On April 7, 2026, the United States and Iran agreed to a two-week ceasefire, brokered by Pakistan, with Iran committing to reopen the Strait of Hormuz for safe passage. Within minutes, oil futures dropped 6%, and stock markets surged. The relief was palpable because for five weeks, the Iran war had sent energy prices soaring past $100 per barrel, threatening to reignite the very same inflationary pressures that had tormented the global economy since 2021.

But here is the uncomfortable question that the ceasefire does not answer: when oil prices fall, will consumer prices follow? Or will corporations quietly pocket the savings, keeping prices high while their input costs decline?

This is the question at the heart of the greedflation debate, one of the most contentious and politically charged economic arguments of the decade. “Greedflation” is the claim that a significant portion of the post-pandemic inflation surge was driven not by supply shortages or excess demand, but by corporations opportunistically expanding their profit margins under the cover of a global crisis. Critics call it populist nonsense. Proponents say the data is overwhelming. The truth, as economists have discovered, is more nuanced than either side admits.

What Is Greedflation?

Greedflation, a portmanteau of “greed” and “inflation,” refers to a situation where corporations raise prices by more than their increased costs justify, expanding profit margins during periods of high inflation. The term entered the mainstream economic vocabulary in 2022 and 2023 as consumer prices surged across the developed world, while corporate earnings reports simultaneously showed record or near-record profits.

In standard economic theory, inflation can be driven by several factors. Demand-pull inflation occurs when too much money chases too few goods. Cost-push inflation occurs when rising input costs (energy, raw materials, wages) force producers to raise prices. Monetary inflation occurs when excessive money supply growth devalues the currency. These are the categories you find in any economics textbook.

Greedflation represents something that traditional models handle poorly: the role of market power in the inflation process. When a small number of firms dominate a market, as is the case in many modern industries, from food processing to energy to shipping, they have the ability to set prices above competitive levels. During normal times, competitive pressure and consumer resistance limit this power. But during a crisis, when information asymmetry between firms and consumers is high and when consumers expect prices to rise anyway, firms may find an opportunity to expand margins without losing customers.

The economic mechanism works as follows. A supply shock, such as the pandemic-era shipping disruption or the 2022 Russian invasion of Ukraine, raises input costs for all firms. Firms pass these costs to consumers, which is normal and expected. But some firms raise prices by more than their costs have increased, capturing additional profit. Because every firm in the supply chain faces the same inflationary environment, consumers cannot easily distinguish between legitimate cost pass-through and opportunistic margin expansion. The crisis provides what economists call “cover” for price increases that would not have been tolerated in a stable price environment.

What the Research Actually Shows

The greedflation debate has produced a rich body of research from central banks, international institutions, and independent economists. The findings are neither as damning as progressive critics suggest nor as dismissive as corporate defenders claim.

