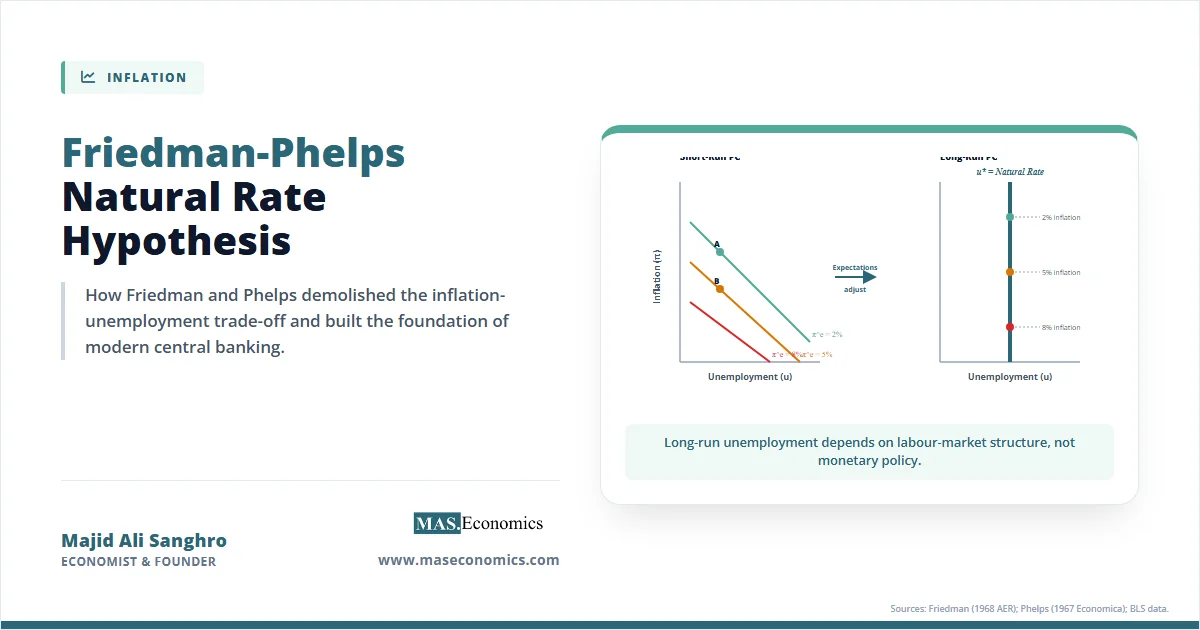

The natural rate hypothesis transformed macroeconomics by demonstrating that any attempt to push unemployment below its equilibrium level produces only temporary gains, because rational workers eventually adjust inflation expectations and the short-run Phillips curve shifts upward, yielding a vertical long-run Phillips curve. Before Milton Friedman and Edmund Phelps independently developed this framework, the Phillips curve appeared to offer policymakers a stable menu of inflation-unemployment combinations. The natural rate hypothesis destroyed that consensus and built the foundation for modern central banking.

The Logic Behind the Natural Rate

During the 1960s, the macroeconomic policy consensus rested on the observed inverse correlation between inflation and unemployment. Paul Samuelson and Robert Solow (1960) presented this relationship as a policy menu: society could choose lower unemployment at the cost of higher inflation, or lower inflation at the cost of higher unemployment. Keynesian economists believed fiscal and monetary policy could permanently steer the economy along this curve, selecting the optimal trade-off. The Kennedy and Johnson administrations explicitly relied on this logic. Walter Heller, Chairman of the Council of Economic Advisers under President Kennedy, advocated for tax cuts to push unemployment down to 4%, believing the economy could sustain this low rate with only moderate inflation. The economic establishment widely accepted that a stable, exploitable trade-off existed.

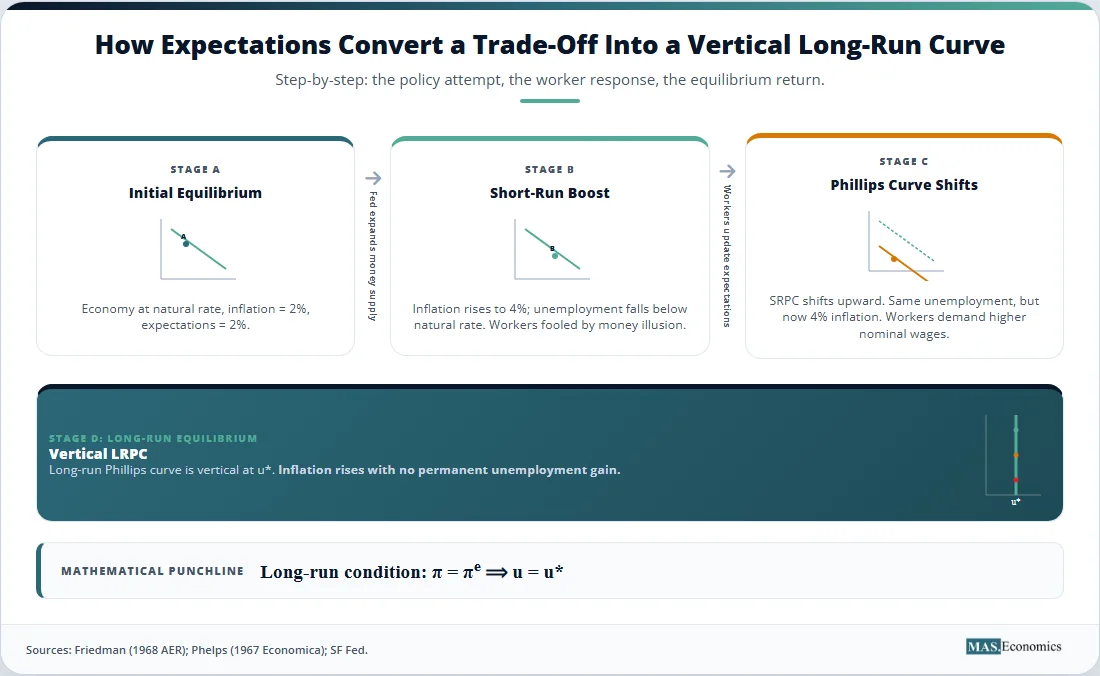

Milton Friedman challenged this consensus in his December 1967 Presidential Address to the American Economic Association, published in 1968. Edmund Phelps independently developed similar ideas in his 1967 Economica paper. Their core insight was simple but devastating: workers care about real wages, not nominal wages. When inflation rises unexpectedly, firms perceive higher prices for their output and demand more labour, while workers initially mistake rising nominal wages for rising real wages. Employment rises temporarily because of this money illusion.

Once workers realise that higher nominal wages simply match the higher cost of living, they adjust their inflation expectations upward. They demand even higher nominal wages to compensate for the erosion of their purchasing power. Firms, facing higher labour costs, reduce employment back to its original level. The economy returns to its previous unemployment rate, but with permanently higher inflation. The short-run Phillips curve shifts upward.

Any sustained attempt to hold unemployment below its natural rate requires constantly accelerating inflation. Policymakers must continually surprise workers with higher inflation than they expect. Because expectations eventually catch up to reality, the inflation rate must keep rising to create the nominal wage illusion that drives the employment boost. The long-run Phillips curve is vertical at the natural rate of unemployment, meaning monetary policy cannot permanently reduce unemployment below this structural level.

Natural Rate Hypothesis in Equations

The natural rate hypothesis formalises the distinction between short-run and long-run Phillips curves through the expectations-augmented Phillips curve.

Expectations-Augmented Phillips Curve

The baseline formulation incorporates expected inflation and the deviation of unemployment from its natural rate:

where \( \pi_t \) is actual inflation, \( \pi_t^e \) is expected inflation, \( u_t \) is the actual unemployment rate, \( u^* \) is the natural rate of unemployment, \( \alpha > 0 \) is the slope parameter governing the responsiveness of inflation to the unemployment gap, and \( \varepsilon_t \) represents cost-push supply shocks. The parameter \( \alpha \) captures the short-run trade-off: a larger \( \alpha \) means a steeper short-run Phillips curve, implying that a given reduction in unemployment produces a larger increase in inflation.

Long-Run Vertical Phillips Curve

The long-run condition occurs when expectations adjust fully to actual inflation. Setting \( \pi_t = \pi_t^e \) and assuming no supply shocks (\( \varepsilon_t = 0 \)), the equation reduces to:

Unemployment returns to its natural rate regardless of the inflation rate. The long-run Phillips curve is vertical at \( u^* \). The parameter \( \alpha \) governs the speed of adjustment but does not affect the long-run equilibrium. Whether inflation is 2% or 20%, unemployment converges to the natural rate once expectations fully adjust.

Adaptive Expectations Specification

Friedman (1968) modelled expectation formation using an adaptive process where workers update their beliefs based on past forecast errors:

The parameter \( \lambda \) governs the speed of learning. When \( \lambda = 1 \), expectations adjust fully in one period, meaning \( \pi_t^e = \pi_{t-1} \). Smaller values of \( \lambda \) imply slower adjustment, extending the period during which policymakers can exploit the short-run trade-off. The political economy implications are significant: politicians with short electoral horizons may be tempted to exploit the temporary trade-off, pushing unemployment down before an election and leaving the subsequent inflationary consequences to their successors. The adaptive specification implies that expectations eventually converge to reality, but the transition can be slow and costly.

Accelerationist Hypothesis

If a policymaker attempts to maintain unemployment permanently below the natural rate at \( \tilde{u} < u^* \), the adaptive expectations framework generates an accelerationist result. Substituting the policy target into the Phillips curve and iterating forward shows that the change in inflation is strictly positive:

Inflation must not only be high, but must constantly accelerate. Each period, the policymaker must generate inflation above the now-higher expected inflation to recreate the real wage gap that stimulates employment. This accelerationist property was the most policy-relevant implication of the natural rate hypothesis. It demonstrated that the long-run cost of targeting an unsustainably low unemployment rate is hyperinflation, not merely high inflation.

Rational Expectations Sharpening

Lucas (1972, 1973) replaced the adaptive mechanism with model-consistent rational expectations. Under rational expectations, agents use all available information, including knowledge of the policy rule, to form forecasts. The expectations-augmented Phillips curve becomes:

Only unanticipated inflation, the difference between actual inflation and rational expectations of inflation, moves unemployment away from the natural rate. Systematic monetary policy, which agents can anticipate, has no real effects. This rational expectations sharpening strengthened the natural rate hypothesis by showing that even the short-run trade-off exists only when policy surprises the public. The policy-ineffectiveness proposition of Sargent and Wallace (1975) emerged directly from this formulation: any announced, credible monetary policy affects only nominal variables, leaving real output and employment unchanged.

Key Assumptions and Limitations

The natural rate hypothesis rests on three core assumptions. First, the natural rate exists and is unique, determined by structural labour-market factors including demographics, search frictions, union density, and the generosity of unemployment insurance. Second, workers and firms care about real wages, not nominal wages, meaning they ultimately adjust their behaviour in response to changes in purchasing power. Third, expectations eventually catch up with reality, whether through adaptive learning or rational information processing.

Several important limitations challenge these assumptions. First, Friedman never wrote a formal mathematical model with all the properties he claimed in his 1968 address. As Forder (2010) and Tobin (1995) have documented, the original presentation was verbal and intuitive, leaving later economists to construct the formal apparatus. This lack of initial rigour has led to ongoing debates about what Friedman actually meant and whether the natural rate is a fixed point or a shifting zone.

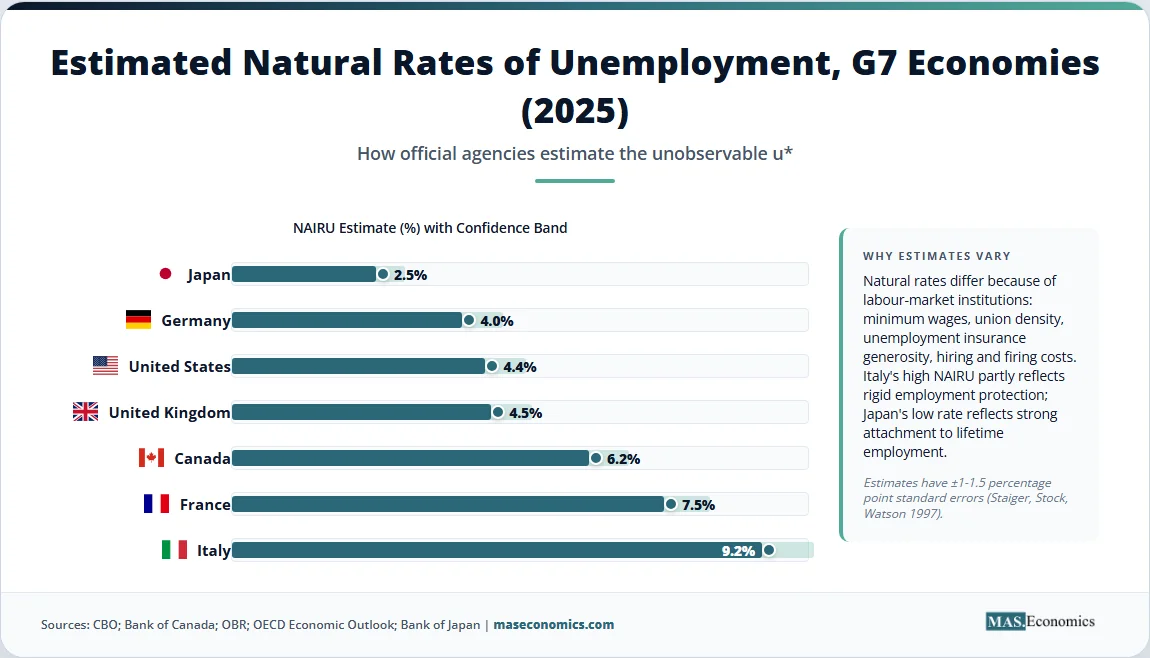

Second, the natural rate is unobservable and time-varying. Empirical estimates for the US natural rate range between 4% and 8%, depending on the sample period and methodology. The Congressional Budget Office regularly revises its estimates of \( u^* \), making real-time policy guidance uncertain. Orphanides (2001) demonstrated that the Federal Reserve’s policy errors in the 1970s stemmed partly from real-time mismeasurement of the natural rate; policymakers believed \( u^* \) was around 4-5%, when in reality demographic shifts and structural changes had pushed it closer to 6-7%. If policymakers cannot observe the natural rate, they cannot know whether unemployment is above or below it, rendering the policy prescription ambiguous.

Third, hysteresis, introduced by Blanchard and Summers (1986), challenges the assumption that the natural rate is determined solely by structural factors. Long unemployment spells erode workers’ skills and detach them from the labour market, raising \( u^* \) endogenously. A deep recession can permanently increase the natural rate, meaning that demand shocks have permanent supply-side effects. Under hysteresis, the long-run Phillips curve is not vertical, and expansionary policy can permanently reduce unemployment by reversing the labour market scarring caused by the recession.

Fourth, downward nominal wage rigidity may create a long-run trade-off at low inflation rates. Akerlof, Dickens, and Perry (1996) argued that firms are reluctant to cut nominal wages, creating inefficiencies at low inflation that prevent the labour market from clearing. Near-zero inflation may therefore be associated with persistently higher unemployment, violating the vertical long-run Phillips curve prediction. Their model of near-rational behaviour suggested that when inflation is very low, workers and firms do not pay close attention to aggregate price changes, meaning expectations adjust slowly and the short-run trade-off persists longer than the natural rate hypothesis predicts.

Empirical Evidence for the Natural Rate Hypothesis

The empirical validation of the natural rate hypothesis came primarily from the macroeconomic events of the 1970s, but its testing has evolved significantly over subsequent decades.

Friedman (1968) and Phelps (1967) developed the hypothesis theoretically before the supporting evidence emerged. Lucas (1973) provided international evidence showing that countries with more variable inflation had steeper Phillips curves, consistent with the rational expectations version of the hypothesis, where agents in high-inflation environments pay more attention to aggregate price changes. His analysis of data from eighteen countries demonstrated that the apparent trade-off vanished as inflation became more volatile, confirming that the short-run curve was not stable.

The Great Stagflation of the 1970s provided the most compelling empirical vindication. Between 1972 and 1980, US inflation rose from 3.4% to 13.5% while unemployment simultaneously rose from 5.6% to 7.1%. This positive co-movement of inflation and unemployment was impossible under the stable Phillips curve framework but was exactly what the natural rate hypothesis predicted: the short-run Phillips curve had shifted upward as expectations adjusted. The 1973 oil shock initiated the process, but the persistence of inflation throughout the decade reflected the expectations adjustment mechanism Friedman had described. The original Phillips curve could not account for stagflation; the expectations-augmented version explained it as the inevitable result of attempting to hold unemployment below the natural rate through monetary expansion.

Staiger, Stock, and Watson (1997) demonstrated the empirical difficulty of estimating the natural rate, which they operationalised as the NAIRU. Their analysis showed standard errors of roughly 1.5 percentage points around point estimates, meaning the true natural rate could plausibly be anywhere in a three-point range. This imprecision limits the hypothesis’s practical usefulness for real-time policymaking, a point emphasised by their JEP article.

Ball and Mankiw (2002) revisited the NAIRU framework, showing that supply shocks can shift the natural rate temporarily, complicating the relationship between inflation and unemployment. Their analysis showed that the natural rate is not a constant structural parameter but a moving target influenced by oil prices, productivity growth, and demographic shifts. Gordon’s triangle model of inflation similarly incorporated supply shocks, inertia, and demand pressure as separate drivers, offering a more flexible empirical framework than the simple expectations-augmented formulation.

Modern estimates place the US natural rate around 4.4% according to the Congressional Budget Office and the San Francisco Federal Reserve. Blanchard (2018) revisited the hypothesis in his Journal of Economic Perspectives article “Should We Reject the Natural Rate Hypothesis?”, concluding that while the evidence supports a flat but not strictly vertical long-run Phillips curve, the natural rate remains a useful organising concept. The flatness means that the long-run trade-off, if it exists, is sufficiently small that policymakers should still treat the curve as approximately vertical for practical purposes.

Sources: BLS CPI data; BLS unemployment series.

Sources: BLS CPI data; BLS unemployment series.

| Year | US Inflation (%) | US Unemployment (%) | Fed Funds Rate (%) | Episode |

|---|---|---|---|---|

| 1965 | 1.6 | 4.5 | 4.04 | Pre-shift baseline |

| 1972 | 3.4 | 5.6 | 4.43 | Late “stable” PC |

| 1975 | 9.1 | 8.5 | 5.82 | First oil shock |

| 1980 | 13.5 | 7.1 | 13.36 | Stagflation peak |

| 1982 | 6.1 | 9.7 | 12.26 | Volcker disinflation |

| 1986 | 1.9 | 7.0 | 6.81 | Expectations re-anchored |

|

||||

How the Natural Rate Hypothesis Matters

The natural rate hypothesis fundamentally altered the practice of macroeconomic policy. Its implications extend from the theoretical rejection of fine-tuning to the institutional design of modern central banks.

Before the natural rate hypothesis, Keynesian discretionary stabilisation policy aimed to fine-tune aggregate demand. Policymakers believed they could permanently keep unemployment low by accepting moderately higher inflation. The natural rate hypothesis ended this practice. If the long-run Phillips curve is vertical, demand stimulus produces only temporary employment gains and permanently higher inflation. The goal of monetary policy shifted from minimising unemployment to maintaining price stability, recognising that sustainable unemployment is determined by structural factors outside the central bank’s control. This shift represented the most profound change in macroeconomic policy thinking since the Keynesian revolution itself.

This theoretical shift motivated the birth of central bank independence. Friedman’s argument that monetary policy cannot reduce unemployment in the long run, but can cause inflation, provided the intellectual foundation for rules-based, inflation-targeting frameworks. The Reserve Bank of New Zealand adopted inflation targeting in 1990, followed by the Bank of Canada in 1991, the Bank of England in 1992, and the European Central Bank in 1998. These institutional reforms were direct descendants of the natural rate logic: if monetary policy cannot systematically improve real outcomes, its primary mandate should be price stability. Central bank independence insulated monetary policy from the political temptation to exploit the short-run trade-off for electoral gain.

Paul Volcker’s disinflation of 1979–1982 stands as the most dramatic policy embodiment of the natural rate hypothesis. Volcker raised the federal funds rate to nearly 20%, accepting a peak unemployment rate of 10.8% in 1982 to break the entrenched inflation expectations of the 1970s. The severe recession was the short-run cost of shifting the short-run Phillips curve back down. The sacrifice ratio, the cumulative loss in output and employment required to reduce inflation by one percentage point, was substantial. Once expectations re-anchored, inflation fell sharply while unemployment eventually returned to its natural rate. The Volcker episode demonstrated both the validity of the natural rate hypothesis and the high transition costs of correcting an expectations shift. It also proved that while the long-run Phillips curve is vertical, the path back to the natural rate after expectations have become unanchored is agonisingly slow.

The 2022–2024 Federal Reserve tightening cycle tested the natural rate hypothesis in a new context. Fed Chair Jerome Powell’s “soft landing” thesis held that the central bank could cool inflation without causing a severe recession, partly because the post-pandemic Beveridge curve had shifted outward. The debate centred on whether \( u^* \) had risen permanently due to labour market reallocation, or whether the natural rate remained near its pre-pandemic level. If \( u^* \) had risen, then low unemployment did not signal an overheating economy, and the Fed could ease policy sooner. If \( u^* \) was unchanged, persistent tight labour markets would eventually reignite inflation. Labour market data became the central focus of this debate. The post-COVID surge in job-to-job transitions and the rise of remote work suggested that matching efficiency in the labour market had changed, potentially altering the structural natural rate in ways that traditional estimates could not immediately capture.

Fiscal policy frameworks also rely on natural rate estimates. The CBO and the OECD use estimates of \( u^* \) to compute structural budget balances, distinguishing between cyclical deficits that will automatically correct as the economy returns to the natural rate and structural deficits that require policy changes. An inaccurate estimate of the natural rate leads to miscalibration of fiscal space. The same logic applies in the United Kingdom, Australia, and Canada, where fiscal rules depend on output gap estimates derived from natural rate calculations.

Hysteresis debates in Europe provide the strongest ongoing challenge. The Eurozone’s persistently high unemployment after the 2008 financial crisis, particularly in Greece, Spain, and Italy, suggested that the deep recession had raised the natural rate itself. Blanchard and Summers (1986) argued that prolonged unemployment destroys human capital and reduces labour force attachment, making the natural rate endogenous to the business cycle. Under hysteresis, expansionary policy might permanently reduce unemployment rather than merely creating inflation, invalidating the strict natural rate hypothesis. The European experience showed that prolonged demand shortfalls can create their own structural damage, turning cyclical unemployment into structural unemployment.

The Reserve Bank of Australia estimates the NAIRU at approximately 4.5%, using it as a key input in monetary policy decisions. When unemployment falls below this estimate, the RBA tightens policy to prevent inflation from accelerating. The Australian experience mirrors that of other advanced economies: the natural rate provides a discipline mechanism for policymakers, even if its exact value is uncertain.

The Nobel Prize committee recognised the importance of this framework. Friedman received the 1976 Nobel Prize partly for his natural rate work, and Phelps received the 2006 Nobel Prize for his analysis of intertemporal tradeoffs in macroeconomic policy. These awards confirmed the hypothesis as a cornerstone of modern macroeconomics.

Today, the natural rate hypothesis faces new challenges from political pressures on central bank independence. When politicians demand that central banks prioritise employment over price stability, they are implicitly rejecting the natural rate hypothesis and reviving the discredited idea that monetary policy can permanently reduce unemployment. The hypothesis remains the strongest theoretical defence against such political incursions, explaining why central banking institutions guard their independence so fiercely. The causes of inflation are deeply intertwined with these institutional structures, and the natural rate hypothesis clarifies why separating monetary policy from fiscal politics is essential for price stability.

MASEconomics Explains

4 economic concepts behind the natural rate hypothesis

Conclusion

The natural rate hypothesis converted the Phillips curve from a stable policy menu into a short-run-only relationship, establishing that monetary policy cannot permanently reduce unemployment below its structural equilibrium. The hypothesis predicted the 1970s stagflation that the original Phillips curve could not explain, motivated the global shift toward independent and inflation-targeting central banks, and provided the theoretical justification for the Volcker disinflation. While the natural rate remains unobservable and the hypothesis faces ongoing challenges from hysteresis evidence and post-pandemic labour-market shifts, its core insight endures: sustainable unemployment is determined by real structural factors, not by the central bank’s willingness to tolerate inflation.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.