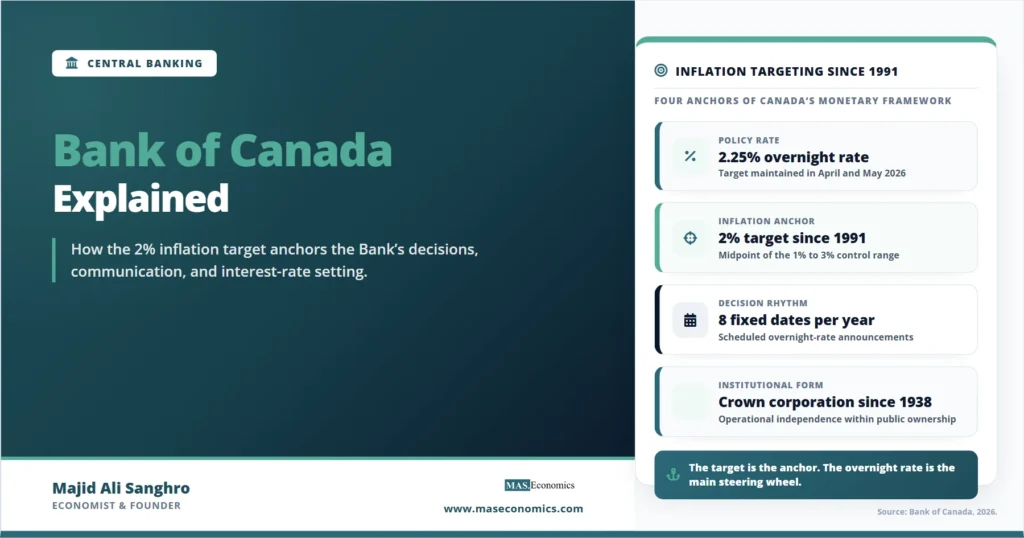

The Bank of Canada held its target for the overnight rate at 2.25% on April 29, 2026, with the Bank Rate at 2.50% and the deposit rate at 2.20%. The decision marked the sixth consecutive hold since the rate settled in October 2025, closing one of the most consequential easing cycles in the institution’s modern history. Between the summer of 2024 and late 2025, the Governing Council delivered nine consecutive cuts that brought the policy rate down from a peak of 5%, a level it had reached after the fastest tightening sequence Canada had seen in a generation.

That rate path is set by an institution most Canadians rarely think about until their mortgage renews. The Bank of Canada is the country’s central bank, created by an Act of Parliament that received royal assent in 1934 and opened its doors in 1935. It does not take deposits or issue personal accounts. Instead, it sets the price of overnight money, issues the physical currency, manages the federal government’s debt and foreign reserves, and acts as the ultimate backstop for the financial system. Its single most important commitment, the one that organizes almost everything else it does, is a number agreed jointly with the federal government in 1991: keep inflation near 2%.

This profile covers the Bank’s mandate, its 1991 inflation-targeting framework, its governance through the Governing Council, its policy toolkit, and the major episodes that shaped it. It is the evergreen reference that supports our news coverage of Bank of Canada rate decisions, Canadian inflation prints, and the broader Canadian economy.

Mandate and Core Functions

The legal mandate of the Bank of Canada is unusually compact. The preamble to the Bank of Canada Act has not changed since 1934, and it still states that the Bank exists to regulate credit and currency in the best interests of the economic life of the nation. There is no statutory dual mandate of the kind written into United States law, and no numerical inflation target embedded in the statute itself. The 2% target lives in a separate joint agreement with the government rather than in the founding legislation, which gives the framework flexibility but also makes it a matter of renewable agreement rather than permanent law.

Around that core monetary responsibility sit four operational functions. The Bank is the sole issuer of Canadian banknotes, designing and producing the physical currency in circulation. It acts as the fiscal agent for the federal government, managing the issuance and servicing of Government of Canada debt and administering the country’s foreign exchange reserves. It promotes the stability and efficiency of the financial system, including oversight of systemically important payment and clearing systems. And it serves as the lender of last resort, supplying emergency liquidity to solvent institutions during periods of stress. These roles are not unique to Canada; they are the standard architecture of a modern central bank, explored in our companion piece on what central banks actually do.

What distinguishes the Bank is the clarity with which it has subordinated these functions to a single, communicated objective. Where the Federal Reserve weighs employment and prices as co-equal goals, the Bank of Canada treats low and stable inflation as the best contribution monetary policy can make to economic welfare, including a strong labour market. Employment enters the framework, but as a consideration within the flexible pursuit of the inflation target rather than as a separate mandate of equal standing.

The 1991 Agreement That Defined the Institution

For most of its first half-century, the Bank of Canada had no explicit nominal anchor. Through the 1970s and early 1980s it experimented with monetary aggregate targeting, an approach that broke down as the relationship between money growth and inflation became unstable. By the late 1980s, Governor John Crow had concluded that the Bank needed an explicit, communicable commitment to price stability, a view he set out publicly in early 1988.

The turning point came in February 1991. Acting on a shared concern about the economic damage from high inflation, then running near 5%, Governor Crow and Minister of Finance Michael Wilson announced a set of formal inflation-reduction targets in a joint press release issued alongside the federal budget. Canada became the second country in the world, after New Zealand, to adopt inflation targeting as the organizing principle of monetary policy. The initial path set a target of 3% for the end of 1992, declining to 2% by the end of 1995, with a band of one percentage point on either side. Inflation fell faster than the schedule required, reaching close to 2% by January 1992.

Two features of the 1991 design still matter. The first is that the framework was a partnership announced jointly by the government and the Bank, not a unilateral central bank policy and not a piece of legislation. That gives the target democratic legitimacy while preserving the Bank’s operational independence over how to hit it. The second is the renewal mechanism. The agreement is reviewed and renewed every five years, which forces a periodic, evidence-based re-examination of the target rather than treating 2% as permanent doctrine. The framework has been renewed several times since, most recently in December 2021, and that agreement runs to the end of 2026. The current review is therefore live, the first since the post-pandemic inflation surge tested the framework under real strain.

The target is defined precisely. It aims to keep total consumer price index inflation at the 2% midpoint of a 1% to 3% control range over the medium term, with policy calibrated to return inflation to target over a horizon of roughly six to eight quarters, the lag the Bank estimates for its actions to work through the economy. That medium-term horizon is the reason the Bank looks through temporary price shocks, a discipline that connects directly to the logic of inflation targeting as a policy framework and to the broader role of monetary anchors in shaping expectations.

Governing Council Decision Process

Monetary policy at the Bank of Canada is made by the Governing Council, and its decision process differs sharply from the recorded majority votes of the Federal Open Market Committee. The Council consists of the Governor, the Senior Deputy Governor, and the Deputy Governors. As of 2026, Tiff Macklem serves as Governor, a post he has held since June 2020, with Carolyn Rogers as Senior Deputy Governor. The Council reaches its decisions by consensus rather than by a tally of individual votes, and it does not publish a dissent record. This consensus model means the institution speaks with a single voice, which strengthens the clarity of its communication but offers outside observers less visibility into internal disagreement than the American dot plot or the published vote splits of the Bank of England.

The Governor sits at the apex of the structure. Under the Bank of Canada Act, the Governor is the chief executive officer and chairs the Board of Directors. The appointment is made by the Bank’s own Board of Directors with the approval of the federal Cabinet, for a renewable term of seven years, a design intended to insulate the role from the electoral cycle. The Board of Directors, whose outside members are appointed by the Governor in Council, oversees the Bank’s administration and finances but does not set monetary policy; that authority rests with the Governing Council.

Policy rate decisions are announced on eight fixed dates each year, a predictable schedule that removes guesswork about timing. Four of those announcements are accompanied by the Monetary Policy Report, the Bank’s quarterly publication of its base-case projections for growth and inflation and its assessment of the risks around them. The Governor and Senior Deputy Governor hold a press conference on Report dates, and the Bank also publishes a summary of the Council’s deliberations, its closest equivalent to meeting minutes.

The relationship with the federal government is governed by an unusual safeguard known as the directive power. The Bank operates with day-to-day independence, but the law provides that if an irreconcilable conflict arises between the Governor and the Minister of Finance over monetary policy, the Minister may issue a written, public directive instructing the Bank on the policy to follow. The Governor must then either comply or resign. The directive has never been used. Its existence resolves the question of ultimate accountability in a democracy while making any government intervention so visible and so politically costly that the threat alone preserves the Bank’s practical autonomy. This balance between independence and accountability is the central tension explored in our piece on central bank independence.

The Overnight Rate and the Rest of the Toolkit

The Bank’s primary instrument is the target for the overnight rate, the interest rate at which major financial institutions borrow and lend one-day funds among themselves. Changes in this single rate ripple outward into the prime rate, mortgage rates, business lending, and bond yields, the chain of effects described in our explainer on how monetary policy transmits through the economy. The Bank keeps the actual overnight rate close to its target by operating a corridor: the Bank Rate, currently 2.50%, sets the ceiling at which the Bank lends to financial institutions, and the deposit rate, currently 2.20%, sets the floor at which it pays interest on settlement balances. The target rate sits between them, currently at 2.25%.

Beyond the policy rate, the Bank holds a wider set of tools that come into use mainly during stress. The table below summarizes the main instruments and how each is deployed.

| Tool | What It Does | Typical Use |

|---|---|---|

| Target for the overnight rate | Sets the benchmark policy rate that anchors short-term borrowing costs | Standard policy decision on eight fixed dates each year |

| Operating band (Bank Rate and deposit rate) | Ceiling and floor that keep the market overnight rate near target | Used continuously to implement the rate decision |

| Open market and repo operations | Adjusts settlement balances and overnight funding conditions | Day-to-day management of liquidity and the overnight rate |

| Quantitative easing | Large-scale purchases of Government of Canada bonds to lower long-term rates | Crisis response when the policy rate is near its lower bound |

| Quantitative tightening | Letting bond holdings roll off at maturity to shrink the balance sheet | Post-crisis normalization after a period of easing |

| Forward guidance | Communication about the likely future path of the policy rate | Shapes expectations, especially when the rate is constrained |

| Emergency liquidity facilities | Lending to solvent institutions against collateral during stress | Lender-of-last-resort support in a financial crisis |

|

Source: Bank of Canada, monetary policy and market operations documentation, 2026.

|

||

The asset-purchase tools are recent additions to the Canadian toolkit. The Bank used quantitative easing on a large scale only once, during the pandemic, buying Government of Canada bonds to support market functioning and ease financial conditions when the policy rate was effectively at its floor. It ended those purchases in October 2021 and began quantitative tightening in April 2022, letting maturing bonds roll off without replacement. Canada moved through balance-sheet normalization faster than most peers, helped by a smaller balance sheet relative to the size of its economy and a shorter average maturity on its holdings, and the Bank announced the end of quantitative tightening in early 2025, returning to a routine framework for managing its balance sheet.

From Volcker’s Shadow to the Pandemic Surge

The Bank of Canada has been shaped by the same global forces that defined every major central bank in the modern era, but its responses carry a distinctly Canadian stamp.

The first defining episode was the inflation of the 1970s and the disinflation that followed. Canada, like the United States and much of the advanced world, allowed inflation to climb into double digits during that decade, and the credibility cost of letting it persist drove the eventual move toward an explicit anchor. The lessons of that period, examined in our piece comparing the Great Inflation across countries, are the direct intellectual ancestor of the 1991 framework. The painful trade-off between inflation and unemployment that the era exposed is the same mechanism described by the Phillips Curve, and managing that trade-off credibly is precisely what inflation targeting was designed to do.

The second was the 2008 global financial crisis. Canada entered the crisis with a conservative, well-capitalized banking system, and no Canadian bank failed or required a direct government bailout, an outcome often cited as evidence of the strength of Canadian financial regulation. The Bank’s role was as a liquidity provider rather than a rescuer of insolvent institutions, the textbook function of a lender of last resort. It cut the policy rate aggressively and supplied emergency liquidity, but it did not need the alphabet soup of facilities that the Federal Reserve deployed.

The third and most testing episode was the pandemic and its inflationary aftermath. In March 2020, the Bank cut the policy rate to 0.25%, its effective lower bound, and launched its first large-scale bond-buying program. As supply chains broke, commodity prices climbed, and pandemic-era stimulus met pent-up demand, inflation rose to multi-decade highs, peaking above 8% in 2022. The Bank responded with the fastest tightening cycle in its modern history, raising the overnight rate from 0.25% to 5% between March 2022 and mid-2023, then holding it there into early 2024 while inflation cooled. As inflation returned toward target, the Bank began cutting in the summer of 2024, delivering nine reductions that brought the rate to 2.25% by October 2025. The chart below traces that path.

The Pressures Shaping the Next Decade

Three forces will define the Bank’s work through the rest of the 2020s.

The first is the framework renewal due at the end of 2026. The current agreement, signed in December 2021, expires this year, and the review takes place in the shadow of the worst inflation overshoot since targeting began. The central question is whether the 2% target and the 1% to 3% range remain the right design after a period in which inflation ran far above the band for an extended stretch. The Bank has examined alternatives such as average inflation targeting and higher target levels in previous reviews and retained the existing framework each time. Whether it does so again, and how it explains the choice, will set the doctrine for the next five years.

The second is the country’s deep exposure to United States trade policy. Canada sends roughly three-quarters of its exports to a single market, and the tariff disputes that intensified in 2025 created a genuine policy bind. Tariffs raise prices, which argues for tighter policy, while the hit to exports and investment weakens demand, which argues for easier policy. The Bank’s April 2026 communications described exactly this two-directional risk, and resolving it is harder for Canada than for almost any other advanced economy because the shock is simultaneously inflationary and contractionary. This dependence is the central theme of our profile of the Canadian economy.

The third is the structure of the Canadian household balance sheet. Canada carries some of the highest household debt levels in the advanced world, much of it in mortgages that reset at intervals rather than being fixed for the life of the loan. That makes the transmission of rate changes to household budgets unusually fast and unusually powerful, which sharpens the impact of every decision the Governing Council takes and narrows the margin for error. A policy rate that would be merely restrictive elsewhere can bite hard in an economy where a large share of borrowers face renewal at higher rates within a few years.

Explains

Four ideas behind the Bank of Canada

Connect these ideas to the wider library of central banking and inflation articles.

Explore the MASEconomics BlogConclusion

The Bank of Canada is best understood as an institution organized around a single promise made in 1991: to keep inflation near 2%. That commitment, renewed jointly with the federal government every five years, shapes its governance through a consensus-driven Governing Council, its reliance on the overnight rate as the primary tool, and its willingness to look through temporary shocks while defending the medium-term anchor. The preamble to its founding Act has not changed since 1934, but the framework it operates has been rebuilt around the credibility of that inflation target.

As of May 2026, the Bank holds the overnight rate at 2.25% after a tightening cycle that reached 5% and an easing cycle of nine consecutive cuts. The year ahead brings a framework renewal under the strain of the worst inflation overshoot in the targeting era, a trade relationship with the United States that pulls policy in two directions at once, and a household sector whose heavy, fast-resetting debt makes every rate decision land harder than it would elsewhere. How the Governing Council navigates those pressures will determine whether the framework that has defined the institution for more than three decades carries cleanly into its fourth.

Frequently Asked Questions

What is the Bank of Canada in simple terms?

The Bank of Canada is the country’s central bank. It sets the policy interest rate, issues the physical currency, manages the federal government’s debt and foreign reserves, supports the stability of the financial system, and acts as a lender of last resort during crises. It does not offer personal bank accounts or retail services.

What is the Bank of Canada’s inflation target?

The Bank aims to keep total consumer price index inflation at the 2% midpoint of a 1% to 3% control range over the medium term. The target was first adopted in 1991 in a joint agreement with the federal government and is reviewed and renewed every five years, most recently in December 2021.

Who decides Bank of Canada interest rates?

Interest rate decisions are made by the Governing Council, which includes the Governor, the Senior Deputy Governor, and the Deputy Governors. The Council reaches decisions by consensus rather than a recorded vote and announces the policy rate on eight fixed dates each year.

Is the Bank of Canada independent from the government?

The Bank operates with day-to-day independence over how it conducts monetary policy. The law does give the Minister of Finance a directive power to override the Bank in an irreconcilable dispute, but it must be issued as a public written instruction and has never been used. Its visibility is what makes the Bank’s practical independence credible.

When was the Bank of Canada created?

The Bank of Canada Act received royal assent in 1934, and the Bank opened in March 1935. It began as a privately owned institution and was nationalized as a federal Crown corporation by 1938, which it remains today.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics