences of an \(I(1)\) series, that is, working with the change from one period to the next rather than the level, usually produces a stationary series on which ordinary regression is valid. Differencing removes the accumulated trend that drives the spurious correlation. The cost is that differencing discards information about the long-run levels of the variables, and it answers a different question: it describes how changes relate to changes, not how levels relate to levels.

There is one important exception that rescues levels regressions in special cases. Two \(I(1)\) series can be genuinely linked if they share a common stochastic trend, so that a particular linear combination of them is stationary even though each series individually is not. This is cointegration, and it is the line that separates a spurious regression from a meaningful long-run relationship. When two series are cointegrated, regressing one on the other in levels is not spurious; it estimates a real equilibrium relationship. The methods for testing this directly, and for modeling the short-run dynamics around the long-run equilibrium, are developed in the treatment of cointegration and the Engle-Granger method. The whole apparatus of cointegration exists precisely to tell apart two cases that look identical in a raw levels regression: a false relationship between drifting series and a true one between series tied together over the long run.

Caveat. Adding a deterministic time trend to the regression does not reliably cure spurious regression when the series have unit roots. A time trend handles series that are trend-stationary, meaning stationary around a fixed line, but it does not address the stochastic trend of a random walk. Distinguishing a deterministic trend from a stochastic one is itself part of what unit-root testing decides.

Where Spurious Regression Sits in the Toolkit

Spurious regression is one of the clearest illustrations of why the assumptions behind a method matter as much as the method itself. The mechanics of fitting a line are the same whether the underlying series are stationary or not, which is exactly why the trap is so easy to fall into. The foundations of fitting and interpreting that line are covered in the treatments of simple linear regression and multiple regression models, and the spurious-regression problem is best understood as what happens when the data fed into those models violate the conditions those models assume.

The problem also connects to the wider question of what a statistical relationship between time series actually means. A high correlation between two trending variables tells us nothing about whether one helps predict the other once their trends are accounted for, which is the question that Granger causality was designed to address, and which itself requires stationary inputs to be meaningful. Seen in this company, spurious regression is not an isolated pitfall. It is the canonical reminder that economic time series carry structure across time, and that ignoring that structure turns the ordinary tools of regression into machines for generating confident nonsense.

Explains

Three ideas that make the spurious-regression trap clear

Build your time-series foundations one diagnostic at a time.

Explore the MASEconomics BlogConclusion

The danger of spurious regression is that it counterfeits every sign of a genuine result. A regression of one nonstationary series on another unrelated nonstationary series typically delivers a large coefficient, a small standard error, a t-statistic that grows with the sample, and a high R-squared. The trended residuals that should expose the problem are invisible unless the analyst inspects them, and the single diagnostic that does flag the trouble, a Durbin-Watson statistic near zero, is easy to overlook in the glow of an apparently strong fit. Yule’s nineteenth-century marriage and mortality series, correlated at 0.95 with no causal link whatever, remains the cleanest demonstration that shared movement over time is not evidence of a shared cause.

The defense is procedural and well established. Test each series for a unit root before interpreting any regression in levels, treat a high R-squared paired with a low Durbin-Watson as a warning rather than a triumph, and difference the series when they are nonstationary and not cointegrated. The one case in which a levels regression survives is cointegration, where a stationary linear combination ties the series together in a genuine long-run relationship. The lesson that runs through all of this is that the validity of a regression depends on the time-series properties of its inputs, and that with economic data those properties cannot be assumed. They have to be tested.

Frequently Asked Questions

What is a spurious regression?

A spurious regression is a regression that shows a statistically significant relationship between variables that are not genuinely related. It typically arises when two nonstationary time series, each trending over time, are regressed on each other in levels. The shared movement through time produces a large coefficient, a high R-squared, and a significant t-statistic, even though the true relationship between the variables is zero.

How do you detect a spurious regression?

Test each series for a unit root before running a levels regression, using a test such as the Augmented Dickey-Fuller test. After running the regression, inspect the Durbin-Watson statistic: a value far below 2, especially near 0, signals trending residuals. Granger and Newbold’s rule of thumb is that if the R-squared exceeds the Durbin-Watson statistic, the regression is likely spurious. Examining the residuals for nonstationarity is the most direct check.

Why does a high R-squared not prove a relationship is real?

Because in a spurious regression the R-squared measures how well two trends line up, not whether one variable explains the other. Two unrelated random walks that both drift over the same period will often produce an R-squared higher than many genuine economic relationships. The size of the fit reflects shared movement over time, which says nothing about a causal or structural link. The behavior of the residuals, not the R-squared, reveals whether the relationship is genuine.

How do you fix a spurious regression?

The usual fix is to difference the nonstationary series, working with period-to-period changes rather than levels, which typically restores stationarity and makes ordinary regression valid. The exception is cointegration: if the two series share a common stochastic trend so that a linear combination of them is stationary, the levels regression is not spurious and instead estimates a real long-run relationship. Testing for cointegration distinguishes the two cases.

Does adding a time trend solve the problem?

Not reliably. Adding a deterministic time trend addresses series that are trend-stationary, meaning stationary around a fixed line. It does not address the stochastic trend of a random walk, which is the usual source of spurious regression. Deciding whether a series has a deterministic trend or a stochastic one is part of what unit-root testing determines, so the time trend is not a substitute for testing for unit roots.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics