When eurozone inflation peaked above 10 percent in October 2022, and US CPI inflation reached 9.1 percent that June, central bankers and journalists reached almost reflexively for a single phrase from the 1970s: the wage-price spiral. The fear was specific. If workers demanded higher wages to recover lost purchasing power, and firms passed those higher labor costs into prices, and households then demanded yet higher wages in response, inflation would feed on itself and become embedded in expectations. By 2024, the spiral had failed to materialize in any sustained way. Headline inflation in the United States and the euro area fell sharply while unemployment stayed near historic lows. The puzzle is not whether the 2022 inflation surge resembled the 1970s. The more interesting question is why two episodes that looked superficially similar produced such different wage-price dynamics, and what that tells us about how inflation actually propagates.

Defining the Wage-Price Spiral

A wage-price spiral describes a self-reinforcing loop between nominal wage growth and price inflation. The mechanism has three components: an initial inflationary impulse, a wage response that at least partly compensates workers for lost real income, and a firm response that passes higher labor costs through to prices. When the loop closes, the second-round wage demand exceeds the first, expectations of further inflation become entrenched, and inflation persists well beyond the original shock.

The textbook version sits inside an expectations-augmented Phillips curve. Nominal wage growth depends on expected inflation, the tightness of the labor market, and any catch-up term for past purchasing-power losses. Price inflation depends on unit labor costs, markups, and supply shocks. Formally, a simplified two-equation system is often written as:

Wage inflation \( \pi^{w}_{t} \) responds to expected price inflation \( \pi^{e}_{t} \), labor-market slack \( (u^{*} – u_{t}) \), and a catch-up term \( \gamma \) on lagged real-wage erosion. Price inflation \( \pi_{t} \) tracks unit labor costs net of productivity growth \( g_{t} \), plus a markup or supply-shock term \( \mu_{t} \).

The spiral becomes self-sustaining when \( \gamma \) is large, when expected inflation responds quickly to realized inflation, and when productivity growth fails to absorb unit-cost pressure. If any of those channels weakens, the loop is interrupted. This is why the formal Friedman-Phelps argument matters. As Friedman and Phelps showed, a stable inflation-unemployment trade-off requires fixed inflation expectations. Once expectations adjust, the trade-off shifts, and the only way to prevent the spiral from accelerating is to anchor expectations directly.

1970s Spiral Episode

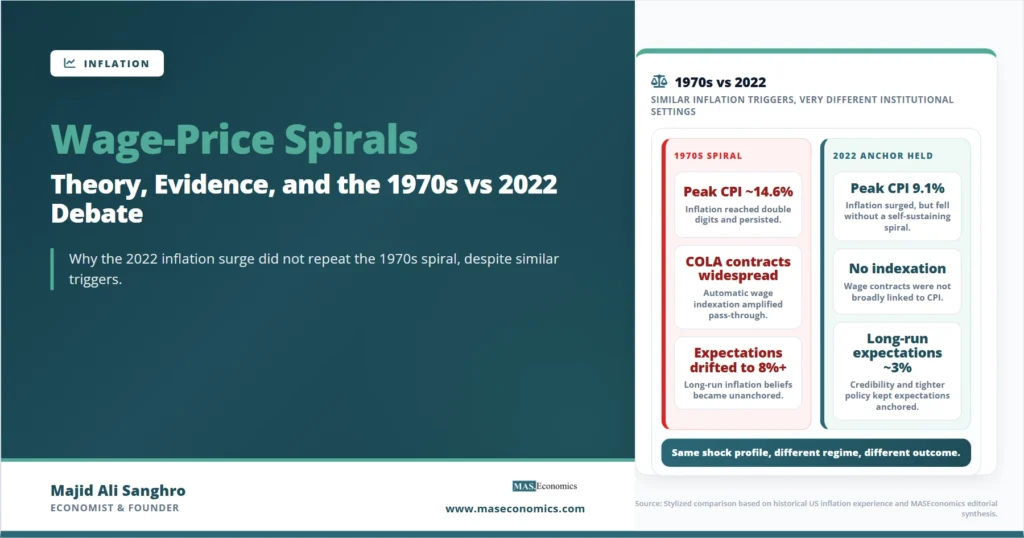

The 1970s episode supplied the visual evidence behind the term. Two oil shocks, in 1973–1974 and 1979–1980, raised import costs sharply for energy-importing economies. Inflation rose, real wages fell, and unionized workforces in the United States, the United Kingdom, France, Italy, and Germany pushed for compensating wage increases. In several countries, those increases were partly automatic. Cost-of-living adjustment (COLA) clauses tied wage growth directly to past CPI inflation. Italy’s scala mobile, introduced in 1975, indexed wages to prices on a quarterly basis. Many US union contracts in manufacturing and transport had COLA provisions through the early 1980s. The institutional architecture made \( \gamma \) close to one.

At the same time, productivity growth was decelerating. Labor productivity in the US business sector, which had grown at roughly 2.8 percent per year in the 1960s, slowed to about 1.4 percent per year from 1973 to 1979, according to Bureau of Labor Statistics productivity data. Unit labor costs rose mechanically, firms raised prices, and the loop closed. Inflation expectations, measured by the University of Michigan survey, drifted above 8 percent by 1980 and showed little response to short-term changes in oil prices. Once expectations had drifted that far, only an unambiguous policy regime change could bring them back. That change arrived as the Volcker disinflation. The associated cost was the recession of 1981–1982, the highest US unemployment rate since 1940, and a sacrifice ratio that remains a reference point in stagflation discussions.

2022 Episode Without Spiral

The 2022 inflation surge had a similar trigger profile. A pandemic-driven goods-sector demand boom collided with constrained supply chains; the Russian invasion of Ukraine pushed European natural gas prices to roughly ten times their 2019 average and global food commodity prices to record highs. Headline CPI inflation reached levels not seen since the early 1980s in most advanced economies. As the 2022–23 global inflation surge showed, the proximate causes leaned heavily on energy and goods prices rather than on wages.

The wage response was real but bounded. Nominal wage growth in the US, measured by the Atlanta Fed’s Wage Growth Tracker, peaked at 6.7 percent in mid-2022 before easing to roughly 4 percent by late 2024. In the euro area, negotiated wages rose by around 4 to 5 percent at peak. Both numbers were unusually high by post-1990 standards, but in real terms, wages still fell during 2022 in most economies. The catch-up was partial, not full, and it largely stopped once headline inflation began to decline.

Two empirical studies have become the reference points for this debate. In an IMF working paper, Alvarez, Bluedorn, Hansen, Huang, Pugacheva, and Sollaci (2022) identified 79 episodes since 1960 in advanced economies where rising inflation coincided with rising nominal wage growth and falling real wages. The authors found that in the majority of those episodes, inflation and nominal wage growth both fell over the following quarters; only a small minority produced sustained spirals. The historical base rate of wage-price spirals, conditional on the necessary preconditions, is low. The 2022 episode was consistent with the typical historical pattern rather than the spiral exception.

The second key piece of evidence comes from an NBER working paper by Bernanke and Blanchard (2023), who decomposed pandemic-era inflation in the United States and ten other economies into shocks to product prices, labor markets, and expectations. They found that the surge was overwhelmingly driven by product-market shocks, particularly energy and food, with a smaller contribution from a tight labor market. Wage-driven inflation entered late and modestly. The decomposition implied that as energy and supply-chain shocks faded, headline inflation would fall regardless of wage behavior, which is largely what happened during 2023 and 2024.

Structural Differences 1970s vs 2022

The structural changes between the two episodes are not subtle. The first is labor-market institutions. Cost-of-living adjustments in private-sector contracts have largely disappeared in the United States since the mid-1980s. Italy abolished the scala mobile in 1992. Union density in the OECD has roughly halved since 1980, from around 33 percent to about 16 percent by 2022, according to OECD data. The mechanical pass-through term \( \gamma \) is much smaller now than it was then. Workers may still demand wage increases, but those increases are negotiated less collectively and less synchronously, which slows the loop.

The second is the monetary regime. The Federal Reserve in 1972 had no formal inflation target, an uncertain commitment to price stability, and a leadership that explicitly weighed unemployment heavily. The 2022 Federal Reserve, in contrast, raised the federal funds rate by 525 basis points between March 2022 and July 2023, the fastest tightening since the early 1980s. The European Central Bank and the Bank of England moved in the same direction. As inflation expectations data from the New York Fed Survey of Consumer Expectations and the University of Michigan survey showed, long-run expectations remained close to 3 percent throughout the episode, even as one-year expectations briefly exceeded 6 percent. The credibility of the inflation-targeting framework absorbed the shock that the pre-1979 framework could not.

The third is product-market structure. The 1970s spiral mechanism relied on stable markups and high unit-labor-cost pass-through in goods-producing industries. The 2022 inflation episode was concentrated in goods and energy initially, and then shifted into services. Service-price inflation has stickier wage sensitivity, but it also has slower diffusion. The greedflation debate over whether markups were the leading edge of inflation, rather than wages, is a related but separate question. The most plausible reading is that 2022 saw a temporary markup expansion in goods that reversed as supply chains normalized, while wages were responding to, not driving, the shock.

| Feature | 1973–1981 (US, advanced economies) | 2021–2024 (US, advanced economies) |

|---|---|---|

| Peak CPI inflation (US) | ~14.6% (March 1980) | 9.1% (June 2022) |

| Trigger | Two oil shocks; loose monetary stance | Pandemic supply chains; energy shock; reopening demand |

| Wage indexation | Widespread COLA clauses; Italian scala mobile | Largely absent in private contracts |

| Union density (OECD avg) | ~33% (1980) | ~16% (2022) |

| Long-run inflation expectations | Drifted to 8%+ by 1980 | Anchored near 3% throughout |

| Productivity growth | Decelerating (1.4% post-1973) | Variable; modest pickup post-2023 |

| Monetary policy regime | Implicit target; late tightening | Formal 2% target; rapid 525 bp tightening |

| Outcome | Persistent inflation; 1981–82 recession | Disinflation without recession by mid-2024 |

|

Source: BLS CPI; OECD Trade Union Database; BLS Productivity; Federal Reserve H.15; Alvarez et al. (2022) IMF WP; Bernanke and Blanchard (2023) NBER WP 31417. Vintages as of late 2024.

|

||

Wage-Price Dynamics in the Data

The stylized claim that wages chase prices, or prices chase wages, hides the underlying dynamics. In both episodes, real wages fell during the inflation surge. In the 1970s, nominal wages eventually outran prices on a sustained basis because the institutional architecture forced them to, even when productivity could not justify the increases. In 2022, nominal wages rose substantially but lagged behind headline inflation for most of the surge. By 2024, with headline CPI down and nominal wage growth still around 4 percent, real wages began rising again, but the cumulative real-wage shortfall from the 2021–2022 period had not been recovered.

Lessons from the 2022 Episode

Three lessons emerge from the comparison. First, the necessary preconditions for a sustained wage-price spiral are quite specific: widespread wage indexation, weak nominal anchors, decelerating productivity, and a slow monetary response. The 2022 episode satisfied at most one of these, and arguably none in their 1970s form. The absence of a spiral was not luck; it followed from the institutional and policy architecture that had been built precisely to prevent it.

Definition. A wage-price spiral is a sustained mutual feedback between wage growth and price inflation. A single round of wage catch-up after a price shock is not a spiral; it becomes one only if expectations re-anchor higher and the catch-up term keeps growing.

Second, expectations are doing more of the work than the textbook decomposition suggests. The flat Phillips Curve of the pre-pandemic decade, and the steeper one that briefly reappeared in 2021–2022, are both consistent with anchored expectations in the long run. The New Keynesian formulation makes this explicit: current inflation depends not only on the current output gap and marginal costs but also on expected future inflation. When the expectations term is firmly anchored at the target, even sharp transitory shocks do not produce sustained inflation. The 2022 anchor held; the 1970s anchor had already failed by the time the first oil shock hit.

Third, the policy implication runs through credibility rather than through wage policy directly. Incomes policies, statutory wage restraint, and prices-and-incomes pacts have a mixed historical record. What worked in the 1980s was the demonstration of monetary commitment, not wage controls. The same logic applies in 2022. The aggressive rate path of 2022–2023 was less about cooling the labor market in real time, given the lags in monetary policy, and more about confirming that the inflation target was a binding constraint on policy choices.

Explains

Three concepts that anchor the wage-price spiral debate.

Continue with related inflation theory and historical episodes.

Explore the MASEconomics BlogConclusion

The wage-price spiral remains a real theoretical possibility, but the empirical record shows it requires institutional and policy conditions that have largely been dismantled in advanced economies. The 1970s episode produced a sustained spiral because indexation, decelerating productivity, and an unanchored monetary regime aligned to make it happen. The 2022 episode did not produce one because indexation had been dismantled, central banks responded quickly and credibly, and long-run inflation expectations stayed anchored despite headline inflation that briefly resembled the worst years of the 1970s. Real wages fell, nominal wages rose, headline inflation declined, and the loop never closed.

The deeper conclusion is that wage-price dynamics are conditional on regime, not on shocks. The same trigger can produce very different outcomes depending on the institutional context in which it lands. Researchers and policymakers who watched 2022 expecting the 1970s were watching for the wrong pattern. The right question was always whether expectations would hold, and whether the framework had the credibility to make them hold. In this episode, the answer was yes.

Frequently Asked Questions

What is a wage-price spiral in simple terms?

It is a self-reinforcing loop in which higher prices push workers to demand higher wages, which raises firms’ costs and pushes prices higher again. The loop becomes a true spiral only when inflation expectations move up with it, so each round of wage and price increases is larger than the previous one.

Did the 2022 inflation surge cause a wage-price spiral?

No. Nominal wages rose, but they did not keep pace with headline inflation, and inflation fell before a sustained feedback loop could form. Studies by the IMF (Alvarez et al., 2022) and Bernanke and Blanchard (2023) found that product-market shocks, particularly energy and supply chains, drove most of the inflation, while wages played a secondary role.

Why was the 1970s different?

Three features lined up: widespread wage indexation (COLA clauses in the US, the scala mobile in Italy), decelerating productivity growth, and a monetary policy framework with no credible inflation anchor. Each round of catch-up wage demands fed into the next round of price increases, and expectations drifted higher until the Volcker disinflation broke the cycle.

What stops a wage-price spiral from forming?

Anchored long-run inflation expectations, the absence of automatic indexation in wage contracts, productivity growth that absorbs unit-cost pressure, and a credible central bank willing to tighten policy in response to inflation. When most of these are in place, even sharp transitory price shocks usually fade without becoming embedded.

Are real wages the same as nominal wages?

No. Nominal wages are the dollar amount workers receive. Real wages adjust that amount for inflation. In the 1970s and again in 2022, nominal wages rose while real wages fell because price inflation outran wage growth. Whether real wages recover later depends on whether wage growth exceeds inflation after the shock passes.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics