You have probably paid for a gym membership you never used, held onto a losing stock far too long, or chosen the default option on a form without reading the alternatives. Classical economics would struggle to explain any of these decisions. After all, the standard model assumes that people are rational agents who carefully weigh costs and benefits, process all available information, and always choose the option that maximizes their well-being.

Behavioral economics says: not so fast.

Over the past five decades, a revolution in economic thinking has shown that real human beings are not the hyper-rational calculators that textbook models describe. We rely on mental shortcuts. We are swayed by how choices are presented. We feel the sting of a loss far more intensely than the pleasure of an equally sized gain. And these are not random errors. They are systematic, predictable patterns that behavioral economists have documented, measured, and increasingly used to design better public policy.

What Is Behavioral Economics?

Behavioral economics is the study of how psychological, cognitive, and emotional factors influence the economic decisions of individuals and institutions. It combines insights from psychology with the analytical tools of economics to build models that better predict how people actually behave, as opposed to how perfectly rational agents would behave.

The field did not emerge overnight. Its intellectual roots stretch back to Adam Smith’s The Theory of Moral Sentiments (1759), in which Smith observed that people are driven by passions, social comparison, and a deep fear of loss. But for most of the twentieth century, mainstream economics chose a different path. The dominant paradigm, known as neoclassical economics, built its models on the assumption that agents are rational, self-interested, and capable of processing unlimited information.

The first serious challenge came from Herbert Simon, who introduced the concept of “bounded rationality” in the 1950s. Simon argued that people do not optimize; they satisfice, choosing the first option that meets a minimum threshold of acceptability rather than exhaustively searching for the best one. Simon received the Nobel Memorial Prize in Economic Sciences in 1978 for this insight.

The breakthrough that launched behavioral economics as a distinct field came from two Israeli psychologists: Daniel Kahneman and Amos Tversky. In a series of landmark experiments during the 1970s, they demonstrated that people systematically deviate from the predictions of expected utility theory. Their 1979 paper, “Prospect Theory: An Analysis of Decision Under Risk,” published in Econometrica, is one of the most cited papers in the history of economics. Kahneman received the Nobel Prize in 2002 for integrating psychological research into economic science.

The next transformative figure was Richard Thaler, who spent decades translating Kahneman and Tversky’s laboratory findings into practical economic applications. Thaler coined the concept of “mental accounting” (why people treat money differently depending on where it comes from), identified the “endowment effect” (why people overvalue what they already own), and co-authored Nudge with legal scholar Cass Sunstein in 2008. Thaler received the Nobel Prize in Economics in 2017 for his contributions to behavioral economics.

Today, behavioral economics is no longer a fringe movement. It is taught in every major economics department, informs policy at the highest levels of government, and has reshaped how businesses design products, set prices, and communicate with customers.

System 1 and System 2: How Your Brain Makes Decisions

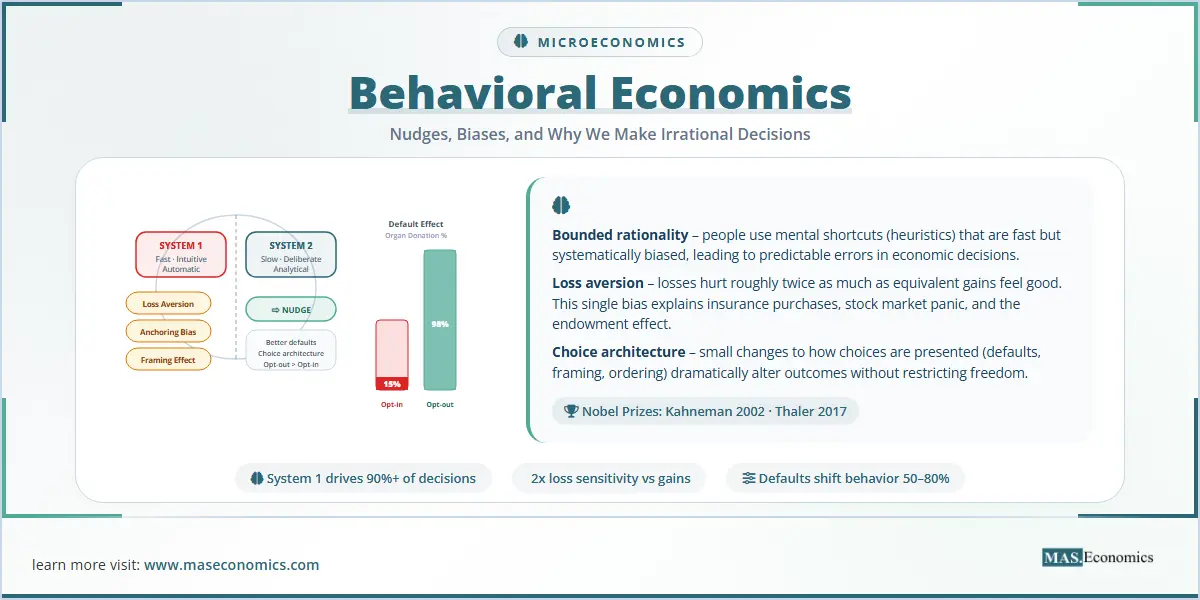

At the heart of behavioral economics lies Kahneman’s dual-process theory, which he popularized in his bestselling book Thinking, Fast and Slow (2011). Kahneman proposed that the human brain operates through two distinct cognitive systems.

System 1 is fast, automatic, and intuitive. It operates with little effort or conscious control. When you flinch at a loud noise, instantly recognize a friend’s face, or feel anxious when a stock price drops, System 1 is at work. It relies on heuristics, which are mental shortcuts that allow rapid judgments. Most of the time, these shortcuts serve us well. But in complex economic environments, they produce systematic errors.

System 2 is slow, deliberate, and analytical. It engages when you calculate a tip, compare mortgage rates, or work through a difficult econometric model. System 2 requires effort, and because mental effort is costly, people tend to default to System 1 whenever possible.

The central insight is this: most economic decisions are made by System 1, not System 2. When consumers choose between products on a supermarket shelf, when investors react to market news, when employees decide whether to enroll in a retirement plan, the fast, automatic system dominates. This is why cognitive biases are not occasional mistakes. They are the default mode of human economic behavior.

This insight has profound implications for economics. Traditional models assume that people behave as if they are always using System 2: carefully weighing probabilities, computing expected values, and comparing marginal utilities. Behavioral economics recognizes that System 2 thinking is the exception, not the rule, and builds models that account for the systematic shortcuts and errors that System 1 produces.

The Key Cognitive Biases That Shape Economic Choices

Decades of research have identified dozens of cognitive biases that affect economic decisions. Below are the most important ones, each with direct relevance to markets, policy, and everyday financial behavior.

Loss Aversion

Loss aversion is arguably the most powerful bias in economics. Kahneman and Tversky’s research showed that people experience the pain of losing approximately twice as intensely as the pleasure of an equivalent gain. Losing $100 feels roughly as bad as gaining $200 feels good. This asymmetry means that people are far more motivated to avoid losses than to pursue gains.

Loss aversion explains an enormous range of economic behavior. It explains why investors hold losing stocks too long (selling would mean “realizing” the loss), why homeowners refuse to sell their house below the purchase price even in a falling market, why consumers are more responsive to price increases than to equivalent discounts, and why employees resist wage cuts even when economic conditions would justify them.

The Anchoring Effect

When people make numerical estimates, they tend to be heavily influenced by the first number they encounter, even when that number is arbitrary or irrelevant. In a classic experiment, Tversky and Kahneman spun a rigged roulette wheel in front of participants and then asked them to estimate the percentage of African countries in the United Nations. People who saw the wheel land on 65 gave significantly higher estimates than those who saw it land on 10, despite the wheel having nothing to do with the question.

Anchoring has powerful implications for pricing strategies. Retailers place expensive items next to standard ones so the standard item looks like a bargain. Real estate agents show an overpriced house first so the next property seems reasonable. Salary negotiations are shaped by whoever states a number first.

The Framing Effect

Identical information presented in different ways leads to different decisions. Tversky and Kahneman’s classic example involved a disease expected to kill 600 people. When the policy options were framed in terms of lives saved (“Program A saves 200 people”), participants preferred the certain option. When the same options were framed in terms of deaths (“Program B: 400 people will die”), participants preferred the risky option. The underlying choice was mathematically identical, yet the framing completely reversed the preference.

Framing effects pervade economic life. “90% fat-free” yogurt outsells yogurt labeled “contains 10% fat.” Investment products described in terms of potential returns attract more buyers than the same products described in terms of potential losses. Tax policies framed as “bonuses” are more popular than identical policies framed as “reduced penalties.”

Status Quo Bias and the Endowment Effect

People have a strong preference for the current state of affairs, even when an alternative would make them objectively better off. This is status quo bias. A closely related phenomenon is the endowment effect: once people own something, they value it more highly than they did before they owned it. In experiments, people demand roughly twice as much to give up a coffee mug they have been given as they would be willing to pay to acquire the same mug.

These biases have enormous policy implications. Default options in retirement plans, insurance contracts, and organ donation registries are extraordinarily powerful precisely because people tend to stick with whatever option is pre-selected.

The Sunk Cost Fallacy

Rational economic agents should ignore costs that have already been incurred and cannot be recovered. But in practice, people consistently let sunk costs influence their decisions. You stay in a bad movie because you paid for the ticket. A company pours more money into a failing project because “we’ve already invested so much.” A government continues funding an uneconomical infrastructure project because abandoning it would mean “wasting” the money already spent. The money pump argument in consumer choice theory illustrates how such irrational cycling of preferences can be exploited.

Hyperbolic Discounting

Standard economic models assume that people discount the future at a constant rate: if you prefer $100 today over $110 in a month, you should also prefer $100 in 12 months over $110 in 13 months. In reality, people’s discount rates are not constant. They are heavily biased toward the present.

This is hyperbolic discounting. People dramatically overvalue immediate rewards relative to future ones, which explains chronic under-saving, over-borrowing, procrastination, and the difficulty of maintaining healthy habits. It is one of the reasons why automatic enrollment in retirement savings plans, which forces the decision into the future by making saving the default, is so effective.

| Bias | What It Is | Economic Example | Policy Implication |

|---|---|---|---|

| Loss Aversion | Losses hurt ~2x more than equivalent gains feel good | Investors hold losing stocks; homeowners reject below-purchase offers | Frame policy changes as avoiding losses, not gaining benefits |

| Anchoring | First numbers encountered distort subsequent estimates | Salary negotiations shaped by the first offer; MSRP as price anchor | Set reference points carefully in policy communication |

| Framing | How options are presented changes the choice made | “90% fat-free” outsells “10% fat”; gains vs. losses framing reverses risk preferences | Present health, tax, and savings messages in gain frames |

| Status Quo Bias | People stick with the current option even when switching is beneficial | Employees stay in default health plans; consumers rarely switch energy providers | Set defaults to the socially optimal option |

| Sunk Cost Fallacy | Past unrecoverable spending influences future decisions | Continuing failed projects because “we’ve invested too much”; staying in bad movies | Require independent cost-benefit reviews for ongoing public projects |

| Hyperbolic Discounting | People dramatically overvalue immediate rewards relative to future ones | Chronic under-saving for retirement; over-borrowing on credit cards | Auto-enroll employees in savings plans with opt-out |

|

|||

Nudge Theory

If cognitive biases are systematic and predictable, can they be used to help people make better decisions? This is the central question behind nudge theory, developed by Richard Thaler and Cass Sunstein in their 2008 book Nudge: Improving Decisions About Health, Wealth, and Happiness.

A nudge is any aspect of the “choice architecture” that alters people’s behavior in a predictable way without forbidding any options or significantly changing their economic incentives. It is not a mandate or a tax. It is a gentle push in a direction that the evidence suggests will improve outcomes.

The most powerful nudge is the default option. The research by Eric Johnson and Daniel Goldstein (2003), published in Science, demonstrated this with a striking example from organ donation policy. In countries where citizens must actively opt in to become organ donors (such as Denmark, the Netherlands, and Germany), donation consent rates range from 4% to 28%. In countries where citizens are automatically enrolled as donors but can opt out (such as Austria, Belgium, and France), consent rates reach 98% to nearly 100%.

The difference is not in attitudes toward organ donation. Surveys show that large majorities in all these countries support donation. The difference is entirely in how the choice is structured. When donating is the default, nearly everyone sticks with it. When not donating is the default, most people stick with that, too. This is status quo bias and loss aversion working in tandem: changing the default feels like an active choice, and active choices require effort that System 1 avoids.

Source: Johnson & Goldstein (2003), Science; updated with 2023 registry data | MASEconomics.com

The chart above reveals the staggering power of default settings. There is no significant difference in cultural attitudes toward organ donation between these countries, yet the policy design creates a sixfold difference in consent rates. This is the essence of nudge theory: small changes to choice architecture produce enormous changes in behavior.

Governments around the world have embraced this approach. The United Kingdom established the Behavioural Insights Team (popularly known as the “Nudge Unit”) in 2010 under Prime Minister David Cameron. It became the first government agency dedicated to applying behavioral science to public policy. The team has since run over 750 randomized controlled trials, influencing policy on tax compliance, energy conservation, job training, and health behaviors.

In the United States, Thaler worked with the Obama administration to establish a Social and Behavioral Sciences Team in 2015. Similar units now operate in over 200 government agencies worldwide, from Australia to Singapore to the World Bank.

How Behavioral Economics Is Changing Policy and Business

The practical impact of behavioral economics extends far beyond organ donation defaults. Here are the most significant applications transforming policy and business around the world.

Retirement Savings

One of Thaler’s most celebrated contributions is the Save More Tomorrow (SMarT) program, developed with Shlomo Benartzi. The program exploits three behavioral insights simultaneously. First, it uses the default effect by auto-enrolling employees into retirement savings plans. Second, it exploits hyperbolic discounting by asking employees to commit to saving more in the future (when the sacrifice feels distant) rather than immediately. Third, it ties increases to future pay raises, so employees never see their take-home pay decrease, avoiding loss aversion.

The results were extraordinary. In the first implementation, employee savings rates increased from 3.5% to 13.6% over four pay raises. The 2006 Pension Protection Act in the United States, which encouraged auto-enrollment in 401(k) plans, was directly influenced by this behavioral research.

Tax Compliance

The UK Behavioural Insights Team found that a single line added to tax reminder letters, stating that “9 out of 10 people in your area have already paid their taxes,” increased payment rates by 5 percentage points. This leverages social norms, another powerful behavioral tool. People are strongly motivated to conform to what they perceive others are doing.

Health and Wellness

Placing healthier food options at eye level in school cafeterias, a strategy known as “cafeteria nudging,” increased vegetable consumption by 25% without removing any choices. Calorie labeling on restaurant menus, simplified prescription instructions, and text message appointment reminders all draw on behavioral insights to improve health outcomes without restricting individual freedom.

Marketing and Pricing

Businesses have long used behavioral economics intuitively. Subscription services exploit status quo bias by making cancellation difficult. Retailers use anchoring by displaying a high “original price” next to the “sale price.” Airlines use price discrimination strategies informed by framing effects, showing “only 3 seats left at this price” to trigger scarcity-driven urgency. Understanding these mechanisms helps consumers recognize when they are being nudged and make more informed decisions.

Behavioral Economics vs. Classical Economics

It is important to understand that behavioral economics does not reject classical economics. It refines it. Revealed preference theory and indifference curve analysis remain powerful tools for understanding consumer behavior in competitive markets with simple choices. The rational agent model works remarkably well when decisions are repeated, feedback is immediate, and stakes are moderate. People learn to be good shoppers for groceries because they buy them every week and can easily compare prices.

Where behavioral economics adds its greatest value is in decisions that are infrequent, complex, and consequential: choosing a mortgage, selecting a health insurance plan, planning for retirement, or voting on public policy. These are precisely the domains where System 2 should dominate but where System 1 typically takes over because the complexity overwhelms deliberate analysis.

The field has also enriched our understanding of market failures. Traditional market failure analysis focuses on externalities, public goods, and information asymmetries. Behavioral economics adds a new category: “internalities,” where individuals make choices that harm their own future selves due to present bias, limited attention, or cognitive overload.

Criticisms and Limitations

Behavioral economics is not without its critics, and a balanced assessment requires acknowledging several important challenges.

The libertarian paternalism debate. Critics argue that nudges, even when well-intentioned, represent a form of manipulation. If governments can nudge people toward “better” choices, who decides what “better” means? This concern is especially acute in authoritarian contexts where nudge techniques could be used to suppress dissent rather than improve welfare.

The replication crisis. Some of the field’s famous findings have faced challenges in replication studies. Several high-profile priming effects reported in early behavioral economics literature have failed to replicate in larger, pre-registered studies. However, the core findings (loss aversion, the default effect, anchoring, hyperbolic discounting) have replicated robustly across cultures and contexts.

Scalability. Nudges work well for specific, bounded decisions, but they are less effective for complex structural problems like income inequality or climate change, which require systemic policy interventions beyond choice architecture.

Despite these limitations, the empirical foundation of behavioral economics is strong, its practical applications are growing, and its integration into mainstream economic thinking is now irreversible.

MASEconomics Explains

Four economic concepts you need to understand behavioral economics

Cognitive Bias

A systematic pattern of deviation from rational judgment. Unlike random errors, cognitive biases are predictable and consistent, allowing economists to model and anticipate them. Major biases include loss aversion, anchoring, framing, status quo bias, and hyperbolic discounting.

Nudge Theory

A framework for influencing behavior by changing how choices are presented, without restricting options or significantly altering incentives. Developed by Richard Thaler and Cass Sunstein, nudges include default settings, social norm messaging, and simplified information design.

Loss Aversion

The empirical finding that the psychological impact of a loss is approximately twice as large as the impact of an equivalent gain. First documented by Kahneman and Tversky in Prospect Theory (1979), loss aversion is the foundation for understanding risk behavior, the endowment effect, and status quo bias.

Choice Architecture

The design of environments in which people make decisions. A choice architect organizes the context in which people choose: the number of options, the default selection, the order of presentation, and the information provided. Every decision has an architecture, and that architecture is never neutral.

Key Takeaway and Conclusion

Behavioral economics has demonstrated, with rigorous experimental evidence, that human beings are not the perfectly rational agents of classical economic theory. We are predictably irrational. We overweight losses, anchor to irrelevant numbers, default to the status quo, throw good money after bad, and systematically overvalue the present at the expense of the future.

But this irrationality is not a weakness of the discipline. It is its greatest opportunity. Because these biases are systematic, they can be anticipated, modeled, and used to design better institutions, policies, and markets. The nudge revolution has shown that small, low-cost changes to choice architecture can produce dramatic improvements in savings rates, health outcomes, tax compliance, and organ donation, all without restricting individual freedom.

Behavioral economics helps you spot when your gut (System 1) is steering you wrong, so your wiser self (System 2) can take over.

Economics is about choices. Behavioral economics is about understanding how those choices are really made.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.