The Balassa-Samuelson effect explains the empirical regularity that consumer prices are systematically higher in richer countries by tracing the mechanism through which faster productivity growth in tradable sectors raises wages economy-wide, lifting non-tradable prices and the real exchange rate. This framework, independently developed by Béla Balassa and Paul Samuelson in 1964, provides the dominant theoretical explanation for the “Penn effect,” the observation that price levels rise with income across nations. A haircut, a restaurant meal, or a taxi ride costs four to six times more in Switzerland than in India, even after converting currencies at market rates. The purchasing power parity doctrine struggles with this fact, but the Balassa-Samuelson mechanism explains it as the logical outcome of differential productivity growth across sectors.

What the Balassa-Samuelson Effect Means

The starting point is a striking empirical pattern known as the Penn effect, named after the Penn World Table project that documented it comprehensively. When economists compare price levels across countries, they find that richer nations systematically have higher price levels than poorer ones. A basket of goods and services that costs 100 dollars in the United States might cost only 40 dollars in India or 30 dollars in Ethiopia, after converting at market exchange rates. This pattern is not a minor statistical quirk; it is one of the most robust empirical regularities in international economics.

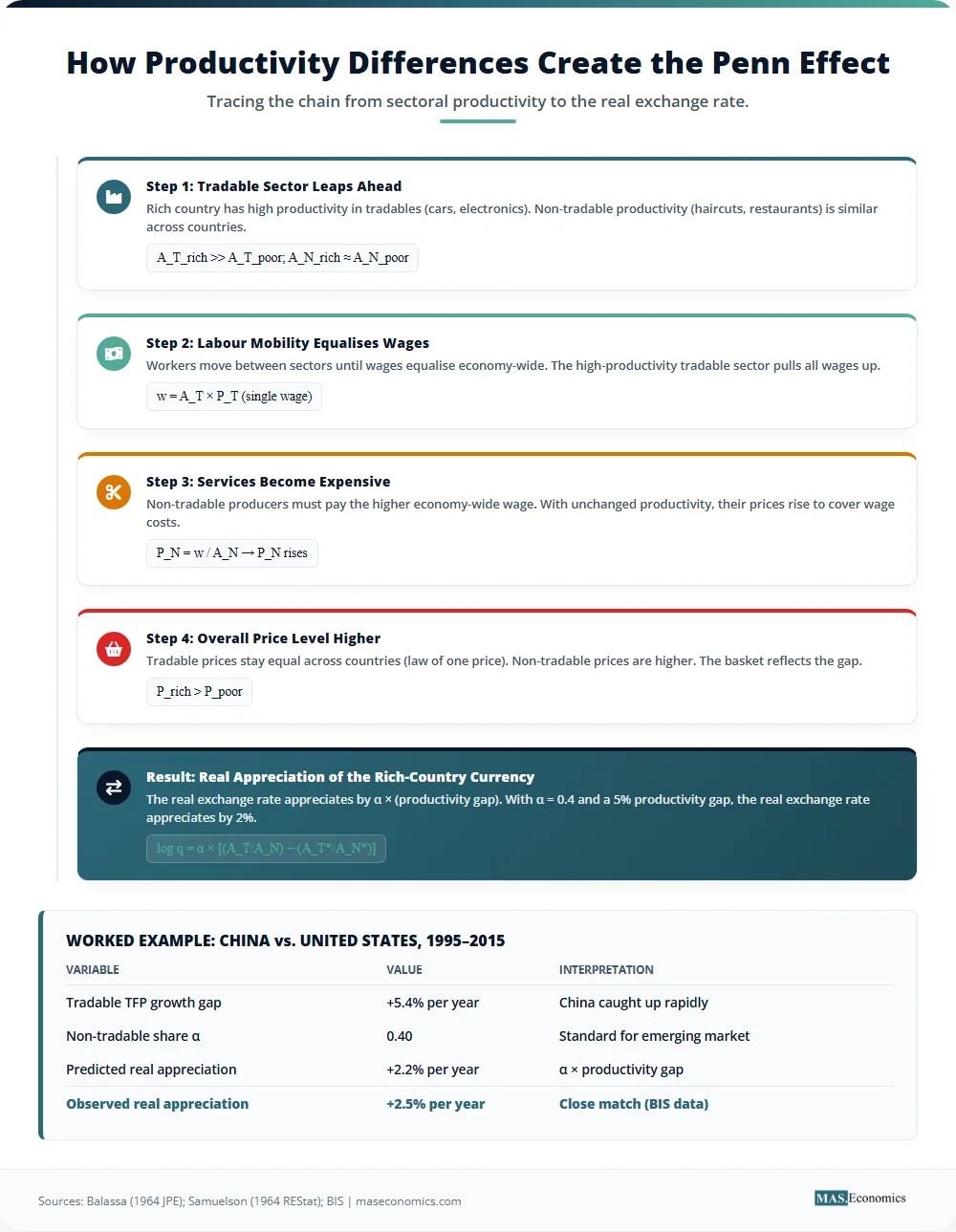

Balassa (1964) and Samuelson (1964), building on an earlier insight by Harrod (1933), provided the explanation. The mechanism rests on the distinction between tradable and non-tradable goods. Tradeable goods, such as cars, electronics, and raw materials, face international price arbitrage. If a car costs less in Germany than in the United States, traders will buy in Germany and sell in the United States until the prices converge, adjusted for transport costs and tariffs. This convergence is the law of one price, and it implies that exchange rates between countries roughly equalise the prices of tradable goods.

Non-tradable goods, such as haircuts, restaurant meals, and real estate, cannot be arbitraged across borders. A barber in Mumbai cannot cut the hair of a client in Manhattan. Because non-tradables do not face international competition, their prices are determined domestically. The key insight is that non-tradables are highly labour-intensive. When a country experiences rapid productivity growth in its tradable sector, perhaps through industrialisation or technological adoption, firms in that sector can afford to pay higher wages to attract workers. Because labour is mobile between sectors within a country, wages in the non-tradable sector must rise to match those in the tradable sector; otherwise, non-tradable firms would lose all their workers.

However, productivity growth in non-tradable sectors tends to be sluggish. A haircut takes roughly the same time in Zurich as it does in Karachi. When non-tradable firms face higher wages but cannot produce output any faster, their unit labour costs rise. To cover these higher costs, they must charge higher prices. The result is that non-tradable prices in rich countries are much higher than in poor countries, while tradable prices are roughly similar. Because non-tradables constitute a large share of the consumption basket, the overall price level in rich countries is higher. This is the Balassa-Samuelson effect, sometimes called the Harrod-Balassa-Samuelson effect to acknowledge Harrod’s earlier anticipation of the logic.

Balassa-Samuelson Effect in Equations

The Balassa-Samuelson model formalises this intuition through a two-sector production framework. The derivation proceeds step-by-step to show exactly how productivity differences translate into price level differences.

Two-Sector Production

Consider a small open economy that produces two types of goods: tradables (T) and non-tradables (N). Each sector uses only labour with sector-specific productivity:

where \(A_T\) and \(A_N\) are productivity parameters, and \(L_T\) and \(L_N\) are labour inputs. Under perfect competition and constant returns to scale, prices equal unit labour costs in each sector:

where \(w\) is the economy-wide nominal wage and \(P_T\) and \(P_N\) are the prices of tradables and non-tradables.

Labour Mobility and Wage Equalisation

Labour is assumed to be perfectly mobile between sectors. Workers move to whichever sector offers a higher wage, equalising wages across the economy. This single wage \(w\) connects the two sectors, ensuring that productivity gains in one sector affect costs in the other.

Law of One Price for Tradables

For tradable goods, the law of one price holds through international arbitrage:

where \(e\) is the nominal exchange rate (domestic currency per foreign currency) and \(P_T^*\) is the foreign price of tradables. Combining the price-setting equation for tradables with the law of one price pins down the domestic wage:

The wage is determined entirely by tradable productivity, the exchange rate, and the foreign tradable price. This is a key result: improvements in tradable productivity directly raise the economy-wide wage.

Deriving Non-Tradable Prices from the Wage

Substitute the wage equation into the non-tradable price equation. Since \(P_N = w / A_N\) and \(w = A_T \cdot e \cdot P_T^*\), we obtain:

The non-tradable price depends on the ratio of tradable to non-tradable productivity, the exchange rate, and the foreign tradable price. When tradable productivity \(A_T\) rises relative to non-tradable productivity \(A_N\), non-tradable prices increase proportionally.

Relative Non-Tradable Price

Dividing the non-tradable price by the tradable price yields the relative price of non-tradables:

The relative price of non-tradables depends solely on the ratio of tradable to non-tradable productivity. If tradable productivity grows faster than non-tradable productivity, non-tradables become relatively more expensive.

Aggregate Price Level and Log Transformation

The aggregate price level is a geometric weighted average of tradable and non-tradable prices, where \(\alpha\) is the share of non-tradables in the consumption basket:

Taking the natural logarithm of both sides:

Substitute the expression for \(\ln P_N\) using the relative price relationship \(\ln P_N = \ln P_T + \ln(A_T/A_N)\):

The aggregate price level equals the tradable price level plus a premium that depends on the productivity gap and the non-tradable share.

Real Exchange Rate Derivation

The real exchange rate \(q\) is defined as the ratio of foreign to domestic price levels, converted at the nominal exchange rate:

Taking logs and substituting the expressions for domestic and foreign price levels (where the foreign economy has analogous variables \(A_T^*\), \(A_N^*\), and \(\alpha^*\)):

Since the law of one price ensures \(P_T = e \cdot P_T^*\), the tradable price terms cancel, yielding:

assuming equal non-tradable shares \(\alpha = \alpha^*\). A 1 percent rise in domestic relative tradable productivity (\(A_T / A_N\)) appreciates the real exchange rate by \(\alpha\) percent. With \(\alpha \approx 0.4\), the elasticity is around 0.4. This is the central quantitative prediction of the Cobb-Douglas production based model. While the Dornbusch model focuses on short-run nominal dynamics, Balassa-Samuelson explains the long-run trend.

Empirical Regression Form

Because cross-country productivity data is difficult to obtain, researchers often substitute real GDP per capita as a proxy for tradable productivity, yielding the empirical Penn-Balassa-Samuelson regression:

Cross-country estimates of \(\beta_1\) typically range between 0.2 and 0.4, confirming that a 1 percent increase in income per capita is associated with a 0.2 to 0.4 percent increase in the price level.

Key Assumptions and Limitations

The Balassa-Samuelson model relies on four key assumptions. First, labour is fully mobile across sectors, ensuring wage equalisation. Second, the law of one price holds for tradable goods. Third, productivity differences between rich and poor countries are concentrated in the tradable sector. Fourth, capital is either internationally mobile or sector-specific in standardised ways that do not distort the basic wage mechanism.

Several important limitations challenge these assumptions. First, the Bhagwati-Kravis-Lipsey alternative argues that poor countries have lower non-tradable prices because of labour endowment differences rather than productivity differences, a concept related to the Heckscher-Ohlin framework. Poor countries are abundantly endowed with labour, making labour-intensive non-tradable services cheap. This factor-endowment explanation competes with the productivity-driven Balassa-Samuelson story, though the two mechanisms are not mutually exclusive.

Second, Rogoff (1996) highlighted the purchasing power parity puzzle: the half-life of real exchange rate deviations is three to five years, which is too long for a productivity-driven story alone to explain. If the Balassa-Samuelson effect were the sole driver, real exchange rates should adjust gradually as productivity converges, but the observed persistence and volatility of real exchange rates suggest other factors, such as nominal rigidities and financial shocks, play important roles.

Third, tradable productivity is difficult to measure separately from non-tradable productivity, especially in developing countries where sectoral data is noisy. Measurement error can bias estimates of the productivity-price level relationship.

Fourth, the model fails in time-series tests for high-income countries with floating exchange rates. Engel (1999) showed that virtually all the variation in real exchange rates among advanced economies comes from movements in the relative price of tradables, not non-tradables, contradicting the Balassa-Samuelson prediction that non-tradable prices drive real exchange rate movements.

Fifth, the model ignores demand-side factors. Bergstrand (1991) argued that as countries grow richer, demand shifts toward services, pushing up non-tradable prices through demand pressure rather than wage cost-push. This income-elastic demand channel provides an alternative explanation for the Penn effect.

Sixth, recent NBER work by Berka and Devereux (2014) and Engel (2014) finds the effect is strongest at very long horizons or across large income gaps, but weak at the high-income margin where productivity differentials are small and demand-side factors dominate.

Empirical Evidence for the Balassa-Samuelson Effect

The empirical literature on the Balassa-Samuelson effect is vast, spanning cross-sectional studies, panel data analyses, and time-series investigations. Balassa (1964) and Samuelson (1964) provided the original empirical documentation, showing strong positive correlations between income levels and price levels across countries.

Heston, Nuxoll, and Summers (1994) confirmed the pattern using Penn World Table data, establishing the Penn effect as one of the most robust stylised facts in international comparisons. Asea and Mendoza (1994) provided a general-equilibrium appraisal, finding that productivity differentials explain a substantial fraction of cross-country price variation, though not all of it.

MacDonald and Ricci (2001), in an IMF Working Paper, extended the analysis to the distribution sector. They used panel data for OECD countries spanning 1970 to 1996, estimating the effect of productivity in the distribution sector on the real exchange rate. Their innovation was recognising that the retail price of a tradable good includes a significant non-tradable margin: the cost of transporting, storing, and selling the product. A country with inefficient distribution systems effectively has higher non-tradable costs embedded in the final price of tradable goods, raising the aggregate price level independently of the traditional Balassa-Samuelson channel. Their results showed that distribution sector productivity is statistically significant and economically meaningful, adding an important refinement to the standard framework.

The BIS Working Paper 143 by Mihaljek and Klau examined Central European convergence with the euro area. Their analysis found that productivity catch-up in the tradable sectors of countries like Slovakia, Poland, and the Czech Republic explained 2 to 4 percentage points of the inflation differential with the euro area. This finding has direct policy implications for the European Central Bank, which must distinguish between Balassa-Samuelson inflation, which reflects real convergence, and demand-driven inflation, which requires a monetary policy response.

Berka, Devereux, and Engel (2018), in an American Economic Review paper, examined real exchange rate dynamics within the Eurozone. Their analysis exploited a unique advantage of the Eurozone: because member countries share a common currency, nominal exchange rate movements cannot confound the analysis. Changes in the real exchange rate within the Eurozone come exclusively from changes in relative price levels, eliminating the noise that plagues studies of countries with floating exchange rates. Using sectoral price indices for Eurozone countries from 1995 to 2015, they constructed measures of tradable and non-tradable productivity and tested whether productivity differentials predicted real exchange rate movements. Their results strongly supported the Balassa-Samuelson mechanism: countries with faster tradable productivity growth experienced higher non-tradable inflation and real exchange rate appreciation, exactly as the theory predicts. The Eurozone common-currency setting provided the cleanest test yet of the framework, and the theory passed.

CEPII Working Paper 2019-11 offered guidance on measurement issues, showing that the choice of deflators, the definition of tradable versus non-tradable sectors, and the treatment of quality differences all affect the estimated magnitude of the effect. Despite these measurement challenges, the cross-sectional relationship between income and prices remains robust.

Sources: Penn World Table 11.0; World Bank ICP 2024.

| Country | Period | Tradable TFP Growth Diff. (%/yr) | Predicted RER Appreciation (%/yr) | Observed RER Appreciation (%/yr) | Source |

|---|---|---|---|---|---|

| Japan | 1973–1990 | +2.1 | +0.8 | +1.1 | OECD STAN |

| South Korea | 1990–2010 | +3.5 | +1.4 | +1.6 | OECD STAN |

| China | 1995–2015 | +5.4 | +2.2 | +2.5 | BIS / PBoC |

| Poland | 2004–2020 | +2.4 | +0.8 | +0.8 | Eurostat / NBP |

| Slovakia | 2004–2020 | +3.0 | +1.2 | +1.4 | Eurostat / NBS |

| India | 2000–2020 | +2.7 | +1.1 | +0.4 | World Bank WDI |

|

|||||

How the Balassa-Samuelson Effect Matters

The Balassa-Samuelson effect is more than an academic explanation for a statistical pattern; it shapes how policymakers, international organisations, and businesses interpret price levels, exchange rates, and external balance.

First, Eurozone convergence and inflation differentials are directly governed by the Balassa-Samuelson mechanism. Central and Eastern European member states, including Slovakia, Estonia, Slovenia, the Czech Republic, and Poland, have run inflation 1 to 3 percentage points above the German rate as their tradable productivity catches up. The ECB explicitly distinguishes Balassa-Samuelson inflation from “harmful” demand-driven inflation in its monetary policy assessments. When Slovak inflation runs above the Eurozone average, part of the gap reflects real convergence through the Balassa-Samuelson channel, not overheating. This distinction matters for interest rate setting: tightening policy to suppress Balassa-Samuelson inflation would choke off legitimate convergence. The cross-country inflation differences within the currency union are a feature of integration, not a policy failure.

Second, China’s real exchange rate appreciation between 1995 and 2015 illustrates the Balassa-Samuelson mechanism on a grand scale. Before 2005, the Renminbi was pegged at 8.28 to the US dollar, suppressing the real exchange rate adjustment that productivity growth would normally produce. The July 2005 revaluation, which moved China to a managed float, allowed the currency to begin appreciating. Over the next decade, the RMB appreciated roughly 50 percent in real terms against the dollar, much of it consistent with rapid tradable productivity growth as China industrialised and integrated into global supply chains. The Solow-Swan growth model predicts this productivity catch-up, and Balassa-Samuelson explains its price-level consequences. The IMF, the Bank for International Settlements, and the US Treasury Department have used Balassa-Samuelson adjustments in their currency-undervaluation assessments, a process complicated by the Mundell trilemma facing managed float regimes. Without accounting for the Balassa-Samuelson effect, analysts would overestimate the degree of Chinese currency undervaluation, because a country with rapidly growing tradable productivity should experience real appreciation.

Third, IMF surveillance and the External Balance Assessment (EBA) model incorporate the Balassa-Samuelson effect. The IMF’s EBA methodology adjusts equilibrium real exchange rates for productivity differentials, rooted in the Balassa-Samuelson framework. When the IMF assesses whether a country’s exchange rate is misaligned, it calculates a “norm” real exchange rate that accounts for the country’s income level and productivity trajectory. Without this adjustment, fast-growing emerging markets would always appear to have undervalued currencies, because their price levels are lower than those of advanced economies.

Fourth, PPP-based GDP comparisons depend critically on the Penn effect. The World Bank’s International Comparison Program calculations explicitly account for the Balassa-Samuelson mechanism when computing real GDP across countries. If one compared GDP using market exchange rates without adjustment, poor countries would appear even poorer than they are, because their low non-tradable prices depress the market-exchange-rate conversion. The ICP uses purchasing power parity conversion factors that reflect the lower price of non-tradables in poor countries, yielding more accurate comparisons of living standards.

Fifth, convergence economics in EU enlargement relies on the Balassa-Samuelson framework. Romania, Bulgaria, and Croatia are on transition paths toward euro adoption. Their productivity catch-up will generate Balassa-Samuelson inflation, creating tensions within the Eurozone as their price levels converge toward the core. The Maastricht criteria require candidate countries to maintain inflation within 1.5 percentage points of the three best-performing EU members. Balassa-Samuelson inflation makes this criterion harder to meet: a country with 2 percent Balassa-Samuelson inflation must run demand-driven inflation below zero to satisfy the Maastricht target, which may require excessively tight monetary policy that slows real convergence. Understanding this mechanism is essential for managing the enlargement process without causing either excessive inflation in the catching-up countries or inappropriate monetary tightening by the ECB.

Sixth, Australian and Canadian “two-speed economy” debates invoke Balassa-Samuelson logic. During commodity booms, the resource sector (a tradable sector) experiences high productivity and profitability, driving up wages economy-wide. Non-tradable sectors, including construction and services, face higher wage bills without corresponding productivity gains, pushing up non-tradable prices and the real exchange rate. This appreciation squeezes the manufacturing tradable sector, a phenomenon related to “Dutch disease,” impacting the international monetary system dynamics for commodity-exporting nations. The Bank of Canada and the Reserve Bank of Australia reference Balassa-Samuelson logic when commenting on resource-driven appreciation and its impact on manufacturing competitiveness.

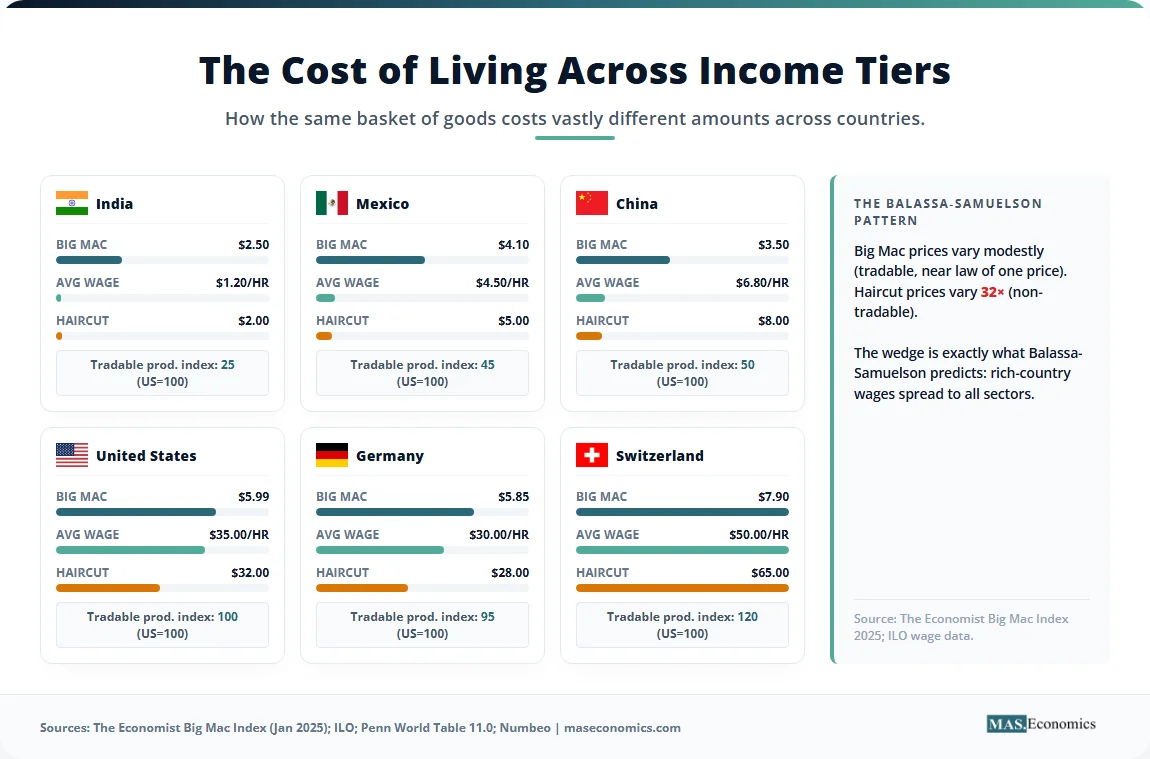

Seventh, the famous Big Mac Index published by The Economist is essentially a one-good Balassa-Samuelson test. The Big Mac is a standardised product sold in over 100 countries, but its price includes both tradable components (beef, bread, sesame seeds) and non-tradable components (rent, labour, local utilities). The tradable ingredients face international price convergence, so their costs are roughly similar everywhere. The non-tradable costs, particularly labour, vary enormously across countries. When the index shows that a Big Mac costs half as much in India as in the United States, the difference largely reflects the non-tradable cost wedge that Balassa-Samuelson formalises. The Economist separates ingredient costs from labour costs implicitly, showing that the local wage component drives the cross-country price variation.

Eighth, cost-of-living adjustments for international assignments rely on Balassa-Samuelson logic. Multinational HR departments use purchasing power parity calculations to set expatriate compensation, recognising that the cost of non-tradable services is systematically higher in high-income countries. An engineer transferred from Mumbai to Zurich requires a significant cost-of-living adjustment, not because tradable goods are more expensive, but because housing, healthcare, and personal services cost far more in the high-productivity Swiss economy.

Ninth, central bank inflation targets in catch-up economies must account for the Balassa-Samuelson contribution. Eastern European central banks, including the National Bank of Poland and the Czech National Bank, have considered targeting headline inflation excluding the Balassa-Samuelson contribution. Because productivity catch-up generates inflation that is both inevitable and benign, targeting a headline inflation rate that includes this component may lead to unnecessarily restrictive policy. Adjusting the target for the Balassa-Samuelson effect allows monetary policy to remain accommodative during the convergence process, supporting real growth without sacrificing price stability.

MASEconomics Explains

4 economic concepts behind the Balassa-Samuelson effect

Conclusion

Balassa-Samuelson effect theory explains why a productivity differential between tradable and non-tradable sectors generates the systematic price-income relationship observed across countries. The model has held up well in long-run cross-section data, where the Penn effect is one of the most robust empirical regularities in economics. However, it performs poorly in high-frequency time-series applications for advanced economies, where nominal exchange rate movements and demand-side factors dominate. The framework remains the standard lens in IMF surveillance, Eurozone convergence economics, and international price comparisons, providing the essential adjustment that prevents fast-growing economies from appearing to have systematically undervalued currencies.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.