The Case For: Profits Drove a Disproportionate Share of Inflation

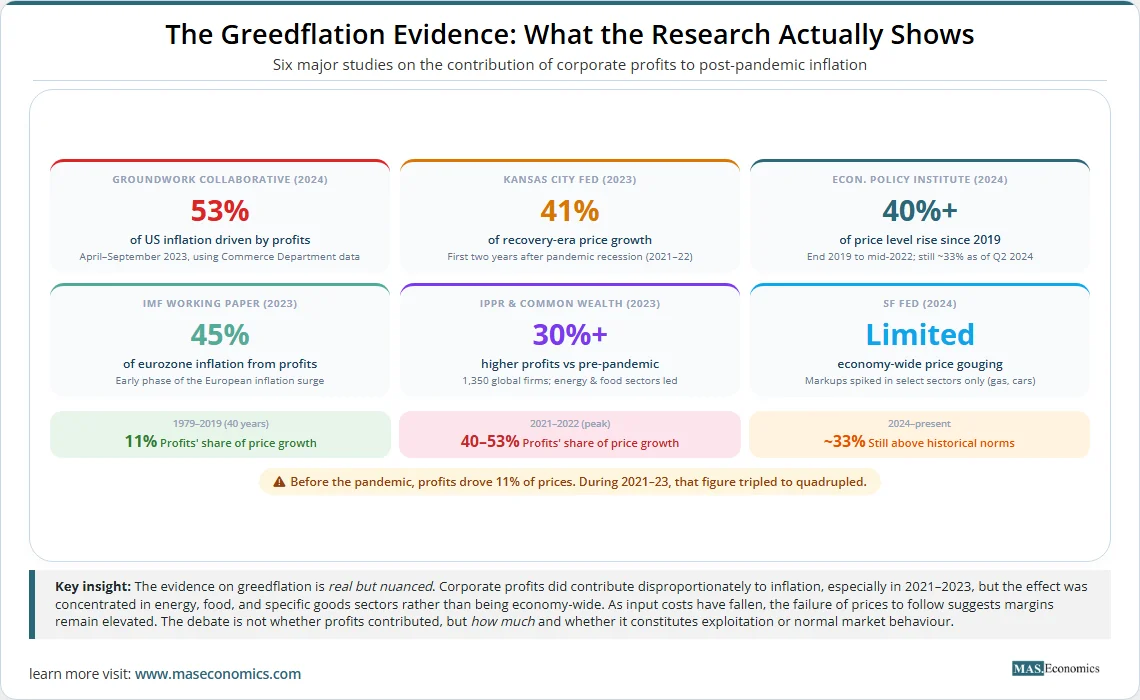

Multiple independent analyses have reached a broadly consistent conclusion: corporate profits contributed a significantly larger share of price increases during 2021 to 2023 than they did in any comparable period in modern history.

The Groundwork Collaborative, analyzing US Commerce Department data, found that corporate profits drove 53% of inflation during the second and third quarters of 2023 and more than one-third of all price increases since the start of the pandemic. In the four decades before the pandemic, profits accounted for just 11% of price growth.

The Federal Reserve Bank of Kansas City reached a similar conclusion from a different angle. Its 2023 research found that corporate profits contributed 41% of inflation during the first two years of the economic recovery following the pandemic recession. The Economic Policy Institute’s chief economist, Josh Bivens, found that rising profits explained more than 40% of the rise in the price level between end-2019 and mid-2022. Even as of mid-2024, profit growth still accounted for roughly a third of overall price increases, well above the long-run average of 11 to 12%.

In Europe, an IMF Working Paper found that approximately 45% of eurozone inflation in the early phase of the surge was attributable to profits. The ECB’s own analysis, published in its June 2023 Economic Bulletin, confirmed that unit profits had “grown strongly of late and made a visible contribution to domestic price pressures in the euro area.” ECB President Christine Lagarde explicitly warned of a “tit-for-tat” dynamic between profits and wages that could entrench inflation at higher levels.

A comprehensive study by the UK-based Institute for Public Policy Research (IPPR) and Common Wealth, which analyzed 1,350 large global companies listed on stock markets in the US, UK, Germany, Brazil, and South Africa, found that nominal profits averaged at least 30% higher at the end of 2022 than they were at the end of 2019. Energy companies such as ExxonMobil and Shell, along with food and commodities giants like Kraft Heinz and Archer-Daniels-Midland, led the surge.

The Case Against: Markets Worked As Expected

Not all research supports the greedflation narrative. A widely discussed paper from the Federal Reserve Bank of San Francisco, published in May 2024, found limited evidence that corporate price gouging was a primary catalyst for the economy-wide inflation surge of 2021 to 2022. The SF Fed researchers acknowledged that some companies exercised pricing power by raising prices above production costs in specific sectors, particularly gasoline, automobiles, and general merchandise. But when looking at markups across the entire economy, they found little evidence of systematic, broad-based price gouging.

Classical economists offer several counter-arguments. First, profit-seeking is the fundamental purpose of a firm, and higher profits during a period of strong demand and constrained supply are exactly what supply and demand theory predicts. Second, the Kansas City Fed noted that the 41% contribution of profits to recovery-era inflation was actually less than the historical average in prior economic recoveries, suggesting this is a normal cyclical pattern rather than unprecedented corporate behavior. Third, short-run profits often rise during inflationary periods as firms raise prices in anticipation of future cost increases, only to see margins compress later as wages and other costs catch up.

The US Chamber of Commerce’s chief policy officer, Neil Bradley, argued that rising profits during this period reflected sustained strong consumer demand rather than exploitation. “This is still a really strong economy from a consumer purchasing standpoint,” he noted, emphasizing that demand remained higher than pre-pandemic levels.

| Study / Source | Finding | Period Covered | Methodology |

|---|---|---|---|

| Groundwork Collaborative | Profits drove 53% of inflation | Q2-Q3 2023 | Commerce Department GDP deflator decomposition |

| Kansas City Fed | Profits contributed 41% of price growth | 2021-2022 | Unit profit decomposition of price level changes |

| Economic Policy Institute | Profits explained 40%+ of price level rise | End 2019 – mid 2022 | NIPA data analysis (BEA Table 1.14) |

| IMF Working Paper | ~45% of eurozone inflation from profits | Early inflation surge | GDP deflator decomposition (wages vs profits vs taxes) |

| IPPR / Common Wealth | Profits 30%+ higher than pre-pandemic | 2019-2022 | Financial statements of 1,350 listed firms globally |

| SF Federal Reserve | Limited economy-wide evidence of gouging | 2021-2022 | Cross-sector markup analysis using BLS and BEA data |

|

|||

The Asymmetric Price Stickiness Problem

Perhaps the strongest evidence for greedflation is not the initial price increases themselves, but what happened afterward. There is a well-documented phenomenon in economics called asymmetric price adjustment, sometimes called the “rockets and feathers” effect. Prices rise quickly when input costs increase but fall slowly, or not at all, when input costs decline.

This pattern has been stark in the post-pandemic period. US grocery prices rose by 23.5% between the end of 2019 and the start of 2024, according to Bloomberg data. Yet by mid-2024, wholesale food prices had stabilized, and many commodity prices had actually fallen. The gap between consumer prices and producer prices widened considerably, a pattern that the consumer price index captures but does not fully explain.

This is where the greedflation argument is most compelling. If prices rose because input costs rose, they should fall when input costs fall. The fact that they have not, at least not proportionally, suggests that something beyond pure cost pass-through is at work. That something, the greedflation argument holds, is the preservation of expanded profit margins.

Goldman Sachs analysts confirmed this dynamic in a March 2024 report, noting that corporate profit margins were expected to remain elevated despite input costs having declined by 3% over the prior 12 months. Companies, the analysts observed, are “typically slower to reduce their prices when costs decline than they are to raise prices when their expenses jump.”

This insight connects directly to the current moment. As the Strait of Hormuz reopens following the April 7 ceasefire and oil prices begin to retreat, the critical test for the greedflation thesis will be how quickly, or slowly, energy companies and downstream businesses pass those savings on to consumers.

Source: Economic Policy Institute analysis of BEA NIPA Table 1.14 data; Groundwork Collaborative (2024) | MASEconomics.com

The chart illustrates the central finding of the greedflation research. For four decades before the pandemic, corporate profits accounted for approximately 11% of price level changes, a stable, unremarkable baseline. During the pandemic recovery, this figure surged to between 40% and 53%, depending on the time period and study. While it has since moderated, it remains approximately three times the historical norm. This is the empirical core of the greedflation argument: something fundamentally changed in the relationship between corporate profits and prices during this inflation episode.

Why Market Structure Matters

The greedflation debate cannot be understood without examining market structure. The ability to raise prices above competitive levels depends on market power, and market power depends on how concentrated an industry is.

Many of the sectors where greedflation has been most evident, including energy, food processing, shipping, and meatpacking, are highly concentrated. In the US, four companies control approximately 85% of the beef processing market. Three shipping alliances control roughly 80% of global container shipping capacity. A handful of oil and gas majors dominate energy production and refining. In each of these industries, the small number of dominant firms means that competitive pressure, the mechanism that is supposed to prevent persistent margin expansion, is structurally weakened.

This connects to fundamental oligopoly theory. In a perfectly competitive market, firms are price-takers and cannot raise prices above marginal cost without losing all their customers. In an oligopoly, firms are price-makers to some degree, and they can sustain higher margins, particularly during periods of demand uncertainty or supply disruption when consumers are less price-sensitive.

The IPPR/Common Wealth study explicitly identified this dynamic, concluding that “because energy and food prices feed so significantly into costs across all sectors of the wider economy, this exacerbated the initial price shock, contributing to inflation peaking higher and lasting longer than had there been less market power.”

The 2026 Oil Shock

The Iran war and its disruption of the Strait of Hormuz have created what may be the most informative natural experiment for testing the greedflation hypothesis. Oil prices surged above $100 per barrel during the five-week conflict, pushing up energy costs, transportation costs, and food prices across the global economy. Central banks were forced to pause their rate-cutting plans, and consumers faced rising fuel and utility bills.

The April 7 ceasefire, which includes Iran’s agreement to allow safe passage through the Strait of Hormuz during a two-week negotiation period, with formal talks set for April 10 in Islamabad, has already triggered a sharp decline in oil futures. Financial markets reacted with immediate relief, with S&P 500 futures rising more than 1% and oil prices dropping roughly 6% in the hours following the announcement.

If the ceasefire holds and leads to a lasting peace agreement, the greedflation test is straightforward: how quickly will consumer prices fall to reflect lower energy costs? If gasoline prices at the pump, electricity bills, and transportation surcharges decline rapidly to pre-conflict levels, it suggests that the recent price increases were genuine cost pass-through. If they remain elevated long after wholesale costs have declined, it suggests that firms are once again using a crisis as cover for margin expansion.

This is the same dynamic that played out after the 2022 Russian invasion of Ukraine. Oil prices spiked, consumer prices rose, and then oil prices fell substantially, but many consumer prices remained stubbornly high. Energy price shocks have a well-documented asymmetric transmission: they flow downstream quickly when costs rise but slowly when costs fall.

There is reason for cautious optimism that this episode may unfold differently. Public awareness of greedflation is far higher now than it was in 2022. Regulatory attention has intensified, with competition authorities in both the US and EU increasing scrutiny of pricing practices in concentrated industries. And consumers, fatigued by years of rising prices, are showing greater willingness to switch brands and reduce spending, which the data on declining sales volumes at many consumer-facing companies confirms.

How Greedflation Fits Into the Broader Inflation Framework

For students of economics, the greedflation debate raises important theoretical questions about how inflation is modeled and understood.

Standard macroeconomic models treat inflation primarily as a monetary and demand-side phenomenon. The Phillips Curve framework attributes inflation to labor market tightness and expectations. The quantity theory of money attributes it to excessive money supply growth. The IS-LM model treats the price level as determined by the interaction of aggregate demand and money market equilibrium. None of these frameworks has a natural place for the behavior of firms as an independent driver of inflation.

Greedflation introduces what some economists call a “sellers’ inflation” channel, a concept developed in a 2023 working paper by Isabella Weber and Evan Wasner at the University of Massachusetts Amherst. Weber and Wasner argue that in an economy with significant market concentration, firms in upstream sectors (energy, food, shipping) can use a supply shock as an “impulse” that triggers a cascade of price increases throughout the supply chain. Each firm along the chain raises prices in response to the upstream increase, but each adds a margin on top of the cost pass-through, amplifying the original shock.

This “sellers’ inflation” model helps explain why the post-pandemic inflation was both more severe and more persistent than standard models predicted. It also explains why inflation targeting through interest rate increases was slower to work than expected: monetary policy operates primarily on the demand side, but if a significant portion of inflation is driven by margin expansion on the supply side, rate increases may suppress demand without addressing the root cause.

What Can Governments Do About Greedflation?

If greedflation is a real phenomenon, the policy response requires tools beyond traditional monetary policy. Several approaches have been proposed or implemented.

Competition enforcement. Strengthening antitrust enforcement to reduce market concentration could limit firms’ ability to raise prices above competitive levels. The Biden administration took steps in this direction in the US, and the European Commission has intensified merger scrutiny. However, structural market reforms take years or decades to produce results.

Price transparency. Requiring firms to disclose their cost structures and margin changes during inflationary periods could reduce the information asymmetry that enables greedflation. This approach has been adopted in some European countries for energy pricing.

Windfall profit taxes. The EU and UK implemented windfall profit taxes on energy companies in 2022 and 2023, capturing some of the extraordinary profits generated during the energy crisis. While politically popular, economists debate whether such taxes discourage investment or merely redistribute excess profits.

Consumer protection. Regulators in several countries have targeted “shrinkflation,” the practice of reducing product size while maintaining the same price, as a form of hidden price increase. France now requires supermarkets to label products that have been downsized, making the practice more transparent to consumers.

Why This Debate Matters Now More Than Ever

The greedflation debate is not an abstract academic exercise. It has direct consequences for how policymakers respond to the current economic situation.

If the post-Iran-war inflation is primarily driven by genuine supply disruptions, then monetary policy should respond cautiously, holding rates steady until the supply shock passes. This is essentially what the Federal Reserve, ECB, and Bank of England did at their March 2026 meetings.

But if a significant portion of the price increases involves margin expansion by firms with market power, then holding rates steady may not be enough. It may actually make things worse, because higher interest rates suppress demand and employment while leaving the profit-driven component of inflation untouched. In this scenario, competition policy, transparency requirements, and consumer protection measures become essential complements to monetary policy.

The ceasefire and the prospect of Islamabad peace talks offer the global economy an opportunity to step back from the brink. If oil prices stabilize and the Strait of Hormuz returns to full operation, the inflationary impulse from the conflict should dissipate. But whether consumers actually see lower prices at the pump, in grocery stores, and on utility bills will depend on whether corporations pass their savings through, or whether they treat the crisis, like the last one, as an opportunity to lock in higher margins.

MASEconomics Explains

Four economic concepts at the heart of the greedflation debate

Greedflation

A term describing the phenomenon where corporations raise prices by more than their increased costs justify, expanding profit margins during periods of high inflation. Research shows profits contributed 40-53% of US price increases during 2021-2023, compared to a 40-year average of just 11%.

Market Power

The ability of a firm to set prices above the competitive level without losing all its customers. Market power increases with industry concentration and is the structural prerequisite for greedflation. Firms in highly concentrated sectors (energy, food processing, shipping) showed the largest margin expansions during the inflation surge.

Asymmetric Price Adjustment

The empirical observation that prices rise rapidly when input costs increase (“rockets”) but fall slowly when input costs decrease (“feathers”). This asymmetry is a key indicator of greedflation: if prices were purely cost-driven, they would adjust symmetrically in both directions.

Sellers’ Inflation

A theoretical framework proposed by Isabella Weber where firms with market power use supply shocks as cover to raise prices beyond cost pass-through, triggering a cascade of price increases through the supply chain. Unlike demand-pull inflation, sellers’ inflation cannot be effectively addressed by interest rate increases alone.

Key Takeaway and Conclusion

The greedflation debate reveals a gap in how mainstream economics understands inflation. For decades, inflation theory focused almost exclusively on monetary aggregates, labor markets, and demand conditions. The post-pandemic inflation episode has forced a reckoning with the supply side of the equation, specifically with the role that corporate pricing power, market concentration, and strategic margin expansion play in amplifying and prolonging price shocks.

The evidence is clear that corporate profits contributed a disproportionate share of inflation during 2021 to 2023, far exceeding the historical norm. The evidence is also clear that this effect was concentrated in specific sectors, particularly energy, food, and shipping, rather than being uniformly distributed across the economy. The debate is not about whether profits contributed, but about how much of that contribution reflects normal market dynamics versus exploitative pricing behavior.

For consumers navigating the aftermath of the Iran war oil shock, the practical lesson is simple: watch whether prices come down as fast as they went up. History suggests they will not, at least not without pressure from competition, regulation, and informed consumer choices. For policymakers, the lesson is that monetary policy alone is an incomplete tool for fighting inflation when market power is a significant contributor to price pressures.

The coming weeks will provide a real-time answer. With the Strait of Hormuz reopening and peace talks beginning in Islamabad on April 10, the supply-side impulse behind the latest inflation scare should begin to fade. The question is whether firms will follow the supply-side logic all the way down, or stop halfway, as they did before.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.