On August 9, 2011, the Federal Open Market Committee released a statement with an unusual sentence: economic conditions were “likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013.” The central bank was committing, for the first time, to a specific date for keeping policy easy. Markets responded immediately. Two-year Treasury yields fell roughly 8 basis points, ten-year yields fell about 17 basis points, and equity prices rallied. The Fed had not changed the policy rate; it had only changed what it said about the future. This was forward guidance deployed as a deliberate policy tool, and it confirmed what the academic literature had argued since the late 1990s: when conventional rate policy runs out of room, the central bank can still move financial conditions by managing expectations about where rates will go next.

Forward guidance differs from routine central bank commentary in being explicit, carrying a specific time horizon, and serving as a substitute for conventional rate moves at the lower bound. The mechanism is among the most important policy innovations of the post-crisis era, forming the foundation for nearly all current central bank communication about future policy paths.

From Open Mouth Operations to Deliberate Communication

Central banks have always influenced expectations. Alan Blinder, in his work on central bank communication, traced the tradition back through the Bundesbank’s monetary signaling in the 1970s to the Federal Reserve’s earliest open-market operations, when the chairman’s testimony before Congress was understood as a policy instrument in its own right. The informal label “open mouth operations” captured the idea that central bankers could move markets simply by speaking, without conducting any actual transactions. Mervyn King, while at the Bank of England, used the same term to describe the way central bank communication had become an active tool alongside the policy rate.

Forward guidance differs from these older forms of communication in three ways. First, it is explicit rather than implicit. The central bank announces in plain language what it expects to do with the policy rate, rather than leaving market participants to infer the path from speeches and testimony. Second, it has a specific time horizon attached, whether expressed as a calendar date, a state of the economy, or a probability-weighted projection. Third, it is meant to be a substitute for, or a complement to, conventional rate moves, particularly when the policy rate has reached its lower bound and cannot easily be cut further.

The intellectual foundation was laid by Paul Krugman in his 1998 paper on Japan’s liquidity trap and developed more formally by Michael Woodford in the 2000s. Woodford’s argument was that monetary policy works primarily through expectations about the entire future path of short-term rates, rather than through the current rate alone. Long-term yields, mortgage rates, corporate borrowing costs, and asset prices all depend on what markets believe about the central bank’s reaction function over the years to come. If the central bank can credibly commit to keeping rates low for longer than markets would have expected, long-term rates fall today, financial conditions ease, and the economy responds even though the spot policy rate has not moved. The argument was theoretical when first published, but the post-2008 environment made it operational.

Three Families of Forward Guidance

Forward guidance in practice has taken three main forms, distinguished by the kind of commitment the central bank makes. The differences matter because each form trades off precision for flexibility in different ways.

The first form is qualitative or open-ended guidance. The central bank says rates will stay low “for some time”, “for an extended period”, or “until the recovery is well established.” No date is named, no economic threshold is specified, and the central bank retains complete discretion to change course when conditions warrant. The Federal Reserve used this language extensively from late 2008 through mid-2011. The European Central Bank under Mario Draghi used similar language in the early years of the euro area crisis. Qualitative guidance is the least binding form, but it is also the easiest to issue, and it conveys directional information without locking the central bank into a specific path.

The second form is date-based or calendar guidance. The central bank names a specific date through which it expects policy to remain in a particular stance. The Federal Reserve’s August 2011 commitment to keep rates low “at least through mid-2013” was the first explicit calendar guidance from a major central bank. The Fed extended the horizon to “late 2014” in January 2012 and then to “mid-2015” in September 2012. The Bank of Canada used a conditional commitment in 2009 that named a specific date, April 2010. Date-based guidance is more concrete than qualitative guidance and provides clearer market signaling, but it also makes the central bank’s communication brittle: if economic conditions change before the date is reached, the central bank must either break its commitment or maintain a stance that is no longer appropriate.

The third form is state-based or threshold guidance, also called Evans-rule guidance after Charles Evans, the former president of the Federal Reserve Bank of Chicago, who advocated for it in 2011. The central bank ties policy to specific economic conditions: rates will stay low until unemployment falls below a threshold, until inflation rises above a threshold, or until both conditions are met. The Federal Reserve adopted threshold guidance in December 2012, committing to keep rates low until unemployment fell below 6.5 percent, provided inflation remained below 2.5 percent. The Bank of England introduced similar threshold guidance under Mark Carney in August 2013. State-based guidance is conditional on the economy rather than on the calendar, which makes it more robust to shocks but also more complex to communicate.

| Dimension | Qualitative | Date-Based | State-Based |

|---|---|---|---|

| Form of commitment | “Some time”, “extended period” | Specific calendar date | Economic threshold, such as unemployment or inflation |

| Precision | Low | High | Medium |

| Flexibility if conditions change | High | Low | Built-in conditioning |

| Risk of breaking the commitment | Minimal | Substantial | Low because it auto-adjusts |

| Market impact on long yields | Modest | Largest at announcement | Strong, plus volatility |

| Communication complexity | Low | Moderate | High |

| Example central banks | Fed 2008–2011; ECB 2013– | Fed Aug 2011–Mar 2014; BoC 2009–2010 | Fed Dec 2012–Mar 2014; BoE Aug 2013–Feb 2014 |

| Net trade-off | Easy to issue, weak signal | Strong signal, fragile | Robust but complex |

|

Source: Federal Reserve, Bank of England, Bank of Canada, and European Central Bank policy statements; academic literature on central bank communication.

|

|||

The progression across the post-2008 period reflects an institutional learning curve. Central banks started with qualitative language because it was familiar and committed little. They moved to date-based guidance when the qualitative language stopped moving markets. They moved to state-based guidance when the calendar dates began to bind on policy in unhelpful ways. By 2014, most major central banks had retired the more rigid forms and returned to softer guidance combined with quarterly projections, which became the dominant framework for the rest of the decade.

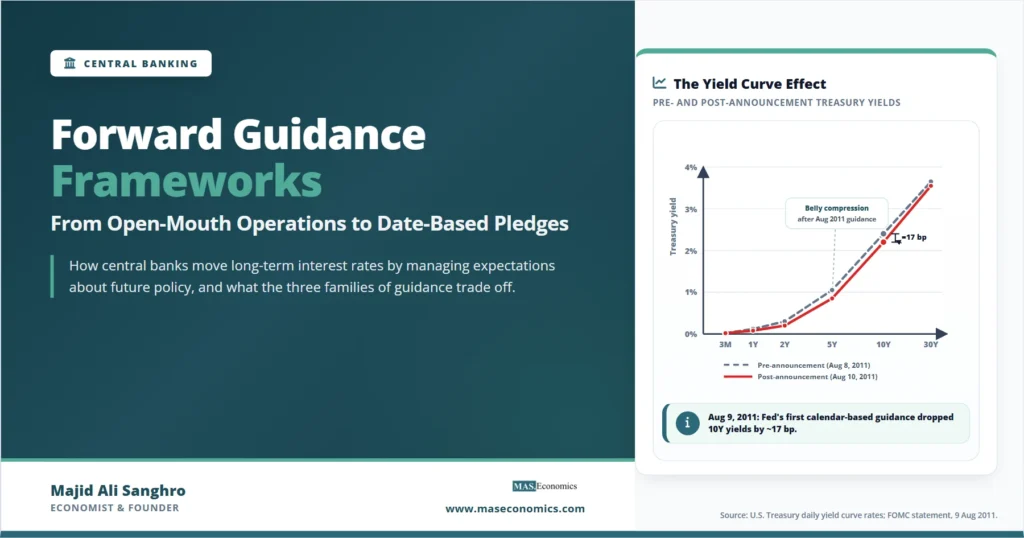

The Yield Curve Effect

The clearest way to see what forward guidance does is to look at the yield curve before and after a major guidance announcement. The August 2011 Fed announcement is the cleanest case study, because it was the first explicit calendar guidance and because markets had no prior commitment to price against.

Three patterns in the chart are worth pulling out. The 3-month and 6-month rates barely moved because they were already near zero and could not fall further. The 2- to 7-year maturities fell most sharply, between 7 and 20 basis points, because this is the part of the curve most sensitive to the expected path of policy over the next few years, which is what the guidance directly addressed. The 30-year yield barely moved, because the August 2013 guidance horizon was much shorter than the 30-year maturity, and forward expectations of policy that far out are anchored more by long-run neutral rate expectations than by short-term guidance. This pattern of “belly compression” became the signature footprint of forward guidance in the bond market.

Mechanics of the Expectations Channel

The economic intuition behind forward guidance follows from a simple identity. The yield on a long-term bond can be decomposed into the expected average of future short-term rates over the life of the bond, plus a term premium. A 10-year Treasury yield, for instance, reflects what markets expect 3-month rates to average over the next ten years, plus a premium for holding duration risk. If a credible central bank announces it will keep short rates near zero for two more years, the expected average over the first two years of the ten-year horizon drops sharply. Even if the long-run expectation stays unchanged, the 10-year average falls, and the 10-year yield falls with it.

This channel makes forward guidance particularly powerful at the lower bound, when conventional rate cuts are no longer possible. The central bank cannot move the spot rate from zero to negative without invoking unconventional measures, but it can shift the expected path of future rates by committing to keep them at zero longer than markets had priced. Long yields fall, mortgage rates fall, corporate borrowing costs fall, the dollar depreciates, equity valuations rise, and financial conditions ease across multiple channels. The mechanism is the same one that conventional rate cuts use, but it operates on expectations rather than on the spot rate.

Expectations Hypothesis of the Yield Curve

The same mechanism explains why forward guidance is most powerful in normal times when central banks have credibility. If markets do not believe the commitment, the expected rate path does not adjust, and long yields do not fall. The Bank of Japan’s repeated attempts at forward guidance through the 2000s had limited effect, partly because markets did not believe the bank would maintain accommodative policy long enough for the commitment to bind. The Federal Reserve’s commitments in 2011 and 2012 worked because the Fed had built credibility through the prior decades of inflation-targeting practice. Quantitative easing operations conducted alongside the guidance reinforced this credibility, because the bond purchases made it costly for the Fed to suddenly reverse course.

Empirical Evidence on Effectiveness

Forward guidance has been studied intensively since its emergence as a deliberate policy tool. The academic verdict is broadly positive but qualified.

The strongest evidence comes from event studies measuring yield changes around guidance announcements. Refet Gurkaynak and colleagues at the Federal Reserve found that the August 2011 announcement and subsequent guidance changes moved 2-year yields by 10 to 25 basis points on impact, with effects fading over weeks to months as the news was absorbed. Similar event studies of the Bank of England’s August 2013 threshold guidance, the ECB’s 2013 statement of “rates at present or lower levels for an extended period”, and the Bank of Canada’s 2009 conditional commitment found comparable directional effects on local sovereign curves.

The harder question is whether forward guidance affected the real economy beyond the financial conditions channel. The transmission mechanism is the same as conventional policy: lower long-term rates ease borrowing costs, which support investment and consumption, which feed back into output and inflation. But the magnitude of the real effect depends on how long the lower yields persist, how responsive borrowers are, and what the central bank does later. Several Fed staff studies estimated that the cumulative effect of all forward-guidance episodes from 2008 to 2014 was equivalent to perhaps 100 to 200 basis points of additional conventional easing, which was substantial but not transformative.

A more critical strand of literature, including work by Marco Del Negro and colleagues at the New York Fed and by Lawrence Christiano and others, identified the “forward guidance puzzle”: standard New Keynesian models predict implausibly large effects from credible long-horizon commitments. If the model says a four-year guidance promise should move output by 10 percent, but the actual effect is closer to 1 to 2 percent, something is wrong with either the model or the credibility assumption. The resolution most economists have settled on is that real-world credibility is partial, that horizons beyond two to three years are heavily discounted by markets, and that guidance is most effective when it confirms rather than surprises against the market’s existing expectations.

Forward guidance is a tool of credibility, not of magic. A central bank that has consistently followed through on its guidance gains incremental credibility with each cycle, and its future guidance moves markets more reliably. A central bank that has often broken its guidance loses this credibility, and the tool becomes weaker over time. The effectiveness of guidance is therefore endogenous to the institutional history of the central bank using it.

The 2021-2022 Stress Test

The most serious test of forward guidance as a tool came in late 2021 and 2022. The Federal Reserve had spent much of 2020 and 2021 communicating that policy rates would stay near zero through at least 2023, conditional on the recovery proceeding as projected. When inflation surged unexpectedly in mid-2021, the Fed faced a choice. It could honor the prior guidance and accept rising inflation expectations, or it could break the guidance and tighten policy to contain inflation. It chose the latter, moving from near-zero rates in March 2022 to over 5 percent by mid-2023, the fastest tightening cycle in decades.

The episode illustrated both the value and the limit of forward guidance. The value was that the prior accommodative commitment had genuinely held expected rates lower than they would have been in the absence of guidance, supporting the economy through the most acute pandemic phase. The limit was that when conditions changed sharply, the guidance became a constraint on policy. The Fed’s framework and prior communication had to be abandoned, and the credibility cost of doing so was material. Several FOMC participants subsequently acknowledged that the 2021 guidance had been too aggressive in retrospect, but the formal review of central bank communication that this would normally trigger was folded into the broader 2025 framework review.

Other central banks faced similar problems. The European Central Bank’s prior guidance that rates would remain at zero “or lower” until specified conditions were met had to be abandoned in mid-2022. The Bank of Japan’s yield curve control framework, itself a form of quantitative forward guidance, came under sustained pressure as global rates rose, and the BoJ eventually exited negative rates in March 2024. The lessons of the episode have shaped how central banks talk about forward guidance going forward: more conditional, shorter horizon, more explicit about the dependence on data, and more willing to acknowledge that the guidance does not commit future committees.

Forward Guidance in Current Practice

The aggressive date-based and threshold-based guidance of 2011-2014 has been largely retired. What remains is a softer form of communication built around two main devices: the published projections of policymakers and the qualitative descriptions of expected reaction functions in policy statements.

The Federal Reserve’s Summary of Economic Projections, published quarterly, includes the famous dot plot showing each FOMC participant’s view of the appropriate federal funds rate over the next several years. While the SEP is not formal guidance, it conveys substantially more information than the qualitative language in pre-2008 statements. The European Central Bank publishes a similar set of projections in its quarterly Monetary Policy Statements. The Bank of England publishes detailed reaction-function language and a fan chart of inflation projections. In each case, the communication is conditional and qualified, but it provides clear directional signals about where the central bank expects policy to go.

The second device is the explicit articulation of the reaction function. Central banks now routinely describe how their policy would respond to specified deviations of inflation or unemployment from target. The language of “data dependence”, widely used since 2022, is a form of forward guidance that commits the central bank not to a date or a threshold but to a process of evaluating incoming information. This is the weakest form of guidance, but it is also the most flexible. It survives sudden shifts in conditions without forcing the central bank to break a prior commitment.

What has not survived is the use of forward guidance as a binding substitute for conventional policy. The 2011-2014 experience showed that explicit calendar and threshold commitments are effective when the lower bound is binding, but they impose real constraints on subsequent flexibility. The current consensus among major central banks is that strong forward guidance should be reserved for lower-bound episodes, while in normal times the projections and reaction-function language are sufficient to manage expectations without locking in commitments that may later need to be broken.

Explains

Three concepts behind the forward guidance toolkit

From guidance frameworks to the dot plot and the broader toolkit of central bank communication.

Explore the MASEconomics BlogConclusion

The forward guidance innovation of the post-2008 period transformed central bank communication from a peripheral activity into a core policy tool. By managing expectations about the future path of short-term rates, central banks discovered they could move long-term yields, ease financial conditions, and support the economy even when the spot policy rate had reached the lower bound. The progression from qualitative language to date-based commitments to state-based thresholds reflected an institutional learning curve, with each form trading precision against flexibility in different ways. The 2011-2014 era of explicit calendar and threshold commitments showed both the power and the fragility of the technique: it worked when credibility was strong and conditions stable, but it became a constraint when conditions changed.

The current frameworks have largely retired the aggressive forms of guidance in favor of softer signaling through projections and reaction-function language. The post-2022 inflation surge has further reinforced the preference for flexibility. Whether the more rigid forms of guidance return depends on whether the lower bound becomes binding again in future cycles. The structural decline of the neutral rate of interest implies that this is more likely than not, in which case the toolkit developed in the 2010s will be the starting point for the next round of unconventional communication. The mechanism is well understood, the credibility costs of misuse are clearer than they were a decade ago, and the institutional memory at major central banks is unusually rich on this particular instrument.

Frequently Asked Questions

What is forward guidance?

Forward guidance is the practice of central banks announcing in advance their expected future policy stance, with the aim of shaping market expectations and influencing financial conditions today. It can take qualitative form (“rates will stay low for some time”), date-based form (“rates will stay low until mid-2013”), or state-based form (“rates will stay low until unemployment falls below 6.5 percent”). It is most powerful when the policy rate is at the lower bound and conventional easing is no longer available.

Why does forward guidance affect long-term interest rates?

Long-term yields reflect the expected average of short-term rates over the bond’s life, plus a term premium. If the central bank credibly commits to keeping short rates lower for longer than markets had expected, the expected average falls, and long yields fall with it. This is the same mechanism through which conventional rate policy operates, but it works on the expected path of future rates rather than on the current spot rate.

When did the Federal Reserve first use explicit forward guidance?

The Fed used qualitative forward guidance from late 2008 onward. The first explicit date-based guidance came on August 9, 2011, when the FOMC committed to keep rates “at least through mid-2013.” This was extended to “late 2014” in January 2012 and to “mid-2015” in September 2012. State-based threshold guidance was added in December 2012, tying rates to unemployment falling below 6.5 percent.

What is the difference between date-based and state-based guidance?

Date-based guidance names a specific calendar date through which policy is expected to remain in a particular stance. State-based guidance ties policy to economic thresholds such as unemployment or inflation reaching specified levels. Date-based guidance provides a stronger signal but is brittle if economic conditions change. State-based guidance is more robust because it auto-adjusts to conditions, but it is more complex to communicate.

Did forward guidance work in the 2008-2014 period?

The empirical evidence suggests yes, though with qualifications. Event studies of guidance announcements consistently found significant moves in 2- to 7-year Treasury yields, equity prices, and the dollar. Estimates of the cumulative effect across multiple guidance episodes suggest the equivalent of 100 to 200 basis points of additional conventional easing. However, the real-economy impact was smaller than New Keynesian models predict, reflecting partial credibility and the practical limits of long-horizon commitments.

Why did central banks move away from aggressive forward guidance?

The 2021-2022 inflation surge exposed the cost of binding commitments. The Fed’s prior guidance that rates would stay near zero through 2023 had to be abandoned as inflation rose, and the credibility cost of doing so was material. Central banks now prefer softer forms of communication through projections and conditional reaction-function language. Aggressive guidance is reserved for genuine lower-bound episodes where conventional easing is unavailable.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics