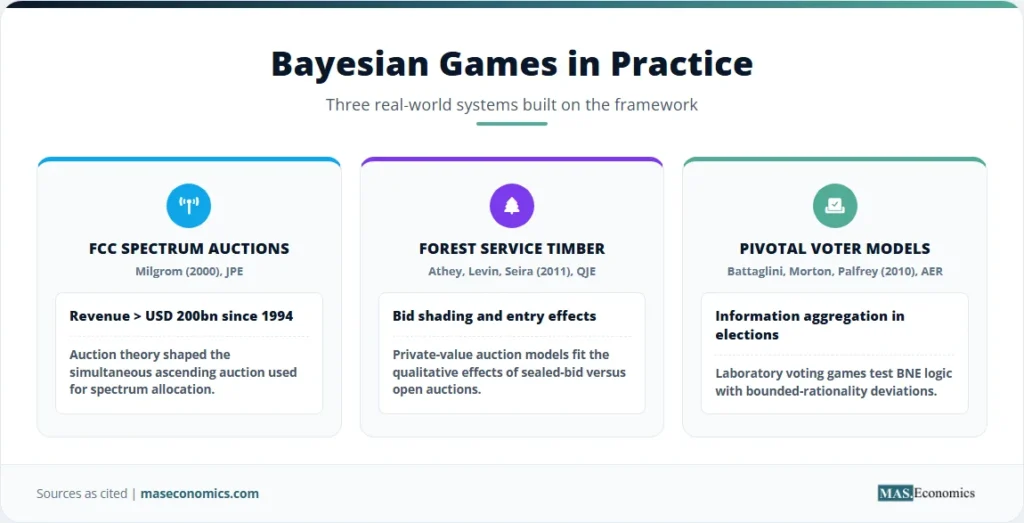

John Harsanyi published a three-part series in Management Science between 1967 and 1968 titled “Games with Incomplete Information Played by Bayesian Players.” The 1994 Nobel Committee credited that work with showing how games of incomplete information could be analysed systematically. FCC spectrum auctions designed with auction-theory tools have generated more than USD 200 billion in government revenue since the early 1990s.

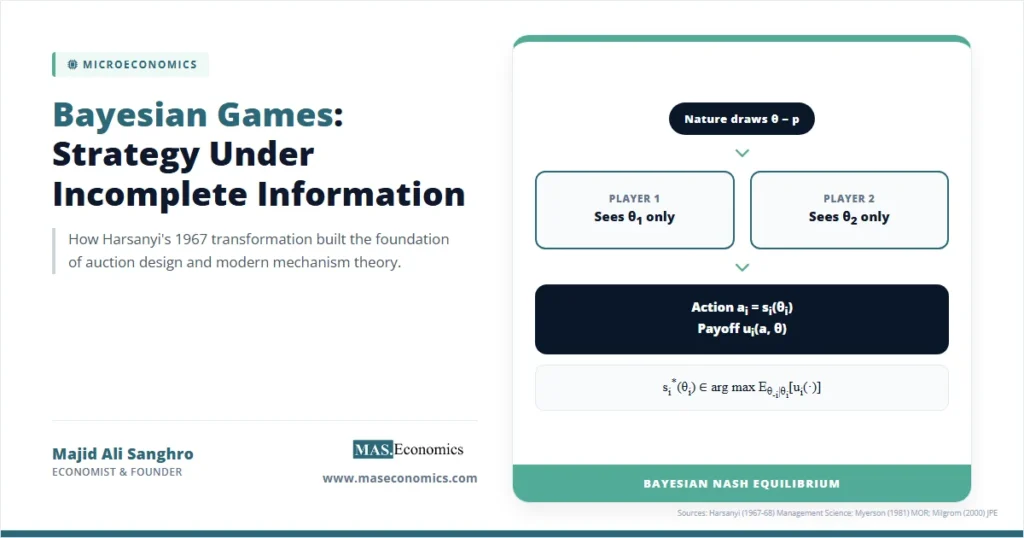

Bayesian Games are the formal model of strategic interaction when players have private information about payoffs, values, costs, preferences, or technologies. Each player has a type drawn from a common-prior distribution; each observes only her own type; each chooses an action that depends on her type. The equilibrium concept is Bayesian Nash Equilibrium, an interim best response for every type. Traditional Nash equilibrium assumes common knowledge of payoffs, but Harsanyi’s transformation replaced unknown private information with types drawn by Nature, making auctions, mechanism design, and signalling models tractable.

Types Turn Ignorance Into Structure

The core innovation in Bayesian games is the type. A type is a compact way to describe everything payoff-relevant that a player privately knows. In an auction, a type may be a bidder’s valuation. In a market-entry game, it may be a firm’s cost. In a signalling model, it may be worker productivity. In a political game, it may be a candidate’s policy preference or a voter’s private signal.

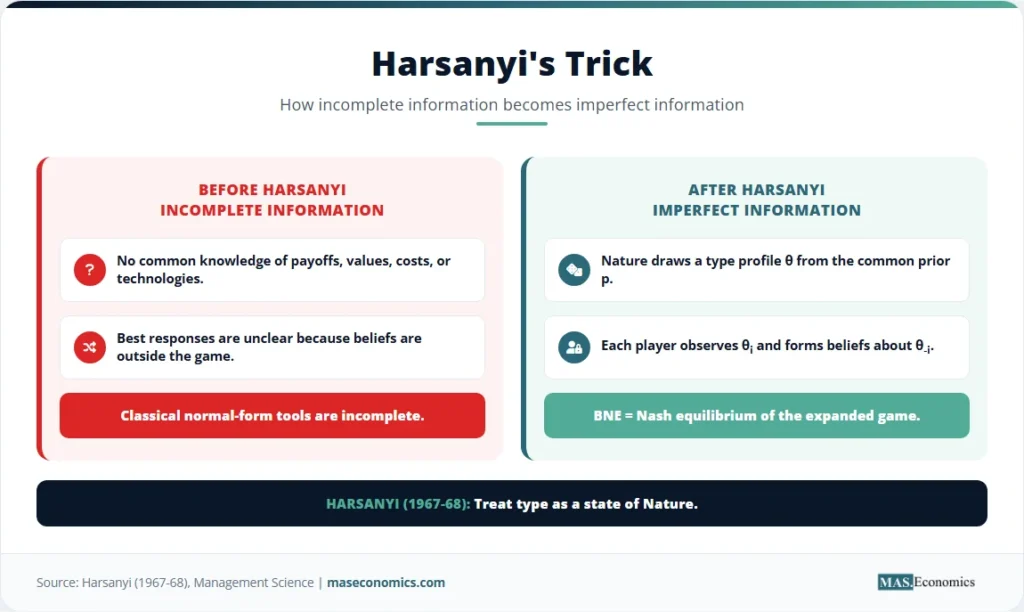

Before Harsanyi, incomplete information created a conceptual problem. If a player does not know another player’s payoff function, the ordinary best-response logic becomes unclear. Strategy depends on beliefs, but beliefs were not part of the classical normal-form game. Harsanyi solved the problem by placing beliefs inside the model. Nature first draws a type profile from a common prior. Each player observes her own type. The original game then proceeds, with each player forming beliefs about others’ types using Bayes’ rule.

This transformation changes the object of strategy. In a complete-information game, a strategy usually maps decision points into actions. In a Bayesian game, a strategy maps types into actions. A bidder with a high valuation may bid aggressively. A bidder with a low valuation may shade more heavily or exit. The equilibrium must make each type’s action optimal, given the posterior beliefs generated by that type.

The framework is now central to auction theory, mechanism design, information economics, and modern industrial organisation. Its importance comes from one simple fact: most economic environments contain private information, and private information changes incentives.

The Bayesian Game Formalism

A Bayesian game is written as:

The set \(N = \{1, \dots, n\}\) contains the players. The type space is \( \Theta = \Theta_1 \times \cdots \times \Theta_n \), where \( \theta_i \in \Theta_i \) is player \(i\)’s private type. The action space is \( A = A_1 \times \cdots \times A_n \). The function \(p(\theta)\) is the common prior over type profiles. The payoff function \(u_i: A \times \Theta \to \mathbb{R}\) gives player \(i\)’s payoff as a function of actions and types.

Player \(i\) observes only \( \theta_i \). She does not observe \( \theta_{-i} \), the vector of other players’ types. She therefore forms a posterior distribution using Bayes’ rule:

In a pure-strategy Bayesian game, player \(i\)’s strategy is a function:

A behavioural strategy maps types into probability distributions over actions:

A strategy profile \(s^* = (s_1^*, \dots, s_n^*)\) is a Bayesian Nash Equilibrium if every type of every player is choosing an interim best response. Formally, for every player \(i\), every type \( \theta_i \in \Theta_i \), and every alternative action \(a_i \in A_i\):

The word “interim” matters. The player knows her own type but does not know others’ types. The equilibrium condition is not ex ante optimality before anyone learns anything. It is not ex post optimality after all types are known. It is optimal at the moment private information has been received, but rivals’ private information remains hidden.

Harsanyi’s transformation converts a game of incomplete information into a game of imperfect information. Nature draws \( \theta \sim p \). Nature reveals \( \theta_i \) only to player \(i\). Players then choose actions. The Bayesian Nash Equilibrium of the incomplete-information game is the Nash equilibrium of this Harsanyi-transformed game. This is the technical bridge between private information and standard non-cooperative game theory.

The canonical example is the first-price sealed-bid auction. Two bidders draw independent private values \(v_i\) from the uniform distribution on \([0,1]\). Each submits a bid \(b_i\) without observing the other bidder’s value. The high bidder wins and pays her own bid. The loser pays zero. A symmetric Bayesian Nash Equilibrium is a strictly increasing bidding function \( \beta(v) \).

If bidder 1 has value \(v_1\) and submits bid \(b\), her expected payoff is:

Because \( \beta \) is strictly increasing, winning means \( v_2 < \beta^{-1}(b) \). With uniform values, the probability of winning is \( \beta^{-1}(b) \). The expected payoff becomes:

The first-order condition is:

In symmetric equilibrium, \( b = \beta(v_1) \), so \( \beta^{-1}(b) = v_1 \). Substitution gives:

The solution is:

Each bidder bids half her private value. This is bid shading: bidders reduce bids below valuations because the winning bidder pays her own bid. In a second-price auction, truthful bidding \( \beta(v)=v \) is a Bayesian Nash Equilibrium. Under the standard independent-private-values assumptions, both formats yield the same expected seller revenue, the logic later generalised in the Revenue Equivalence Theorem associated with William Vickrey and Roger Myerson’s optimal auction design.

Existence also matters. Milgrom and Weber’s distributional-strategies paper established general equilibrium-existence results for games with incomplete information under standard compactness, continuity, and distributional conditions. That result gives the framework mathematical stability beyond finite classroom examples.

| Symbol | Name | Definition |

|---|---|---|

| \(N\) | Players | Decision-makers in the strategic environment. |

| \(\Theta_i\) | Type space | Player \(i\)’s possible private-information states. |

| \(A_i\) | Action space | Player \(i\)’s possible actions. |

| \(p(\theta)\) | Common prior | Shared probability distribution over type profiles. |

| \(u_i(a,\theta)\) | Payoff function | Payoff depending on actions and type profile. |

| \(s_i(\theta_i)\) | Strategy | Action chosen by player \(i\) for each type. |

| BNE | Equilibrium | Interim best response for every type of every player. |

| \(\beta(v)\) | Bidding function | Bid chosen as a function of private value. |

|

||

Where the Assumptions Bite

Bayesian games depend on five core assumptions. The first is the common prior. Players may receive different information, but they begin from the same probability distribution over states. Robert Aumann’s agreement theorem gave this assumption deep implications: agents with the same prior cannot persistently “agree to disagree” when their posteriors are common knowledge.

The second assumption is common knowledge of the game structure. Players must know the action spaces, type spaces, payoff functions, and prior. They must also know that others know them, and so on. This is demanding, but it is what allows the model to produce precise equilibrium predictions.

The third assumption is that types contain all payoff-relevant private information. A model that leaves out important private information may produce misleading equilibria. A firm’s “cost type” may not be enough if it also has private information about capacity, demand, regulation, or financing. A bidder’s valuation may not be enough if she also receives private signals about resale value.

The fourth assumption is Bayesian updating. Players must update beliefs with Bayes’ rule after observing their own type or signal. The fifth is interim rationality. Each type must prefer its prescribed equilibrium action to any alternative action, given beliefs about other types.

The common-prior assumption is the most contested. In many real settings, disagreement may reflect different models, different priors, or ambiguity rather than different signals drawn from a shared distribution. Behavioural game theory, heterogeneous-prior models, rationalisability, and \( \Delta \)-rationalisability relax parts of the standard framework. These alternatives keep the private information insight but weaken the assumption that all uncertainty is probabilistic and commonly understood.

Type spaces also raise foundational questions. A model may specify that a player is “high cost” or “low cost,” but real private information can involve beliefs about beliefs about beliefs. Mertens and Zamir’s universal type-space framework addressed this by asking how rich a type space must be to represent all hierarchies of beliefs. The result made Bayesian games more foundational, but also showed how abstract real applications can become.

Finally, Bayesian games handle risk better than ambiguity. When probabilities are known, or modelled as if known, the common-prior structure is natural. Under Knightian uncertainty, where agents do not know the probability distribution itself, extensions such as Gilboa and Schmeidler’s max-min expected utility are needed. Standard Bayesian Nash Equilibrium is not designed for non-unique priors or deep ambiguity.

Evidence from Auctions and Voting

Bayesian games moved from theory to applied economics most visibly through auctions. Spectrum auctions are the flagship case. Paul Milgrom’s “Putting Auction Theory to Work” explains how the simultaneous ascending auction was introduced in 1994 to allocate radio-spectrum licences in the United States. FCC auction summaries show the first nationwide narrowband PCS auction in July 1994 raised more than USD 617 million, and later spectrum auctions scaled the framework dramatically.

The design problem was Bayesian from the start. Bidders had private valuations, uncertain complementarities across licences, and strategic incentives to reveal or conceal information through bids. Auction rules had to discipline collusion, reduce exposure problems, and help bidders aggregate information. Modern auction design is therefore not only an application of price theory. It applies Bayesian game theory.

Timber auctions provide another empirical test. Susan Athey, Jonathan Levin, and Enrique Seira studied U.S. Forest Service timber auctions in the Quarterly Journal of Economics. They compared open and sealed-bid auctions and found systematic differences in entry, bidder composition, allocation, and revenue. Their private-values auction model with endogenous participation accounts for the qualitative effects of the auction format. The results show how private information and strategic bidding shape real procurement and resource-allocation markets.

Voting games offer a third application. In Bayesian voting models, citizens receive private signals about candidate quality, policy states, or the value of turnout. A vote is costly, and the chance of being pivotal depends on beliefs about how others vote. Laboratory work by Marco Battaglini, Rebecca Morton, and Thomas Palfrey on information aggregation and strategic abstention tests the logic of large-election Bayesian models. The evidence supports important qualitative predictions, while deviations point to bounded rationality, social preferences, or mistakes in probability assessment.

The chart shows why the same private-value environment can produce different bidding strategies. In the first-price auction, the symmetric Bayesian Nash Equilibrium is \( \beta(v)=v/2 \) with two uniform bidders. In the second-price auction, truthful bidding \( \beta(v)=v \) is optimal. The allocation and revenue implications depend on assumptions, but the strategic logic differs sharply.

Markets Built on Private Information

Auction theory is the most direct application. The Vickrey-Clarke-Groves mechanism, the Revenue Equivalence Theorem, and Myerson’s optimal auction all rely on strategic reasoning under private information. Bidders have values. The seller has design objectives. The mechanism must induce actions or reports that produce the desired allocation and payment rule. That is a Bayesian game.

Modern markets use this logic constantly. Treasury-bond auctions, spectrum auctions, procurement auctions, electricity-market auctions, online advertising auctions, and platform-pricing systems all contain private values, private costs, or private information about demand. Auction rules shape how participants reveal information and how much surplus is captured by buyers, sellers, or the state.

Mechanism design extends the logic. Instead of asking what will happen in a given game, mechanism design asks which game should be built to achieve a target outcome. The revelation principle allows many problems to be studied as direct mechanisms in which agents report types. Incentive compatibility then requires truthful reporting to be a Bayesian Nash Equilibrium. This connects Bayesian games to taxes, regulation, healthcare payment systems, carbon-pricing schemes, and platform governance.

The Mirrlees optimal-income-tax model is a major example. Workers privately know their productivity or effort cost. The tax authority observes income, not innate ability. The problem is to design a tax schedule that balances redistribution against incentive effects. The resulting model is not a simple public-finance exercise. It is a Bayesian incentive problem with hidden types.

Industrial organisation also relies on Bayesian games. In limit-pricing models, an incumbent firm may have private cost information. An entrant observes prices and tries to infer whether entry will be profitable. Milgrom and Roberts’ asymmetric-information approach gave a fully game-theoretic foundation to limit pricing, replacing older intuition with equilibrium signalling logic.

Signalling games are Bayesian games with sequential structure. In Spence signalling, education can transmit information about productivity. In the Akerlof market for lemons, quality differences and asymmetric information can destroy trade. These models differ in timing and message structure, but they share the same foundation: types, beliefs, strategies, and equilibrium behaviour under incomplete information.

Finance adds another layer. Market microstructure models study how informed and uninformed traders interact. In Kyle-style insider-trading models, an informed trader chooses order flow while market makers infer information from prices and quantities. Prices become signals. Trading becomes strategic communication. The market-clearing outcome is a Bayesian equilibrium object rather than a simple supply-and-demand crossing.

The broader lesson is that private information is not a detail added after the main theory. It changes the theory. Once players have types, strategy becomes a function of information. Once beliefs matter, equilibrium requires consistency between actions and posteriors. Once mechanisms are designed around incentives, the boundary between game theory mathematics and policy design becomes thin. Bayesian games are therefore one of the central languages of modern strategic behaviour.

MASEconomics Explains

4 economic concepts behind Bayesian games

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Bayesian Games formalise strategic choice when players have private information. Harsanyi’s transformation made incomplete-information games tractable by introducing types, a common prior, posterior beliefs, and strategies that map information into actions. Bayesian Nash Equilibrium then requires every type to choose an interim best response.

The first-price auction shows the framework in its cleanest form. With two independent uniform private values, the symmetric equilibrium bid is \( \beta(v)=v/2 \), while second-price auctions make truthful bidding optimal. That contrast explains why auction design, revenue equivalence, and mechanism design all rely on Bayesian reasoning.

The modern applications are broad: spectrum auctions, timber sales, voting experiments, optimal taxation, regulation, limit pricing, signalling, and market microstructure all use private-information equilibrium logic.

Frequently Asked Questions

What is a Bayesian game?

A Bayesian game is a game in which at least one player has private information about payoffs, values, costs, or preferences. The private information is represented by a type, and players form beliefs about other players’ types using a prior distribution.

What is Bayesian Nash Equilibrium?

Bayesian Nash Equilibrium is a strategy profile in which every type of every player chooses an interim best response. The player knows her own type but forms beliefs about the types of others.

What is the Harsanyi transformation?

The Harsanyi transformation converts a game of incomplete information into a game of imperfect information. Nature draws types from a common prior, reveals each player’s own type, and the resulting transformed game can be analysed with standard equilibrium tools.

Why are Bayesian games important in auctions?

Auction bidders usually know their own valuations but not the valuations of rivals. Bayesian games model that private information directly, which makes them central to first-price auctions, second-price auctions, spectrum auctions, and optimal auction design.

What is the common-prior assumption?

The common-prior assumption states that players share the same probability distribution over possible type profiles before private information is observed. Players may hold different posteriors after observing different signals, but those beliefs come from the same prior.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics