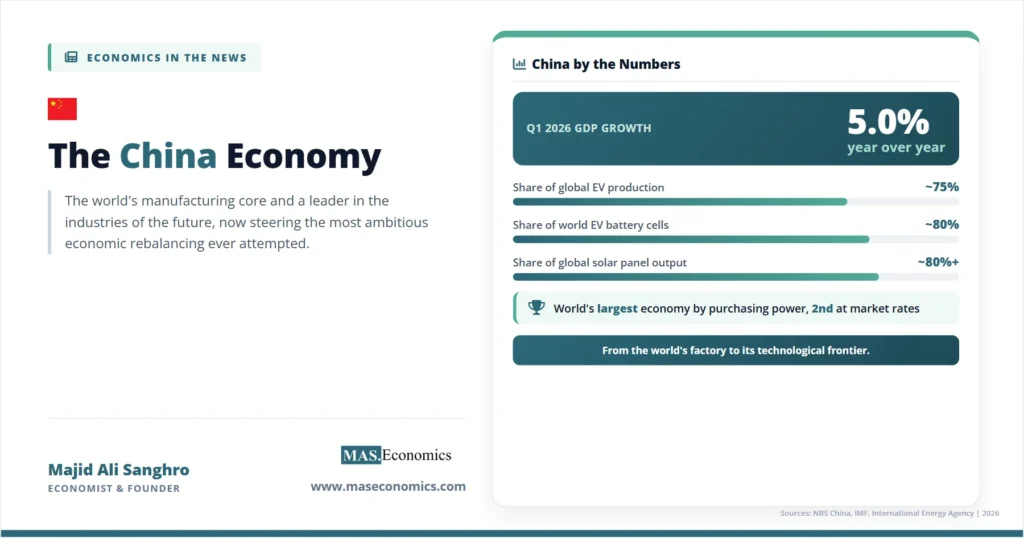

In the first quarter of 2026, China’s economy grew 5 percent from a year earlier, a pace most advanced economies can only envy, while its factories produced roughly three out of every four electric vehicles made anywhere on earth. Those two facts capture what the China economy has become: the manufacturing core of the global economy and, increasingly, the technological frontier of it. In a single generation, China moved from a poor, largely agricultural society to the world’s second-largest economy by market exchange rates and the largest by purchasing power, lifting hundreds of millions of people out of poverty in what may be the fastest sustained expansion in economic history.

China is a continental economy of about 1.41 billion people with nominal output approaching 20 trillion dollars. It is the world’s largest manufacturer, largest exporter, largest auto exporter, and the dominant producer in many of the industries that will define the coming decades, from electric vehicles and batteries to solar panels and increasingly advanced electronics. In 2026, it is also an economy in deliberate transition, shifting from the property-and-investment model that powered its rise toward one built on consumption, services, and high-technology industry. Understanding modern China means understanding both the scale of what it has achieved and the careful rebalancing its policymakers are now steering.

Reform and Global Rise

China’s transformation began with the reforms launched at the end of the 1970s, which opened the economy to private enterprise, foreign investment, and global trade. Over the following four decades, growth averaged close to 10 percent a year for long stretches, a rate that doubles the size of an economy roughly every seven to eight years. The mechanism was, in part, the classic process of catch-up growth that the Solow-Swan growth model describes: a country starting far below the technological frontier can grow rapidly by accumulating capital, moving workers from farms into factories, and absorbing technology from abroad.

What set China apart was the speed and scale at which it did this, and the way it integrated itself into global supply chains. By joining the World Trade Organization in 2001 and positioning itself as the workshop of the world, China became central to the production networks that link economies together, the structures we examine in global value chains and the digital economy. Foreign firms built factories, transferred know-how, and made China the assembly point for a vast share of global manufacturing, a process that drew heavily on the inward foreign direct investment that reform-era policy actively courted. The result reshaped the entire pattern of world trade and made China indispensable to the globalized economy.

The human dimension of this growth is its most striking achievement. Over the reform era, China lifted roughly 800 million people out of extreme poverty, the largest and fastest reduction in poverty in recorded history. A predominantly rural population became a predominantly urban one as hundreds of millions moved from the countryside to cities, and a vast middle class emerged where almost none had existed. Life expectancy, education, and living standards rose across the board. Whatever debates surround China’s model, the scale of material improvement it delivered to its people is not in dispute, and it is the proper starting point for understanding why the country approaches its next phase with confidence rather than crisis.

Resilient Q1 2026 Growth

The latest data underscores that resilience. The National Bureau of Statistics reported first-quarter 2026 GDP growth of 5 percent year over year, reversing the gentle slowing seen late in 2025 and putting the economy at the top of its 4.5 to 5 percent annual target range. Industrial output expanded 6.1 percent, accelerating from the previous quarter, and exports grew strongly, with foreign trade up around 15 percent. The economy delivered this even as the energy shock from the Middle East conflict raised input costs worldwide, a sign of the underlying momentum in China’s industrial base.

Beneath the headline, the composition told a more nuanced story. Growth leaned heavily on industry and exports, while domestic consumption recovered only modestly and youth unemployment remained elevated. Inflation was low, with consumer prices rising around 1 percent, reflecting cautious household spending rather than overheating. This is the central feature of China’s current moment: an economy whose supply side is powerful and whose demand side is still being rebuilt, a gap that policymakers are working deliberately to close, as the framework in what GDP growth tells us about economic health helps make clear.

| Indicator | Value | Source and period |

|---|---|---|

| Economy size (global rank) | 2nd (1st by PPP) | IMF, 2026 |

| Nominal GDP (2026 est.) | ~US$20.9 trillion | IMF / NBS |

| Real GDP growth (Q1 2026) | 5.0% | NBS, April 2026 |

| 2026 official growth target | 4.5%–5.0% | State Council, 2026 |

| GDP per capita | ~US$14,900 | IMF, 2026 |

| CPI inflation | ~1.0% | NBS, March 2026 |

| Share of global EV production | ~75% | IEA, 2025 |

| R&D spending (share of GDP) | 2.7%, rising to 3.2%+ | China target, 2024–2030 |

|

Sources: National Bureau of Statistics of China; IMF, World Economic Outlook (April 2026); International Energy Agency, Global EV Outlook 2026.

|

||

Manufacturing Dominance and Upgrading

China’s manufacturing position is the foundation of its economic power, and it has changed character. The country was long known for assembling goods designed elsewhere, capturing the low-value steps in a production chain while the profitable design and branding stayed abroad. That is no longer an accurate description. China now leads in entire advanced industries, designing and producing the most sophisticated products in several of the sectors that will shape the global economy for decades.

The clearest example is electric vehicles. China accounts for roughly three-quarters of the electric cars produced worldwide, six of the world’s ten largest EV makers are Chinese, and the country has become the largest auto exporter on earth, overtaking Japan and Germany. Domestic firms such as BYD compete on technology and cost rather than on cheap labor, and Chinese companies produce more than 80 percent of the world’s EV battery cells, controlling much of the supply chain from critical-mineral processing through finished packs. The story extends to solar panels, where China dominates global production, and to a fast-growing capability in robotics, advanced electronics, and artificial intelligence.

The breadth is what distinguishes China’s position from that of any single-industry exporter. The country builds and operates the world’s largest high-speed rail network, leads in commercial drones and telecommunications equipment, and has become a serious force in semiconductors despite export controls aimed at slowing its progress. In battery chemistry, firms such as CATL have pioneered fast-charging and lower-cost designs that set the global standard. Chinese technology companies are deploying artificial intelligence across manufacturing and services, and the government’s industrial strategy explicitly targets the technologies it judges decisive for the next two decades. This is the profile of an economy that has moved from imitation to innovation across a remarkably wide front, drawing on the same forces of investment, scale, and technological absorption that growth theory associates with sustained advances in productivity, a connection explored in our wider coverage of how artificial intelligence is reshaping productivity and growth.

This ascent up the value chain reflects deliberate strategy and sustained investment. China spends about 2.7 percent of GDP on research and development, with a target above 3.2 percent by 2030, and its industrial policy has concentrated resources in the technologies it judges strategic. The competitive intensity of its domestic market, where dozens of firms fight for share, drives rapid innovation and cost reduction in a way that has proven hard for rivals to match. Whether one views this through the lens of comparative advantage or of state-directed industrial policy, the outcome is the same: in a widening set of advanced industries, China is now the country others are trying to catch, a reversal of the relationship described in comparative advantage and specialization.

Rebalancing Away from Property and Investment

For most of its rise, China grew by investing: in factories, infrastructure, and above all property. Construction and real estate became enormous shares of the economy and of household wealth. That model delivered extraordinary results but eventually reached its limits, producing excess housing supply, heavy local-government debt, and an economy more dependent on building than on the spending of its own citizens. Since 2021 the property sector has been in a managed correction, with developer defaults, falling sales, and lower land revenues for local governments.

China’s policymakers have chosen to manage this transition rather than reinflate the old model. The official approach, captured in the new development model for property and in the priorities of the 15th Five-Year Plan covering 2026 to 2030, aims to turn real estate into a source of steady housing demand rather than a speculative growth engine, while raising the share of the economy driven by household consumption. The International Monetary Fund and the World Bank have both endorsed the direction and urged China to go further by strengthening social safety nets, which would reduce the precautionary saving that holds consumption down. This is a deliberate, difficult pivot toward a more balanced and sustainable growth model.

Investment-led, high savings

Local-government land revenue

Low-cost export assembly

High-technology manufacturing

Innovation and rising R&D

Advanced exports: EVs, batteries, solar

Structural Challenges

An honest profile records the headwinds alongside the strengths, because China’s policymakers themselves treat them as the central agenda. Three stand out. The first is weak domestic consumption: Chinese households save a large share of their income, partly because the social safety net for healthcare, pensions, and unemployment is thinner than in other large economies, and converting that caution into spending is the core of the rebalancing challenge. The second is the property correction, which weighs on household wealth and confidence even as authorities contain the financial risks. The third is demographics.

China’s population has begun to decline and is aging rapidly, the result of decades of low fertility, including the long one-child policy. A shrinking workforce will, over time, slow the economy’s potential growth and raise the cost of supporting retirees, the same pressures that have shaped Japan and that we examine in the silver economy and in how aging populations impact price levels. China is responding by raising the retirement age and investing in automation and robotics to offset a smaller labor force, but demographics are the one constraint that even effective policy can only soften, not remove. The IMF has noted that slowing productivity growth, an aging population, and elevated debt will weigh on medium-term growth, which is why the move toward higher-value, innovation-led industry matters so much.

Debt is the fourth challenge, and it is concentrated rather than systemic. Local governments borrowed heavily to fund infrastructure and supported themselves through land sales that have now fallen sharply, leaving many with obligations that are hard to service. Beijing has begun swapping local debt into longer-dated, lower-cost forms to ease the refinancing pressure, a managed approach that contains the risk without a disorderly reckoning. The advantage China holds is that most of this debt is owed domestically and the central government’s own balance sheet is comparatively strong, giving it room to support the transition. The task is to deleverage the riskier pockets of the system while keeping credit flowing to the productive parts of the economy, a balance that requires the financial reforms now underway to proceed steadily rather than abruptly.

What ties these challenges together is that they are the predictable costs of a successful transition, not signs of failure. An economy completing its catch-up phase naturally sees growth moderate as it approaches the technological frontier and can no longer rely on cheap labor and capital accumulation alone. Rebalancing toward consumption, absorbing a property correction, and adapting to an older population are the problems of a country that has already become wealthy, not a poor one. China’s policymakers have framed the agenda in exactly these terms, prioritizing the quality and durability of growth over the headline rate, which is why the official targets have eased from the double-digit pace of earlier decades to a more sustainable middle single-digit range.

China in the Global Trading System

China’s scale makes its economic choices everyone’s concern. It is the largest trading partner of most countries in the world, the dominant supplier in critical supply chains, and the engine of demand for commodity exporters from Australia to Brazil. That centrality is also the source of friction. The tariff conflict of 2025 and 2026 placed steep duties on Chinese goods in the United States and prompted restrictions elsewhere, while China responded by tightening control over exports of critical minerals and battery technologies where it holds a commanding position. We trace the wider consequences of this in our account of the global tariff war of 2025–2026.

China’s strategic response has been to diversify. Facing tariffs in Western markets, Chinese manufacturers have expanded aggressively into Southeast Asia, Latin America, the Middle East, and beyond, and have built production facilities abroad to serve markets directly. More than half of electric cars sold outside Europe and the United States in 2025 were Chinese brands. This global expansion, carried out by increasingly sophisticated multinational corporations of Chinese origin, marks a new phase: China is no longer only the world’s factory but the home base of firms competing at the technological frontier across the globe. The relationship with the United States, the world’s other economic superpower, sits at the center of this, and the contrast between the two systems is visible in our profile of the US economy.

Renminbi and Financial System Transition

China’s currency, the renminbi, occupies an unusual place in the global system. China manages its exchange rate more actively than most large economies, allowing the renminbi to trade within a guided range rather than floating freely, which gives policymakers a tool for supporting exporters and managing capital flows. As the Federal Reserve held US rates high through 2026 to fight inflation, the resulting interest-rate gap put downward pressure on the renminbi, the same force acting on most currencies against a strong dollar. The way exchange rates respond to such differentials and to underlying price levels over time is the territory of purchasing power parity, and on that measure the renminbi remains some distance from full convertibility and from the international role its economy’s size might suggest.

Beijing has long sought to raise the renminbi’s standing in global trade and finance, encouraging its use in cross-border settlement and in lending to partner countries. Progress has been real but gradual, constrained by the capital controls that China maintains to preserve financial stability. The domestic financial system, dominated by large state banks, has been central to managing the property correction, extending credit to stabilize developers and absorbing strains that in a more market-driven system might have produced a sharper crisis. The World Bank and IMF have argued that deeper, more transparent capital markets and a stronger role for non-bank institutions such as pension and insurance funds would improve the allocation of capital and support the shift toward consumption. Reforming the financial system without destabilizing it is one more balance China must strike as it modernizes an economy of its scale.

Outlook for 2026

The near-term outlook is for solid if gradually moderating growth. China met its 5 percent target in 2025 and started 2026 at the same pace, and most external forecasters expect full-year growth in the mid-4 percent range as the property drag continues and export growth normalizes. The energy shock from the Middle East raises input costs and complicates the picture, but as a large and diversified economy, China is better placed to absorb it than most, a contrast with the oil-importing strains examined in our analysis of the 2026 Iran oil shock. Expansionary fiscal policy and monetary easing are supporting demand while the rebalancing proceeds.

The longer view is what matters most. China is attempting something no economy of its size has done: to shift from investment-led catch-up growth to innovation-and-consumption-led mature growth, while managing a property correction, an aging population, and an increasingly contested global trading environment, all at once. The achievements are real, and the strengths are durable: a manufacturing base without rival, leadership in the industries of the future, a vast and improving capacity for innovation, and policymakers who understand the transition they must make. The development China has delivered over four decades is among the most consequential economic stories of the modern era, and how it manages the next phase will shape not only its own prosperity but the structure of the entire global economy.

Conclusion

The China economy in 2026 is the story of a development success now entering a new and more complex chapter. Four decades of reform turned a poor agricultural society into the world’s manufacturing core and its leader in the industries that will define the coming decades, from electric vehicles and batteries to solar power and advanced electronics. First-quarter growth of 5 percent, an industrial base producing three-quarters of the world’s electric cars, and rising investment in research and innovation all testify to an economy whose strengths are formidable and whose ascent up the value chain is far from finished.

The task now is transition. China is deliberately shifting from a model built on property and investment toward one led by consumption, services, and high technology, while managing the property correction, a thinner social safety net, and a population that has begun to age and shrink. These are real challenges, and China’s policymakers have placed them at the center of the agenda rather than denying them. The country retains the manufacturing scale, the technological momentum, and the policy capacity that carried it this far. Whether it can complete the most ambitious economic rebalancing ever attempted at this scale is the defining question of the China economy, and the answer will shape the global economy for a generation.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics