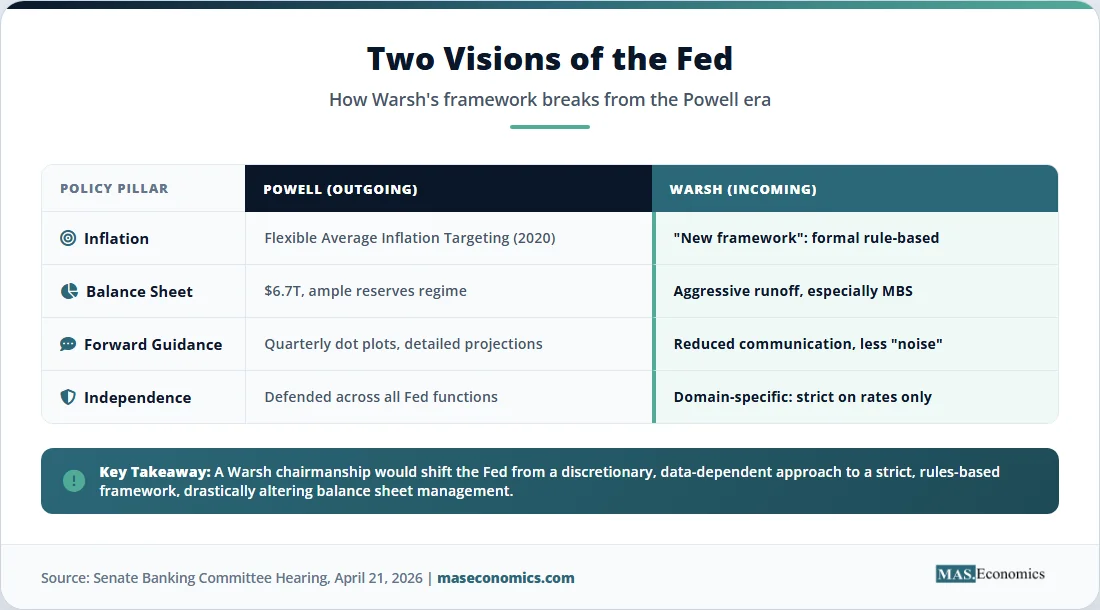

The Senate Banking Committee voted 13 to 11 along party lines on April 29, 2026, to advance Kevin Warsh Federal Reserve nomination to the full Senate, clearing the most consequential procedural hurdle in the path to replace Jerome Powell as the next chair of the United States central bank. Powell’s four-year term as chair expires on May 15. The full Senate vote is scheduled for the week of May 11, and with Republicans holding the majority, confirmation is widely viewed as a near certainty.

The committee vote was the first fully partisan endorsement of a Fed chair nominee in the panel’s history, according to Senator Elizabeth Warren of Massachusetts. The break with bipartisan tradition reflects the unusual circumstances of the transition: a Department of Justice criminal investigation into Powell that paused only days before the vote, a sitting president who has openly demanded lower interest rates, and a nominee whose monetary philosophy diverges sharply from the Powell-era playbook.

What follows is a complete picture of who Warsh is, what he believes, how the Fed chair selection process works, and what his confirmation would mean for interest rates, the Fed’s balance sheet, and the broader US economy.

The Numbers That Define the Moment

Three numbers anchor the transition. The Fed’s balance sheet stands at roughly $6.7 trillion as of late April 2026, down from a pandemic peak near $9 trillion but still nearly eight times its pre-2008 level. The federal funds rate sits in a target range of 3.50 to 3.75 percent, where Powell’s FOMC held it on April 29 in what is likely his final rate decision as chair. And the Fed’s preferred inflation measure has run above the 2 percent target for several years, leaving the incoming chair with an inheritance of unfinished disinflation.

Warsh, 56, is no stranger to the institution. He served on the Federal Reserve Board of Governors from 2006 to 2011, becoming the youngest governor in history at the time of his appointment by President George W. Bush. He resigned in February 2011 after publicly dissenting against the second round of quantitative easing. His return to Washington as the prospective chair would close a fifteen-year arc that began with one of the most aggressive monetary expansions in modern history and would now place him in charge of unwinding what remains of it.

How the Nomination Reached This Point

The path to the chairmanship was not smooth. President Donald Trump named Warsh as his nominee in January 2026 after an internal contest that, according to Treasury Secretary Scott Bessent, included Kevin Hassett, Christopher Waller, Michelle Bowman, and the BlackRock executive Rick Rieder. Trump told reporters in January that he preferred Hassett to remain at the National Economic Council, clearing the way for Warsh.

The nomination collided almost immediately with a politically charged DOJ investigation into Powell over cost overruns on the Fed’s headquarters renovation. Powell, in a January statement, accused the administration of targeting him over the Fed’s refusal to cut rates as aggressively as Trump demanded. Republican Senator Thom Tillis of North Carolina vowed to block any Trump Fed nominee until the probe was withdrawn. A federal judge dismissed several grand jury subpoenas in March. By late April, with the DOJ effectively standing down, Tillis dropped his hold and called Warsh an “outstanding nominee” at the April 21 confirmation hearing.

That hearing produced a striking moment. Warsh told the committee he would be “strictly independent” as chair, rejecting the Democratic charge that he would serve as a “sock puppet” for the White House. He also called for “a regime change in the conduct of policy” and a new “inflation framework,” signaling a deliberate break with the Powell era. The committee vote followed eight days later.

Timeline of the Transition

| Date | Event | Significance |

|---|---|---|

| January 2026 | Trump nominates Warsh | Selection follows interviews with Hassett, Waller, Bowman, Rieder. |

| January 2026 | DOJ probe into Powell announced | Tillis vows to block any Fed nominee until investigation closes. |

| March 2026 | Federal judge dismisses subpoenas | Effectively halts the criminal investigation into Powell. |

| April 21, 2026 | Senate Banking Committee hearing | Warsh pledges independence; calls for new inflation framework. |

| April 29, 2026 | Committee votes 13-11 | First fully partisan committee vote in Fed history. |

| April 29, 2026 | Powell holds rates at 3.50–3.75% | Likely his final rate decision as chair. |

| Week of May 11 | Full Senate confirmation vote | Simple majority required; Republicans hold the Senate. |

| May 15, 2026 | Powell’s term as chair expires | Powell remains on the Board as governor. |

|

||

Who Is Kevin Warsh

Born in Albany, New York, in 1970, Warsh graduated from Stanford with a degree in public policy and earned his law degree at Harvard. He spent seven years at Morgan Stanley as a mergers and acquisitions banker, rising to vice president before joining the Bush White House in 2002 as special assistant to the president for economic policy and executive secretary of the National Economic Council. In that role, he handled the administration’s response to corporate accounting scandals, including the negotiations around the Sarbanes-Oxley Act.

His 2006 nomination to the Fed Board surprised many observers. At 35, he had no formal economics doctorate and limited monetary policy experience. The Bush administration argued that his Wall Street background would complement Ben Bernanke’s academic expertise. The Senate Banking Committee advanced him 20 to 0 and confirmed him by voice vote, a contrast that economists at Fortune and elsewhere have noted highlights how dramatically the politics of Fed appointments have shifted.

Inside the Bernanke Fed, Warsh became a critical conduit to Wall Street during the 2008 panic. He was deeply involved in the Bear Stearns rescue and the negotiations with foreign central banks that produced the dollar swap line system. After the immediate crisis passed, he grew increasingly uneasy with the unconventional tools the Fed had adopted. His November 2010 dissent over the second round of asset purchases, known as QE2, was rooted in concern that monetary expansion of that scale blurred the line between fiscal and monetary authority. He left the Board in February 2011.

The intervening fifteen years have been spent at Stanford’s Hoover Institution, on corporate boards, and in active commentary on monetary policy. His public writings and speeches consistently return to a small set of themes: rules over discretion, a smaller central bank balance sheet, and a clearer separation between the Fed’s monetary mandate and its other functions.

The Economic Vision Warsh Brings to the Chair

Warsh’s monetary philosophy can be summarized in three interlocking commitments. First, a preference for rules-based monetary policy over the discretionary, data-dependent approach that has dominated US central banking since the 1990s. He has called the Fed’s existing framework one of “permanent improvisation” and has cited the Taylor rule and nominal GDP targeting as serious alternatives.

Second, a deep skepticism of the Fed’s expanded balance sheet. At the April 21 hearing, Warsh told senators that “the Fed balance sheet has played a particularly, I think, unhelpful role in helping the Fed achieve its dual mandate.” He has argued elsewhere that a large central bank ledger blurs the line between monetary and fiscal authorities and is “why the Fed is in the business of politics.” He intends to shrink the balance sheet, though at the hearing, he was careful to add that any unwinding “took decades to build” and would require “time, patience, and care.”

Third, a redefinition of central bank independence. Warsh has described Fed independence as varying by domain: at its peak in the conduct of monetary policy, lower in international finance and other areas where, in his phrasing, “Fed officials are not entitled to the same special deference.” He has proposed what he calls a new “Fed/Treasury accord” to govern the balance sheet, an idea he has yet to detail publicly. Six former Fed officials interviewed by CNBC in early May described his comments as unclear at best and worrisome at worst, with one anonymous senior official warning that “if followed to its logical conclusion, the Fed could lose control of its balance sheet.”

Some observers have noted a softening relative to his 2010 stance. Brian Levitt, an Invesco strategist, wrote after the April hearing that Warsh’s tone is “increasingly dovish compared to his first go-round at the Fed,” with a more nuanced view of inflation in an environment shaped by tariffs and supply shocks. Whether that flexibility persists once he holds the gavel remains an open question.

How the Federal Reserve Chair Is Actually Selected

The selection process is set out in the Federal Reserve Act of 1913 and operates in four stages. Understanding the mechanics matters because the chair is not simply appointed: the role is layered into a broader Board structure with overlapping terms designed to insulate monetary policy from short-term political cycles.

Stage one: presidential nomination. The president selects a nominee from the seven members of the Board of Governors or, more rarely, names someone who is simultaneously nominated to the Board and elevated to chair. The chair serves a four-year renewable term. The president’s choice is constrained politically by Senate composition but legally constrained only by the requirement that the nominee be a current or incoming Board member.

Stage two: Senate Banking Committee review. The committee, currently chaired by Senator Tim Scott of South Carolina, conducts a financial and background review, holds public hearings, and submits written follow-up questions. The committee then votes to advance, hold, or reject the nomination. Warsh cleared this stage on April 29 with the narrowest possible Republican margin.

Stage three: full Senate vote. Confirmation requires a simple majority of senators present and voting, a threshold lowered from the previous 60-vote standard by the 2013 procedural changes that ended the filibuster for most executive branch nominations. Republicans currently hold the Senate, making confirmation arithmetic favorable for Warsh.

Stage four: oath of office and term structure. Once confirmed, the chair takes the oath and assumes leadership of the Board of Governors and, by virtue of the role, the chair of the Federal Open Market Committee. Here, a critical institutional nuance applies: the chair serves a four-year term, but Board members serve fourteen-year terms. Powell will remain on the Board as a governor after May 15, a fact already reshaping expectations of how the FOMC will function under Warsh.

Powell vs Warsh: Two Visions of the Fed

The contrast between the outgoing and incoming chairs is sharper than any transition since Paul Volcker handed the chairmanship to Alan Greenspan in 1987. Powell has presided over the most aggressive use of the Fed’s balance sheet in history, the adoption of flexible average inflation targeting in 2020, and the rapid tightening cycle that brought rates from zero to a 5.25-5.50 percent peak before the gradual cuts that began in 2024. Warsh has signaled a fundamental rewrite of the policy architecture.

The chart below traces the Fed’s balance sheet evolution and shows why Warsh’s critique has the force it does. The institutional ledger that was roughly $800 billion when he joined the Board in 2006 is now more than eight times that size, even after three years of quantitative tightening.

Source: Federal Reserve Board H.4.1 release, Congressional Research Service. Year-end values; 2026 figure reflects late-April level.

The visual makes Warsh’s argument concrete. The expansion is not the work of a single crisis. It is the cumulative effect of three rounds of QE between 2008 and 2014, the pandemic response of 2020-2022, and the slow grind of partial normalization since. For a chair who has called the Fed’s footprint a “fiscal” overreach, the asset side of the ledger is the policy battleground.

What Markets and the Economy Should Expect

Four channels will determine how a Warsh Fed differs from a Powell Fed. The first is the path of interest rate decisions. Warsh has rejected the suggestion that he will simply cut rates on Trump’s demand. At the hearing, he said plainly that “presidents want lower rates” but added that the decision belongs to the Fed. A rules-based reaction function would, by most readings of the Taylor rule, prescribe a slower path of cuts than Trump has demanded so long as inflation remains above 2 percent. The result is likely a “higher for longer” policy stance, with cuts conditional on clearer evidence of disinflation.

The second channel is the balance sheet. Markets have already begun pricing in the prospect of accelerated runoff. Mortgage-backed securities are the most exposed segment because Warsh has argued the Fed should not own them at all. A faster MBS runoff would lift mortgage rates relative to Treasuries, with knock-on effects for housing affordability. The Treasury market would face heavier supply absorption from private investors. Equity valuations, especially for long-duration growth stocks, would face a higher discount rate. The pace will matter more than the direction. Warsh has publicly committed to caution, and any FOMC majority for an aggressive unwind is far from assured.

The third channel is institutional. The functions of the Fed extend well beyond monetary policy: bank supervision, payments infrastructure, currency swap lines with foreign central banks, and lender-of-last-resort facilities. Warsh’s proposed Fed-Treasury accord and his domain-specific view of independence raise the possibility that some of these functions could be reclassified or constrained. Treasury Secretary Bessent has publicly mentioned new swap line requests from Gulf states, including the United Arab Emirates. How a Warsh Fed responds will be the first concrete test of where independence ends, and Treasury coordination begins.

The fourth channel is credibility. Claudia Sahm, the former Fed economist who developed the Sahm rule recession indicator, told Fortune that the partisan committee vote suggests “this is not normal” will be a recurring theme of Warsh’s tenure. Long-term inflation expectations remained anchored through the April hearing, with the five-year breakeven barely moving. That is a vote of provisional confidence by markets. It is also conditional. If a Warsh Fed is perceived as bending to White House demands on rates, the resulting rise in inflation expectations would force higher rates regardless of FOMC intentions. The historical record on politically captured central banks is unambiguous and unflattering.

For the global economy, a Warsh Fed implies somewhat tighter US dollar conditions than the Trump administration would prefer. Dollar liquidity for emerging markets via swap lines could become more constrained or more conditional. Capital flows would respond to a higher real US interest rate. Countries with dollar-denominated debt would face renewed servicing pressure. The effect would be uneven: net commodity exporters and economies with strong reserve positions could absorb the shift, while frontier economies with thin dollar buffers would feel it more acutely.

MASEconomics Explains

Four economic concepts behind the Fed transition

Conclusion

The Kevin Warsh Federal Reserve nomination represents the most significant institutional transition at the US central bank in nearly two decades. Warsh enters the chairmanship with a clear policy agenda: rules-based monetary policy, a smaller balance sheet, and a redefined boundary between the Fed and the Treasury. His 13-11 committee vote, the first fully partisan endorsement in the panel’s history, reflects the political environment surrounding the appointment rather than the qualifications of the nominee. The full Senate is expected to confirm him in the week of May 11, before Powell’s term expires on May 15. Markets have so far granted the incoming chair the benefit of the doubt, with long-term inflation targeting credibility intact. Whether that confidence holds will depend on the policy choices Warsh makes in his first year and on the institutional resilience of central bank independence under sustained executive pressure. The next chapter of US monetary policy begins with a chair who has spent fifteen years arguing that the Fed grew too large, too political, and too discretionary. The economy is about to learn what he intends to do about it.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.