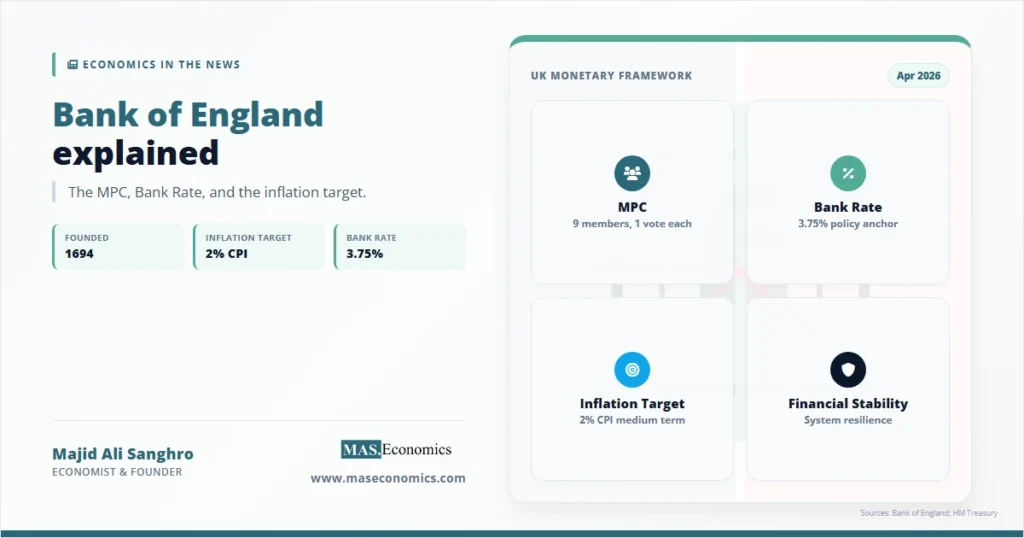

The Bank of England maintained Bank Rate at 3.75% in April 2026 after the Monetary Policy Committee voted 8–1 to hold policy steady. Bank of England explained means understanding more than one interest-rate decision. It means understanding how Britain’s central bank uses Bank Rate, inflation forecasts, financial-stability tools, and institutional independence to anchor the UK monetary system.

The Bank is the United Kingdom’s central bank. It issues banknotes, sets monetary policy, supervises financial stability, supports payment systems, manages market operations, and acts as a backstop when financial markets face liquidity stress. Its modern public identity rests on one visible target: keeping CPI inflation at 2% over the medium term.

The Bank’s role is often described through the Bank Rate. That is accurate but incomplete. The Bank of England is also a financial-stability institution, a market operator, a bank supervisor through the Prudential Regulation Authority, and a public institution whose credibility affects sterling, gilt yields, mortgage pricing, business investment, and inflation expectations.

The Mandate and Functions of the Bank of England

The Bank of England is the UK’s central bank. Its public mandate has two main pillars: monetary stability and financial stability. Monetary stability means keeping inflation low and stable. Financial stability means protecting the resilience of the financial system so banks, insurers, markets, and payments can continue functioning through stress.

The Bank’s most visible policy tool is the Bank Rate. Bank Rate is the interest rate paid on reserves held by commercial banks at the Bank of England. It influences the interest rates that households and firms face through mortgages, savings accounts, business loans, credit cards, bond yields, and wider financial-market pricing. A higher Bank Rate normally tightens financial conditions. A lower Bank Rate normally eases them. The effect is powerful, but not instant. Monetary policy works with lags because firms and households adjust spending, borrowing, saving, and pricing decisions gradually.

The Bank does not set the inflation target by itself. The UK government sets the target, and the Bank is responsible for achieving it. The current target is 2% CPI inflation, as confirmed in the Treasury’s monetary policy remit. The Bank’s own inflation guide explains the same framework: the government sets a 2% target to keep inflation low and stable.

The Bank also has a secondary role in supporting the government’s economic objectives, including growth and employment, subject to price stability. That hierarchy matters. The Bank can support sustainable growth, but it cannot ignore inflation. It can cushion demand shocks, but it cannot permanently raise productivity, remove trade frictions, or solve fiscal constraints. Those problems belong to the wider economy and government policy.

Several existing MASEconomics articles help place this role in a wider framework. The Bank’s work fits within central banking and monetary policy, uses many of the instruments described in monetary policy tools, and depends on the credibility discussed in central bank independence. Its decisions also connect directly to the UK economy, because interest rates affect households, firms, public debt costs, sterling, housing, and financial markets.

Historical Evolution of the Bank

The Bank of England was founded in 1694 as a private bank to act as banker to the government. Its origin was fiscal and military. The state needed finance. The Bank helped raise money and manage government borrowing. Over time, that government-banker role expanded into note issue, public-debt management, crisis lending, financial-market operations, and eventually modern central banking.

For much of its history, the Bank was closely tied to the City of London and the government. It was not originally an independent inflation-targeting central bank. It evolved through crises. Nineteenth-century banking panics strengthened the idea that the Bank should act as lender of last resort. The Bagehot principle, associated with lending freely against good collateral at a penalty rate during panic, became one of the foundations of modern crisis central banking.

Britain’s gold-standard era gave the Bank a different anchor. Monetary policy was constrained by convertibility into gold and by the need to defend sterling. That system imposed discipline, but it also limited domestic policy flexibility. During the twentieth century, wars, depression, devaluation, capital controls, and post-war reconstruction changed the Bank’s role again. The Bank was nationalised in 1946, which formally moved ownership from private shareholders to the state.

The post-war decades were marked by recurring inflation, sterling pressure, wage-price conflict, and balance-of-payments concerns. The Bank operated within a system where elected governments had more direct control over interest-rate decisions. Monetary policy was often influenced by fiscal needs, exchange-rate pressures, and political timing. This structure made it harder to separate short-term political incentives from the long-term need for price stability.

The 1970s and early 1980s showed the cost of unstable inflation. High inflation distorted wage bargaining, asset prices, savings, business planning, and sterling confidence. Later reforms moved the UK toward a more rule-based monetary framework. The adoption of inflation targeting in the early 1990s marked a major shift. The government announced an inflation objective, and monetary policy became more transparent.

The decisive modern turning point came in 1997. The newly elected government granted the Bank operational independence over interest-rate decisions. The Bank of England Act 1998 created the statutory Monetary Policy Committee and gave it responsibility for monetary policy within the Bank. This reform separated the inflation target, set by the government, from the operational choice of Bank Rate, decided by the MPC.

Independence changed the Bank’s credibility. Interest-rate decisions became regular, published, explained, and voted on by named policymakers. Minutes and voting records created accountability. The Bank still answers to Parliament and works within a government-set remit, but day-to-day rate setting no longer belongs to ministers. That division is the core of the modern UK monetary constitution.

The Monetary Policy Committee

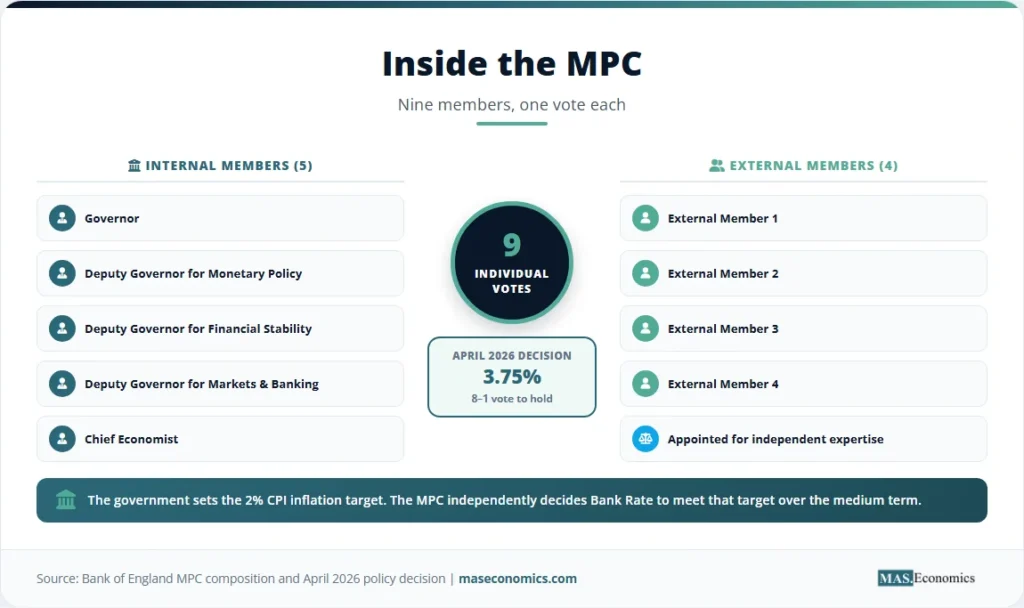

The Monetary Policy Committee is the decision-making body that sets the Bank Rate. The Bank states that the MPC has nine members: the Governor, the three Deputy Governors for Monetary Policy, Financial Stability, and Markets and Banking, the Bank’s Chief Economist, and four external members appointed by the Chancellor. Each member has one vote.

The committee meets eight times a year. Before each decision, members review inflation, wages, labour-market data, GDP, business surveys, fiscal policy, global shocks, sterling, credit conditions, financial-market pricing, and the Bank’s own forecasts. The decision is not a mechanical reaction to the latest inflation print. The MPC is forward-looking. It asks what policy stance is needed to return inflation to the target sustainably over the medium term.

The voting structure matters because it allows disagreement. A 9–0 vote indicates consensus. A split vote signals different views on inflation persistence, spare capacity, wage growth, external shocks, or the risks of overtightening. In April 2026, the MPC voted by an 8–1 majority to maintain Bank Rate at 3.75%, according to the Bank’s April 2026 monetary policy summary. That vote showed broad support for holding policy steady, with one member preferring a different path.

The MPC’s structure blends internal institutional knowledge with external expertise. Internal members bring access to Bank staff analysis, market intelligence, financial stability information, and forecasting infrastructure. External members bring independent judgment and different professional backgrounds. This mix is meant to reduce groupthink and strengthen public confidence.

Transparency is part of the system. The Bank publishes policy summaries, minutes, speeches, reports, and forecasts. The Governor and other MPC members appear before Parliament. When inflation deviates from target by more than one percentage point, the Governor must write an open letter to the Chancellor explaining why inflation has moved away from target, what the Bank is doing, and when inflation is expected to return.

The MPC does not decide fiscal policy, tax policy, public spending, immigration rules, trade agreements, or planning reform. This boundary matters. Monetary policy can influence demand and expectations, but productivity, housing supply, trade frictions, and public investment are outside the MPC’s direct control. This is why Bank decisions often feel central to the economy while still being only one part of macroeconomic management.

How Bank Rate Works

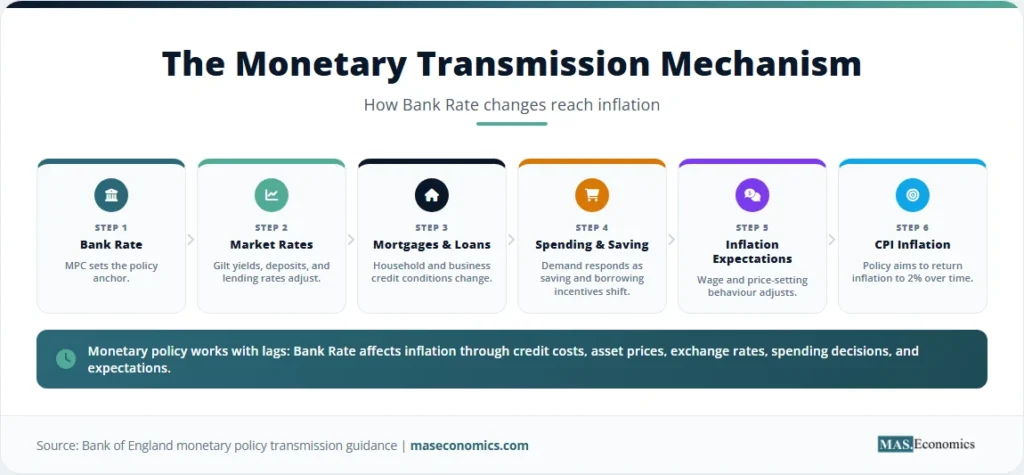

Bank Rate is the operational centre of UK monetary policy. When the Bank changes Bank Rate, it changes the return paid on reserves and influences short-term market rates. Commercial banks, building societies, investors, pension funds, and other financial institutions then reprice loans, deposits, bonds, derivatives, and exchange-rate expectations. The transmission mechanism is broad.

The first channel is the borrowing-cost channel. Higher Bank Rate normally raises mortgage rates, consumer-loan rates, and business borrowing costs. This reduces demand by making borrowing more expensive and saving more attractive. Lower Bank Rate normally does the opposite. It supports demand by reducing the cost of credit and lowering the reward for holding safe cash-like assets.

The second channel is the exchange-rate channel. Higher interest rates can support sterling by making UK assets more attractive relative to foreign assets. A stronger pound can reduce import-price inflation. A weaker pound can raise import costs but may support exporters. This channel connects the Bank to the open-economy logic discussed in the Mundell-Fleming model and the exchange-rate adjustment issues behind the J-curve effect.

The third channel is the expectations channel. If households, workers, firms, and markets believe the Bank will keep inflation near 2%, wage-setting and price-setting behaviour become more stable. If credibility weakens, inflation expectations can drift. That makes inflation harder to control because firms raise prices pre-emptively and workers demand higher wages to protect real incomes.

The fourth channel is the asset-price channel. Interest rates affect bond prices, equity valuations, commercial property values, and housing prices. When discount rates rise, the present value of future cash flows falls. This is why monetary policy can reshape financial conditions even before households and firms change spending. Articles such as Yield Curve Explained and Bond Duration and Convexity help explain why bond markets react so quickly to central-bank signals.

The fifth channel is the bank-lending channel. Banks adjust credit supply depending on funding costs, capital positions, deposit competition, loan demand, and expected defaults. A higher policy rate can reduce loan growth even when official credit rationing does not exist. This channel became especially important after the global financial crisis and during later stress episodes.

Bank Rate is not the Bank’s only tool. The Bank has also used asset purchases, commonly called quantitative easing, to lower long-term interest rates and support market functioning. It later began unwinding parts of its balance sheet through quantitative tightening. These tools connect to quantitative easing, quantitative tightening, and the wider question of central bank balance sheets.

| Tool or function | Main body | Economic purpose | Transmission channel |

|---|---|---|---|

| Bank Rate | Monetary Policy Committee | Return inflation to the 2% target over the medium term. | Borrowing costs, saving returns, sterling, expectations, and asset prices. |

| Quantitative easing | Bank and MPC | Support monetary conditions and market functioning when rates are near lower limits or markets are stressed. | Gilt yields, portfolio rebalancing, liquidity, and financial-market confidence. |

| Quantitative tightening | Bank and MPC | Reduce the stock of assets purchased under earlier QE programmes. | Balance-sheet size, gilt-market supply, term premia, and reserve conditions. |

| Financial-stability policy | Financial Policy Committee | Identify and reduce systemic risks to the UK financial system. | Capital buffers, mortgage-market rules, leverage limits, and risk warnings. |

| Prudential supervision | Prudential Regulation Authority | Promote the safety and soundness of banks, insurers, and major financial firms. | Capital requirements, liquidity standards, stress testing, and supervisory action. |

| Lender of last resort | Bank of England | Provide liquidity to solvent institutions or markets during exceptional stress. | Emergency liquidity, collateral operations, and confidence support. |

| Banknotes and payments | Bank of England | Maintain confidence in money and core payment infrastructure. | Currency issuance, settlement systems, payment resilience, and trust. |

|

|||

The Inflation Targeting Framework

The UK inflation-targeting framework is simple in design and complex in practice. The government sets a 2% CPI inflation target. The Bank’s MPC sets policy to meet that target over the medium term. The word “medium term” matters because monetary policy cannot offset every short-run price movement immediately. Energy prices, food prices, taxes, exchange-rate movements, and global supply shocks can push inflation away from target before the Bank Rate has time to affect demand.

The Bank, therefore, focuses on persistence. A one-time rise in energy prices is not the same as a wage-price spiral. A temporary import-price shock is not the same as broad domestic inflation pressure. The MPC studies pay growth, services inflation, labour-market slack, inflation expectations, corporate margins, fiscal policy, and global prices to judge whether inflation will return to target or remain stuck above it.

The UK inflation shock after 2021 tested this framework. Global supply constraints, energy prices, labour-market tightness, fiscal support, and post-pandemic demand shifts pushed inflation far above target. The Bank raised Bank Rate sharply from the pandemic floor of 0.1% to a peak of 5.25% in 2023. Later, as inflation cooled but did not disappear, policy moved into a more difficult phase: deciding how quickly to ease without reigniting inflation.

The April 2026 decision shows that dilemma. The Bank’s April 2026 Monetary Policy Report stated that the MPC voted 8–1 to maintain Bank Rate at 3.75%. The report also placed the decision inside a global environment affected by energy and commodity-price uncertainty. The policy message was not that inflation was solved. It was that the MPC would adjust policy as needed to return inflation sustainably to the target.

Inflation targeting has benefits. It gives households and firms a clear nominal anchor. It allows financial markets to form expectations around a known objective. It helps separate monetary policy from short-term political cycles. It also allows public accountability because outcomes can be compared with the target.

The framework also has limits. A 2% target does not tell the MPC exactly how fast to move rates after a shock. It does not solve supply problems. It does not identify the neutral interest rate with certainty. It does not prevent forecasting errors. And it does not remove distributional effects. Higher rates may be necessary for inflation control, but they also raise mortgage payments and debt-service costs. Lower rates may support demand, but they can raise asset prices and risk-taking.

Crisis‑Driven Institutional Change

The Bank of England’s credibility has been shaped by repeated crises. Each episode changed what the Bank was expected to do. The nineteenth-century banking panics strengthened the lender-of-last-resort role. The gold standard collapsed, and sterling crises exposed the limits of fixed exchange-rate discipline. The inflation of the 1970s pushed the UK toward modern monetary rules. The global financial crisis reshaped the Bank’s financial-stability responsibilities.

The 2007–2009 crisis was a major institutional turning point. Northern Rock exposed weaknesses in the UK’s pre-crisis regulatory structure. Liquidity stress, wholesale funding dependence, and bank fragility forced emergency interventions. After the crisis, the UK reorganised financial regulation. The Bank regained a central role in bank supervision through the Prudential Regulation Authority and macroprudential oversight through the Financial Policy Committee.

The Financial Policy Committee identifies, monitors, and acts to reduce systemic risks. Its work is separate from the MPC’s inflation objective, but the two are connected. A central bank that ignores financial fragility can lose monetary control during a crisis. A central bank that ignores inflation can damage financial stability through unstable expectations and distorted pricing.

COVID-19 created another test. The Bank cut rates, supported market functioning, and used asset purchases during a severe economic shock. The aim was not simply to lower borrowing costs. It was also to prevent financial dysfunction from turning a health shock into a deeper financial crisis. This was monetary policy and market-stability policy operating together.

The 2022 gilt-market stress was a different kind of episode. A sharp rise in gilt yields exposed vulnerabilities in liability-driven investment strategies used by pension funds. The Bank intervened temporarily to restore market functioning. The episode showed that financial stability can be threatened outside the banking system and that central banks must understand non-bank finance, collateral calls, leverage, and market liquidity.

The Bank’s more recent challenge has been credibility after the inflation surge. Like other central banks, it faced criticism for underestimating inflation persistence. The House of Lords Economic Affairs Committee and the externally led Bernanke review raised questions about forecasting, communication, governance, and internal challenge. These debates do not remove the case for independence. They point to the need for better institutional learning inside an independent framework.

The chart shows the Bank’s recent policy cycle in condensed form. The pandemic period placed the Bank Rate near zero. The inflation surge required rapid tightening. The 2026 setting reflects a restrictive but lower stance than the 2023 peak. This path also shows why monetary policy lags matter: the full effect of rate changes arrives after the decision has already been made.

Independence and Accountability

Central bank independence is not the same as isolation. The Bank of England operates within a democratic framework. Parliament created its powers. The government sets the inflation target. The Chancellor appoints external MPC members. The Governor and senior officials appear before parliamentary committees. The Bank publishes minutes, reports, speeches, and balance-sheet information.

Independence refers mainly to operational freedom. The MPC chooses the policy rate needed to meet the target. Ministers do not vote on Bank Rate. This arrangement reduces the temptation to keep interest rates too low before elections or to use monetary policy to hide fiscal problems. The economic logic is direct: inflation control requires credibility, and credibility depends on the public believing that policy will not be bent to short-term political needs.

Accountability is the other side of independence. The Bank must explain its decisions, its forecasts, its errors, and its judgment. If inflation is far above target, the Bank cannot simply blame external shocks. It must explain why the policy is appropriate and how inflation will return to the target. If unemployment rises or growth weakens, the Bank must explain why the inflation objective still requires its chosen stance.

The forecasting debate after the inflation surge made this tension visible. Forecasting is not a technical appendix to monetary policy. It is central to how the MPC chooses rates. If models underestimate inflation persistence, policy may be too loose for too long. If models overstate persistence, policy may remain too tight and damage output unnecessarily. The Bank’s institutional challenge is therefore not only to forecast better, but to allow disagreement, scenario analysis, and judgment to challenge model outputs.

Communication has become a policy tool in its own right. Speeches, minutes, vote splits, press conferences, and forecast paths all influence expectations. Markets do not wait for rate changes alone. They react to the words around the decision. This makes clarity important. A central bank that speaks too vaguely can confuse markets. A central bank that speaks too rigidly can trap itself if the data change.

Future Reform Challenges

The Bank of England’s future challenges fall into four broad areas: inflation credibility, financial stability, balance-sheet management, and institutional legitimacy.

The first challenge is inflation credibility in a supply-shock world. Energy shocks, food shocks, shipping disruption, geopolitical conflict, climate-related price movements, and trade fragmentation can all push inflation away from target. Monetary policy cannot produce gas, unload ships, or build houses. Yet if supply shocks feed wages and expectations, the Bank must respond. The hard judgment is deciding when a price shock is temporary and when it has become persistent domestic inflation.

The second challenge is financial stability outside the banking system. The 2008 crisis centred on banks. Later stress episodes showed risks in pension funds, hedge funds, money markets, gilt markets, and non-bank finance. The Bank’s lender-of-last-resort function increasingly has to consider markets as well as institutions. That raises difficult questions about moral hazard, collateral, eligibility, and the boundary between liquidity support and fiscal risk.

The third challenge is the balance sheet. Quantitative easing expanded central-bank balance sheets across the world. Quantitative tightening reduces them, but the process affects gilt markets, bank reserves, remittances to the Treasury, and public perceptions of central-bank losses. The Bank must manage its balance sheet in a way that supports monetary control without appearing to finance government deficits or disrupt market functioning.

The fourth challenge is public legitimacy. Central banks became more visible after the financial crisis, the pandemic, and the inflation surge. Their decisions affect mortgages, rents, savings, wages, pensions, public finances, and asset prices. That visibility raises political pressure. Independence survives only when the public sees the institution as competent, transparent, and accountable.

The Bank also faces the challenge of digital money and payment innovation. Central bank digital currency, stablecoins, tokenised deposits, faster payments, and private settlement systems can change the structure of money. The Bank must protect monetary stability while allowing innovation. The MASEconomics article on CBDCs vs. stablecoins explains why this debate is no longer theoretical.

Climate risk is another long-term issue. The Bank does not set climate policy, but it must assess financial risks from physical damage, transition costs, stranded assets, insurance losses, and energy-market volatility. This links directly to debates about central banks and climate change. The key institutional question is where financial-risk analysis ends and political allocation begins.

For the UK, the Bank’s future role will remain tied to the wider economic structure. A low-productivity economy with high public debt and expensive housing places more pressure on monetary policy. If supply-side reforms raise productivity and investment, the Bank can focus more narrowly on inflation and financial stability. If structural weakness persists, every rate decision will carry heavier political and social weight.

MASEconomics Explains

4 economic concepts behind the Bank of England

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Bank of England explained is the story of how Britain’s central bank connects inflation targeting, Bank Rate, financial stability, and institutional credibility. The Bank began as the government’s banker in 1694 and became a modern independent central bank after the reforms of 1997 and the Bank of England Act 1998. Its Monetary Policy Committee sets Bank Rate to return inflation to the 2% target, while the wider institution supports financial stability through supervision, market operations, and lender-of-last-resort functions. The Bank’s credibility depends on independence, transparency, accurate judgement, and public accountability.

Frequently Asked Questions

What does the Bank of England do?

The Bank of England is the central bank of the United Kingdom. It sets monetary policy, issues banknotes, supports financial stability, supervises major financial firms through the Prudential Regulation Authority, operates payment infrastructure, and can provide liquidity during financial stress. Its most visible task is keeping inflation close to the government’s 2% target.

Who sets interest rates in the UK?

Interest rates are set by the Bank of England’s Monetary Policy Committee. The MPC has nine members, and each member has one vote. The committee meets eight times a year to decide Bank Rate based on inflation, growth, wages, labour-market conditions, financial markets, and the outlook for the UK economy.

What is Bank Rate in simple terms?

Bank Rate is the main interest rate set by the Bank of England. It influences the rates charged on mortgages, loans, business credit, savings accounts, and market interest rates. When Bank Rate rises, borrowing usually becomes more expensive and demand weakens. When Bank Rate falls, borrowing usually becomes cheaper and demand receives support.

Why does the Bank of England target 2% inflation?

The 2% inflation target gives the UK economy a clear price-stability anchor. Inflation that is too high reduces purchasing power and makes planning difficult. Inflation that is too low can increase the risk of weak demand and deflation. A symmetric 2% target gives the Bank a benchmark for keeping inflation low, stable, and predictable.

Is the Bank of England independent?

The Bank of England has operational independence over monetary policy. The government sets the inflation target, but the Monetary Policy Committee decides how to use Bank Rate to meet that target. The Bank remains accountable to Parliament through published minutes, reports, hearings, speeches, and public explanations of its decisions.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics