In 1931, Harold Hotelling published “The Economics of Exhaustible Resources” in the Journal of Political Economy. The paper derived a single equation relating the price path of a non-renewable resource to the rate of interest. It launched the field of natural-resource economics. The Hotelling Rule says that under perfect competition and certainty, the net price of an exhaustible resource, price minus marginal extraction cost, must grow at the real rate of interest. Hotelling published a separate and equally famous result two years earlier on spatial competition; the Hotelling location model is a different result from a different paper. What follows derives the rule from a dynamic optimisation problem, presents the empirical record from oil and copper prices, and traces its grip on climate policy, critical-minerals strategy, and the valuation of resource companies today.

What the Hotelling Rule Means

The Hotelling Rule emerged from the conservation-versus-development debate that dominated American resource policy in the 1920s. Conservationists argued that private owners would extract resources too quickly, leaving future generations impoverished. Developers argued that market prices would naturally regulate extraction, rising as scarcity increased and signalling the appropriate time to slow down. The debate lacked a rigorous analytical framework. Hotelling provided one.

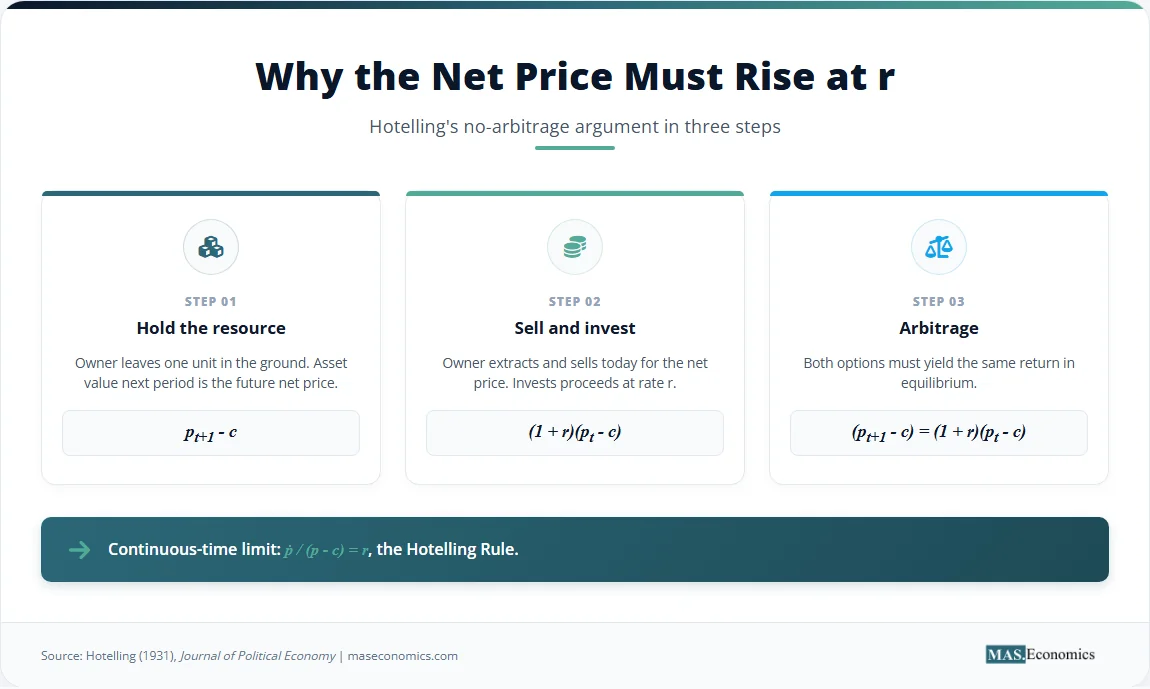

Hotelling approached the problem by treating an exhaustible resource as a financial asset. A barrel of oil left in the ground is an asset that yields a return through its price appreciation. A barrel of oil extracted and sold yields a return equal to the interest rate earned on the cash proceeds. The resource owner is an investor choosing between two assets: the underground resource and a bank deposit. For the owner to be indifferent between holding the resource and selling it, the two assets must offer the same rate of return.

This arbitrage argument is the core of the theory. If the net price of the resource is expected to grow more slowly than the interest rate, the owner is better off extracting the resource today, selling it, and investing the proceeds in a bank account. Every rational owner will extract, supply will flood the market, and the current price will fall until the expected future price growth equals the interest rate. If the net price is expected to grow faster than the interest rate, the owner is better off leaving the resource in the ground. Supply is withheld, the current price rises, and the expected future price growth falls. Arbitrage forces the system into equilibrium where the net price grows at exactly the real interest rate.

The result is powerful because it does not depend on demand elasticity, the size of the resource stock, or the time horizon. It is a pure no-arbitrage condition. It tells us that the scarcity rent, the economic return to owning a finite resource, must rise at the rate of interest. The scarcity rent is the difference between the market price and the marginal cost of extraction. In a competitive market, this rent is the shadow price of the resource in situ, the value of leaving it in the ground for one more period.

The Hotelling Rule provides the baseline for how non-renewable resource prices should behave. It is the standard against which actual price paths are judged. Deviations from the rule reveal the influence of factors the baseline model assumes away: technological change, reserve uncertainty, market power, and the emergence of substitute goods. The rule does not predict the level of prices, which depends on demand and initial stock, but it predicts the slope of the price path over time.

Hotelling Rule in Equations

The mathematical derivation of the Hotelling Rule formalises the arbitrage intuition using optimal control theory. A resource owner holds a stock \( S_t \) of an exhaustible resource and chooses an extraction path \( q_t \) over time. The state equation governs the depletion of the stock:

The owner maximises the present value of profits at constant marginal extraction cost \( c \) and market price \( p_t \). The objective function is:

Here, \( r \) is the real interest rate, and \( T \) is the exhaustion date when the stock reaches zero. The current-value Hamiltonian for this problem is:

In this Hamiltonian, \( \mu_t \) is the shadow price, or the in-situ value, of the resource. It is the opportunity cost of extracting one unit today rather than leaving it in the ground. The first-order condition with respect to the control variable \( q_t \), assuming an interior solution where extraction is positive, requires the marginal profit from extraction to equal the marginal opportunity cost:

This equation states that the net price, or the price minus marginal extraction cost, exactly equals the shadow price of the resource. The costate equation governs how the shadow price evolves over time. It requires the shadow price to grow at the real interest rate:

Combining these two equations yields the central result. Because \( \mu_t = p_t – c \), and \( c \) is constant, the change in the net price equals the change in the shadow price. Substituting the first condition into the costate equation gives the Hotelling Rule:

The proportional growth rate of the net price equals the real interest rate. With zero marginal cost, the rule simplifies to the more familiar form where the gross price grows at the interest rate:

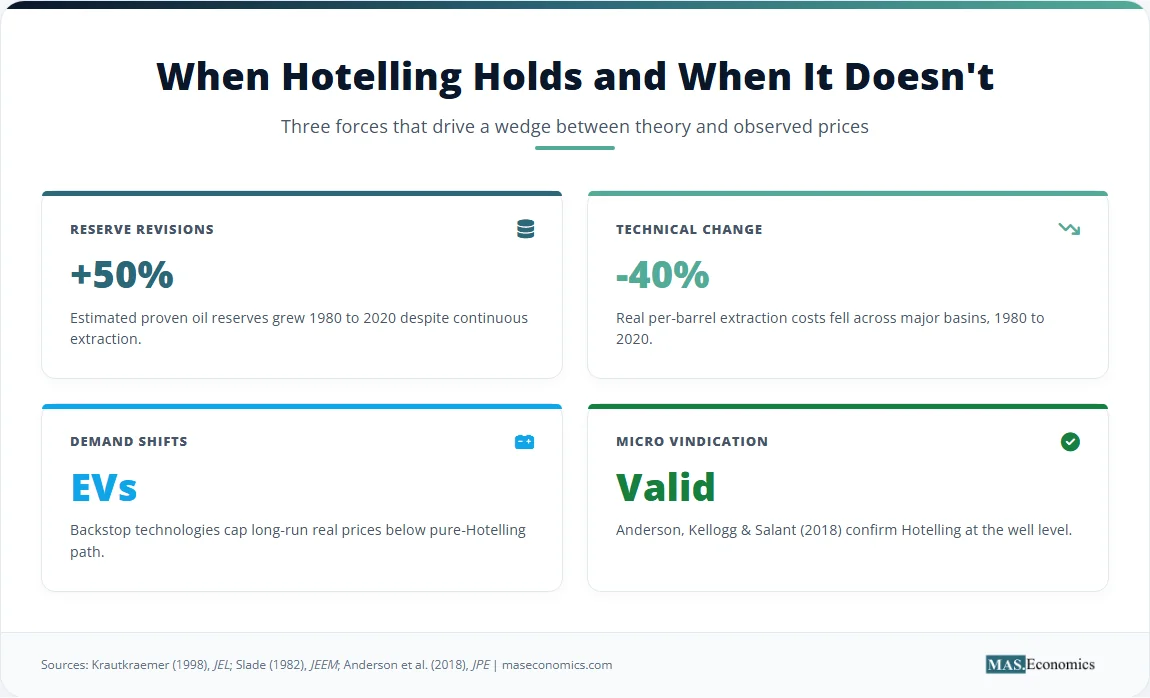

Consider a worked example. Suppose the real interest rate is four percent per year and the current net price of crude oil is sixty dollars per barrel. The Hotelling Rule predicts the net price next year is \( 60 \times 1.04 = 62.40 \), and in ten years \( 60 \times e^{0.04 \times 10} \approx 89.51 \). If the actual oil price in ten years is below this, either the resource is more abundant than thought, which leads to stock revisions, extraction technology has improved, which causes cost falls, or substitutes have weakened demand. All three forces have operated for oil between 1980 and 2020, which is why empirical net-price growth has averaged well below the interest rate.

| Symbol | Name | Definition | Empirical Range |

|---|---|---|---|

| \( S_t \) | Resource stock | Remaining reserves at time \( t \) | – |

| \( q_t \) | Extraction rate | Flow of resource extracted | – |

| \( p_t \) | Market price | Spot price of the resource | – |

| \( c \) | Marginal extraction cost | Cost of extracting one unit | $20–$60 / barrel oil |

| \( r \) | Real interest rate | Discount rate | 1–5% |

| \( \mu_t \) | Shadow price (in-situ value) | Net price = \( p_t – c \) | – |

| \( T \) | Exhaustion date | When stock reaches zero | – |

|

|||

Key Assumptions and Limitations

The Hotelling Rule rests on five central assumptions. First, it assumes perfect competition among resource owners. In a competitive market, no single owner can influence the price. If owners have market power, as OPEC does in the oil market, they can restrict output to keep prices above the competitive level, altering the price path. A monopolist maximises profits by restricting output and stretching the extraction period, which means the price path is steeper and the initial price is higher than under competition.

Second, the model assumes perfect certainty about future demand, technology, and reserves. In reality, resource owners face massive uncertainty. The size of the remaining stock is an estimate that gets revised as exploration proceeds. Future demand depends on economic growth and the development of substitutes. Future technology determines both extraction costs and the viability of alternatives. Uncertainty alters the extraction decision because risk-averse owners may extract faster to avoid the risk of future price collapses.

Third, the model assumes a constant marginal extraction cost. This simplification allows the rule to focus on the net price. In practice, extraction costs vary widely across deposits and over time. Low-cost reserves are extracted first. As these deplete, the industry moves to higher-cost sources, such as deep-water oil or low-grade copper ore. Rising marginal costs push up the gross price, but the net price, the scarcity rent, may actually fall if costs rise faster than gross prices.

Fourth, the framework assumes a homogeneous resource with one grade. Real resources come in multiple grades with different costs. The theory must be extended to handle the transition from high-grade to low-grade deposits, which alters the price path.

Fifth, the model assumes no backstop technology. A backstop is a substitute that can supply the resource in unlimited quantities at a constant cost, such as solar energy replacing fossil fuels. The existence of a backstop places a ceiling on the long-run price of the exhaustible resource. The price cannot rise above the backstop cost, because consumers will switch. This ceiling truncates the Hotelling price path, forcing the price to reach the backstop level exactly at the moment of exhaustion.

These limitations explain why the simple Hotelling Rule rarely matches observed price paths. Margaret Slade showed in 1982 that allowing a U-shaped time path for costs can reconcile the rule with falling observed prices. In the early stages of extraction, technological progress lowers costs faster than scarcity drives them up, so net prices fall. In the later stages, scarcity dominates, costs rise, and net prices increase. This U-shaped pattern fits the historical data for many minerals better than the monotonically increasing net price of the basic model.

Evidence for the Hotelling Rule

Empirical testing of the Hotelling Rule has produced mixed results. The simple version of the rule, predicting exponential growth in net prices at the real interest rate, is overwhelmingly rejected by aggregate data. However, refined versions that account for costs, technology, and market structure find more support. Three studies show this progression.

Margaret Slade provided the first major empirical reassessment in her 1982 Journal of Environmental Economics and Management paper, “Trends in Natural-Resource Commodity Prices: An Analysis of the Time Domain“. Slade examined the price paths of eleven major minerals over the twentieth century. She found that instead of the steady exponential increase predicted by the basic Hotelling model, most mineral prices followed a U-shaped path. Prices generally fell for the first half of the century, driven by technological improvements in extraction and the discovery of new low-cost deposits, and then began rising in the later decades as the easiest reserves were depleted. Slade showed that this U-shaped pattern is broadly consistent with Hotelling once cost-reduction dynamics and reserve revisions are included in the model. The pure model assumes these forces away, but when they are added back, the predicted path matches the data far better.

Jeffrey Krautkraemer surveyed the broader empirical record in his 1998 Journal of Economic Literature paper, “Nonrenewable Resource Scarcity“. Krautkraemer concluded that in-situ resource scarcity is real, meaning the shadow value of remaining reserves is positive, but the effects of this scarcity are largely offset by technical progress and reserve growth. Exploratory drilling consistently adds new reserves, and extraction technology continuously lowers the cost of accessing difficult deposits. These offsetting forces leave observed market prices well below the pure-Hotelling predictions. Krautkraemer also noted that the persistent failure of aggregate prices to rise at the interest rate does not invalidate the theoretical logic of the rule. It merely reflects the fact that the ceteris paribus conditions, particularly constant technology and fixed reserves, do not hold in the real world.

Soren T. Anderson, Ryan Kellogg, and Stephen W. Salant provided the most compelling micro-level vindication in their 2018 Journal of Political Economy paper, “Hotelling Under Pressure“. They used detailed data from Texas oil wells to test the rule at the level of the individual extraction unit. Previous tests used aggregate price data, which mixes high-cost and low-cost producers and conflates exploration success with scarcity rent. Anderson, Kellogg, and Salant found that within-well shadow values do follow the Hotelling Rule once well-level capacity constraints are properly modelled. Oil wells have a maximum flow rate determined by geological pressure. Owners manage this pressure, choosing when to extract and when to shut in the well, exactly as the Hotelling model predicts. The marginal value of the oil left in the well rises at the rate of interest. This result vindicated the theory at the micro level, even though aggregate prices appear to violate it. The aggregate divergence is driven by new discoveries and technological change at the extensive margin, not by a failure of the Hotelling arbitrage logic at the intensive margin.

The Hotelling Rule predicts smooth exponential growth at the real interest rate. Actual prices have followed neither path closely, reflecting reserve revisions, technological change, and demand shifts. Source: Energy Institute Statistical Review of World Energy 2024; World Bank Pink Sheet; Hotelling (1931), JPE.

How the Hotelling Rule Matters

The Hotelling Rule remains the foundational equation of natural-resource economics because it isolates the fundamental trade-off facing any owner of a finite asset: extract now or extract later. Three applications show its continuing relevance to policy and markets.

Climate policy and the green paradox represent the most important application. Hans-Werner Sinn showed in 2008 that announcing future carbon taxes can actually accelerate oil price shocks and current extraction, a counterintuitive result known as the green paradox. The logic is pure Hotelling. A future carbon tax reduces the future net price that the resource owner can expect to receive. Because the net price must rise at the rate of interest to satisfy the Hotelling arbitrage condition, a lower future net price implies that the current net price is too high relative to the required price path. To restore the equilibrium, the current net price must fall, which means the owner must increase the current supply. The resource is extracted faster, not slower. The green paradox has reshaped how economists think about the timing of climate policy. A gradually tightening carbon tax may simply bring forward the extraction of fossil fuels, increasing near-term emissions. The policy implication is that carbon pricing must be designed to avoid this perverse incentive, either by implementing the tax immediately at a high level or by combining it with supply-side restrictions. The green paradox is a direct consequence of the Hotelling logic: resource owners are forward-looking, and their expectations of future policy affect current behaviour. This insight has profoundly influenced green macroeconomics.

Critical minerals and the energy transition provide another testing ground for the Hotelling framework. Lithium, cobalt, and rare-earth elements are essential for batteries and renewable energy technologies. Their prices spiked dramatically between 2021 and 2024 as demand for electric vehicles surged, and then fell sharply as new supply came online. The basic Hotelling Rule says that the scarcity rent on these finite resources must rise over time. The sharp price declines seem to contradict this prediction. The declines reflect exactly the forces that the extended Hotelling models identify: new discoveries that increase the resource stock, and technical change that lowers extraction costs. The rule still anchors expectations of the long-run trend. The International Energy Agency’s Global Critical Minerals Outlook 2024 uses Hotelling-style scarcity-rent calculations as a benchmark to assess whether current prices imply scarcity or abundance. The existence of backstop technologies, such as sodium-ion batteries that replace lithium, also places a ceiling on the long-run price, exactly as the theory predicts. The energy transition relies on these minerals, and the Hotelling framework provides the structure for understanding their price dynamics.

OPEC, Saudi Aramco, and the corporate valuation of reserves show the financial application of the rule. When Saudi Aramco conducted its initial public offering in 2019, the valuation hinged entirely on the present value of its proven reserves under various price paths. Investment-bank discounted cash flow models for oil and mining companies are directly Hotelling exercises. The valuator must forecast the future price path of the resource and discount the resulting revenue stream back to the present. The Hotelling Rule provides the theoretical baseline for that price path. If the net price is expected to rise at the real interest rate, the present value of the future revenue is simply the current net price multiplied by the stock. If the price path deviates from the rule, the valuation changes dramatically. The OPEC cartel complicates this picture because its members restrict output to keep prices above the competitive Hotelling level. Understanding the difference between the competitive price path and the cartel price path is essential for valuing resource companies. The Hotelling framework is the starting point for both analyses. The global oil supply dynamics are routinely analysed through this lens.

MASEconomics Explains

4 economic concepts behind the Hotelling Rule

Conclusion

The Hotelling Rule is the foundational equation of natural-resource economics: net price grows at the real interest rate, or arbitrage between holding and selling the resource breaks down. The no-arbitrage logic is inescapable, but the empirical record shows that aggregate prices rarely follow the pure rule because reserve revisions, technological progress, and demand shifts drive a wedge between theory and observation. Micro-level data from individual oil wells vindicate the rule, and it continues to anchor climate policy debates, critical minerals forecasting, and the corporate valuation of resource reserves.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.